Our early-2025 review found cloud AI revenue surging, non-AI demand recovering faster than expected, and compute capacity still in short supply.

This quarter, the three major cloud AI winners (AWS, GCP) and loser (Azure) were updated again. Amid severely supply-constrained AI compute demand, besides AI data center build-out speed, compute resource allocation (Microsoft's "strategic misstep") also determined cloud revenue growth rates. Oracle and Neocloud remain mired in debt and leverage skepticism, urgently needing rapid compute ramp to dispel market concerns.

1

Amazon AWS

Global Cloud Leader

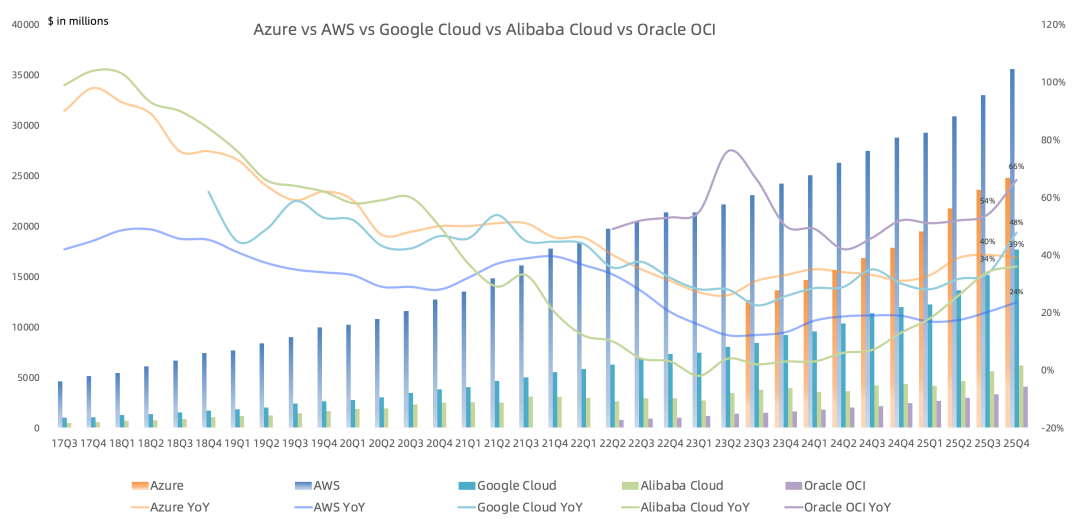

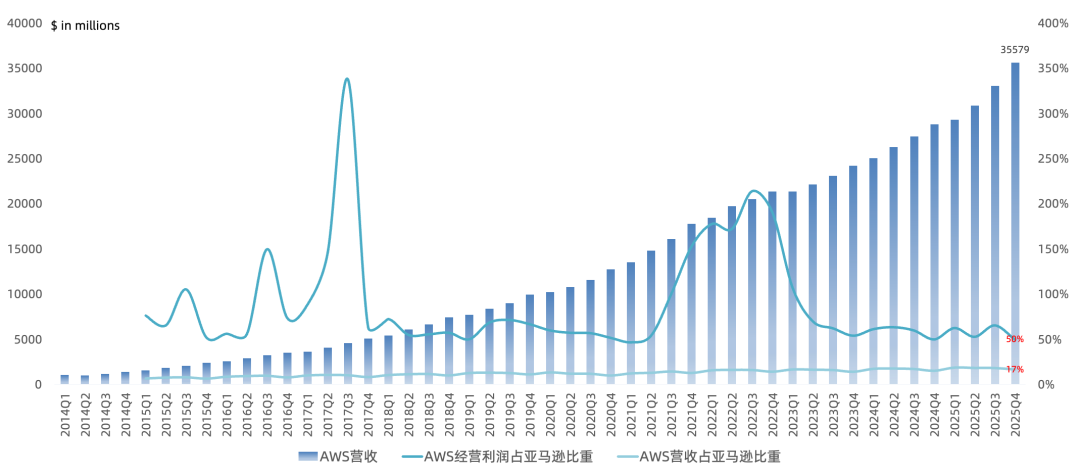

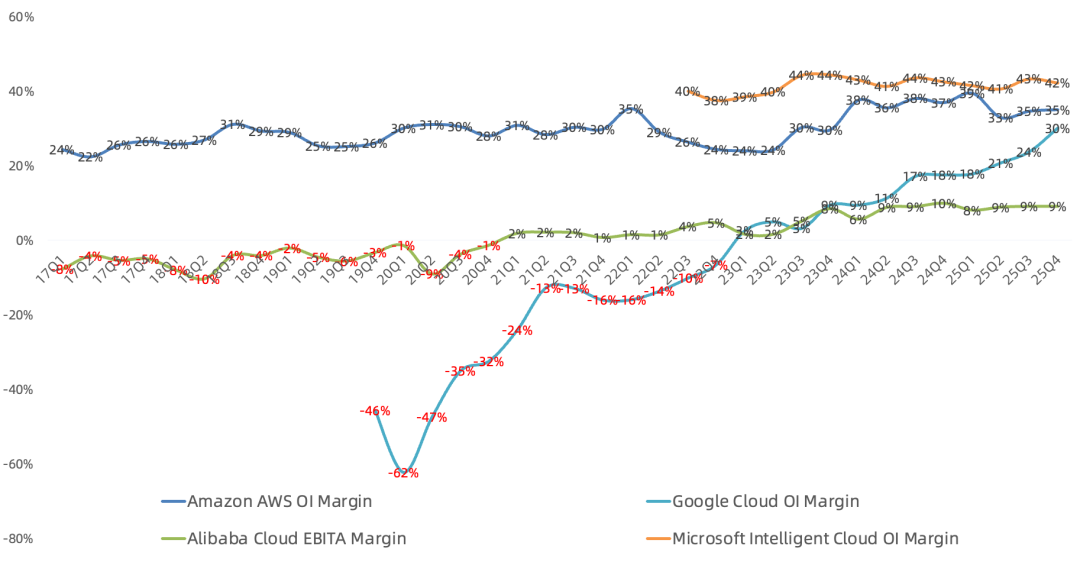

AWS Q4 revenue $35.6B, up 24% year over year, sequential growth acceleration of 4 percentage points, a 13-quarter high; sequential growth of 8%; operating income $12.5B, up 17% year over year, operating margin 35%, down 2 percentage points year over year.

AWS Q4 revenue accounted for 17% of Amazon total revenue, contributing 50% of Amazon operating income. AWS added 3.99 GW of power capacity in 2025, of which 1.2 GW in Q4 alone; expected to double again by 2027; chip business (Trainium, Graviton) combined annualized revenue run rate exceeds $10B, up triple digits year over year, with Graviton CPU annualized run rate revenue in the billions, up over 50% year over year; cumulative 1.4M Trainium2 chips deployed, pre-booked by customers and also used to power Bedrock inference; Project Rainier data center houses 500K Trainium2 chips for training Claude models; Trainium3 demand strong, nearly all Trainium3 capacity will be pre-booked by customers by mid-2026; Trainium4 to be delivered in 2027, 6x FP4 performance improvement over Trainium3; continued strong growth in core non-AI workloads, enterprises refocusing on migrating on-prem infrastructure to cloud, adding large amounts of EC2 compute capacity daily, the vast majority of which uses proprietary Graviton CPU chips; number of top 500 US startups using AWS as primary cloud provider exceeds Microsoft Azure and Google GCP combined; Bedrock annualized run rate revenue in the billions, customer spend up 60% sequentially; Amazon Connect annualized run rate revenue exceeds $1B, up 30% year over year, 20M+ daily interactions; developers using Kiro up over 150% sequentially.

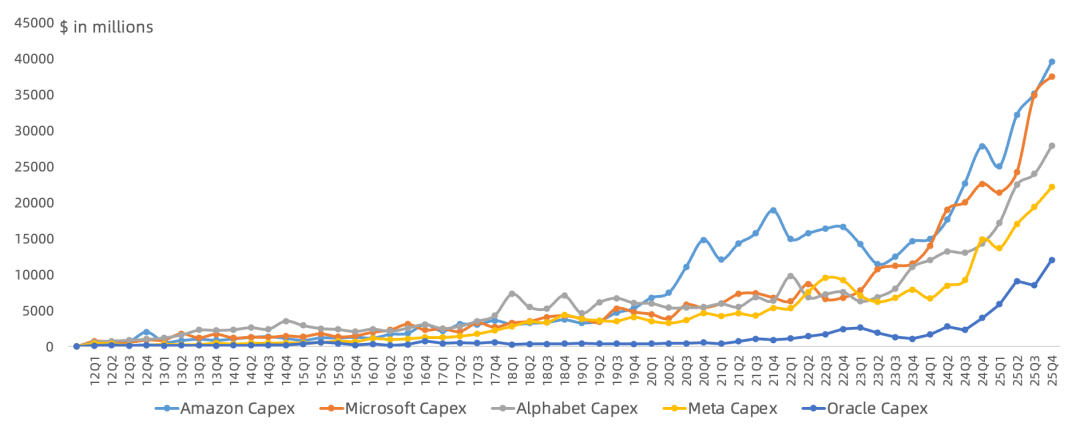

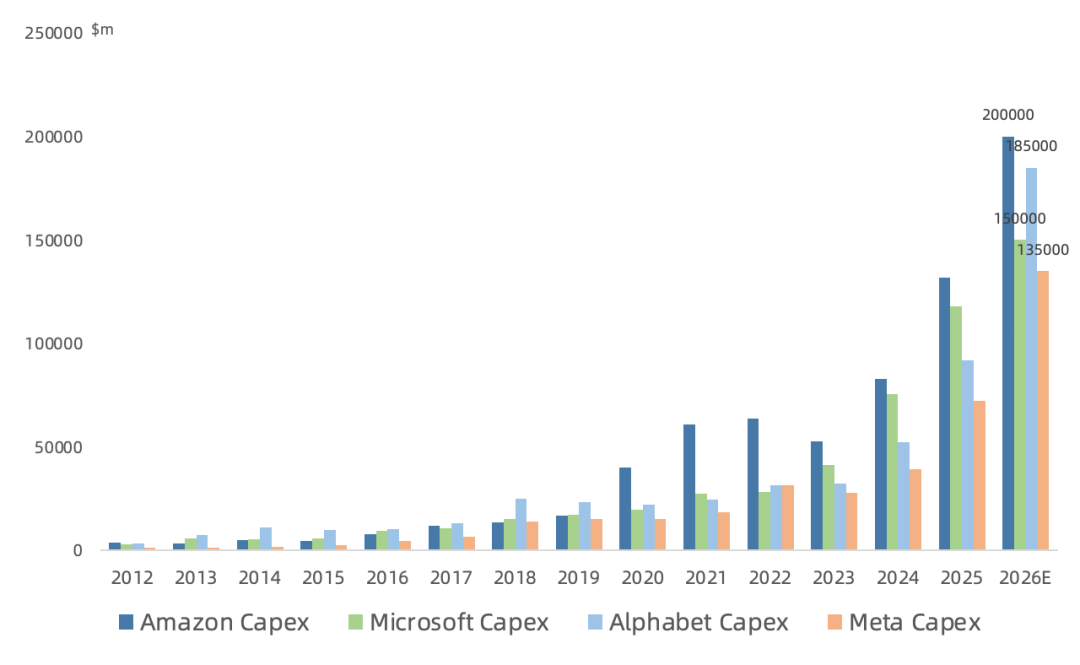

Amazon Q4 capex $39.5B, mostly into AI; the vast majority of AI capex and capacity is for external customers; 2026 capex guided at $200B, the vast majority directed to AWS, given very high AWS demand; will continue adding more compute in 2027 and 2028; management recently touted a ten-year goal of AWS annual revenue reaching $300B (double current levels).

2

Microsoft Azure

Second-Largest Global Cloud

Microsoft Azure Q4 revenue $24.8B, up 39% year over year, sequential growth deceleration of 1 percentage point, making it the only one of the three global hyperscalers with slowing growth.

Azure's Intelligent Cloud segment (Server + Azure + Enterprise Services) revenue $32.9B, up 29% year over year; Intelligent Cloud gross margin 58.8%, down 4.4 percentage points year over year, primarily due to depreciation; total operating income $13.9B, up 28% year over year, operating margin 42%; Intelligent Cloud Q4 revenue accounted for 41% of Microsoft total revenue, contributing 36% of Microsoft operating income.

Azure growth may fluctuate quarterly depending on capacity delivery and go-live timing; if newly online GPUs were allocated entirely to Azure, Azure growth would certainly exceed 40%, but the company must also serve high-margin M365, GitHub, or Dragon Copilot businesses, as well as its own R&D needs; added nearly 1 GW of total capacity in Q4 alone; announced data center investments in 7 countries this quarter to support local data residency requirements, offering the most comprehensive sovereign solutions across public, private, and national partner clouds; providing the broadest model selection among hyperscalers, with over 1,500 customers using both Anthropic and OpenAI models simultaneously on AI Foundry; continuing to invest in first-party models; customers spending over $1M per quarter on AI Foundry grew nearly 80%, with over 250 customers on track to process over 1 trillion tokens on Foundry this year; Microsoft's purchased GPUs are covered by long-term contracts signed with large customers before procurement, covering the full useful life, so investment is essentially collect-cash-before-buy-hardware, no risk of cost recovery; like the CPU era of cloud, margins will improve over time.

In Data & Analytics, Fabric revenue grew 60%, run rate revenue now exceeds $2B, with over 31K customers, and continues to be the fastest-growing analytics platform in the market; over 80% of Fortune 500 companies have active agents built with low-code/no-code tools Copilot Studio and Agent Builder; GitHub Copilot Pro+ subscriptions up 77% sequentially, 4.7M paid subscribers, up 75% year over year.

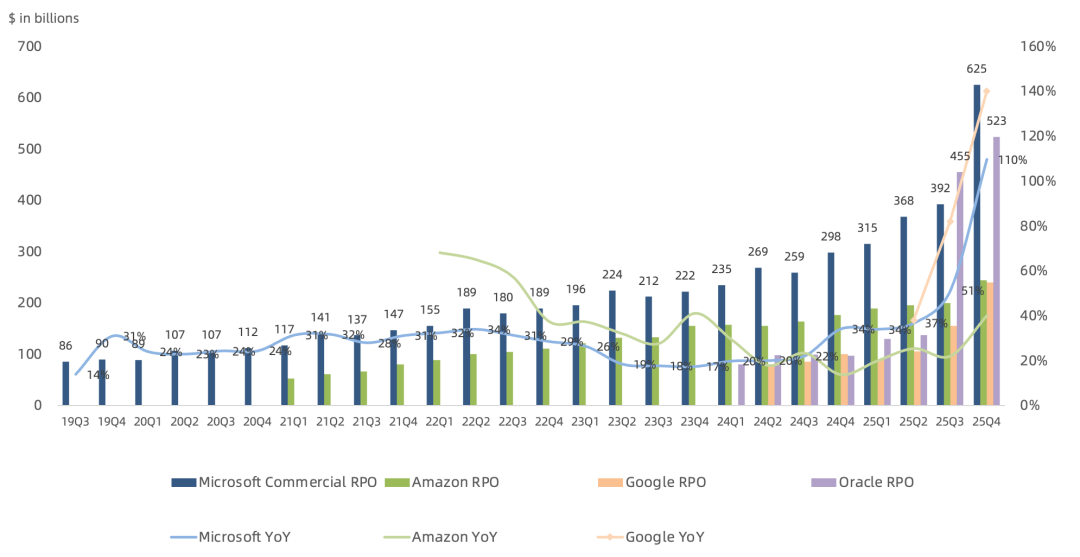

Commercial RPO this quarter $625B, up 110% year over year, of which 45% from OpenAI; ex-OpenAI customer RPO up 28% year over year, driven primarily by Anthropic, weighted average duration ~2.5 years; next quarter Azure revenue guided at 37%-38% year over year growth; Q4 capex $37.5B, 2/3 for short-lived assets, primarily GPUs and CPUs; next quarter capex guided down sequentially, mainly due to delivery timing changes; rising memory prices will impact capex.

3

Google Cloud

Third-Largest Global Cloud

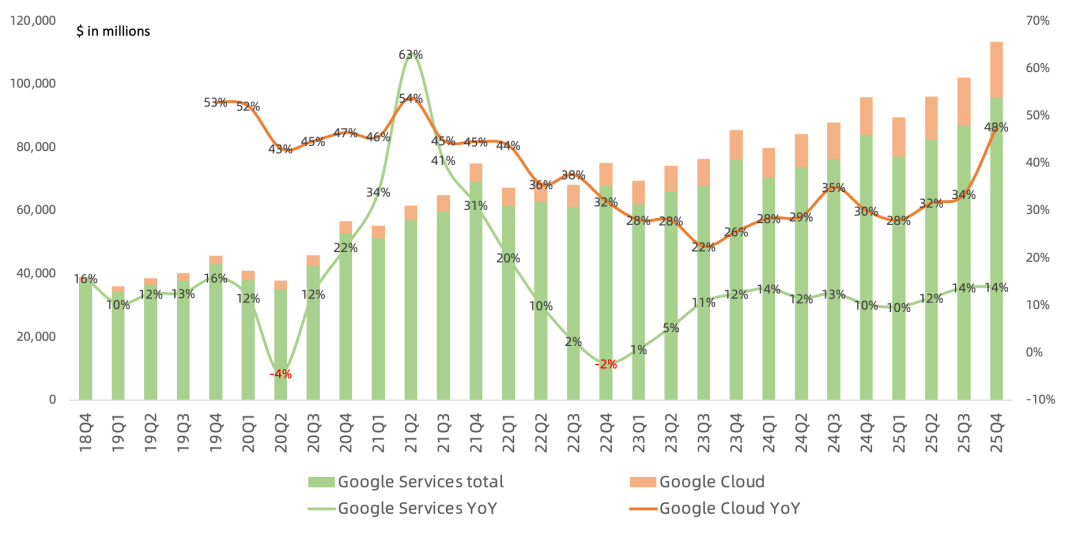

Google Cloud Q4 revenue $17.7B, up 48% year over year, sequential growth acceleration of 14 percentage points; operating income $5.3B, operating margin 30%, up 13 percentage points year over year.

Google Cloud core five businesses: AI Infrastructure, Vertex AI platform, BigQuery data platform, AI network security solutions, Workspace productivity suite; GCP revenue growth continues to exceed overall Cloud growth; over 70% of existing Google Cloud customers are using the company's AI products; existing customers' actual spend exceeds initial commitments by 30%+; Q4 backlog exceeds $240B, up 55% sequentially; Gemini MAU over 750M; 120K enterprises using Gemini; Gemini Enterprise has sold over 8M paid seats; GCP will be among the first to offer the latest Vera Rubin GPU platform; Workspace delivers double-digit growth driven by both ARPU and seat count increases; GCP now has 14 product lines with ARR over $1B; 2026 compute supply expected to remain tight.

Q4 capex $27.9B, ~60% for servers, 40% for data center and network equipment; 2026 capex guided at $175-185B, ramping through the year, ~60% for servers, 40% for data center and network equipment, expected over half of AI compute allocated to Cloud business; strong growth in enterprise AI infrastructure, driven primarily by TPU and GPU deployments; Google focuses on self-built data centers, occasionally leasing externally, most data centers are self-built; no current plans to sell TPUs externally.

4

Alibaba Cloud

China's Cloud Leader

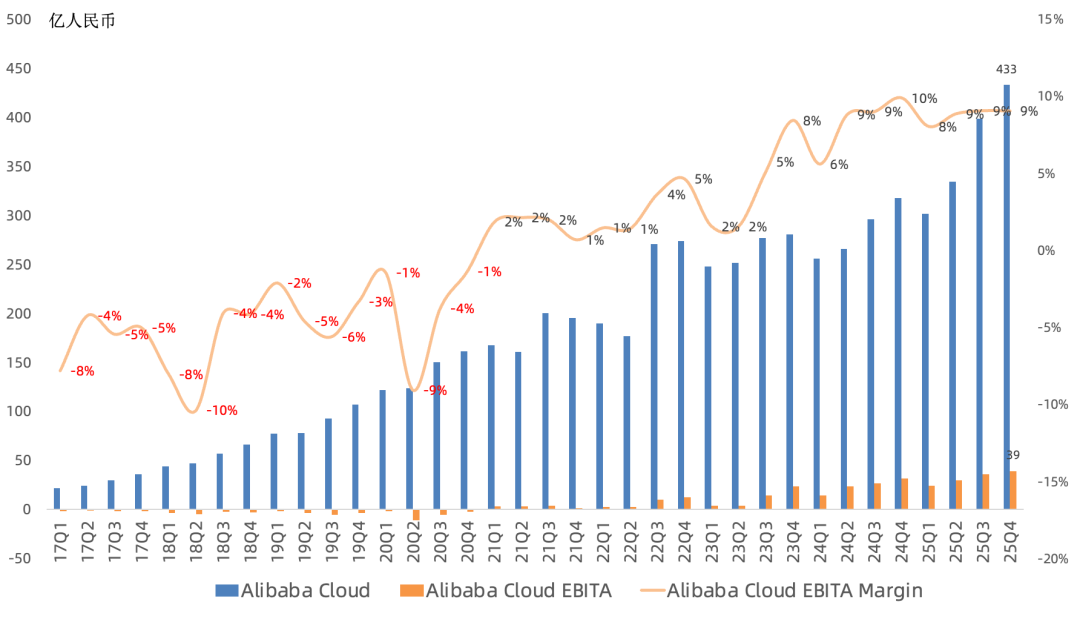

Q4 revenue RMB 43.3B ($6.19B), up 36% year over year, sequential growth acceleration of 2 percentage points; excluding internal consolidated revenue, up 35% year over year, sequential acceleration of 6 percentage points; AI-related revenue achieved triple-digit year-over-year growth for the 10th consecutive quarter; in February this year, Qwen platform-wide MAU exceeded 300M; Alibaba Cloud five-year target $100B, MaaS revenue to surpass IaaS as largest product.

Q4 EBITA profit RMB 3.9B, up 25% year over year, EBITA margin 9%, down 1 percentage point year over year; Q4 capex RMB 29B ($4.1B), previous quarter capex RMB 31.5B.

5

Oracle Cloud

Global Cloud Challenger

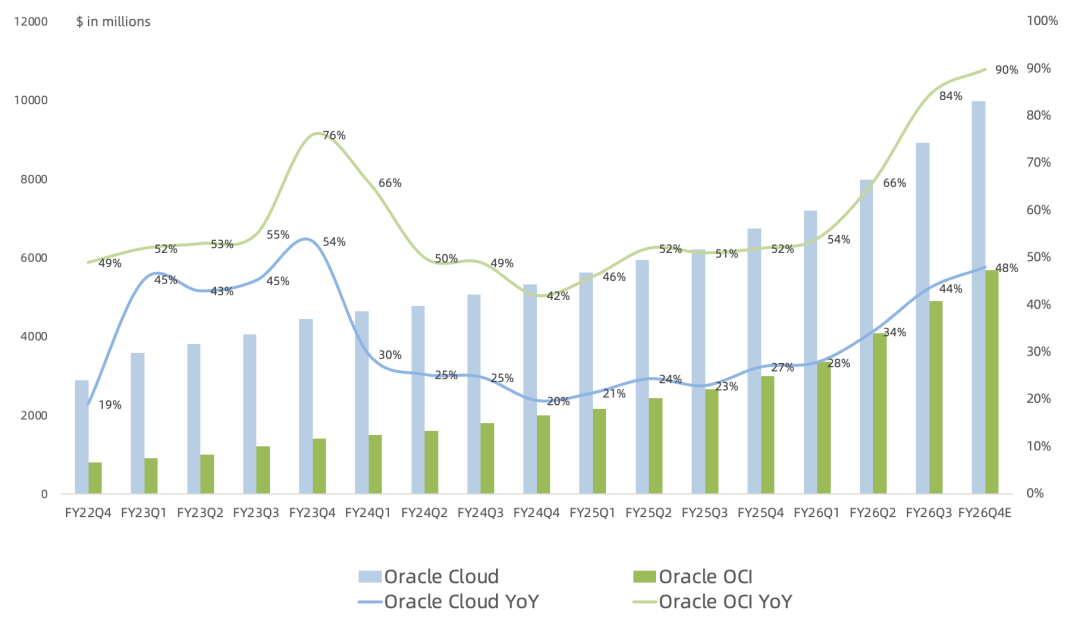

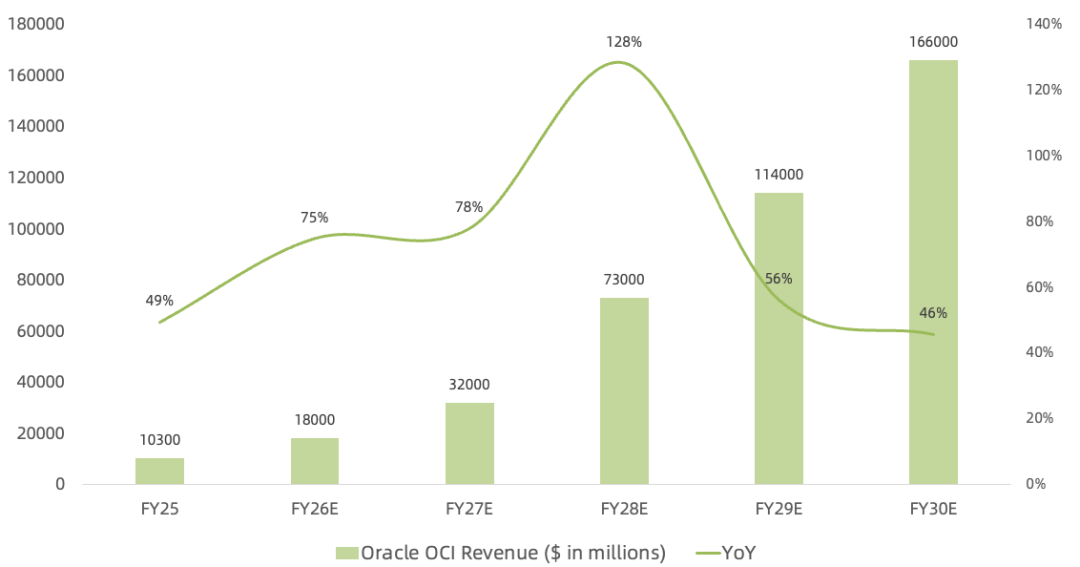

Oracle Cloud Q1, reported earlier as FY26Q3, generated $8.9B of revenue, up 44% year over year with growth accelerating ten percentage points sequentially. OCI infrastructure revenue reached $4.9B, up 84%, with growth accelerating 18 points. Management previously projected IaaS revenue of $32B, $73B, $114B, and $166B in FY27 through FY30, with OCI gross margin between 30% and 40%. This quarter OCI gross margin reached 32%, AI-related OCI revenue grew 243%, and Oracle delivered 400 MW of capacity.

Oracle maintained its $50B FY26 capex guidance but did not provide a specific FY27 figure. Management said Oracle's infrastructure expansion is becoming less dependent on its own capital. More than $29B of contracts involve customer-supplied hardware or customer prepayments, allowing Oracle to expand without generating negative cash flow.

MultiCloud Database revenue through Azure, GCP, and AWS grew 531% year over year. The service is live in 33 Azure regions, 14 Google Cloud regions, and eight AWS regions, with 22 additional regions planned next quarter. Cloud Database revenue grew 35%, while RPO exceeded $553B, up 325% year over year and $29B sequentially.

Oracle Cloud revenue is guided to grow 44%-48% in FY26Q4. Oracle maintained its $67B FY26 total revenue outlook and raised FY27 guidance to $90B from $85B. Oracle now owns 15% of TikTok US and holds one board seat. In February, it announced plans to raise up to $50B through debt and equity. Oracle has raised $30B so far and does not expect to issue bonds beyond the announced amount during calendar 2026.

6

CoreWeave & Nebius

Two AI Neocloud Leaders

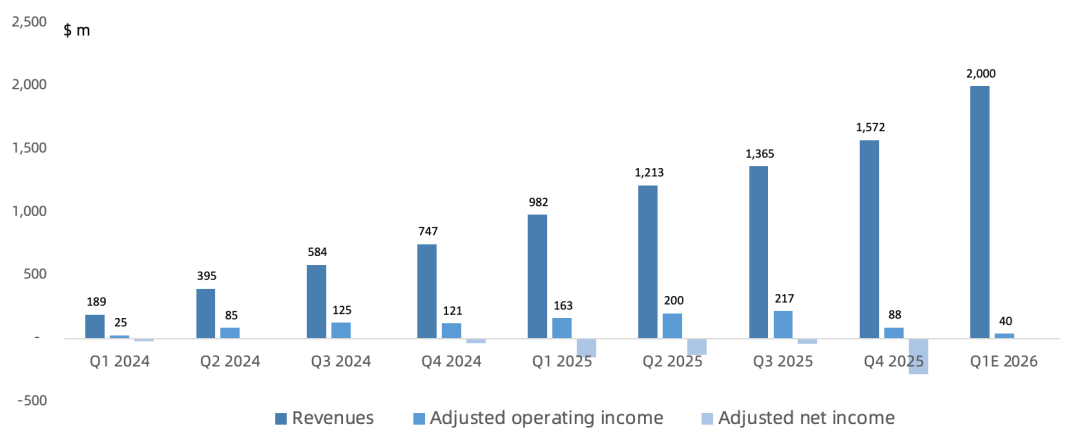

CoreWeave Q4 revenue $1.57B, up 110% year over year; gross margin less depreciation 7.2%, down 15 percentage points year over year; adjusted operating margin 6%; Q4 adjusted EBITDA $900M, up 85% year over year, EBITDA margin 57%, down 7.9 percentage points year over year; Q4 capex $8.24B, significantly exceeding revenue; combined with high leverage and high depreciation, the market remains skeptical of its profitability.

CoreWeave Q4 RPO $60.7B, up 302% year over year, up $10.7B sequentially; company currently operates 43 data centers globally, active power ~850 MW (QoQ +260 MW), contracted power ~3.1 GW (QoQ +0.2 GW), expects 2026 year-end active power to double to over 1.7 GW; new reserved instance customers this quarter approximately double any prior quarter; seeing significantly increased demand for prior-generation GPU architectures while supply remains constrained; incremental demand still seen for Hopper (H100/H200); Q4 H100 average pricing fluctuated within 10% of start-of-year levels; A100 average pricing up from 2025 levels, primarily used for inference; 2026 new capacity essentially fully allocated; target to add over 5 GW of data center capacity before 2030;

Next quarter revenue guided at $1.9-2.0B, up 94%-104% year over year; adjusted operating income $0-40M; Q1 will be the profit trough; 2026 capex guided at $30-35B; 2026 full-year revenue $12-13B, ~140% year over year at midpoint; adjusted operating income guided at $900M-1.1B; 2026 year-end ARR revenue to reach $17-19B; 2027 year-end ARR revenue to exceed $30B; management remains confident in long-term 25%-30% margin target.

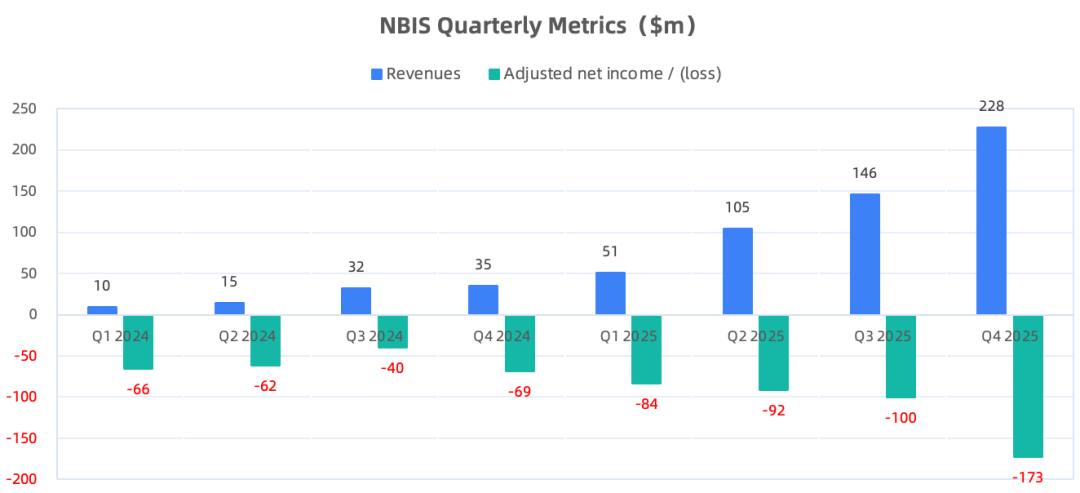

Nebius Q4 revenue $228M, up 547% year over year, of which core AI cloud revenue $214M, up over 800% year over year, accounting for ~94% of revenue; gross margin less depreciation -9.4%; adjusted EBITDA $15M, turning positive sequentially and year over year, EBITDA margin 7%; first quarter achieving positive operating cash flow and EBITDA; Q4 capex $2.06B, surging sequentially and year over year.

Nebius acquired agentic AI search tool Tavily in February this year; Nebius lowers costs by designing its own racks rather than buying from OEMs; as of end-2025 active power 170 MW, signed over 2 GW power capacity, expects 2026 year-end contracted power over 3 GW, active power 800 MW-1 GW; current capacity utilization maxed out, capacity sold out.

2026 capex guided at $16-20B, of which 60% of spend is backed by existing opportunities, no bank borrowing needed; ~20% of total capital needs for data center construction, ~80% for GPUs; expects 2026 year-end ARR $7-9B (25Q4 was $1.25B).

7

DigitalOcean

AWS for Everyone

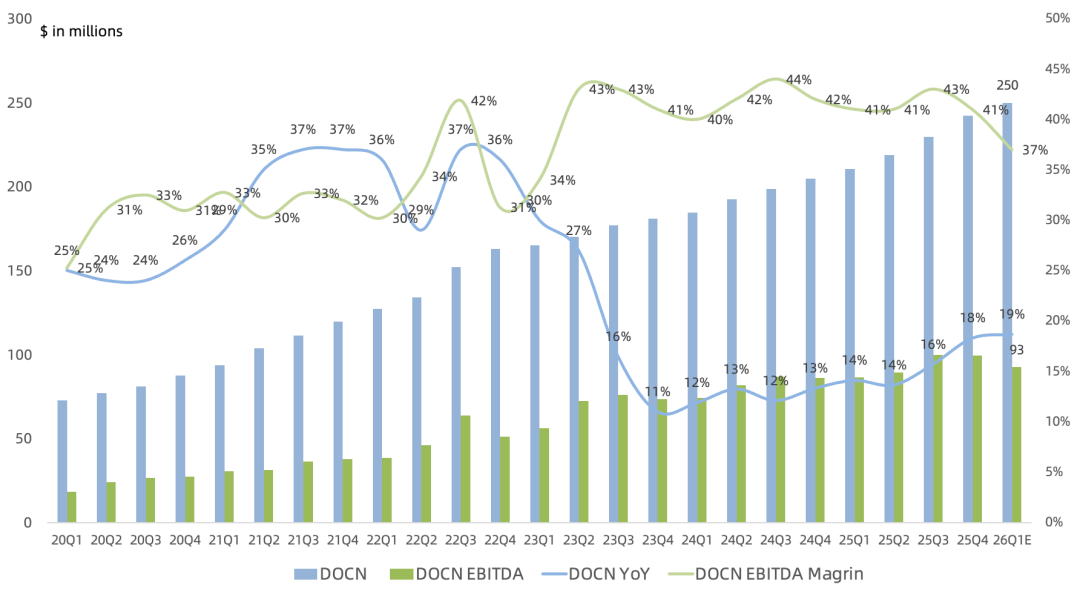

Q4 revenue $240M, up 18% year over year; ARR revenue $970M, up 18% year over year, of which AI ARR revenue up 150% year over year, doubling for the 6th consecutive quarter; AI inference ARR revenue up 254% year over year; gross margin 59%, down 3 percentage points year over year; operating margin 16%, flat year over year.

Q4 EBITDA $99.3M, up 16% year over year; EBITDA margin 41%, down 1 percentage point year over year; Net Dollar Retention Rate 101%, up 2 percentage points sequentially; RPO $134M (previous quarter $47M).

DigitalOcean primarily serves small and medium-sized businesses, making it sensitive to macroeconomic cycles. Its top 25 customers contribute only 10% of revenue. I previously argued that DigitalOcean moved too slowly as AI-native competitors such as CoreWeave and Nebius emerged. H100 instances did not become available to all customers until October 1 last year, and the company's first AI product, GenAI Platform, launched only in early November. DigitalOcean now offers H100, H200, B300, MI300X, MI325X, and MI350X instances.

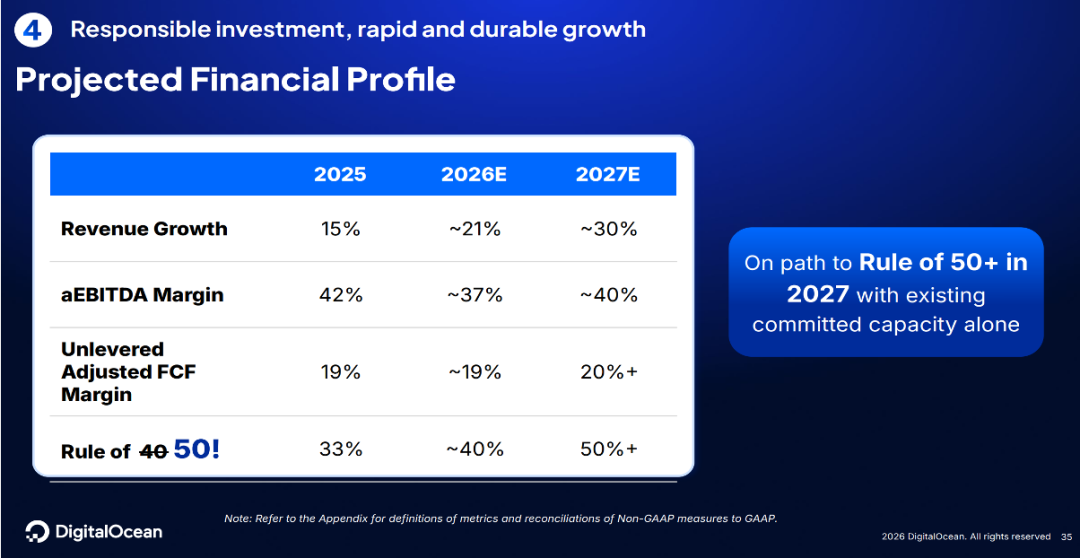

Currently, relative to star Neoclouds, its leverage is lower, but to rapidly meet AI demand it has also begun increasing capex and leverage; expects 6 MW data center to start contributing revenue in 2026Q2, remaining 25 MW data centers to contribute in 2H 2026; expects 2026 overall revenue up 21% year over year, 2027 revenue up 30% year over year.

Conclusion

Cloud companies' capex exploded again this quarter; FAMG + Oracle Q4 capex total exceeded $139B, up 67% year over year. As hyperscalers' compute demand surges, 2026 FAMG four giants' capex guidance upper bound exceeds $670B, up 62% year over year. Going forward, cloud capex concentration in GPU servers will continue to rise, yet the market persistently views this as overinvestment; Amazon has consistently emphasized this scenario closely resembles the early days of cloud computing, but currently cloud is the highest-ROI scenario for AI, bar none. There is also an easily overlooked phenomenon: as AI startups scale, their demand for traditional cloud computing also increases.