With Alibaba's belated report, the Q3 scorecards of the global top four cloud giants are now complete.

Global Cloud #1 Remains Amazon AWS:

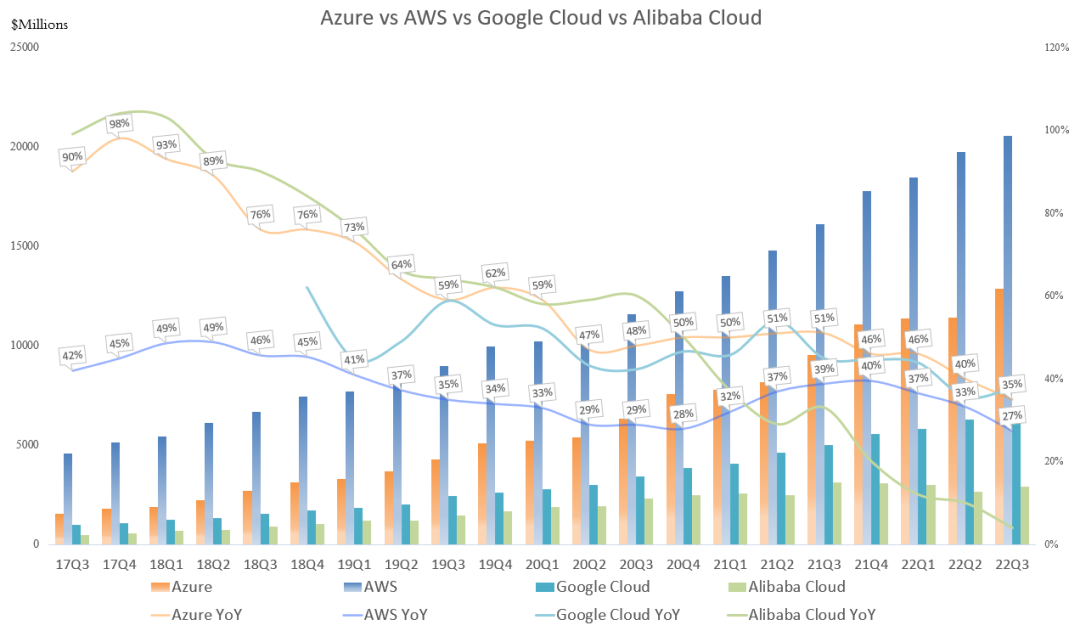

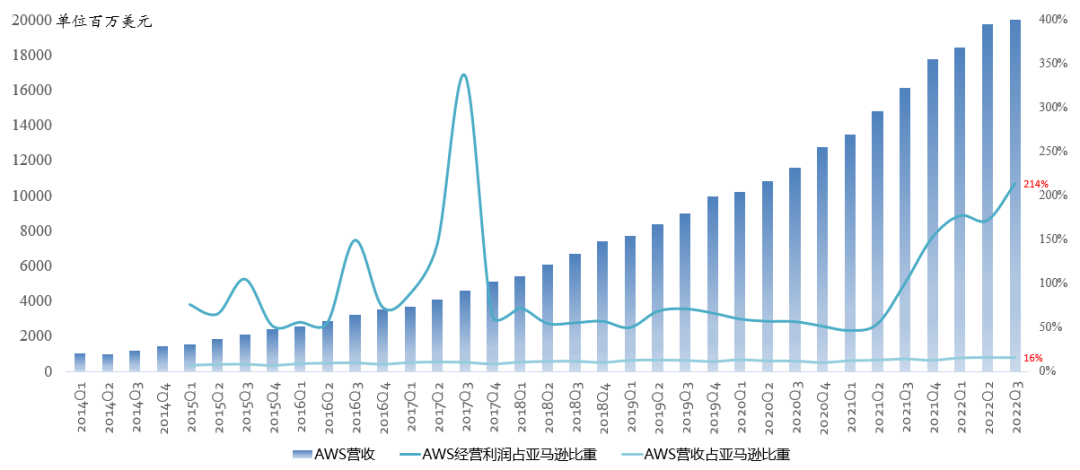

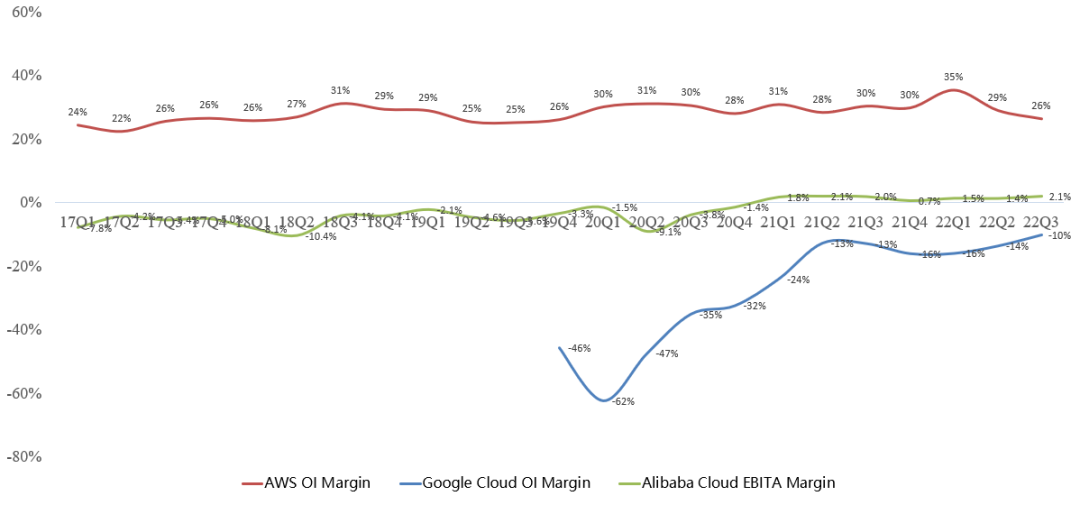

Q3 revenue $20.538B, up 27% year over year, first time above $20B; operating income $5.403B, up 11% year over year; operating margin 26%.

AWS Q3 revenue was 16% of Amazon total revenue but contributed 214% of Amazon's operating income.

Global Cloud #2 Remains Microsoft Azure:

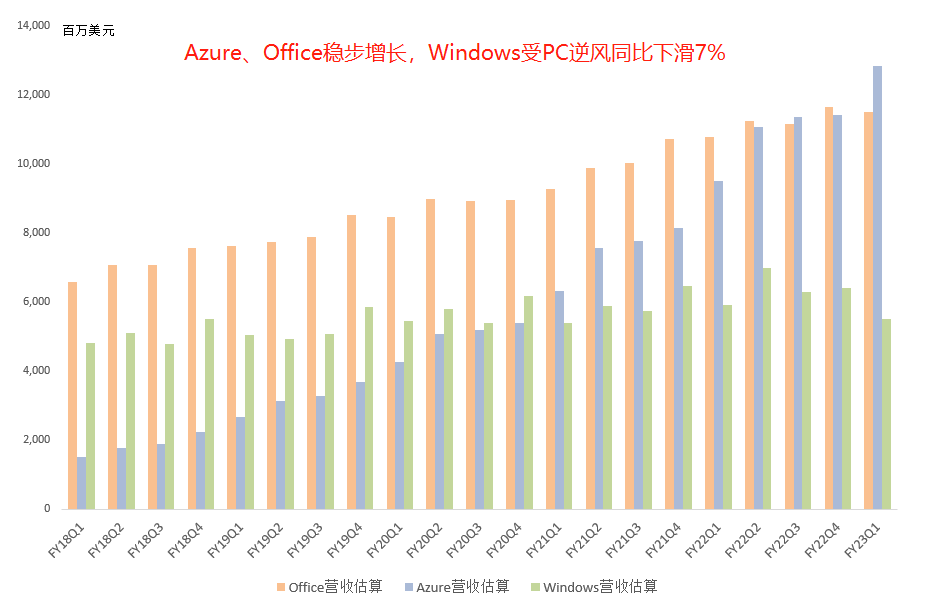

Q3 revenue $12.875B, up 35% year over year, growth falling below 40% for the first time;

Azure's Intelligent Cloud (Server + Azure + Enterprise Services) operating income $8.978B, up 19% year over year, fourth consecutive quarterly record; operating margin 44%;

Intelligent Cloud Q3 revenue was 41% of Microsoft total revenue, contributing 42% of Microsoft operating income;

Next quarter Azure revenue may see its first sequential decline.

Global Cloud #3 Remains Google Cloud:

Q3 revenue $6.868B, up 38% year over year, fastest growth among the global top four. Operating loss $699M, operating loss rate 10%, loss narrowing sharply;

GCP revenue growth again exceeded overall Cloud growth; won Hawaii state government and Australian Securities Exchange deals;

Future capex focus remains Cloud and AI.

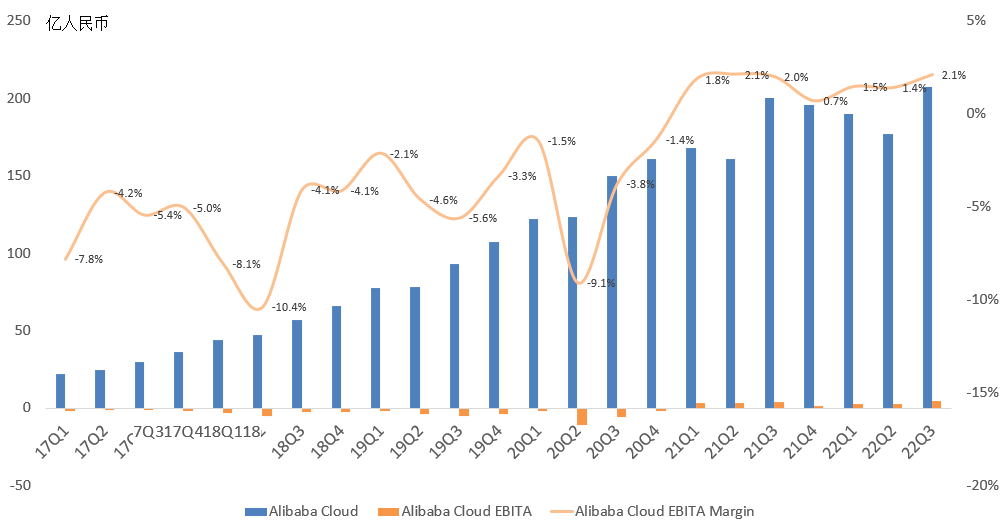

Global Cloud #4 Remains Alibaba Cloud:

Q3 revenue RMB 20.8B ($2.918B), up 4% year over year (-6% USD), sequential growth resumed, growth still trailing the global top four;

Q3 EBITA profit RMB 434M, EBITA margin 2.1%, seventh consecutive quarter of profitability, albeit EBITA basis and including DingTalk.

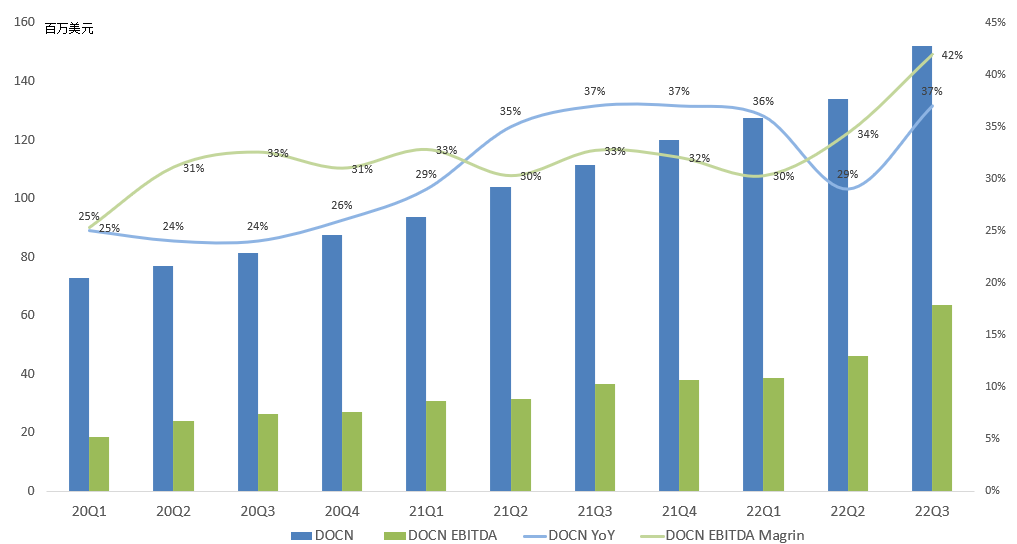

Rising Star: DigitalOcean, the 'People's AWS':

Q3 revenue $152M, up 37% year over year; first operating profit, operating margin 6%; Monthly ARPU $79, up 28% year over year;

Q3 EBITDA profit $63.7M, up 75% year over year, continuing to hit records; EBITDA margin 42%, second consecutive quarterly record;

DigitalOcean's standout feature is a very low sales expense ratio, only 13%; long below R&D and G&A ratios.

DigitalOcean's clear trait is a predominantly SMB customer base, theoretically macro-sensitive, yet performance grew steadily—unexpected. The company cites a sufficiently dispersed customer base and still-low cloud penetration, leaving ample runway.

Summary:

Overall, the global cloud Big 3 continued to deliver steadily, but macroeconomic pressure is becoming evident; against high comps, growth continues to show marginal deceleration.

On profitability, Microsoft and Amazon remain stable; Google is focusing on profitability, potentially turning profitable next year. Alibaba Cloud's sustained profitability also boosts confidence in China's cloud industry, proving the cloud business model is relatively mature.

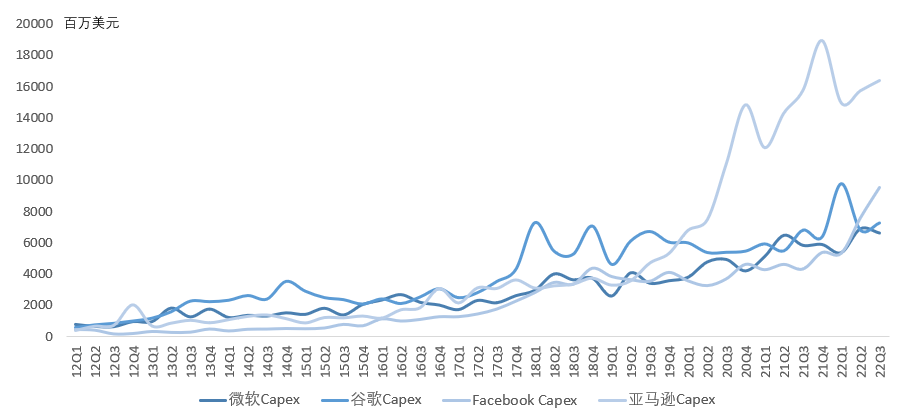

Despite macro headwinds, cloud capex remains at historical highs; FAMG Q3 average capex up 16% year over year, still concentrated in servers, primarily for AI/ML. We still believe sustained cloud prosperity is the most critical link in the data-center semiconductor boom.

Global Top Four Cloud Vendor Characteristics:

Amazon AWS: Marketplace = Apple App Store

Microsoft Azure: IaaS + PaaS + SaaS integration; Google Cloud: Clear Data Cloud advantage, TensorFlow + TPU software-hardware ecosystem