In the previous article "Global Cloud Giants Q1: AI and Non-AI Both Soaring, Compute Still Insufficient," it was noted that cloud AI revenue continued to surge, non-AI demand recovered above expectations, and compute remained undersupplied. This quarter the three major clouds began to show AI winners (Azure, GCP) and a loser (AWS), and compute undersupply is projected to persist into early next year.

1

Amazon AWS

Global Cloud Leader

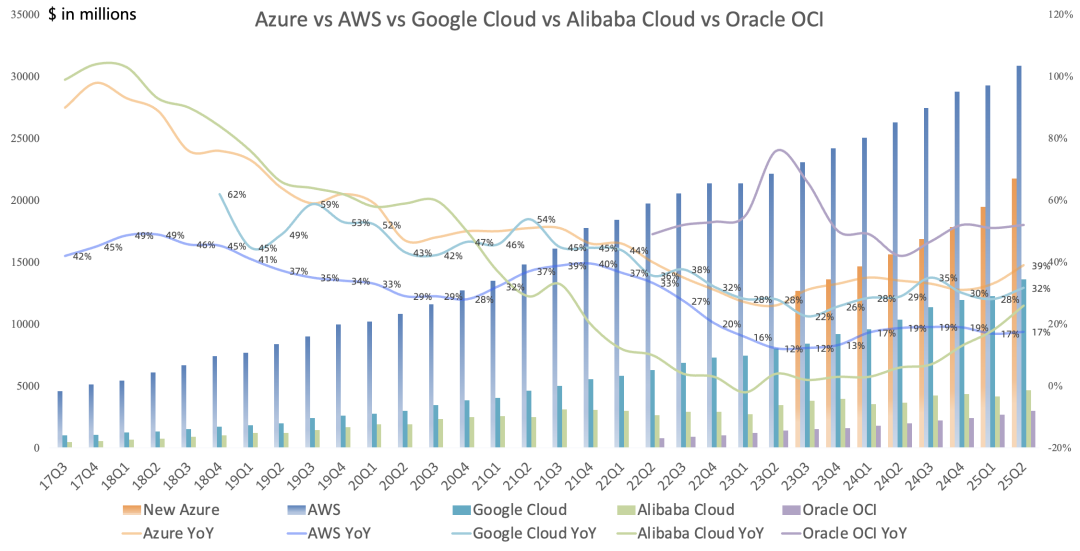

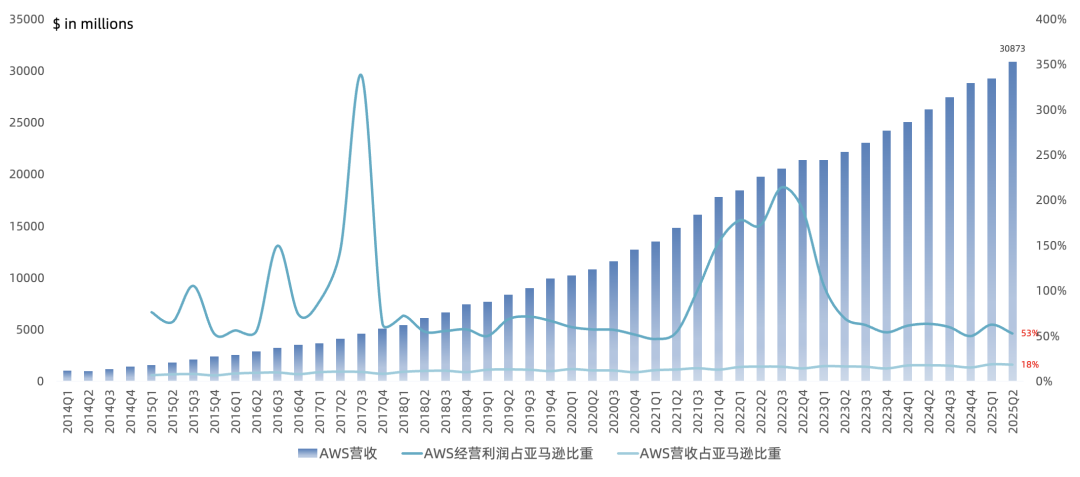

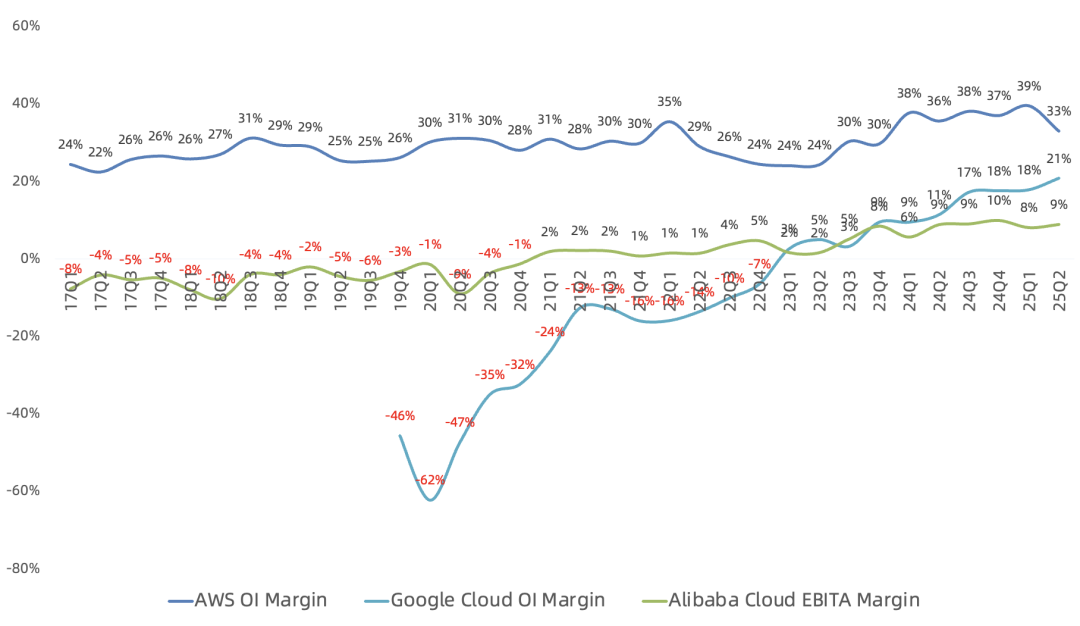

AWS Q2 revenue $30.9B, up 17% year over year, sequential growth rate flat; up 5% sequentially. Operating income $10.2B, up 9% year over year. Operating margin 33%, down 3 points year over year.

AWS Q2 revenue accounted for 18% of Amazon total revenue, contributing 53% of Amazon operating income.

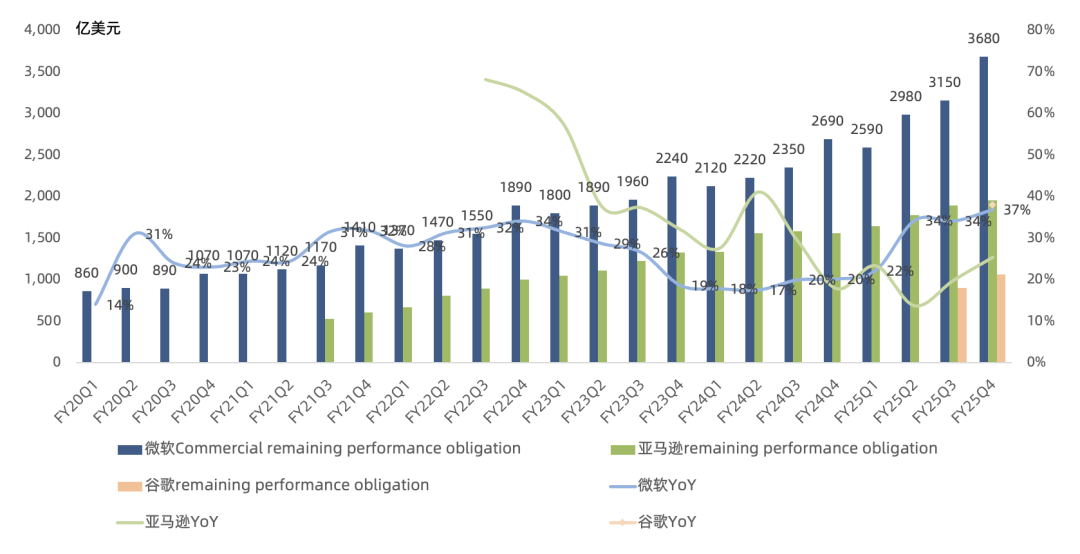

AWS Q2 revenue run rate $123B. Growth in both AI and non-AI. AI revenue run rate reached multiple billions, maintaining triple-digit year-over-year growth. Demand still far exceeds supply capacity; power is the biggest near-term bottleneck. Undersupply expected to persist for several quarters, but improving each quarter. Trainium 2 deploying at larger scale. Launched Amazon EC2 instances powered by NVIDIA Grace Blackwell superchips. Anthropic's Claude 4 added to Bedrock, becoming the fastest-growing model in Bedrock history. RPO $195B, up 25% year over year. Over 85% of global IT spend still on-premises, not yet migrated to cloud. AWS margin decline mainly due to timing of stock-based compensation recognition and higher depreciation from capex.

Q2 capex $31.4B, mostly into AI. Q2 capex seen as representative of quarterly capex run rate for H2.

2

Microsoft Azure

Second-Largest Global Cloud

Microsoft Azure Q2 revenue $21.7B, up 39% year over year, growth continues to lead the global big three clouds.

Intelligent Cloud (Server + Azure + Enterprise Services) revenue $29.9B, up 26% year over year. Gross profit $12.1B, up 23% year over year. Both new all-time highs. Operating margin 41%. Intelligent Cloud accounted for 39% of Microsoft total revenue, contributing 35% of operating income.

Both Azure AI and non-AI revenue beat expectations this quarter, with growth driven primarily by the largest customers; market share continues to rise. AI contribution to Azure growth in line with expectations, but going forward distinguishing AI from non-AI workloads will become more difficult (implying even OpenAI starting to use Azure non-AI workloads). Now 400+ datacenters across 70 global regions, more than any other cloud provider. All regions now support liquid cooling. Added 2GW+ new capacity in just the past 12 months. Even with more capacity coming online, capacity constraints expected to persist through FY26H1. Launched Microsoft Sovereign Cloud covering public and private cloud deployments. Cloud migration continues to accelerate. Azure AI Foundry processed 5Q+ tokens this fiscal year, up 7x year over year. 80% of Fortune 500 using Azure AI Foundry.

Microsoft Fabric becoming the complete data and analytics platform for the AI era, spanning SQL to NoSQL to analytics workloads. Momentum strengthening, revenue up 55% year over year, 25,000+ customers. Fastest-growing database product in Microsoft history. Azure Databricks and Snowflake on Azure also accelerating.

AI demand grew too fast this quarter; expected AI capacity relief pushed to early calendar 2026. Three Azure growth drivers: cloud migration + cloud-native SaaS scale + AI. Commercial RPO $368B, up 37% year over year. Next quarter Azure revenue guided up 37% year over year; capex >$30B.

3

Google Cloud

Third-Largest Global Cloud

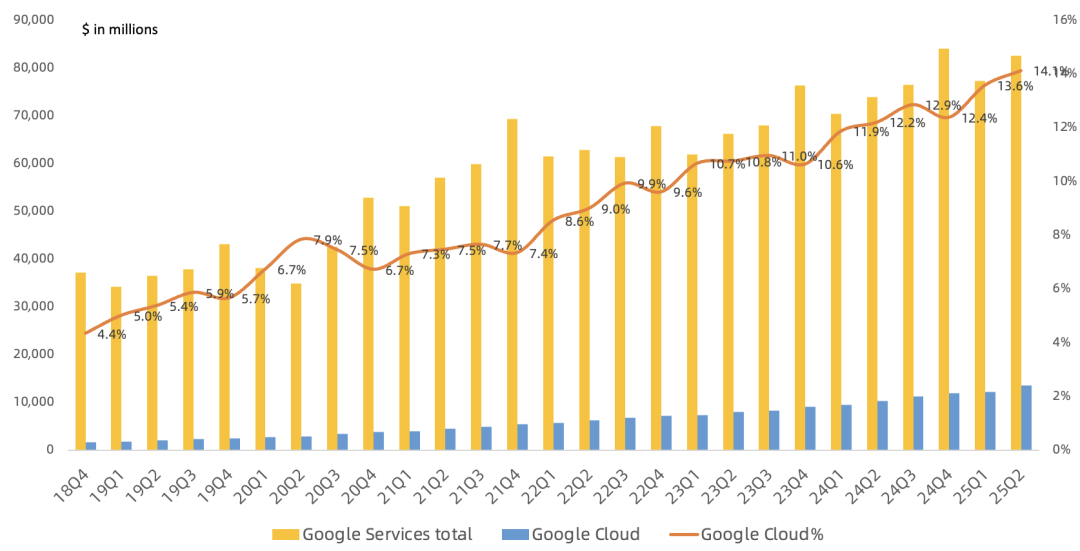

Google Cloud Q2 revenue $13.6B, up 32% year over year, sequential growth acceleration of 4 points. Operating income $2.8B, operating margin 21%, new all-time high.

Google Cloud five core businesses: AI infra, commercial AI platform Vertex, data platform BigQuery, AI cybersecurity solutions, Workspace productivity suite. GCP revenue growth continues to exceed overall Cloud growth. Backlog up 18% sequentially and 38% year over year to $106B. At I/O, monthly token processing disclosed at 4.8Q; now doubled to 9.8Q. Gemini MAU >450M; daily requests up 50%+ vs Q1. Cloud H1 2025 $1M+ deal count already equals full-year 2024; $250M+ mega-deal count doubled year over year. New GCP customers up ~28% sequentially; 85K+ new enterprise customers added this quarter. Workspace driven by ARPU growth.

Management says Google will remain compute-constrained through early 2026.2025 capex guidance raised from $75B to $85B.

4

Alibaba Cloud

China's Cloud Leader

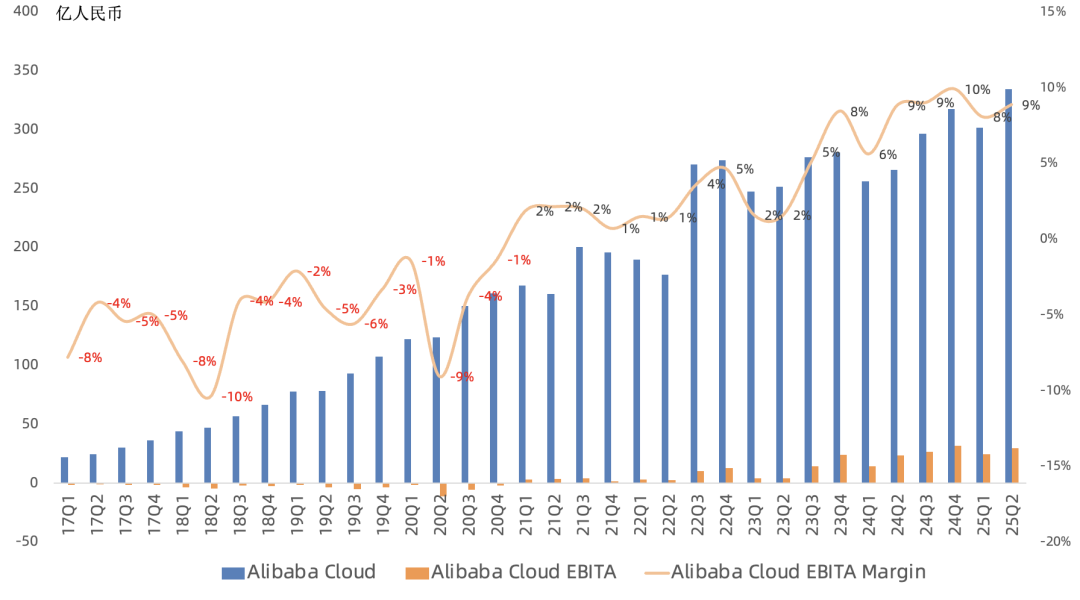

Q2 revenue was RMB 33.4B ($4.662B), up 26% year over year, marking the third consecutive quarter of double-digit year-over-year growth. Excluding internal consolidation revenue, year-over-year growth was also 26%. Core public cloud businesses, led by AI, saw significant revenue growth, with AI-related revenue achieving triple-digit year-over-year growth for the eighth consecutive quarter. Amid surging AI demand, the company also observed sustained growth in compute, storage, and other public cloud services to support AI applications. Management expects Alibaba Cloud's growth rate to continue accelerating.

Q2 EBITA was RMB 3.0B, up 26% year over year, with an EBITA margin of 9%, driven by high-margin public cloud businesses including AI and efficiency gains. Capex this quarter was RMB 38.6B, above market expectations, versus RMB 24.6B last quarter. The Wall Street Journal recently reported that due to the H20 ban and Alibaba's unwillingness to use rival Huawei chips, the company is now developing its own AI chips, which aligns with the logic.

5

Oracle Cloud

Global Cloud Challenger

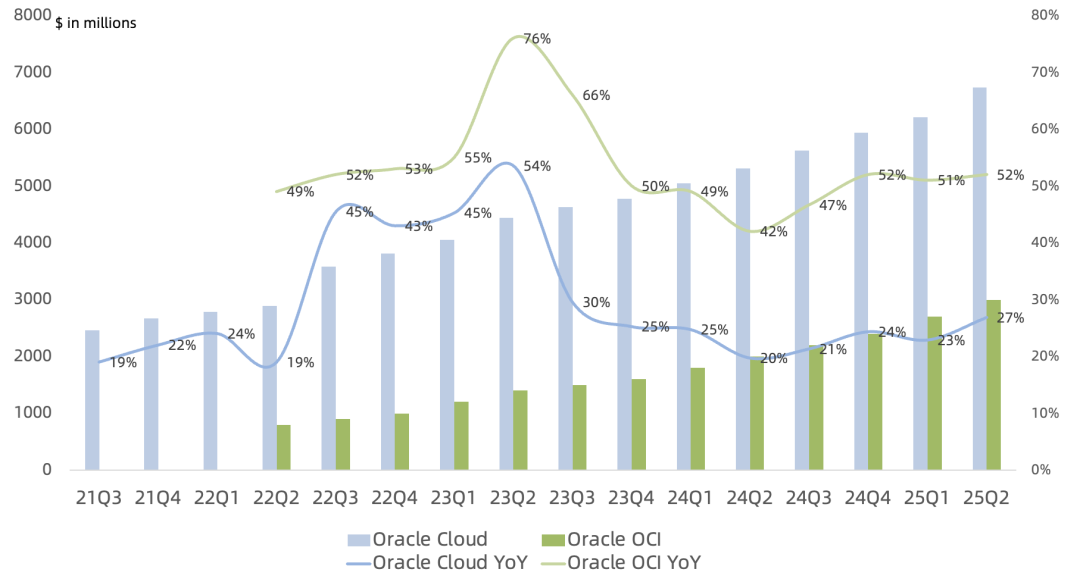

Q2 revenue was $6.74B, up 27% year over year, with growth accelerating 4 percentage points sequentially. OCI (IaaS) revenue was $3.0B, up 52% year over year, while SaaS revenue was $3.7B, up 12% year over year. The company guides FY26 SaaS+IaaS cloud revenue growth >40% year over year, and IaaS revenue growth >70% year over year. Capex this quarter was $9.1B; FY25 capex was $21.2B, up 209% year over year. FY26 capex is guided at least $25B.

OCI consumption revenue grew 62% year over year, remaining in persistent short supply, with FY26 consumption growth expected to accelerate. MultiCloud Database revenue from Azure/GCP/AWS grew 115% sequentially, winning the Temu cloud deal, unrelated to AI. Cloud Database revenue grew 31% year over year, with an annualized run rate of $2.6B. Autonomous Database consumption revenue grew 47% year over year. RPO was $138B, up 41% year over year, with cloud accounting for 80% of total RPO. FY26 RPO growth is guided >100% year over year, including the initial Stargate project.

Multicloud across Azure/AWS/GCP is now live in 23 data centers, with 47 more under construction over the next 12 months. FY26 Multicloud revenue is guided to double year over year. OCI's advantage over peers lies primarily in standardization, automation, and full coverage of data centers from small to large.

6

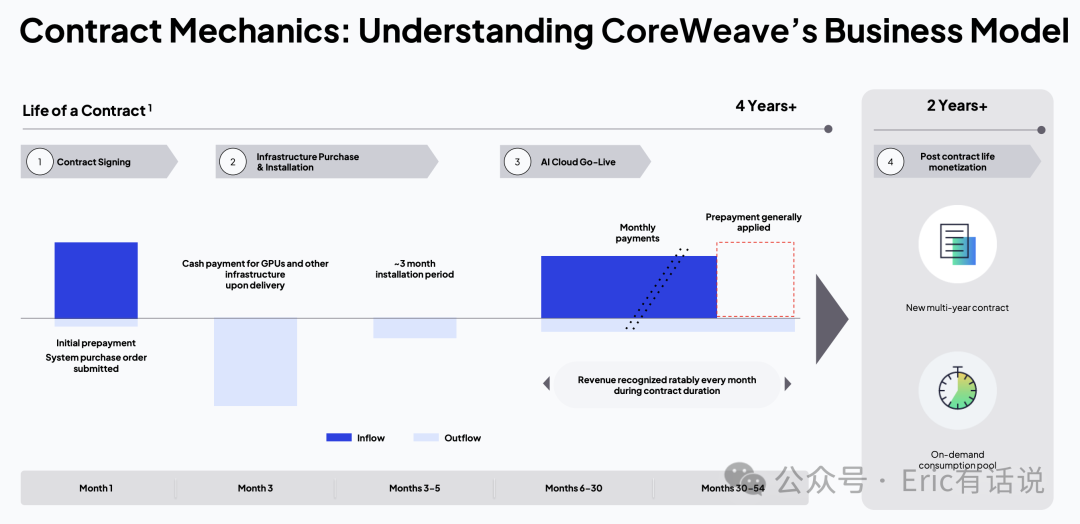

CoreWeave

AI NeoCloud

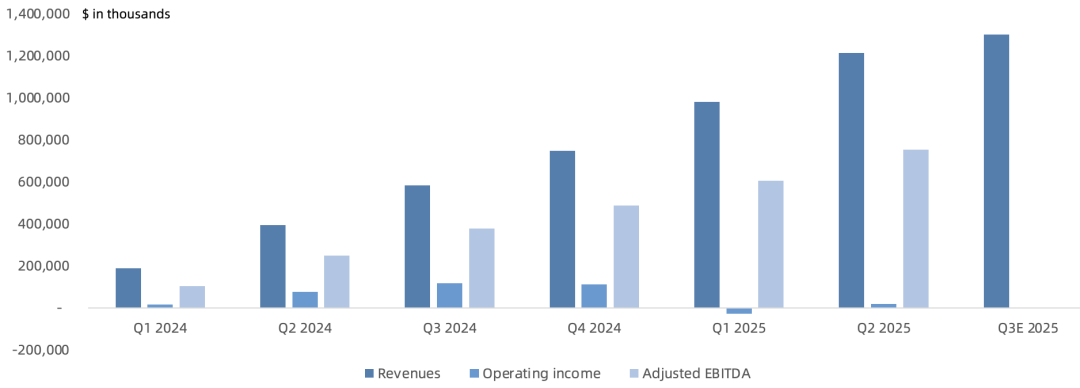

Q2 revenue was $1.2B, up 207% year over year. Gross margin was 74%, up 1.7 percentage points year over year. Operating margin was 2%. Adjusted EBITDA was $750M, with an EBITDA margin of 62%. Q2 capex was $2.9B, with full-year guidance of $20-23B, significantly exceeding revenue. Combined with high leverage, the market questions its profitability.

Q2 RPO was $30.1B, up 86% year over year and 16% sequentially. The company operates 33 data centers globally, with ~470MW of available power (QoQ +50MW) and ~2.2GW of contracted power (QoQ +0.6GW). Per official disclosures, CoreWeave effectively operates on a 'build-to-order' or 'customer-funded capex' model, where data center capacity expansion is directly tied to secured contracts and prepayments.

7

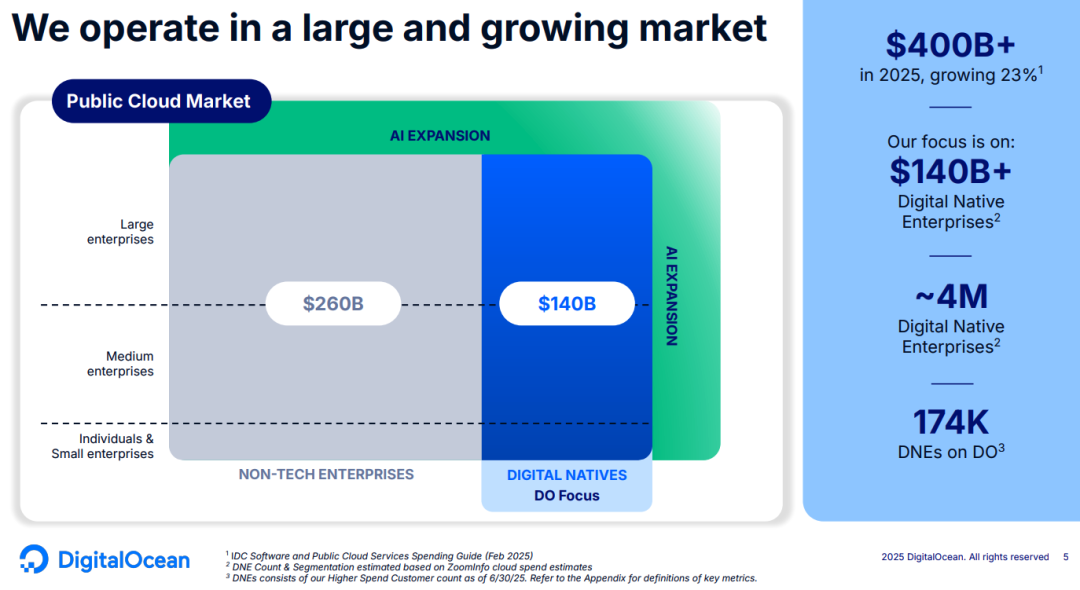

DigitalOcean

AWS for Everyone

Q2 revenue was $220M, up 14% year over year, with AI/ML revenue doubling year over year. ARR was $880M, up 14% year over year. Gross margin was 60%, down 1 percentage point year over year. Operating margin was 16%, up 4 percentage points year over year. Monthly ARPU was $111.7, up 12% year over year, continuing to grow sequentially. Full-year 2025 revenue growth is guided at 14% year over year.

Q2 EBITDA was $89.5M, up 10% year over year. EBITDA margin was 41%, down 1 percentage point year over year. Net Dollar Retention Rate was 99%, down 1 percentage point sequentially. RPO was $58.3M, up 4x sequentially.

DigitalOcean's distinct characteristic is a customer base predominantly of SMBs, making it highly sensitive to macroeconomic cycles. Although ARPU continues to rise, customer count growth remains slow. Previously noted in the AI cloud wave, traditional small cloud player DigitalOcean has been somewhat slow to act against the rise of new entrants like CoreWeave and Nebius. It only opened H100 instances to all customers on October 1 last year and launched its first AI product, GenAI Platform, in early November. It now offers H100, H200, MI300X, and MI325X instances.

Conclusion

Cloud companies' capex exploded again this quarter. FAMG Q2 capex totaled nearly $100B, up 65% year over year with growth accelerating, and up 24% sequentially. As hyperscalers' compute demand surges, 2025 capex guidance for the big four continues to rise sharply, with Google and Meta both raising full-year capex guidance again this quarter. Going forward, cloud capex concentration on GPU servers will keep increasing. The market consistently views this as overinvestment, but Amazon has emphasized this resembles the early days of cloud computing, and cloud remains the highest-ROI scenario for AI, bar none. Another overlooked phenomenon: as AI startups scale, their demand for traditional cloud also grows, e.g., OpenAI on Microsoft Azure.