In the previous article 'Global Cloud Giants Q2: Dawn of Industry Recovery,' we suggested the cloud/SaaS recovery dawn might be imminent. With Alibaba's delayed earnings, the Q3 scorecards of the five global cloud giants are now complete; the industry recovered on schedule.

1

Amazon AWS

Global Cloud Leader

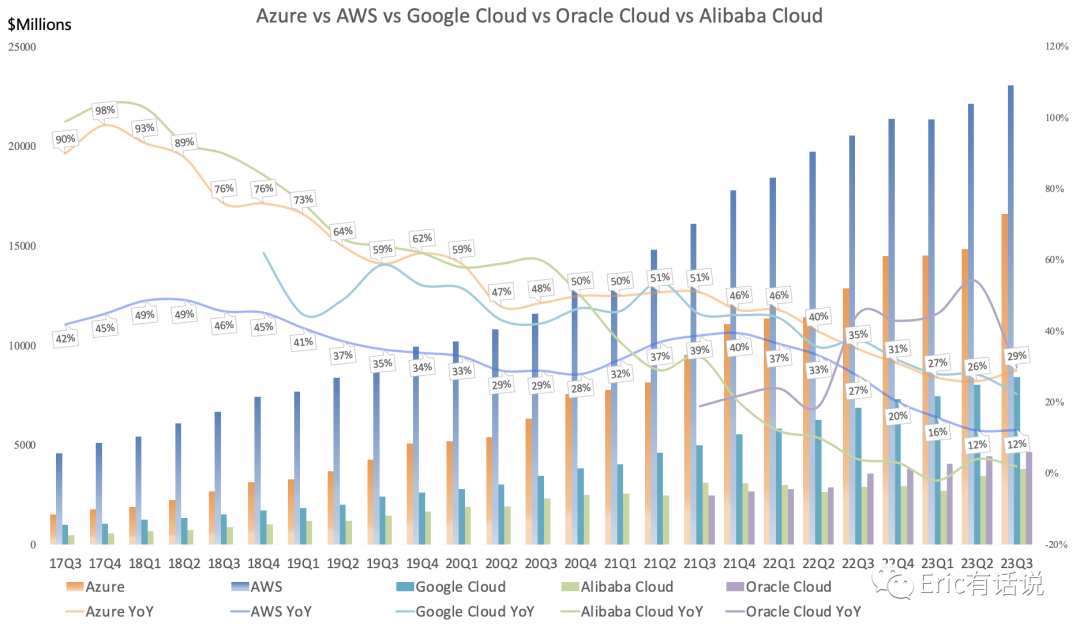

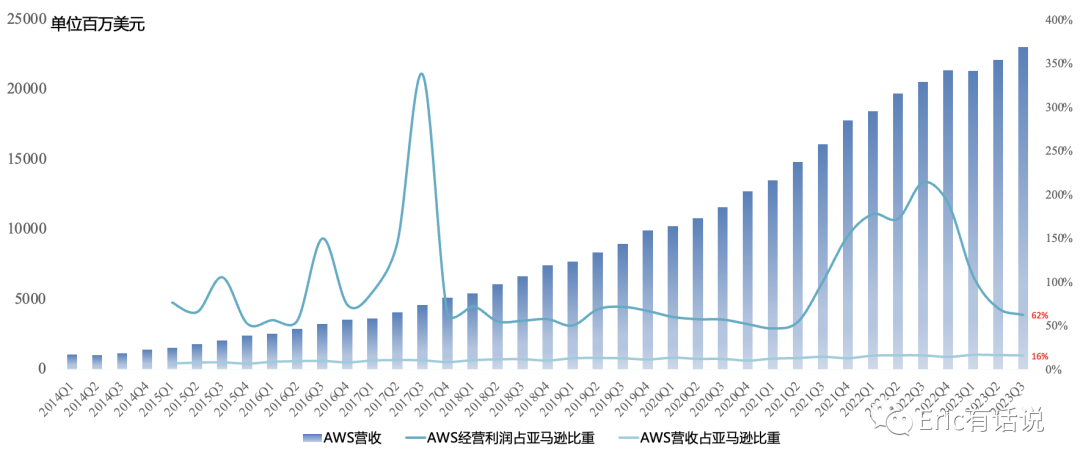

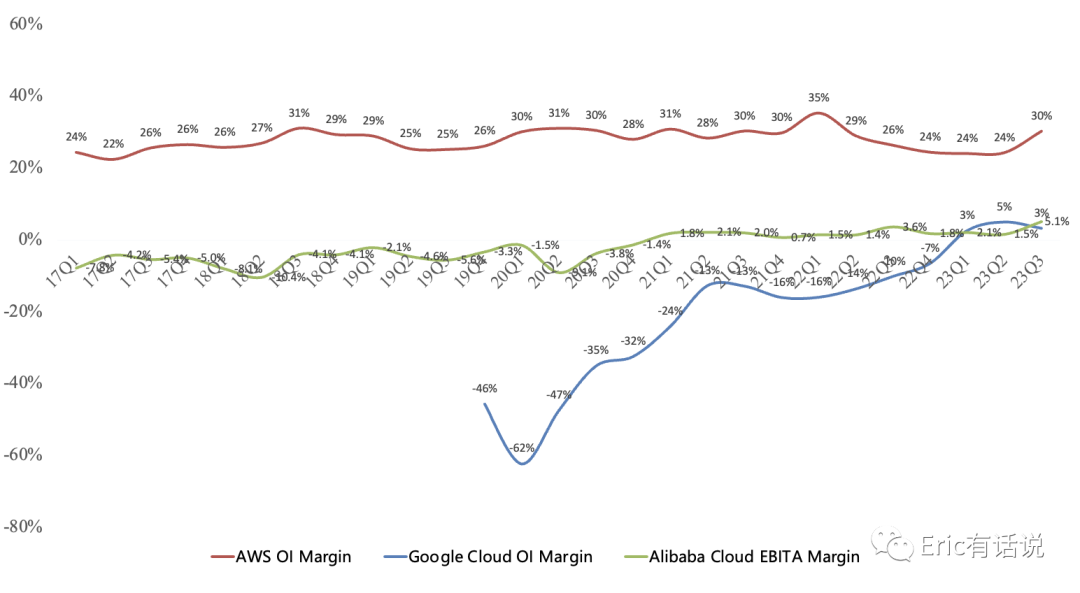

Q3 revenue $23.059B, up 12% year over year, growth rate nearly flat, up 4% sequentially; operating income $6.976B, up 29% year over year, all-time high; operating margin 30%, up 4 percentage points year over year.

AWS Q3 revenue accounted for 16% of Amazon total revenue, contributing 62% of Amazon operating income.

Since Q3 last year, enterprises of all sizes began optimizing cloud spend, slowing growth; this trend will persist but has decelerated; July AWS year-over-year growth rate was consistent with Q2, providing a glimpse of recovery.

2

Microsoft Azure

Second-Largest Global Cloud

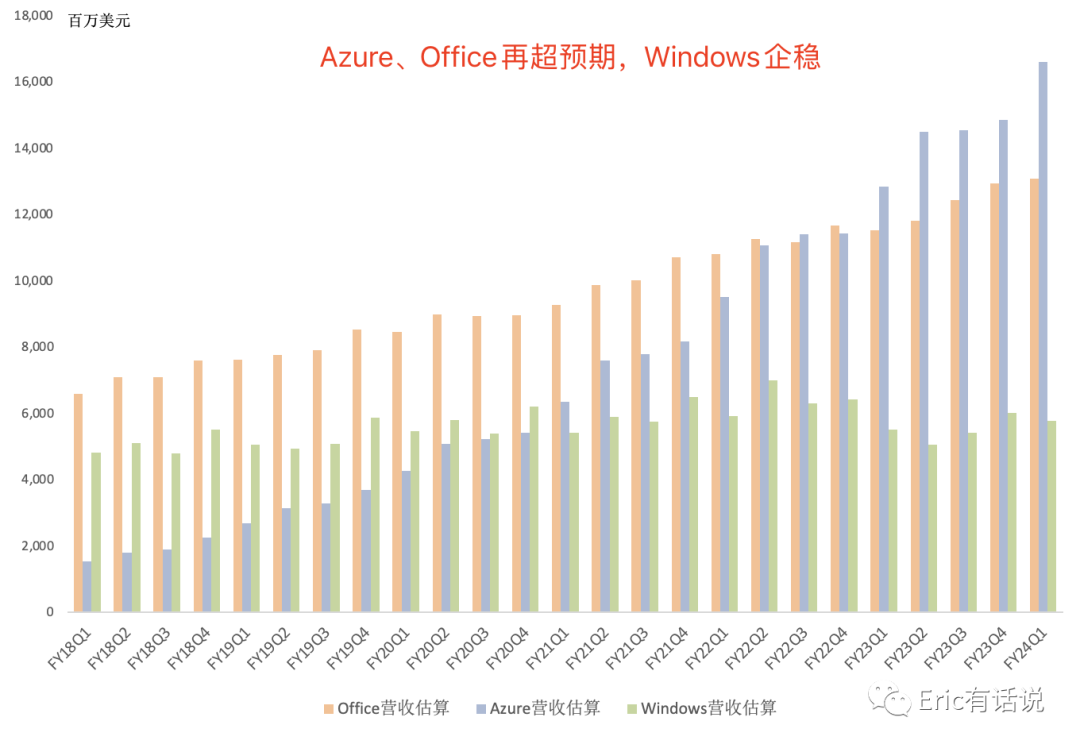

Q3 revenue $16.6B, up 29% year over year, growth re-accelerating, up 12% sequentially.

Intelligent Cloud (Server + Azure + Enterprise Services) operating income $11.751B, up 31% year over year, another all-time high; operating margin 48%.

Intelligent Cloud Q3 revenue accounted for 43% of Microsoft total revenue, contributing 44% of Microsoft operating income.

Azure market share continues to rise; 60+ global data centers, best AI training and inference facilities; Azure AI customers beyond OpenAI include first-party, Meta, Hugging Face; Azure OpenAI Service customers now exceed 18,000; due to Azure AI advantage, seeing more cloud migrations to Azure; Azure Arc now has 21,000+ customers, up 140% year over year; Azure is the only cloud besides Oracle Cloud to offer Oracle Database services; AI contributed 3% to Azure growth.

3

Google Cloud

Third-Largest Global Cloud

Q3 revenue $8.411B, up 22% year over year, growth rate down 6 percentage points sequentially. Operating income $266M, operating margin 3%, profitable for three consecutive quarters.

Currently over 60% of Fortune 1000 companies and over 50% of AI unicorns are Google Cloud customers (70% last quarter); Vertex AI offers 100+ models, active AI projects up 7x sequentially; cloud customers still optimizing costs; Workspace revenue up year over year, ARPU up year over year; GCP revenue growth again exceeded Cloud overall growth; Workspace paid seats exceed 10M; I previously wrote that a key watch item for Google this year is Google Cloud profit release; year-end OPM breaking 10% should be no problem, and will gradually approach AWS's ~20% level, but Q3 margin did not reach expected level, so breaking 10% may have to wait until next year.

4

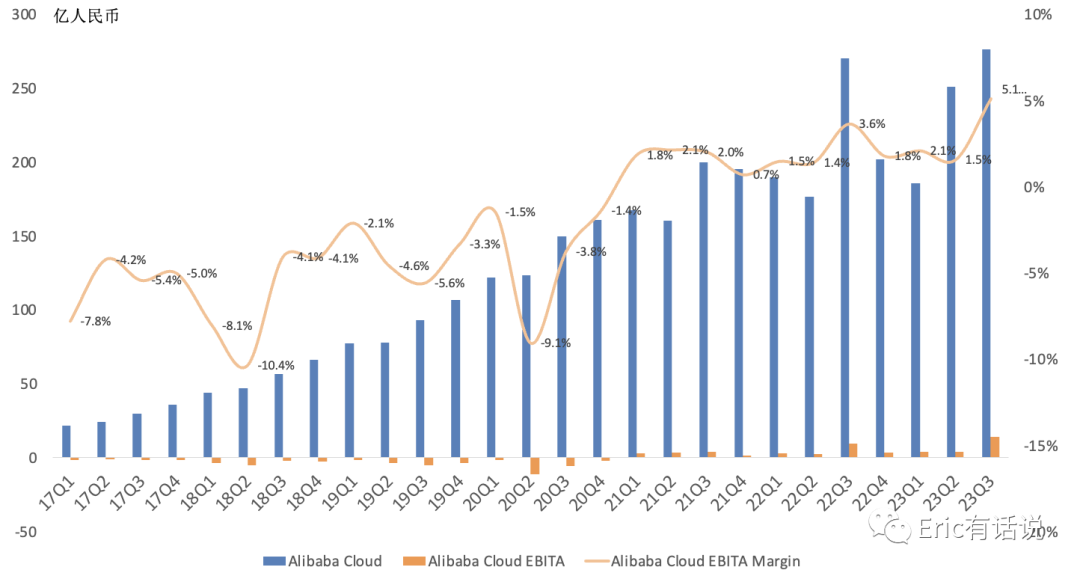

Alibaba Cloud

China's Cloud Leader

Q3 revenue RMB 27.6B ($3.789B), up 2% year over year; excluding internal consolidation, revenue down slightly year over year; revenue definition changed again (Cloud Intelligence Group = Alibaba Cloud, excluding DingTalk); highly anticipated spin-off IPO suspended. Official reason: primarily concerned about chip ban impact on future business.

Q3 EBITA profit RMB 1.409B, EBITA margin 5.1%, profitable for 11 consecutive quarters; margin improved significantly after excluding DingTalk; was DingTalk the main loss driver?

5

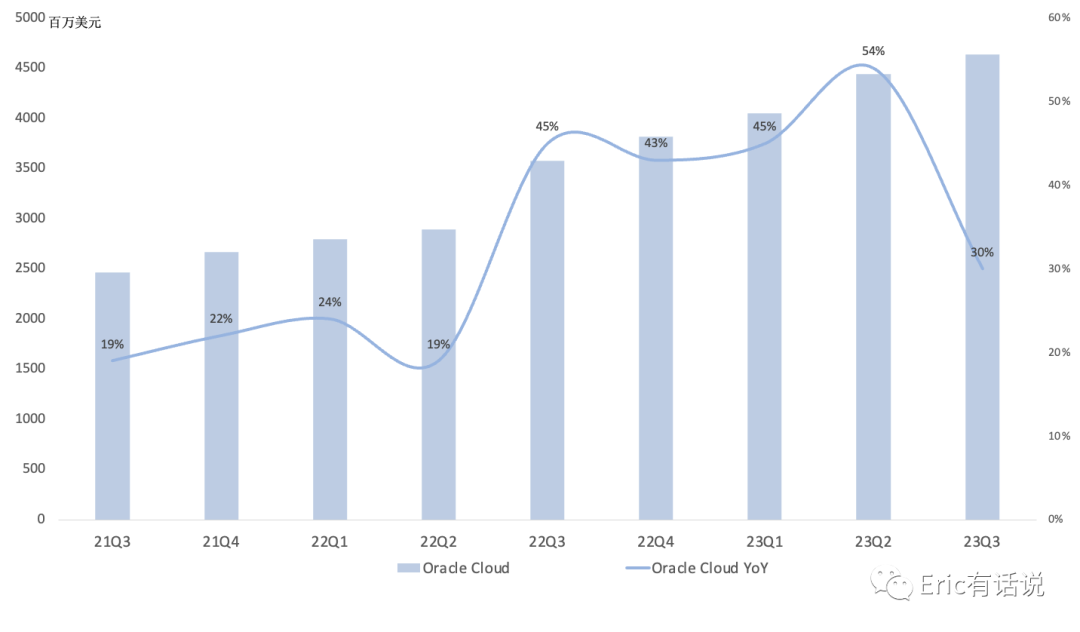

Oracle Cloud

Global cloud #4

Q3 revenue $4.635B, up 30% year over year; by scale should be the fourth-largest cloud globally; composition: $1.5B IaaS (YoY +66%) + $3.1B SaaS (YoY +17%); Oracle SaaS growth has notably slowed.

Oracle's cloud reporting is messy, composition complex, no direct profit disclosure; AI backlog $4B.

6

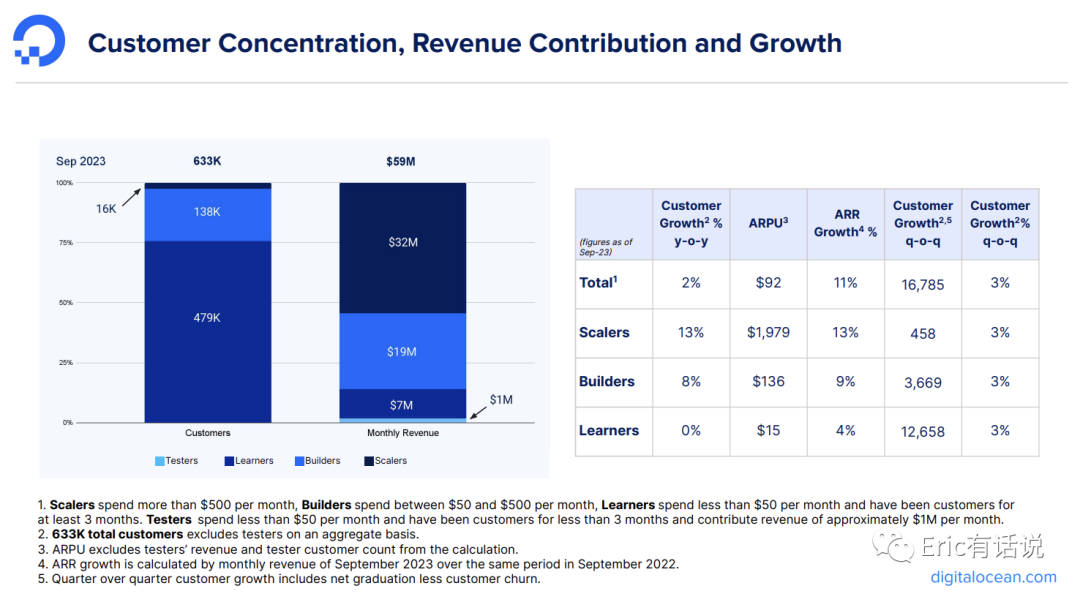

DigitalOcean

AWS for Everyone

Q3 revenue $177M, up 16% year over year; ARR $713M, up 11% year over year; gross margin 60%, down 4 percentage points year over year; operating income surged, operating margin 20%; monthly ARPU $92.06, up 6% year over year; Q4 revenue growth expected only 9% year over year.

Q3 EBITDA $75.8M, up 19% year over year; EBITDA margin 43%; concerning: Net Dollar Retention Rate continued to decline to 96%, new low since Q3 2020, falling below 100%.

DigitalOcean's hallmark is low sales expense ratio, 11% this quarter; long-term below R&D and G&A ratios, enabling profitability with decent margins. But the core problem is no growth, fatal for a small-scale company; Net Dollar Retention Rate persistently declining below 100%.

DigitalOcean's customer base is primarily SMBs, highly sensitive to macro cycles; although ARPU continues to rise, customer count has hit a growth ceiling. With the rise of AI cloud players like CoreWeave, the impact on traditional small cloud providers may just be starting.

Conclusion

Macro pressure persists; global Big 3 cloud growth diverging; AI intensifies cloud migration. Despite cloud giants still helping customers reduce costs, the broader SaaS sector has begun to bottom and rebound; coupled with cooling rate-hike expectations, a host of star SaaS names — SHOP, DDOG, ROKU, RBLX — surged post-Q3 earnings, including some that had blown up in Q2.

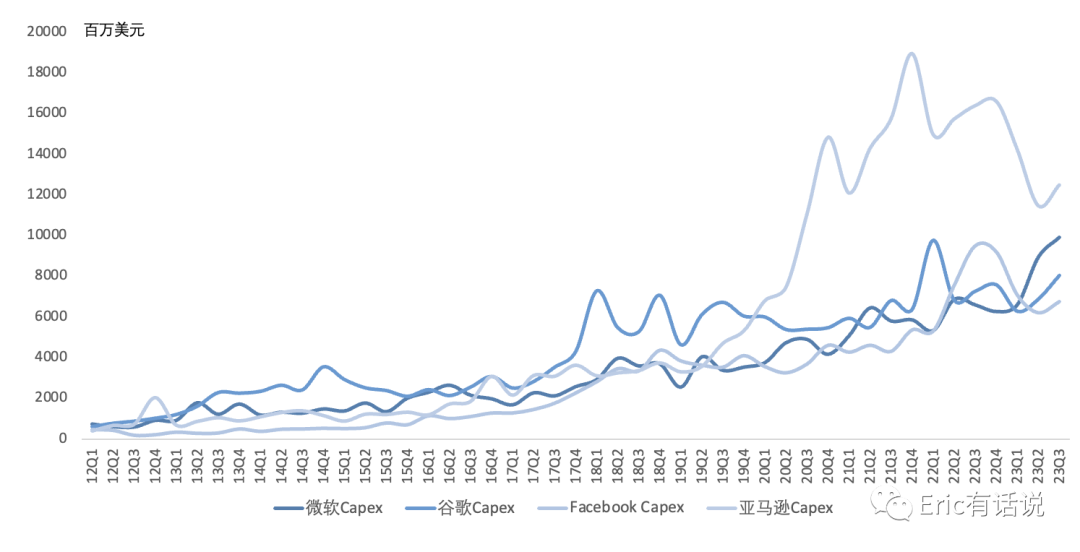

Macro downturn; cloud capex modestly recovering; FAMG Q3 total capex down 6.4% year over year, third consecutive quarter of year-over-year decline, but up 11% sequentially. As AI/ML heats up again, cloud capex concentration on GPU servers will continue to rise.

A side note: today's sudden OpenAI turmoil highlights internal divisions over AI development speed and commercialization, raising concerns about whether AI iteration pace will slow. In the past I might have struggled to understand — leaving money on the table, pursuing AGI for love? But now we are indeed living through a great technological era; ordinary people like me can only quietly watch the gods battle.