In the previous article "Global Cloud Giants Q4: Compute Shortage Constrains Growth, 2025 Capex to Increase Further," it was noted that all three global hyperscalers were constrained by AI compute shortages, with 2025 capex set to rise further. This quarter, cloud AI revenue continued to surge, non-AI demand recovered better than expected, and compute remains in short supply.

1

Amazon AWS

Global Cloud Leader

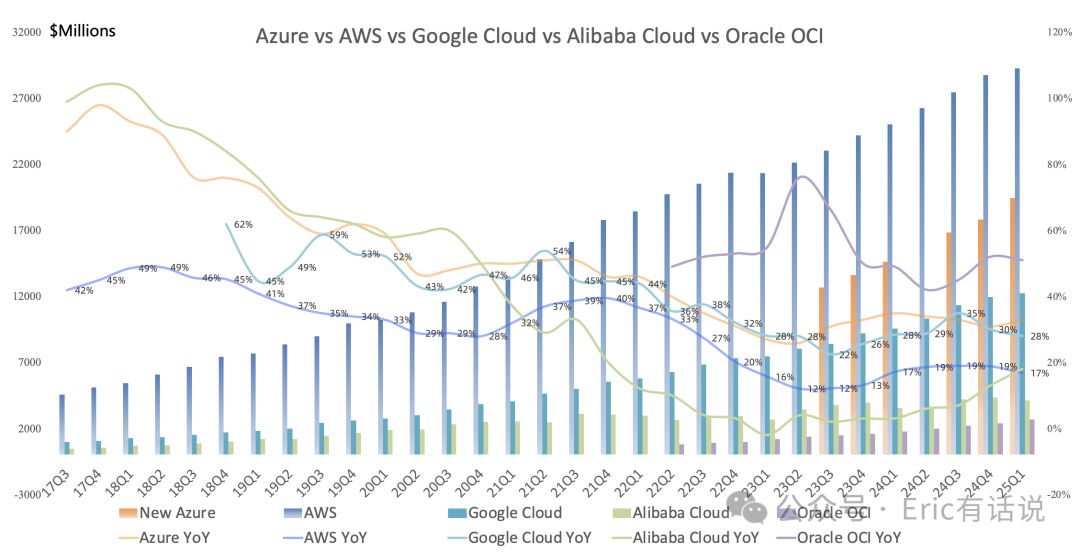

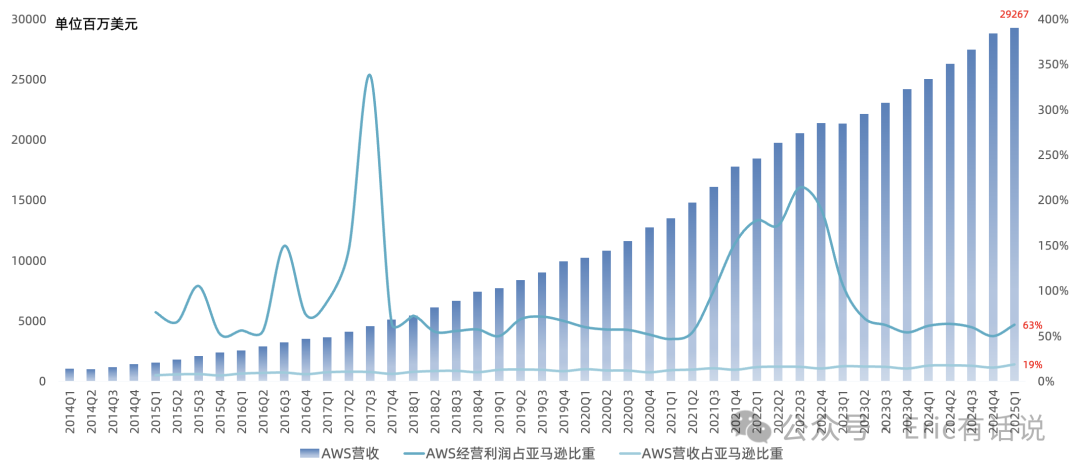

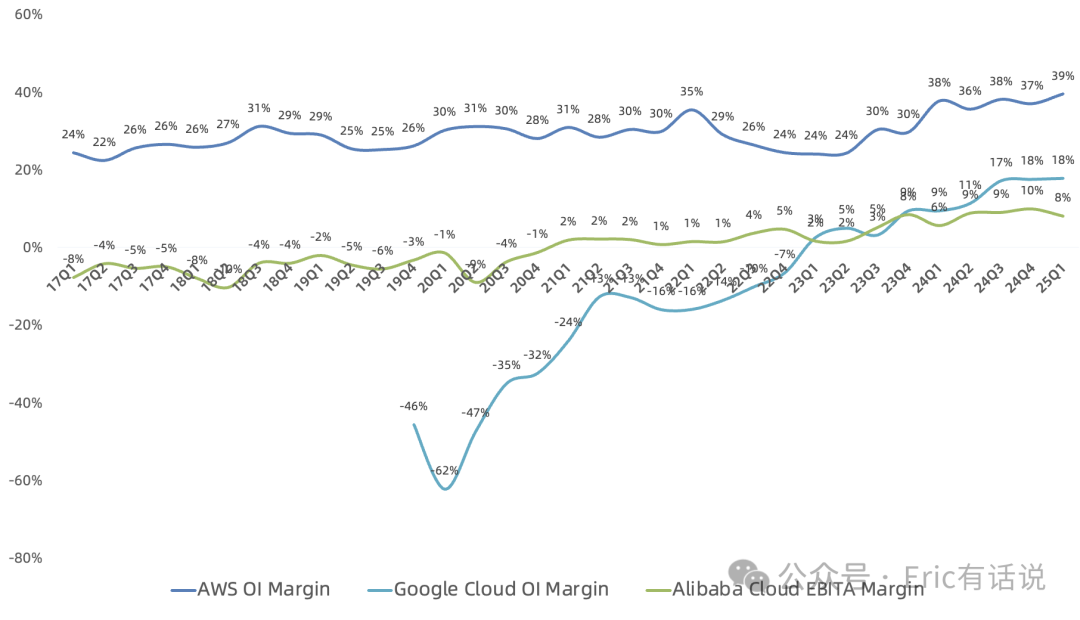

Q1 revenue was $29.267B, up 17% year over year, with the growth rate decelerating 2 percentage points sequentially, and up 2% sequentially; operating income was $11.547B, up 23% year over year, again reaching a record high, with an operating margin of 39%, up 1 percentage point year over year.

AWS Q1 revenue accounted for 19% of Amazon's total revenue and contributed 63% of Amazon's operating income.

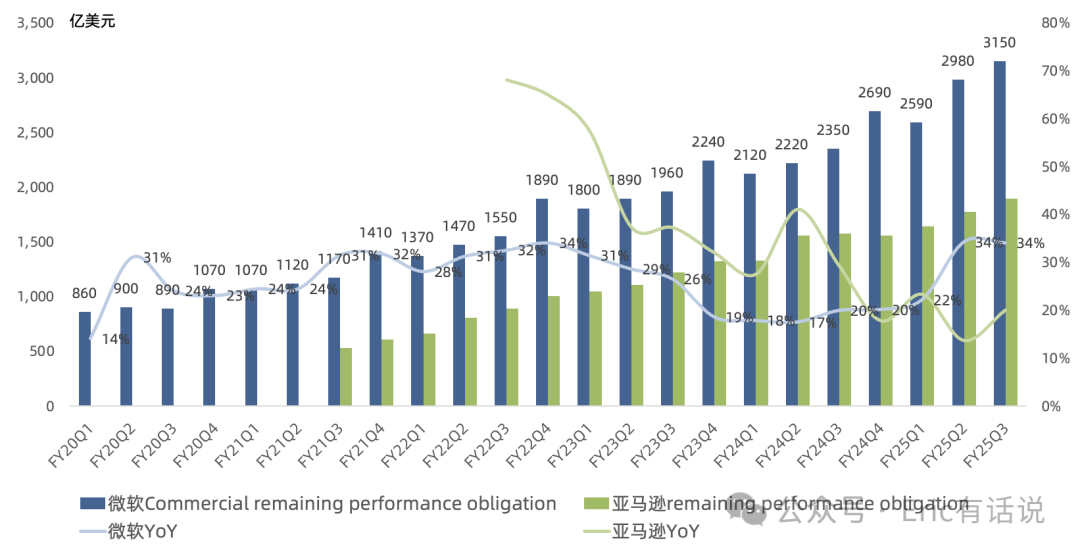

Q1 AWS revenue run rate was $117B, with growth in both AI and non-AI areas; AI revenue run rate reached multiple billions of dollars, maintaining triple-digit year-over-year growth; before generative AI emerged, management believed AWS ultimately had the opportunity to become a multi-hundred-billion-dollar business, and now management believes it could be even larger; plans to add more compute capacity in the second half of this year; currently the compute supply chain has some bottlenecks in motherboards and components, expected to be fixed over the next few months; RPO reached $189B, up 20% year over year, with an average remaining life of 4.1 years; currently over 85% of global IT spend is still used for on-premises deployment and has not yet migrated to the cloud.

Q1 capex was $24.3B, mostly invested in AI; maintaining full-year capex guidance of greater than $100B.

2

Microsoft Azure

Second-Largest Global Cloud

Microsoft Azure Q1 revenue was $19.476B, up 33% year over year, with the growth rate continuing to lead the global top three clouds.

The Intelligent Cloud business (Server + Azure + Enterprise Services) to which Azure belongs posted revenue of $26.751B, up 21% year over year, and operating income of $11.095B, up 14% year over year, both again reaching record highs; operating margin was 41%; Intelligent Cloud Q1 revenue accounted for 38% of Microsoft's total revenue and contributed 35% of Microsoft's operating income.

This quarter both Azure AI and non-AI revenue exceeded expectations, with non-AI revenue beating by a wider margin; AI contributed 16% ($2.3B) of Azure growth; going forward it will become more difficult to distinguish AI from non-AI workloads; reduced the lead time from receiving new GPUs to readiness by nearly 20%, improved AI performance by nearly 30% at the same power in mixed compute clusters, and cut cost per token by more than half; Azure AI Foundry processed over 100 trillion tokens this quarter, up 5x year over year, with a single-month record of 50 trillion tokens; SLMs represented by Phi have been downloaded over 38M times cumulatively; currently hundreds of thousands of customers use M365 Copilot, up 3x year over year, and this quarter saw a record number of customers purchasing more seats; Custom Copilot Studio now has over 230K companies using it, creating 1M custom agents this quarter, up 130% sequentially.

AI demand grew too fast this quarter, and AI compute supply shortages will persist after June; cloud migration continues to accelerate: traditional migration + database usage growth + cloud-native application growth; commercial RPO was $315B, up 34% year over year; expecting next quarter capex to increase sequentially, with FY25 H2 overall capex guidance unchanged.

3

Google Cloud

Third-Largest Global Cloud

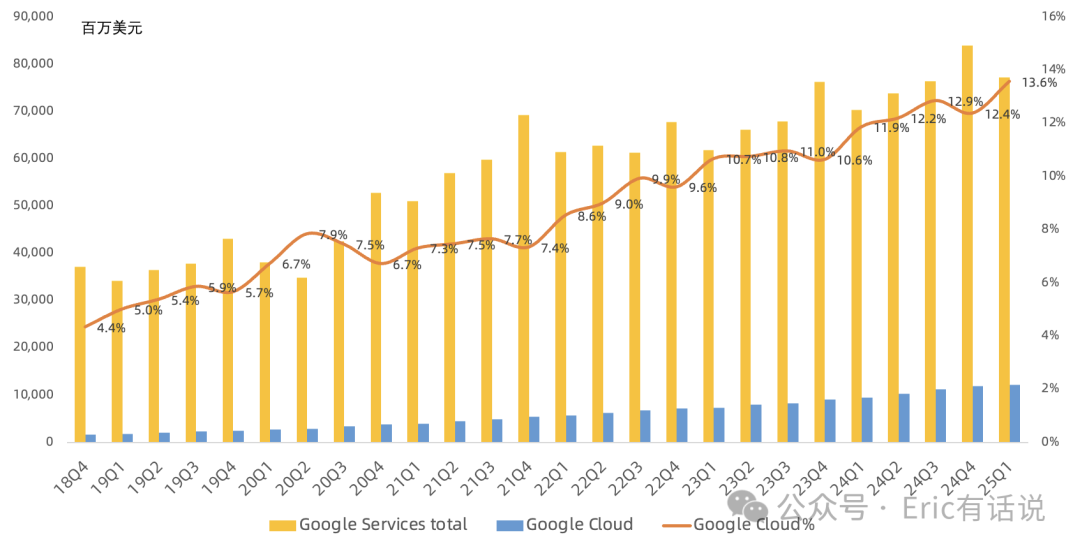

Google Cloud Q1 revenue was $12.26B, up 28% year over year, with the growth rate decelerating 2 percentage points sequentially, constrained by compute capacity; operating income was $2.177B, operating margin 18%, again reaching a record high.

Google Cloud's five core businesses: AI infrastructure, commercial AI platform Vertex, data platform BigQuery, AI cybersecurity solutions, Workspace office suite; this quarter GCP revenue growth significantly exceeded overall Cloud growth; the company was the first cloud provider to launch B200 and GB200, and will launch Vera Rubin in the future; year-to-date AI Studio and Gemini API active users grew over 200%; open-source Gemma models have been downloaded over 140M times cumulatively, AlphaFold is used by over 2.5M researchers; Gemini has been integrated into 15 Google products with monthly active users over 500M.

Management indicated Q2 Google Cloud revenue will still be constrained by compute supply; 2025 capex guidance of $75B unchanged.

4

Alibaba Cloud

China's Cloud Leader

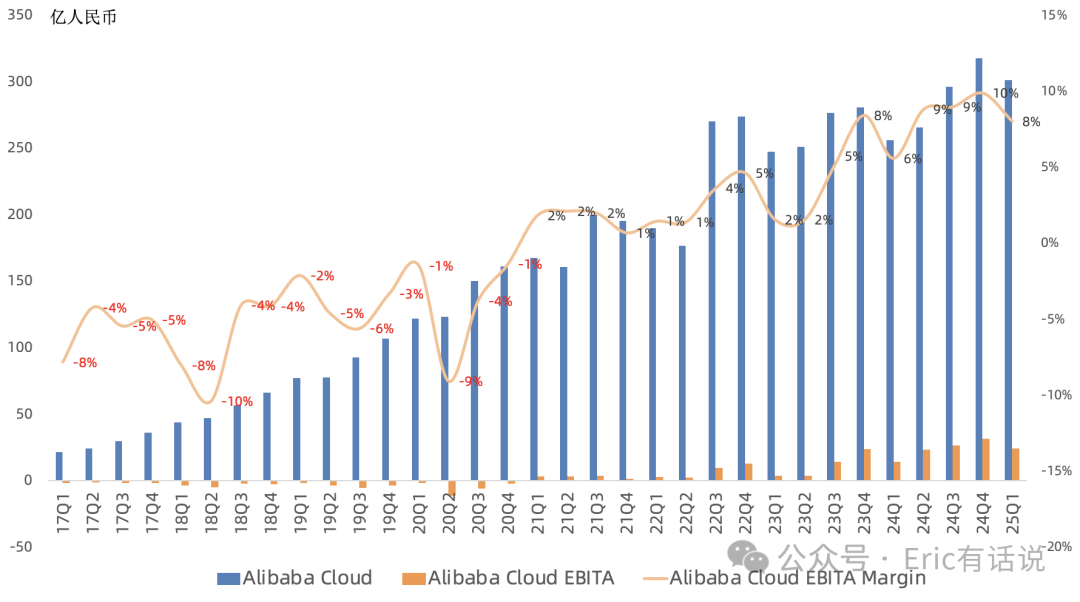

Q1 revenue was RMB 30.127B ($4.152B), up 18% year over year, marking the second consecutive quarter of double-digit year-over-year growth; excluding internal consolidation revenue, up 17% year over year; driven primarily by core public cloud business including AI, with AI-related revenue achieving triple-digit year-over-year growth for the seventh consecutive quarter.

Q1 EBITA profit was RMB 2.42B, up 69% year over year, EBITA margin 8%, driven by high-margin public cloud business including AI and efficiency gains. This quarter capex was RMB 24.6B, below market expectations, compared to RMB 31.4B last quarter; will subsequently assess risks of continuing to use Ascend chips.

5

Oracle Cloud

Global Cloud Challenger

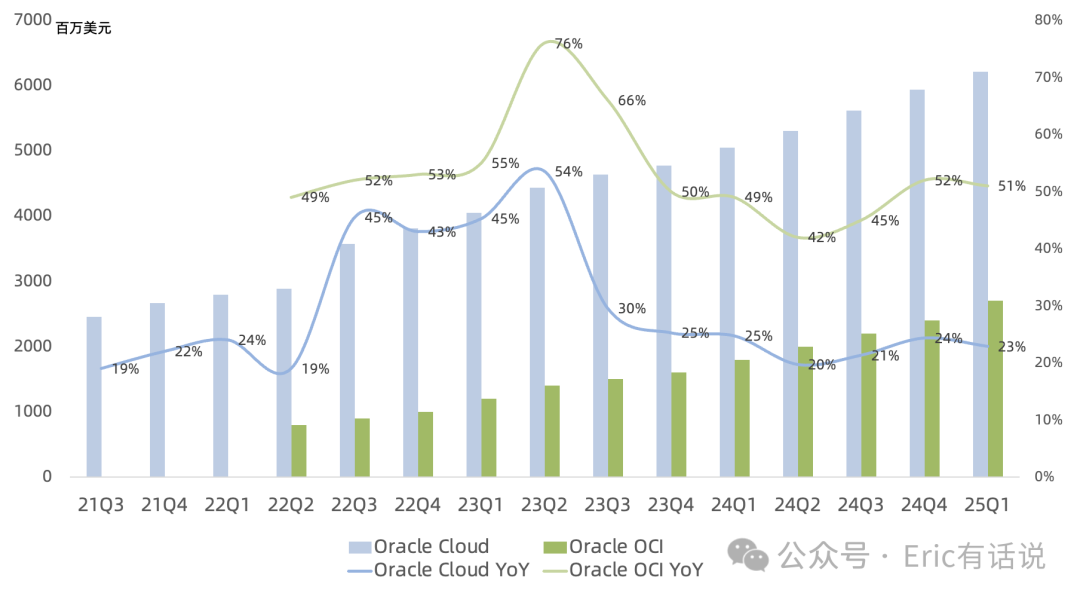

Q1 revenue was $6.21B, up 23% year over year, with the growth rate decelerating 1 percentage point sequentially; of which OCI (IaaS) revenue was $2.7B, up 51% year over year, SaaS revenue was $3.6B, up 10% year over year; this quarter IaaS gross margin and operating income continued to climb; expecting OCI to grow sequentially going forward; this quarter capex was $5.9B, FY25 capex approximately $16B, doubling year over year.

OCI consumption revenue up 57% year over year, of which GPU consumption for AI training TTM up 244% year over year, AI inferencing demand increased significantly; FY26 Q1 supply will improve significantly, FY26 OCI revenue year-over-year growth greater than 50%; compute supply to improve sequentially over the next two quarters; MultiCloud Database revenue from Azure/GCP/AWS up 92% year over year; RPO $130B (excluding Stargate), up 63% year over year, of which Cloud RPO up 90% year over year, accounting for 80% of total RPO.

Preparing to sign Stargate Phase 1 contract, expecting RPO to continue growing thereafter; Cloud major customers include OpenAI, xAI, Meta, NVIDIA, AMD; Oracle currently has 101 live cloud data centers globally, building a 64K liquid-cooled GB200 AI training cluster, expecting 2025 power capacity to double, and triple by end of FY26; to meet existing customers' rapidly growing demand, this quarter signed a multi-billion dollar order with AMD for a 30K MI355X cluster; Azure/AWS/GCP have launched 18 data centers, 40 in planning; OCI's advantages over other vendors are primarily standardization, automation, and data center coverage from small to large.

6

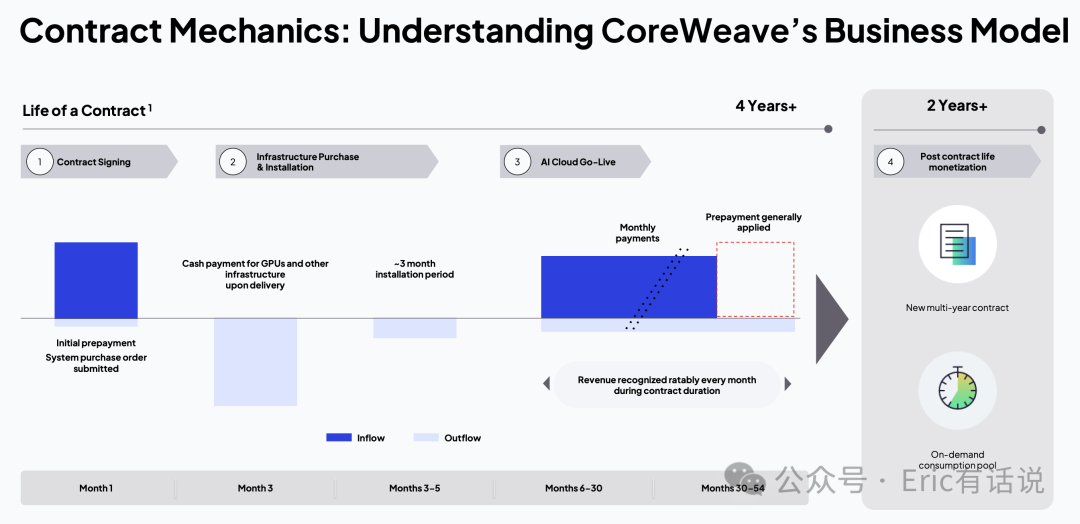

CoreWeave

AI NeoCloud

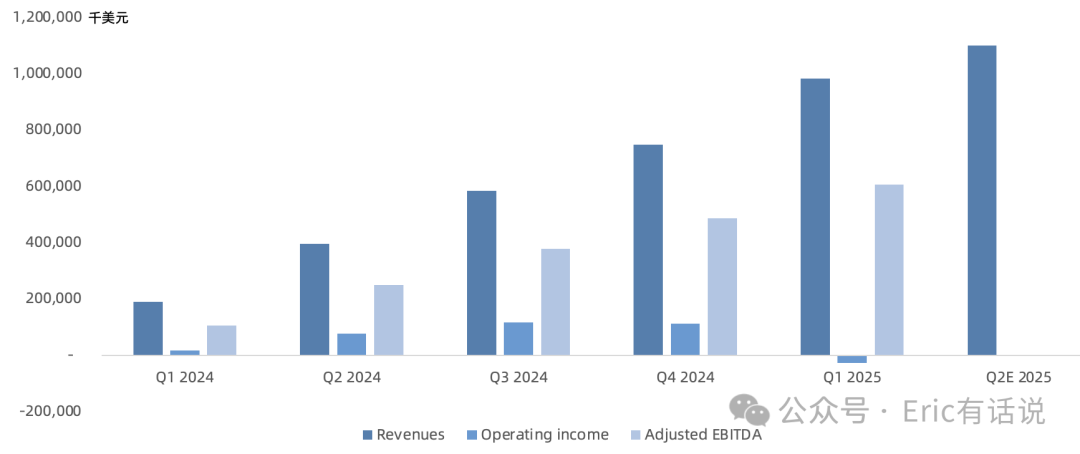

Q1 revenue was $982M, up 420% year over year; gross margin 73%, up 4.7 percentage points year over year, operating loss margin 3%; Q1 adjusted EBITDA profit $606M, EBITDA margin 62%; Q1 capex $1.9B, expecting full-year $20-23B, significantly exceeding revenue, combined with high leverage, the market questions its profitability.

Q1 RPO $25.9B, up 63% year over year, including $11.2B Stargate contract signed in March; the company currently has 33 data centers globally, with ~420MW available power and ~1.6GW contracted power; according to official materials, CoreWeave essentially operates on a 'build-to-order' or 'customer-funded capex' model, with data center capacity expansion directly linked to secured contracts and prepayments.

7

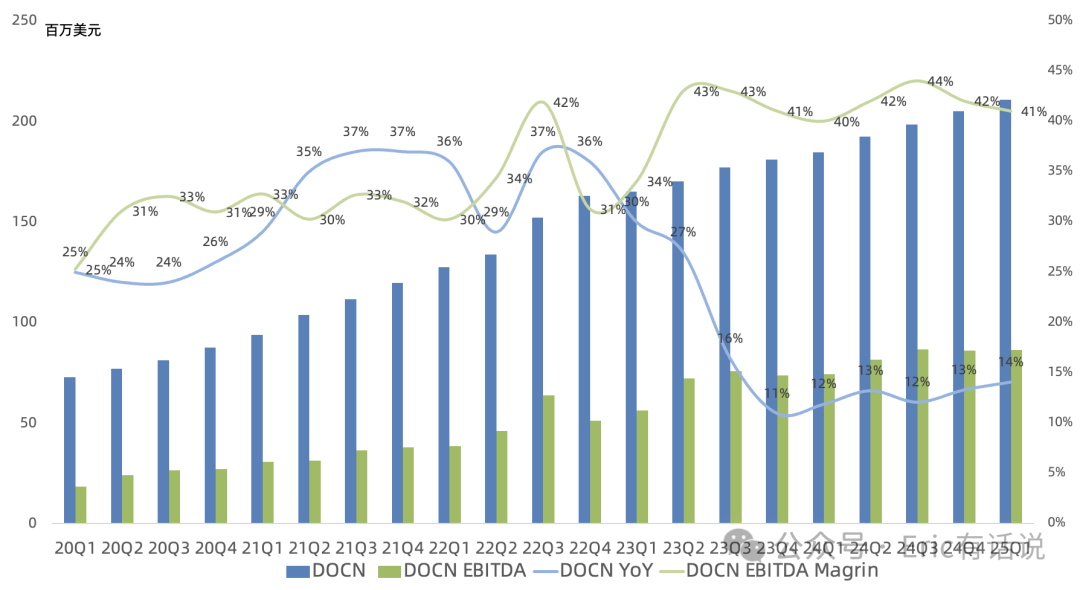

DigitalOcean

AWS for Everyone

Q1 revenue was $210M, up 14% year over year; ARR $840M, up 14% year over year, of which AI ARR up over 160% year over year; gross margin 61%, flat year over year, operating margin 18%; Monthly ARPU $108.56, up 14% year over year, continuing to grow sequentially; expecting 2025 full-year revenue up 12-14% year over year.

Q1 EBITDA profit $86.3M, up 16% year over year; EBITDA margin 41%; this quarter Net Dollar Retention Rate 100%, up 1 percentage point sequentially, first return to 100% since 2023 Q2.

DigitalOcean's distinct characteristic is that its customers are primarily SMBs, making it highly sensitive to macroeconomic cycles; although ARPU continues to rise, customer count growth is slow. Previously noted that in the AI cloud wave, facing the rise of new forces such as CoreWeave and Nebius, traditional small cloud company DigitalOcean may have been somewhat slow to act, only opening H100 instances to all customers on October 1 and launching its first AI product GenAI Platform in early November; currently H200 and MI300X instances are live, with over 5,000 customers deploying over 8,000 agents on the GenAI platform.

Conclusion

Cloud companies' capex exploded again this quarter, with FAMG Q1 total capex continuing to surge 62% year over year, down 3% sequentially. As cloud giants' compute demand increases dramatically, 2025 four-giant capex guidance continues to grow significantly; going forward, cloud companies' capex concentration on GPU servers will continue to rise, yet the market has consistently viewed this as overinvestment, while Amazon has consistently emphasized this scenario closely resembles the early days of the cloud computing era.