In the previous article "Global Cloud Giants Q3: Industry Recovery, AI Accelerates Cloud Migration," it was noted that despite cloud giants continuing to help customers optimize costs, the SaaS sector had begun to bottom out and rebound, and AI was intensifying cloud migration. With Alibaba's delayed earnings, the Q4 scorecards for all five global cloud giants are now in, with revenue growth rebounding and capex also warming up.

1

Amazon AWS

Global Cloud Leader

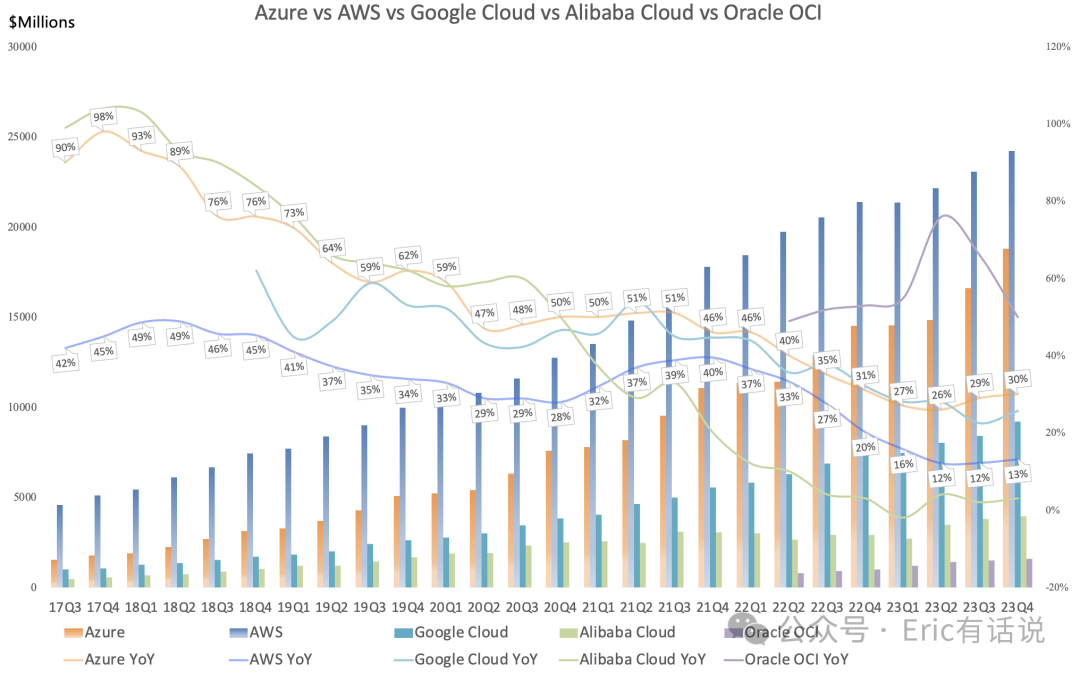

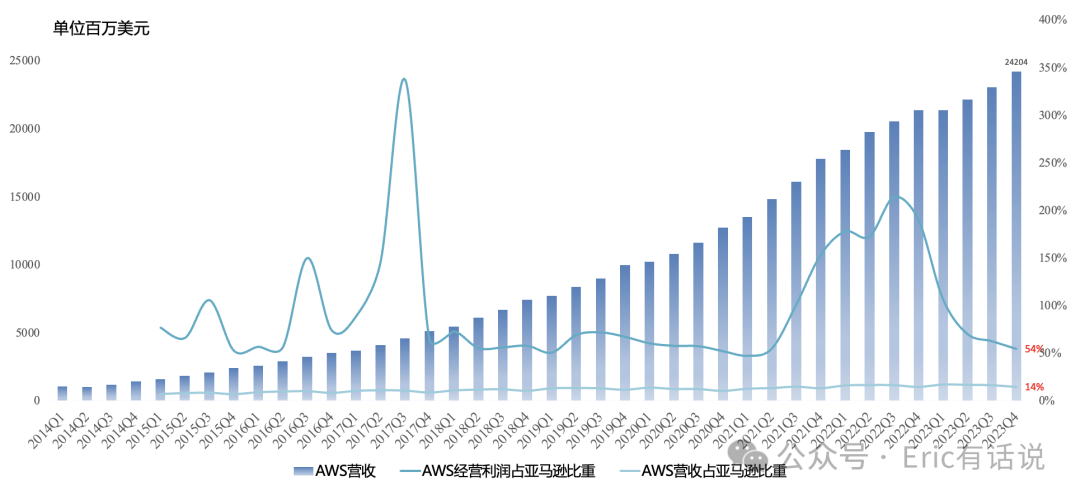

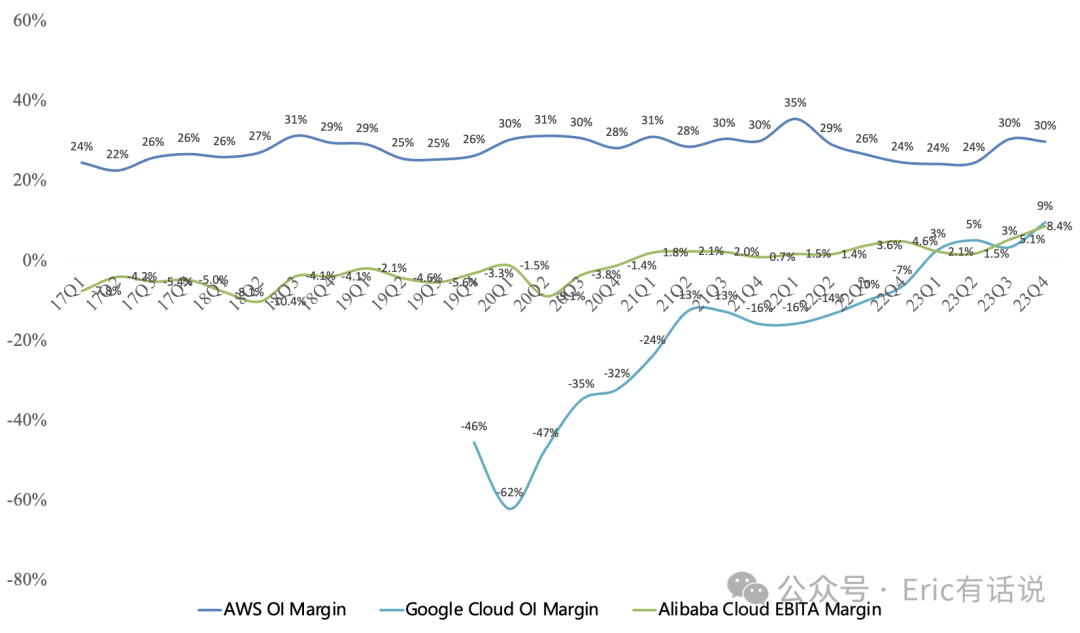

Q4 revenue was $24.204B, up 13% year over year, a 1-percentage-point acceleration, and up 5% sequentially; operating income was $7.167B, up 38% year over year, setting a record for the second consecutive quarter; operating margin was 30%, up 6 percentage points year over year. AWS margin improvement this quarter was primarily driven by cost optimization from layoffs and hiring slowdowns.

AWS Q4 revenue accounted for 14% of Amazon's total revenue, contributing 54% of Amazon's operating income.

Since Q3 last year, enterprises of all sizes began optimizing cloud spend, causing growth to decelerate; this trend weakened significantly this quarter; AI is intensifying cloud migration, and new large deals are growing. AWS 2024 growth is expected to be consistent with 2023 Q4 levels; committed backlog reached $155.7B; management expects GenAI revenue to reach tens of billions of dollars over the next few years.

2

Microsoft Azure

Second-Largest Global Cloud

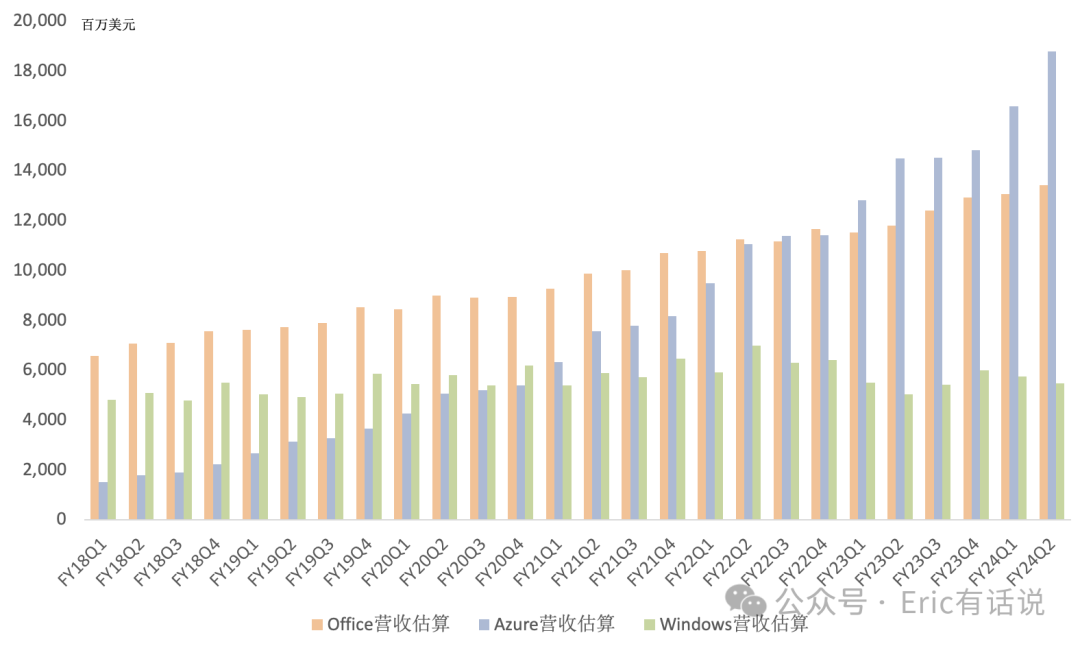

Q4 revenue was $18.8B, up 30% year over year, maintaining the fastest growth among the top three global clouds, and up 13% sequentially.

Azure's Intelligent Cloud segment (Server + Azure + Enterprise Services) operating income was $12.461B, up 40% year over year, setting a record for the fourth consecutive quarter; operating margin was 48%.

Intelligent Cloud Q4 revenue accounted for 42% of Microsoft's total revenue, contributing 46% of Microsoft's operating income.

Azure market share continues to rise. Azure AI customers exceed 53K, over one-third new. MaaS (Models as a Service) showing early results. Over half of Fortune 500 companies use Azure OpenAI Service. Azure deals above $1B continue to grow. Landed a 10-year, $1.5B deal with Vodafone. The AI services Azure provides are mostly inference; training is minimal. AI contributed 6% to Azure growth.

3

Google Cloud

Third-Largest Global Cloud

Q4 revenue was $9.192B, up 26% year over year, a 4-percentage-point sequential acceleration in growth. Operating income was $864M, operating margin 9%, a record high, with profitability achieved in every quarter of 2023.

Over 70% of AI unicorns are Google Cloud customers, including Anthropic, Character.ai, Essential AI, and Mistral AI; Vertex AI offers over 130 models; H2 API requests grew nearly 6x versus H1; Samsung S24 series uses Vertex AI; AI revenue contribution within GCP is increasing; Workspace revenue grew year over year, driven primarily by ARPU growth.

Cloud cost optimization is nearing completion in many regions; I previously wrote that a key 2023 watch item was Google Cloud's profit inflection, with year-end OPM above 10% seeming achievable and gradually approaching AWS's ~20% level over time, though Q3 margin fell short of expectations, pushing the 10% breach potentially into next year. Google Cloud's Q4 beat raises expectations for a 20% margin run-rate next year.

4

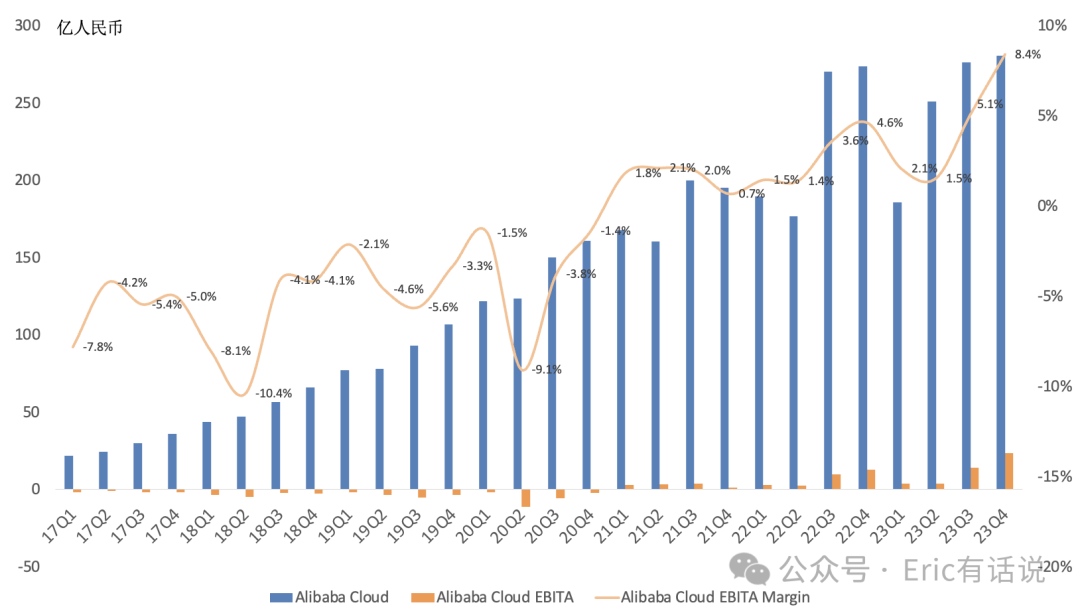

Alibaba Cloud

China's Cloud Leader

Q4 revenue was RMB 28.066B ($3.953B), up 3% year over year; excluding internal consolidation, revenue again declined slightly year over year; but public cloud and services revenue achieved year-over-year growth; Alibaba changed its reporting segment again (Cloud Intelligence Group = Alibaba Cloud, excluding DingTalk).

Q4 EBITA profit was RMB 2.364B, EBITA margin 8.4%, profitable for the 12th consecutive quarter; excluding DingTalk, margin improved significantly; DingTalk losses were indeed severe.

5

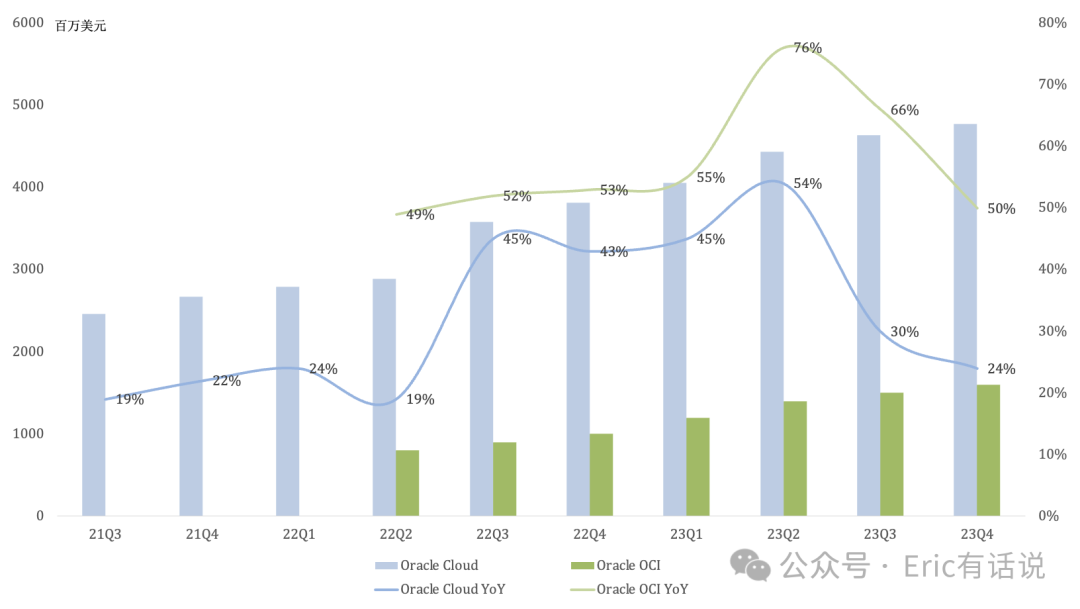

Oracle Cloud

Global cloud #4

Q4 revenue was $4.775B, up 24% year over year; excluding Cerner, revenue was $4.1B, up 24% year over year; OCI (IaaS) revenue was $1.6B, up 50% year over year; SaaS revenue was $3.2B, up 14% year over year.

Gen2 infrastructure cloud revenue grew 55% year over year, annualized run rate of $6B; OCI consumption revenue grew 71% year over year; RPO of $65B exceeds annual revenue; two $1B+ OCI deals expected to close by month-end; OCI expected to maintain 50%+ growth for the next several years with margins continuing to expand.

Oracle's cloud reporting is relatively messy, with a complex composition and no direct profitability disclosure.

Conclusion

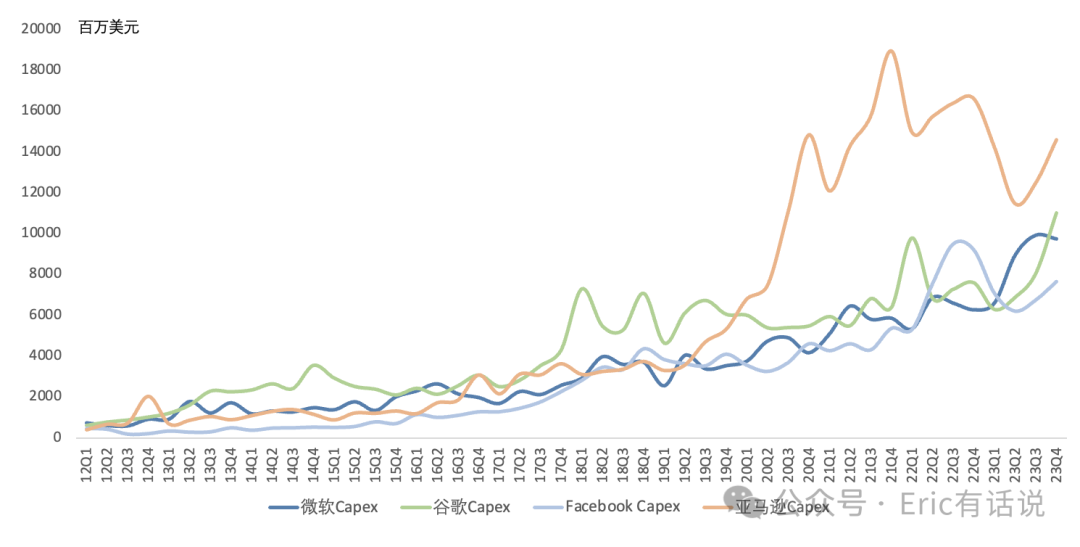

Cloud capex finally saw broad-based growth this quarter; FAMG Q4 capex grew 8% year over year to a record high, ending three consecutive quarters of decline, and grew 16% sequentially. As AI's contribution to cloud revenue growth exceeds expectations, future cloud capex concentration on GPU servers will continue to rise.

Finally, wishing everyone a happy Year of the Dragon.