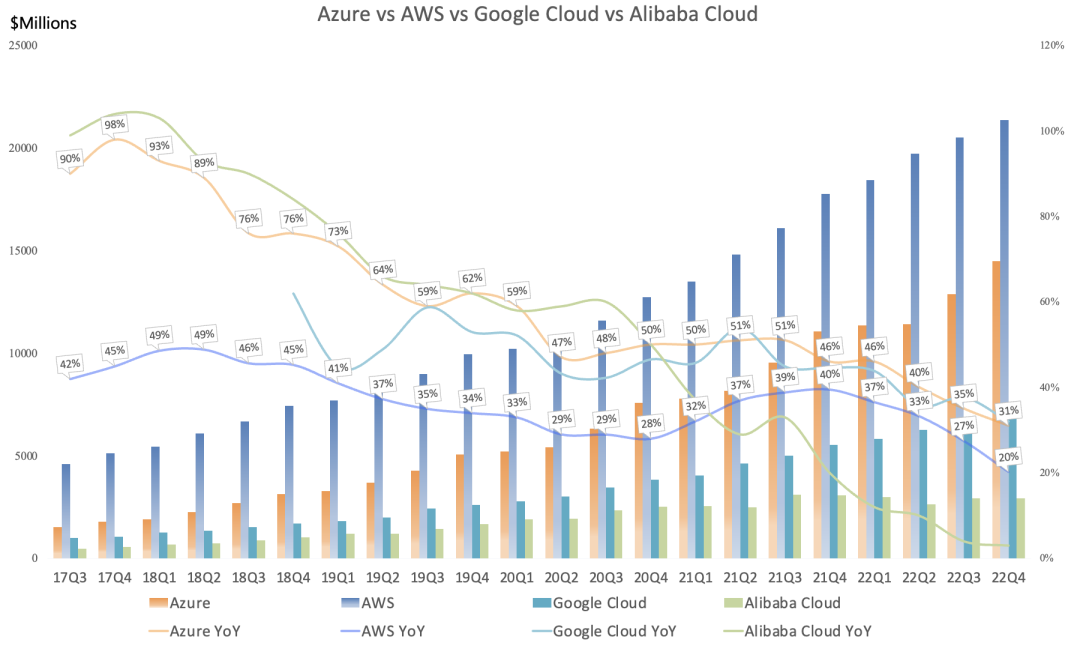

With Alibaba's belated report, the Q4 scorecards of the global top four cloud giants are now complete.

1

Amazon AWS

Global Cloud Leader

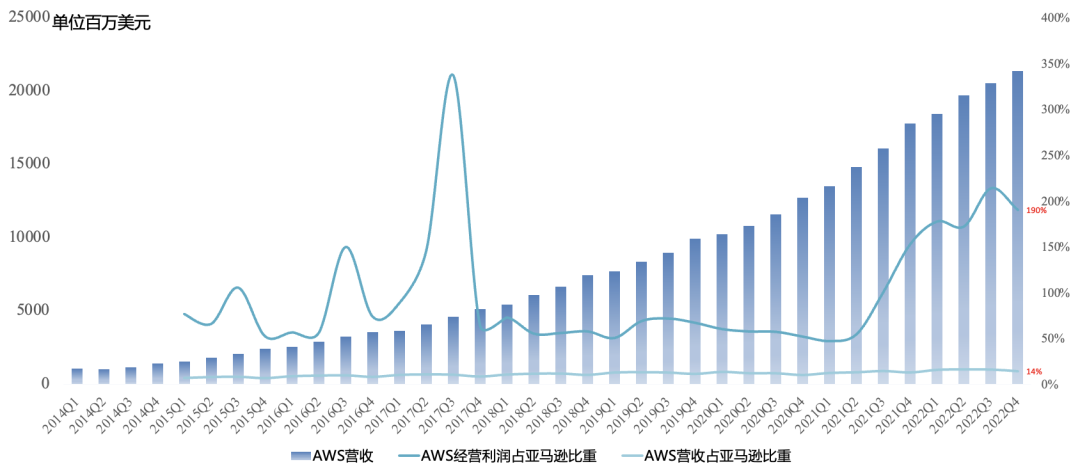

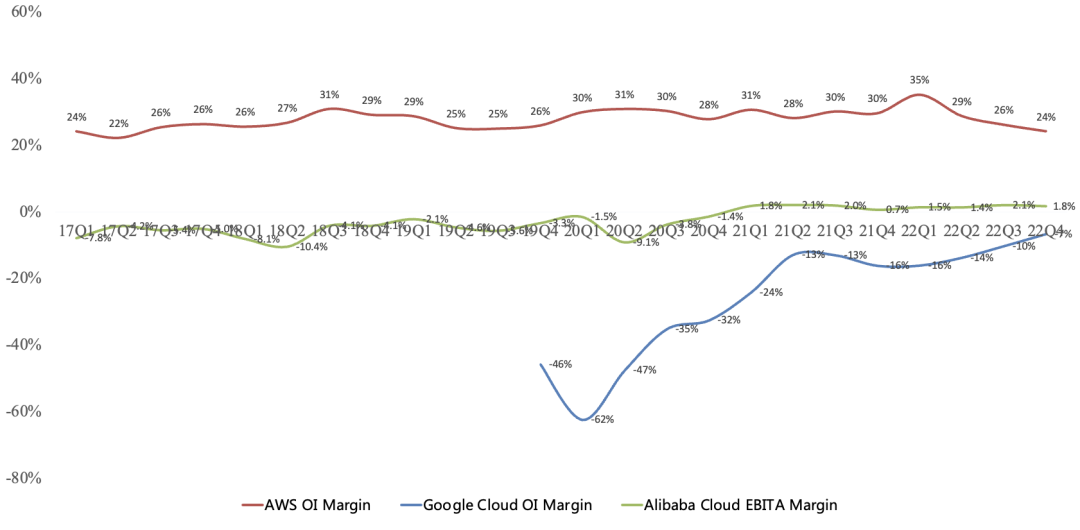

Q4 revenue $21.378B, up 20% year over year, maintaining sequential growth; operating income $5.205B, down 2% year over year; operating margin 24%, down 6 percentage points year over year.

AWS Q4 revenue represented 14% of Amazon total revenue but contributed 190% of Amazon's operating income.

2

Microsoft Azure

Second-Largest Global Cloud

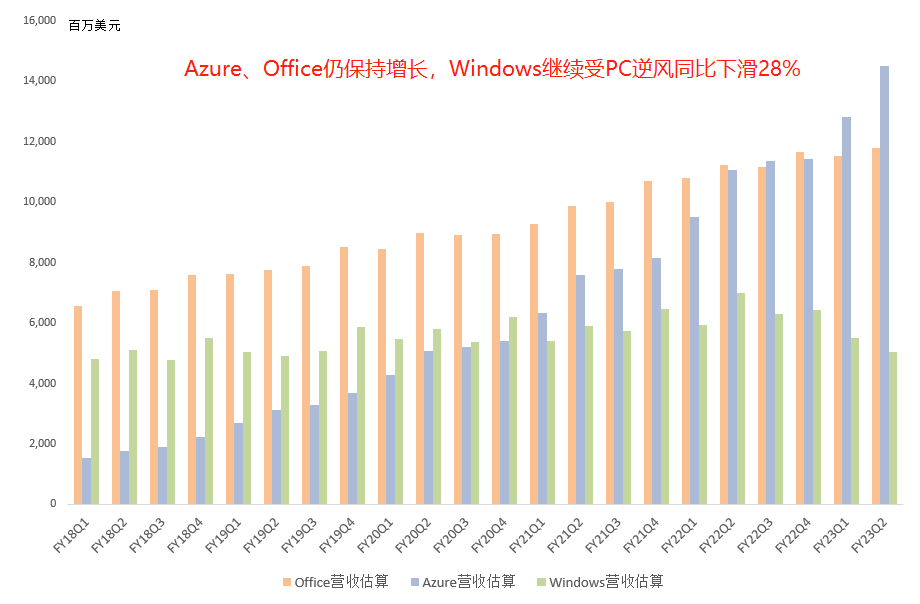

Q4 revenue $14.501B, up 31% year over year, growth continuing to decelerate;

Azure's Intelligent Cloud (Server + Azure + Enterprise Services) operating income $8.904B, up 9% year over year, down slightly sequentially, second-highest ever; operating margin 41%;

Intelligent Cloud Q4 revenue represented 41% of Microsoft total revenue, contributing 44% of Microsoft operating income;

This quarter Azure sequential revenue growth far exceeded expectations; first sequential decline may be pushed to next quarter.

3

Google Cloud

Third-Largest Global Cloud

Q4 revenue $7.315B, up 32% year over year, growth leading the global top four. Operating loss $480M, operating loss rate 7%, loss narrowing sharply, on track for profitability this year.

4

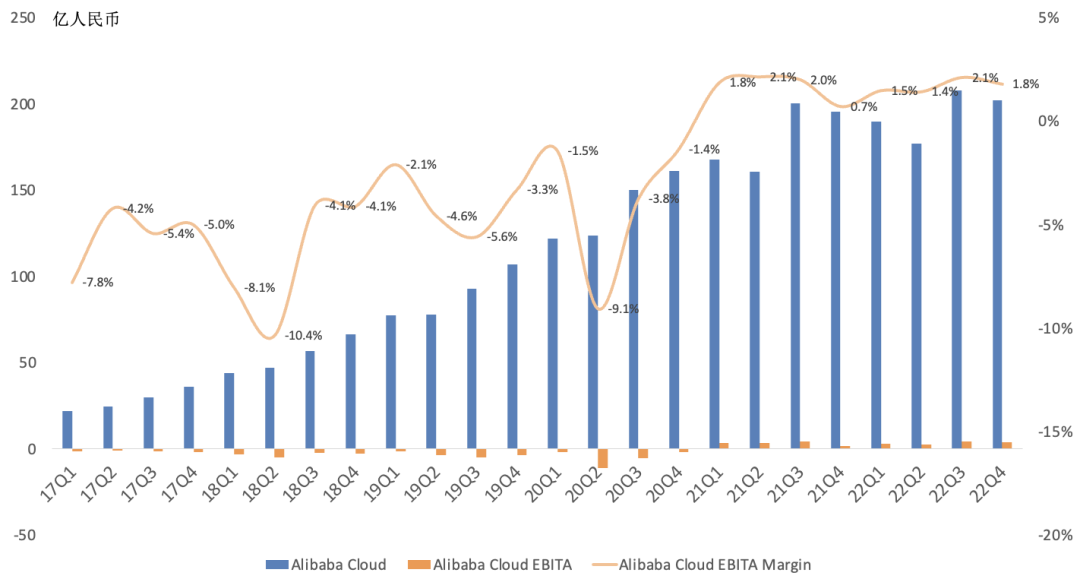

Alibaba Cloud

Global cloud #4

Q4 revenue RMB 20.2B ($2.925B), up 3% year over year (-5% USD), growth still trailing the global top four;

Q4 EBITA profit RMB 356M, EBITA margin 1.8%, eighth consecutive quarter of profitability, albeit EBITA basis and including DingTalk.

5

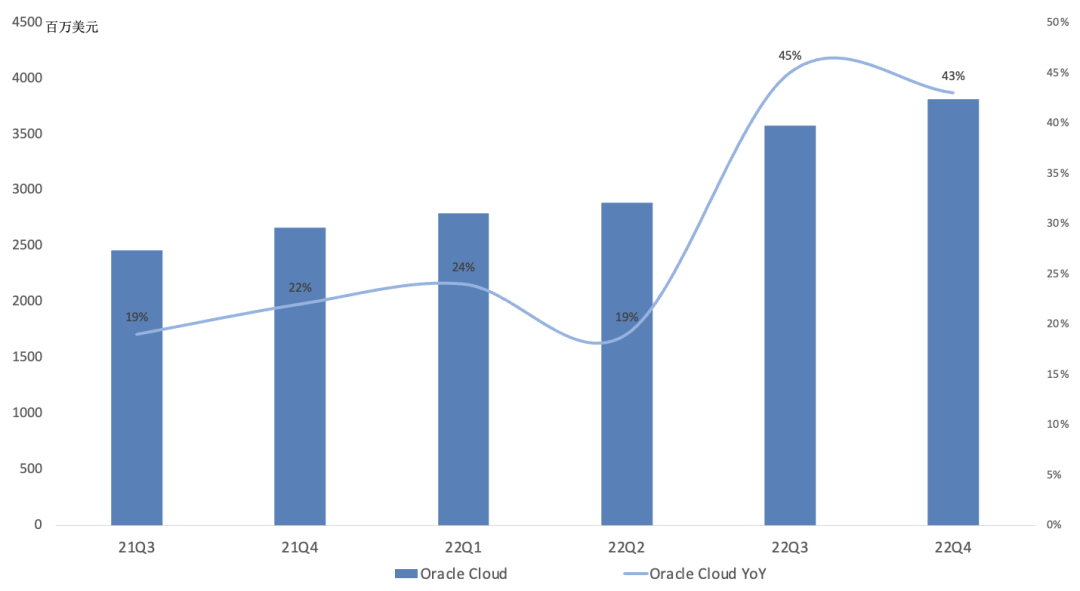

Oracle Cloud

Global Cloud Giants

Q4 revenue $3.8B, up 43% year over year; by scale it should rank ahead of Alibaba Cloud, but its disclosure is $1.0B IaaS (YoY +53%) + $2.8B SaaS (YoY +40%).

Oracle's cloud reporting is relatively messy, with a complex composition and no direct profitability disclosure.

6

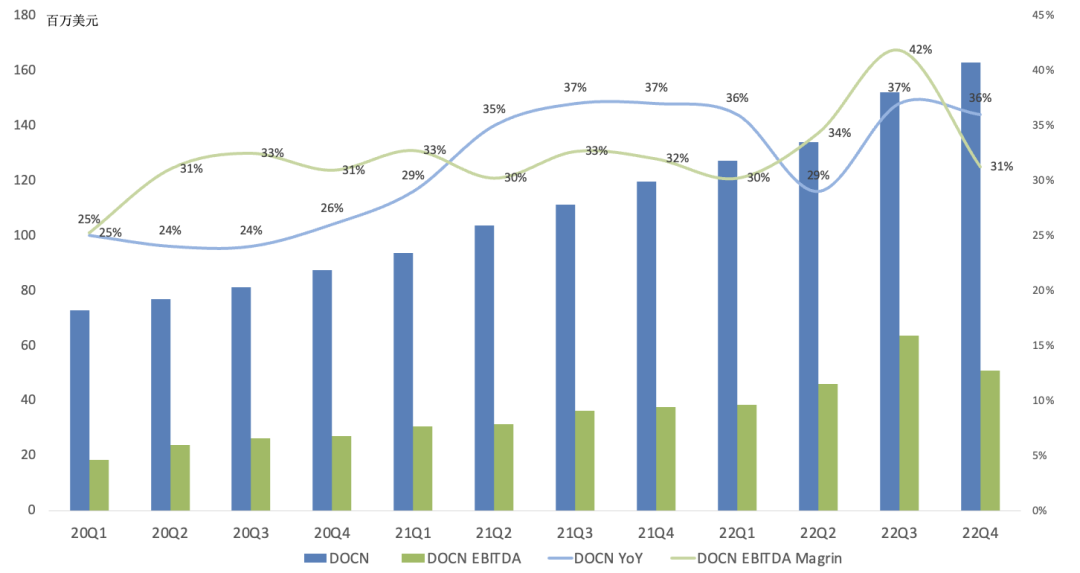

DigitalOcean

AWS for Everyone

Q4 revenue $163M, up 36% year over year; gross margin 61%, down nearly 2 percentage points year over year; operating income turned negative, operating margin -9%; Monthly ARPU $80.27, up 22% year over year.

Q4 EBITDA profit $50.98M, up 35% year over year, down slightly sequentially; EBITDA margin 31%, down 11 percentage points sequentially.

DigitalOcean's hallmark is a low sales expense ratio, only 15% of revenue; long below R&D and G&A ratios. This quarter's margin decline was mainly due to G&A up 48% year over year (from 28% to 31% of revenue) and sales expense up 64% year over year (from 13% to 15% of revenue).

DigitalOcean's clear trait is a predominantly SMB customer base, theoretically macro-sensitive, yet revenue grew steadily and ARPU kept rising. The company cites a sufficiently dispersed customer base and still-low cloud penetration, leaving ample runway.

Conclusion

Overall, the global cloud Big 3 continued to deliver steadily, but macroeconomic pressure is starting to show; against high comps, growth continues to decelerate, and cloud giants are all helping customers cut costs, pressuring margins. However, the industry remains a long-term beneficiary of digitalization and hybrid-cloud trends.

Macro downturn slowed cloud capex growth markedly, but capex remains at historical highs; FAMG Q4 average capex up only 13% year over year, consistent with NVIDIA's call that cloud customers tightened spending more than expected in Q4. However, with AI/ML heating up again, 2023 cloud capex could keep growing; the AI wave may drive a cloud recovery. We still believe sustained cloud prosperity is the most critical link in the data-center semiconductor boom.