TSMC raised its full-year revenue growth outlook again, while net margin surpassed Moutai's 2025 level.

TSMC Q1 Earnings:

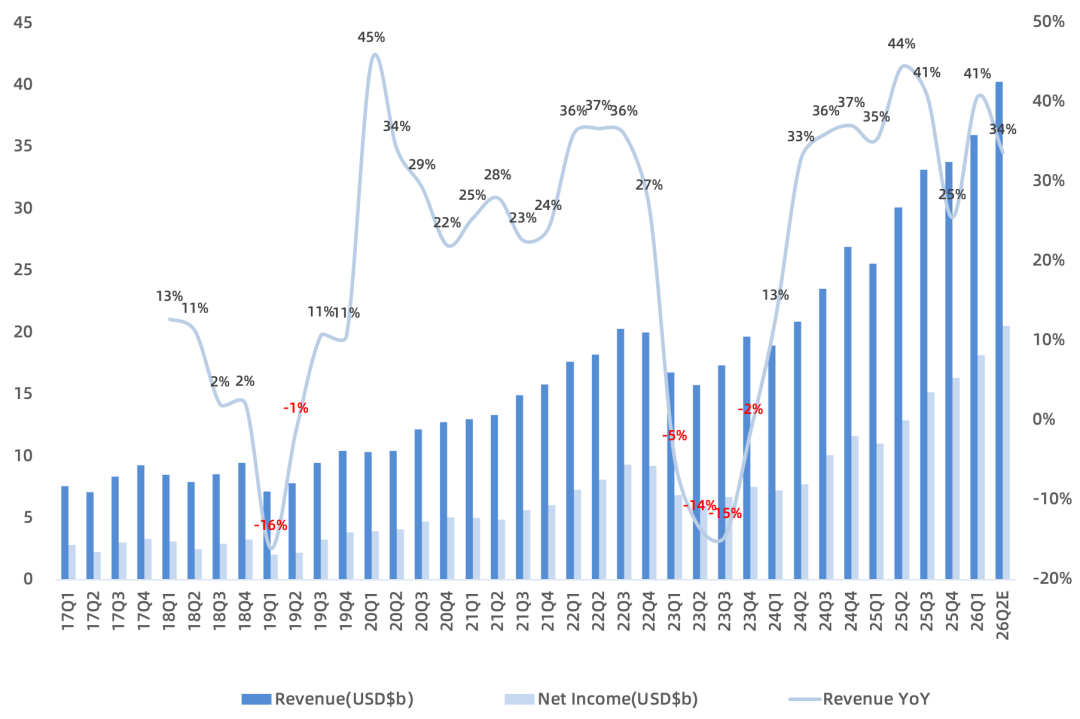

Revenue $35.9B in USD terms, up 41% year over year, up 6% sequentially, above guidance range of $34.6-35.8B, new all-time high; NT$1,134.1B in NTD terms, up 35% year over year, up 8% sequentially;

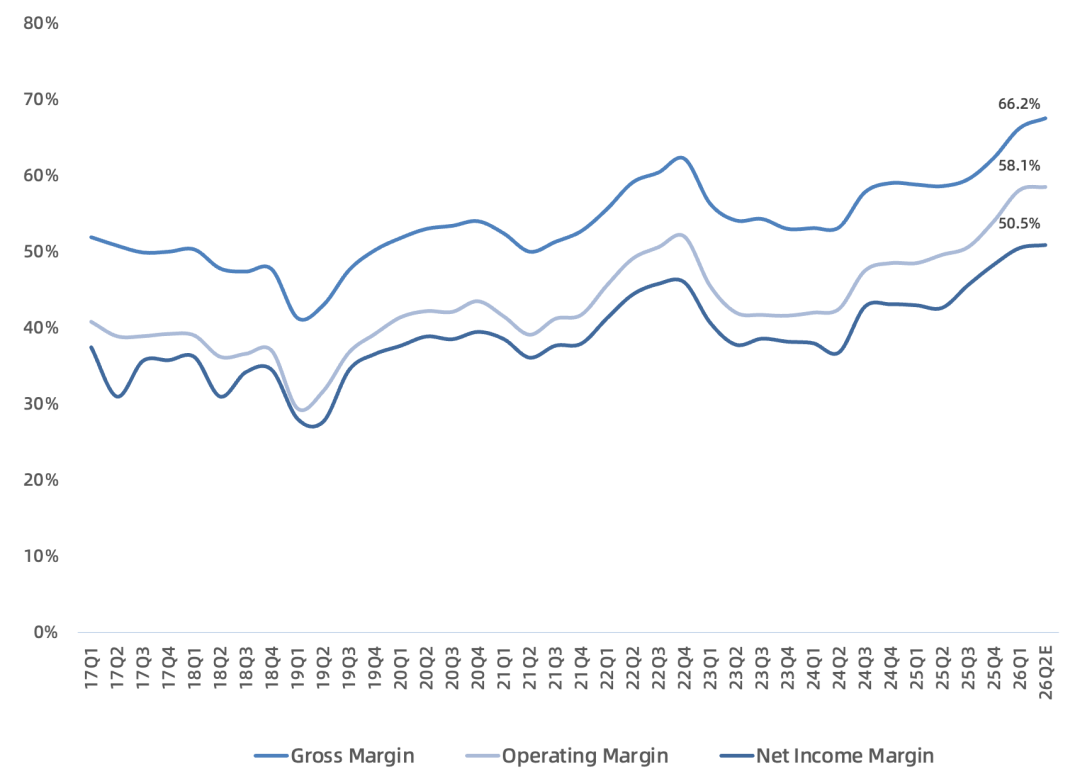

Gross margin 66.2%, up 7.4 percentage points year over year, up 3.9 percentage points sequentially, above guidance range of 63%-65%;

Operating margin 58.1%, up 9.6 percentage points year over year, up 3.9 percentage points sequentially, above guidance range of 54%-56%;

Net income $18.1B in USD terms, up 65% year over year, up 11% sequentially, net margin reached an extraordinary 50.5% for a manufacturer;

Equivalent 12-inch wafer shipments 4.174M (approx. 1.39M/month), up 28% year over year, 8th consecutive quarter of year-over-year growth, up 5% sequentially;

Capex $11.1B in USD terms, up 10% year over year;

By Process and Platform, Q1:

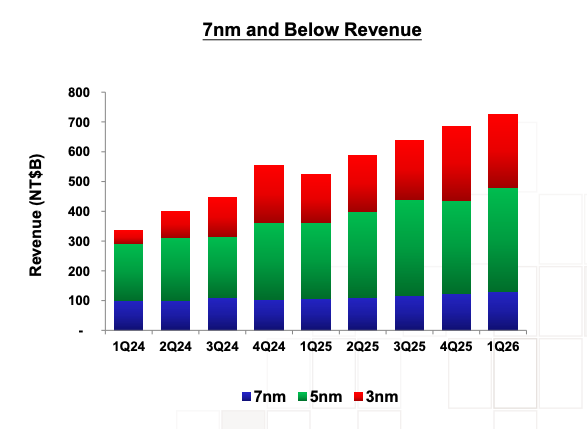

3nm 25% (Apple core node + Google TPU core node + Amazon Trainium3 core node + NVIDIA Vera Rubin core node), 5nm 36% (NVIDIA Hopper + Blackwell core node), 7nm 13%, 16/20nm 7%, 28nm 7%, 40/45nm 3%, 65nm 4%, 90nm 1%, 0.11/0.13um 1%, 0.15/0.18um 2%; advanced nodes 3nm/5nm/7nm 74%, 3nm/5nm combined 61%;

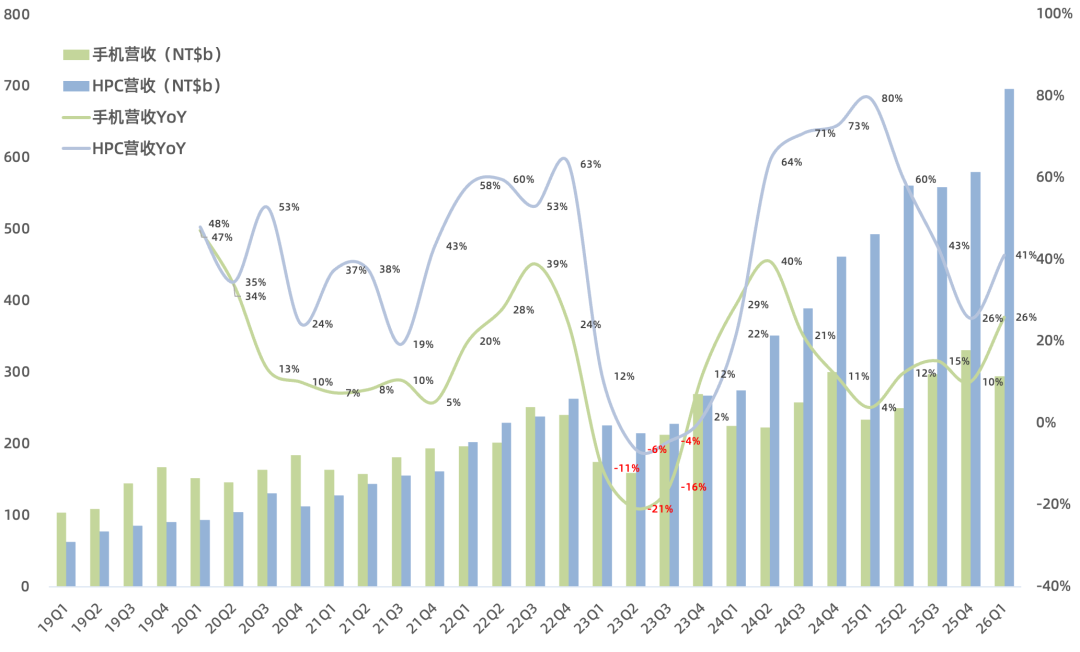

HPC 61%, smartphone 26%, IoT 6%, auto 4%; HPC share exceeds smartphone for 14th consecutive quarter, all-time high; HPC up ~41% year over year, up 20% sequentially; smartphone up ~26% year over year, down 11% sequentially; IoT up 12% sequentially, auto down 7% sequentially;

Outlook:

Guide Q2 revenue $39-40.2B, up 30%-34% year over year, still driven by strong AI; Q2 gross margin 65.5%-67.5%, operating margin 56.5%-58.5%, poised for new all-time highs;

Guide 2026 full-year USD revenue growth >30% year over year (raised), full-year capex at upper end of $52-56B range (raised); management continues to emphasize next three years' capex scale will significantly exceed past three years, but says future revenue growth will continue to outpace capex growth, capital intensity will not spike suddenly over the next few years;

3nm gross margin to exceed company average in H2; N2 entering early volume production, expect H2 to dilute gross margin by ~2%-3% for the full year; A14 R&D progressing well, strong interest from both smartphone and HPC customers, expect 2028 volume production; over the next few years, as overseas fabs ramp through early volume, gross margin diluted 2%-3%, later 3%-4%;

Guide AI revenue (GPU+ASIC+HBM controller) 2024-2029 CAGR near high 50s% (raised); management says AI orders stronger than seen last quarter; CPU increasingly important in AI data centers now, but cannot attribute CPU usage, so CPU not included in AI revenue calculation; advanced packaging capacity remains tight, still need OSAT collaboration;

TSMC historically would not continue expanding a process node after it reached full utilization, but now preparing to expand 3nm globally: Arizona Fab Phase 2 on 3nm, expect 2027 H2 volume; new Tainan 3nm fab in Taiwan, expect 2027 H1 volume; Japan Kumamoto second fab on 3nm, expect 2028 volume;

Memory price increases causing slight softness in smartphone and PC markets, but high-end smartphones performing well;

Collaborating with customer (NVIDIA) on next-gen LPU development, very confident in own technology position;

Building a new fab typically takes 2-3 years, subsequent volume ramp and yield improvement another 1-2 years, no shortcuts; expect capacity to remain tight through 2027;

Overall, as the gatekeeper of AI chip capacity, TSMC's every move tugs at the nerves of global AI thematic investing. Given the pronounced cyclicality of semiconductors, TSMC has historically been very cautious about capacity expansion plans unless it sees long-term, sustainable demand (such as this round of global 3nm expansion).

Given the current situation, management is likely to raise full-year guidance quarter by quarter, with full-year growth potentially challenging the 40% mark. We project TSMC's 2026 revenue reaching $170B and net income hitting $80B, implying a forward PE of under 22x at the current market cap.