Unlike ASML's guidance cut two days ago, TSMC raised guidance again. This once more confirms that large AI exposure is the winning formula, with the same script as Q1 and Q2.

TSMC Q3 Earnings:

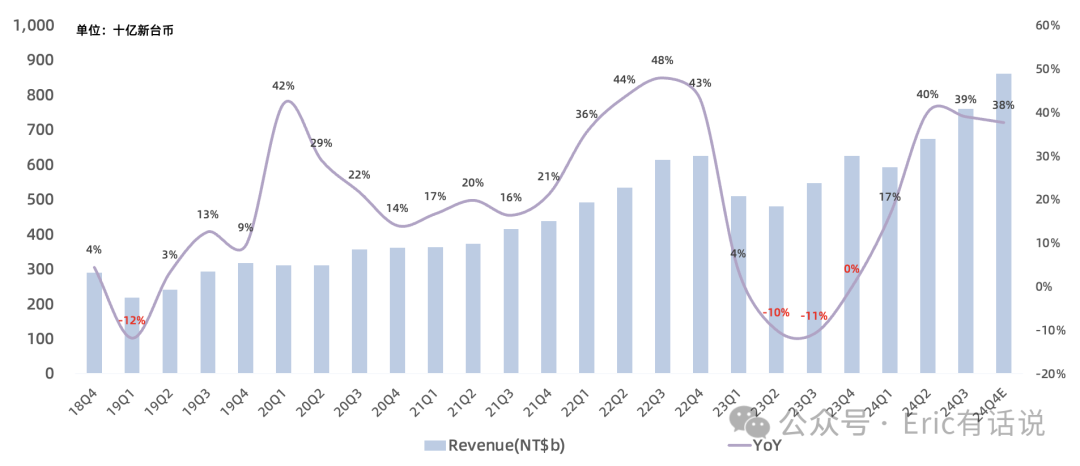

USD revenue was $23.5B, up 36% year over year and 13% sequentially. In NTD, revenue was NT$759.71B, up 39% year over year and 13% sequentially, both setting all-time highs for the second consecutive quarter.

Gross margin 57.8%, up 3.5 percentage points year over year and 4.6 percentage points sequentially.

Operating income was $11.16B in USD, up 55% year over year and 26% sequentially, an all-time high. Operating margin 47.5%.

Net income was $10.06B in USD, up 51% year over year and 31% sequentially, an all-time high. Net margin 43%.

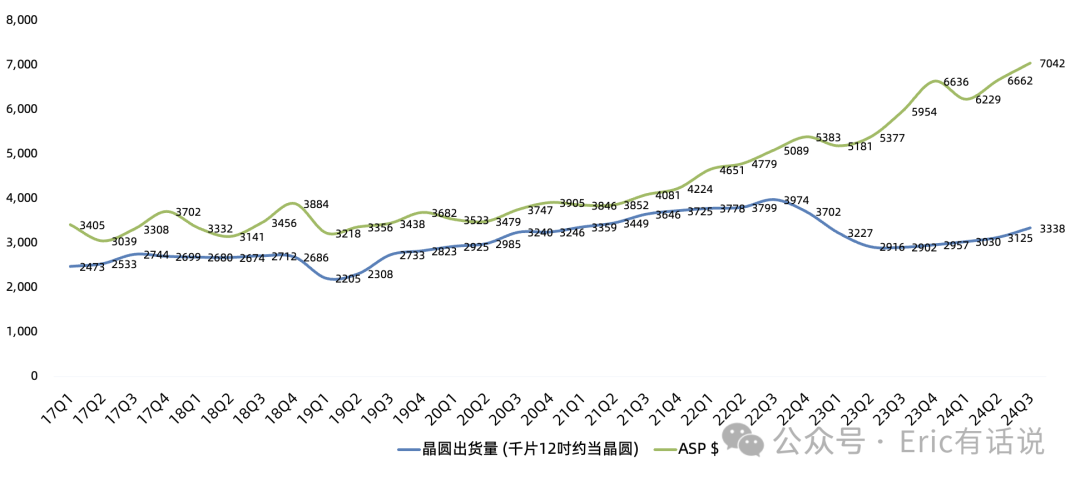

12-inch equivalent wafer shipments were 3,338K, up 15% year over year and 7% sequentially, the second consecutive quarter of year-over-year growth. ASP ~$7,042, up 18% year over year, the 19th consecutive quarter of year-over-year growth, setting a new all-time high.

Capex was $6.4B in USD, down 10% year over year. 2024 capex guidance revised from $30-32B to slightly above $30B.

Looking specifically at process technology and platforms in Q3:

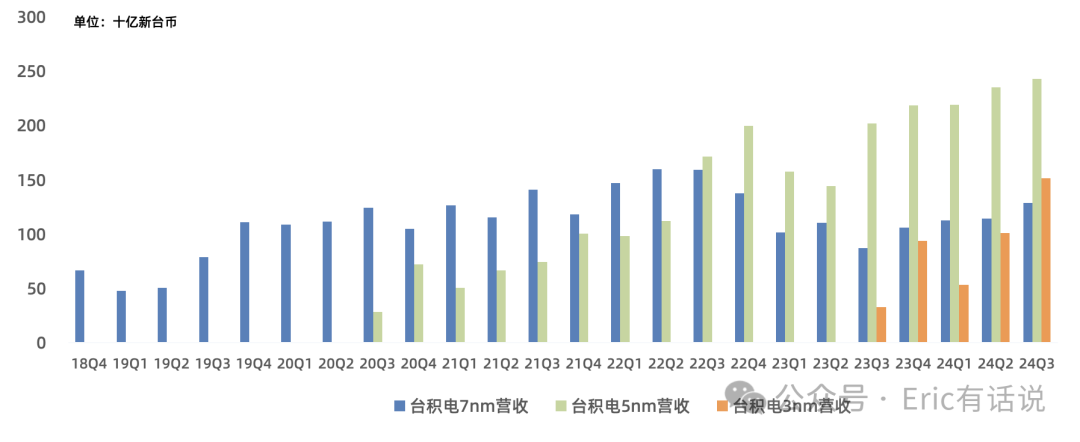

3nm 20%, 5nm 32%, 7nm 17%, 16nm 8%, 28nm 7%, 40/45nm 4%, 65nm 4%, 90nm 1%, 0.11/0.13um 2%, 0.15/0.18um 4%, 0.25um+ 1%. Advanced nodes (3nm/5nm/7nm) 69%, 3nm+5nm combined 52%, both new highs.

3nm revenue grew 50% sequentially, setting a new high for the second consecutive quarter. 5nm revenue grew 20% year over year, setting a new high for the fifth consecutive quarter.

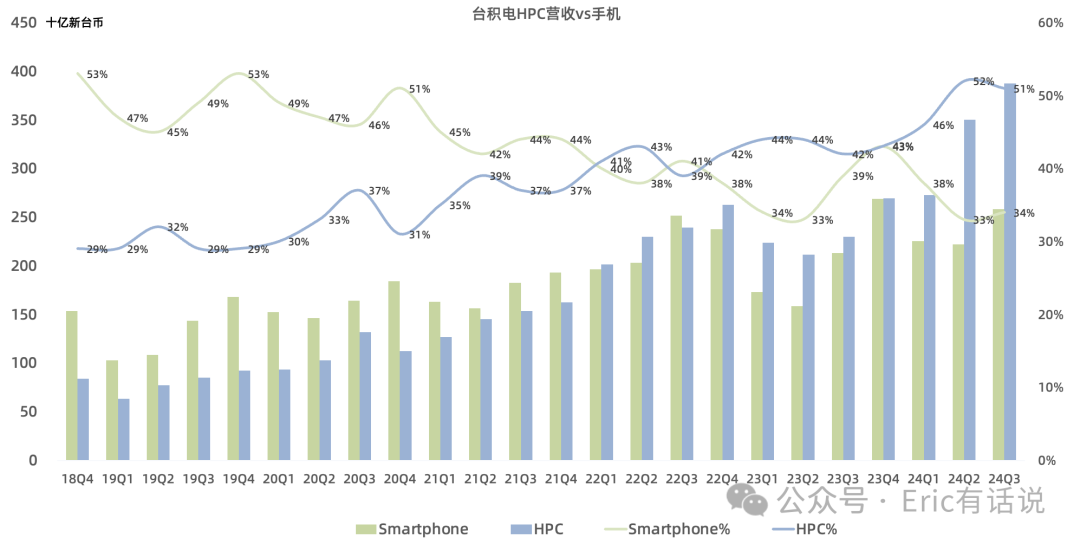

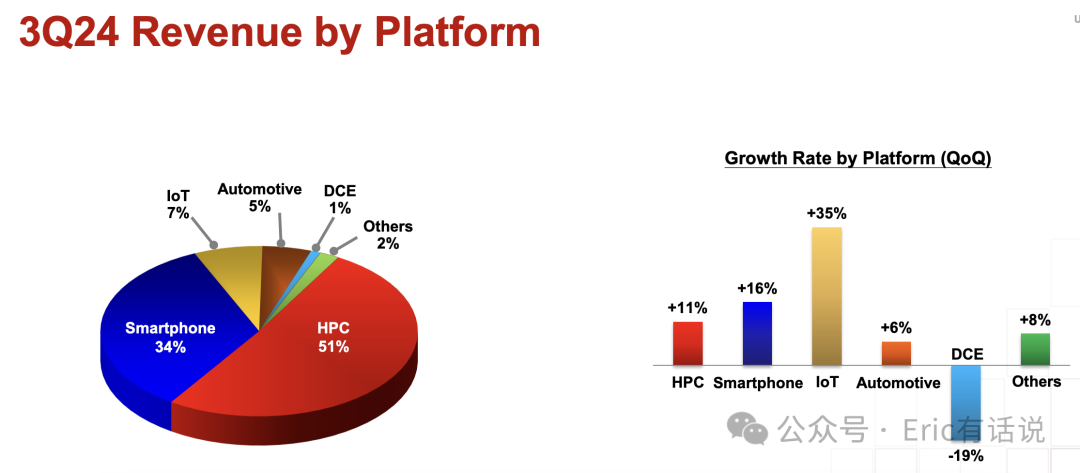

HPC 51%, Smartphone 34%, IoT 7%, Auto 5%. HPC has exceeded smartphone for eight consecutive quarters. HPC grew 11% sequentially; smartphone grew 16% sequentially on new model launches; IoT grew 35% sequentially; auto grew 6% sequentially. I believe NVIDIA is on track to replace Apple as TSMC's largest customer this year, pending verification in the annual report.

Outlook:

Guides Q4 revenue $26.1-26.9B, up 33%-37% year over year, setting another all-time high. Driven by AI-related demand, Q4 N3 and N5 overall utilization is expected to rise further. 2024 full-year USD revenue growth raised from 24%-26% to 30%. Q4 gross margin 57%-59%, operating margin 46.5%-48.5%, benefiting from AI-driven utilization improvement.

TSMC raised its 2024 "foundry 2.0" market share from 28% last quarter to 30%.

Guides 2024 AI-related revenue to grow 3x year over year, with revenue share raised from low-teens% to mid-teens% ($12.5-14.4B). Over the next four years, share will rise to 30%. 2024 advanced packaging revenue share in high-single digits ($6.3-8.1B), with growth over the next five years expected to exceed the company average.

Enterprise AI adoption improves efficiency and quality. At TSMC, a 1% efficiency gain translates to ~$1B in benefit. TSMC will not be the only beneficiary of AI. AI demand is extremely strong and just beginning.

Projects overall semiconductor industry (ex-memory) revenue growth ~10% year over year (unchanged). Non-AI semis are starting to improve.

US Arizona Fab 1 (N4) targets volume production in early 2025. April trial production yields were very high. Fab 2/3 target 2028/2030 volume production with processes more advanced than N4. Japan Kumamoto Fab 1 (28/22/16/12nm) has completed all process qualifications. Fab 2 (focused on consumer electronics/auto/industrial/HPC) begins construction in 25Q4, targeting volume production by end of 2027. Germany auto/industrial fab targets volume production by end of 2027.

Projects 2025 global PC and smartphone low-single-digit growth, driven mainly by silicon content increase.

Will not acquire Intel fabs; will continue to receive sizable orders from Intel.

N2/A16 nodes see very high HPC demand. Chiplet will not affect N2/A16 demand.

Projects 2025 capex higher than 2024.

Overall, TSMC remains very steady. HPC stays strong, full-year guidance raised again, once more confirming that large AI exposure is the winning formula. The downstream semiconductor market still shows only AI demand booming, with other segments awaiting recovery.

At the top end of full-year guidance, TSMC's annual revenue would be $90.1B, net income $36.2B, implying a 30x PE at a trillion-dollar market cap.