Unlike ASML's weak Q1 earnings yesterday, TSMC delivered a satisfactory report. Once again proving that large AI exposure is the winning formula.

TSMC Q1 Earnings:

Revenue in USD was $18.87B, up 13% year over year, down 4% sequentially, ending four consecutive quarters of year-over-year decline. In NTD, revenue was NT$592.64B, up 17% year over year, down 5% sequentially, marking the second consecutive quarter of year-over-year growth.

Gross margin was 53.1%, down 3.2 percentage points year over year, up 0.1 percentage point sequentially; earthquake impact was 0.5 percentage points.

Operating profit in USD was $7.93B, up 4% year over year, down 3% sequentially; operating margin 42%.

Net income in USD was $7.17B, up 5% year over year, down 4% sequentially, ending five consecutive quarters of year-over-year decline; net margin 38%.

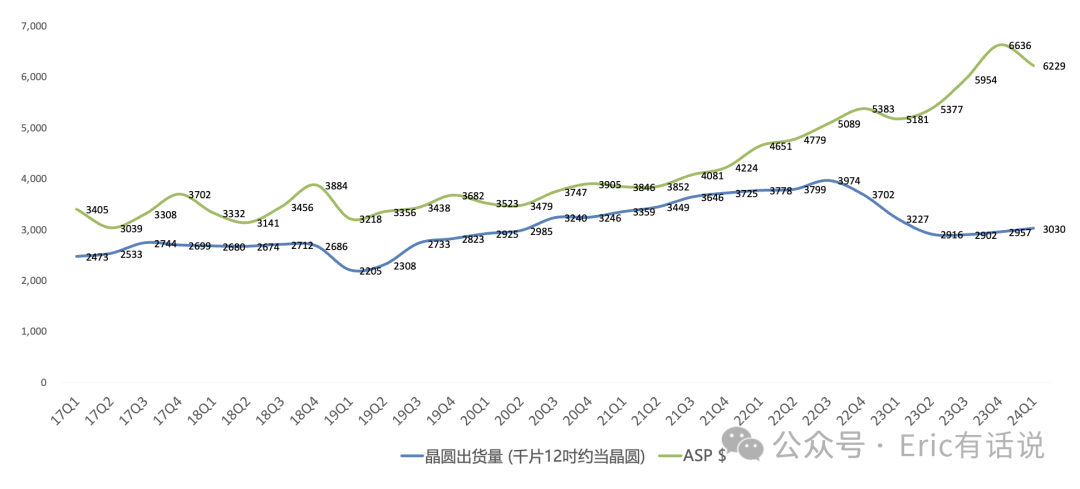

Equivalent 12-inch wafer shipments were 3,030K, down 6% year over year, up 2% sequentially, after two consecutive quarters of sequential decline; ASP was approximately $6,229, up 20% year over year, the 17th consecutive quarter of year-over-year growth.

Capex in USD was $5.77B, down 40% year over year; 2024 capex guidance of $28B-$32B maintained.

By Process and Platform, Q1:

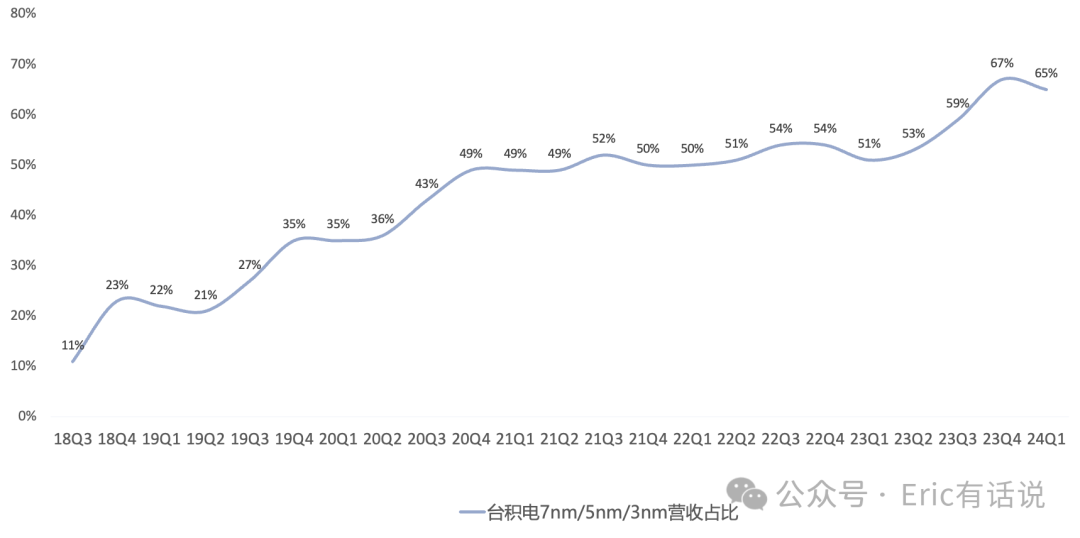

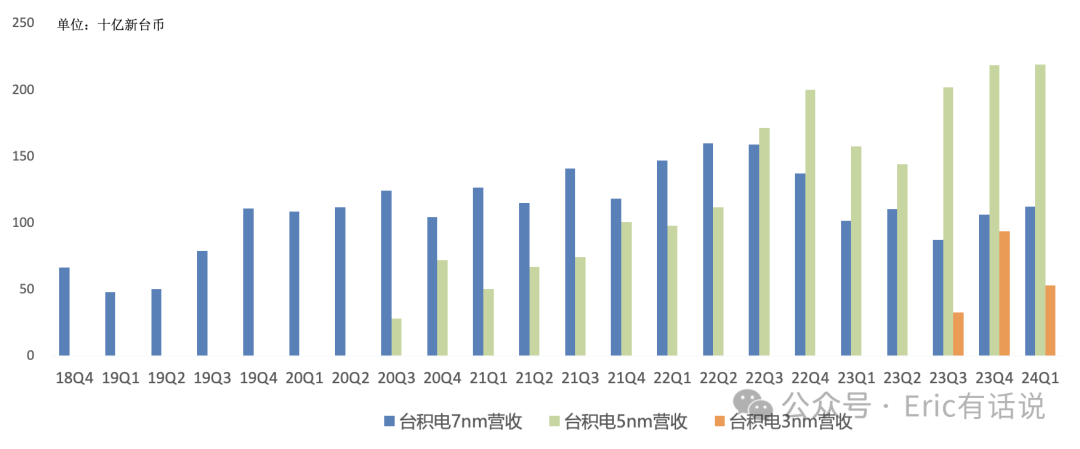

3nm accounted for 9%, 5nm 37%, 7nm 19%, 16nm 9%, 28nm 8%, 40/45nm 5%, 65nm 4%, 90nm 1%, 0.11/0.13um 3%, 0.15/0.18um 4%, 0.25um+ 1%; advanced nodes (3nm/5nm/7nm) accounted for 65%.

5nm revenue grew 39% year over year, marking the third consecutive quarter of record highs.

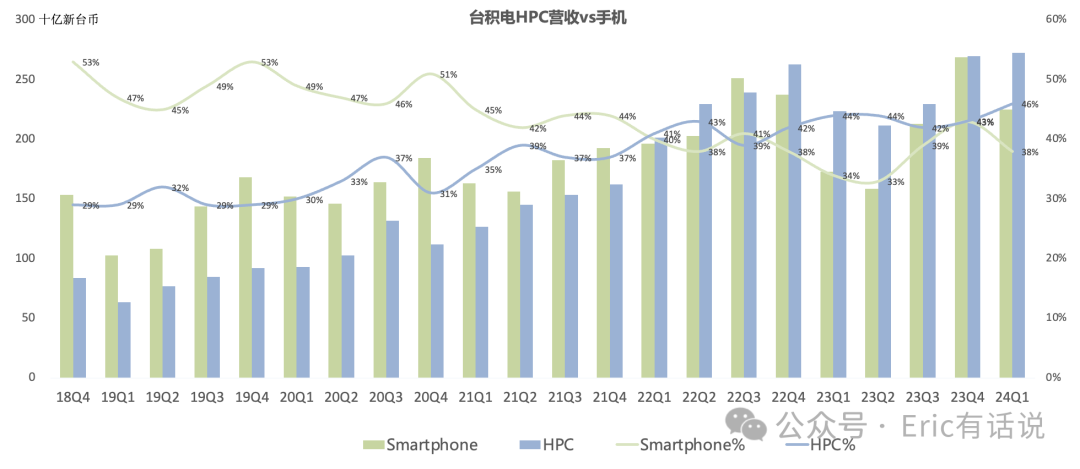

HPC accounted for 46%, smartphone 38%, IoT 6%, auto 6%; HPC share has exceeded smartphone for six consecutive quarters. Smartphone down 16% sequentially due to Apple impact (3nm currently only iPhone A17 Pro/M3 series Mac); HPC up 3% sequentially, IoT up 5% sequentially, auto flat sequentially.

Outlook:

Q2 revenue guided at $19.6B-$20.4B, up 25%-30% year over year, poised to hit a new record high. 2024 revenue to grow quarter by quarter, full-year USD revenue up 21%-26% year over year; Q2 gross margin 51%-53%, operating margin 40%-42%.

Lowered industry growth expectations; 2024 overall semiconductor (ex-memory) revenue growth expected around 10% year over year (previously 10%+), foundry industry revenue growth expected mid-to-high teens% (previously 20%).

Q2 smartphone continues seasonal decline; HPC led by 3nm/5nm drives growth. Full-year traditional server demand slowing, smartphone slowly recovering, PC, IoT and consumer electronics demand remain sluggish, auto semiconductor market to decline.

H2 2024 gross margin headwinds mainly from N3 ramp and electricity price increases; long-term gross margin 53%+ guidance unchanged.

2024 AI revenue expected to double year over year, accounting for low-teens% of total revenue ($8.4B-$11.4B); 5-year CAGR 50%, 2028 AI revenue expected to be 20%+ of total ($30.5B-$36.2B); TSMC long-term revenue growth target CAGR 15%-20%, gross margin 53%+, unchanged.

2024 capex expected at $28B-$32B, 70%-80% for advanced nodes, 10%-20% for mature nodes, 10% for advanced packaging and test. Capex intensity expected to remain in the mid-30% range for the next few years.

N2 volume production in 2025.

US Arizona first N4 Fab targets Y25H1 volume production. Due to strong AI demand, second N3 Fab adding N2 targets Y28 volume production. Third Fab in planning, targeting sub-N2 advanced nodes. Japan Kumamoto Fab 12/16/22/28nm opened end of February, Q4 volume production. Planning second Fab in H2, Y27 volume production 40-6nm. Germany Fab auto/industrial 12/16/22/28nm to break ground Y24Q4.

Overall, TSMC remains steady. Although it lowered 2024 semiconductor industry recovery expectations, it maintained its own full-year high-growth guidance, again proving that large AI exposure is the winning formula. Recent earnings across the board show that aside from strong AI demand and the memory cycle turn, other end markets are still awaiting recovery.

Given Apple's weakness, the likelihood of NVIDIA overtaking Apple as TSMC's largest customer this year has increased significantly. Today's TSMC earnings call again signaled this.

Today's TSMC conference call crashed for over 20 minutes; the glitch may indicate TSMC hasn't bought enough servers.