TSMC management raised full-year revenue guidance again this quarter.

TSMC Q3 Earnings:

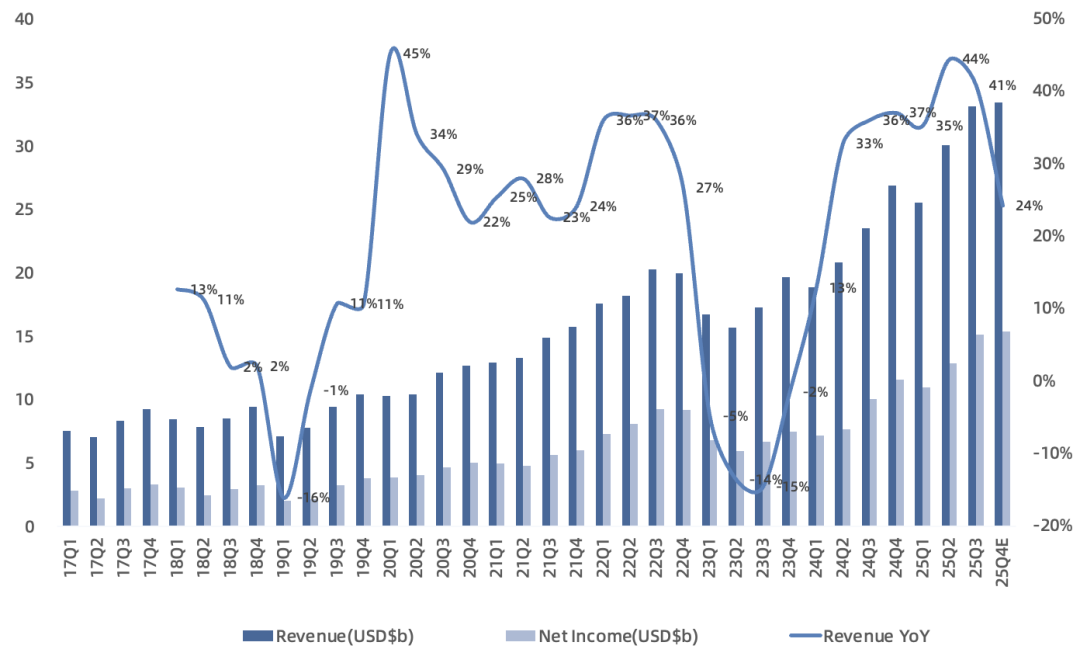

Revenue was $33.1B in USD terms, up 41% year over year and 10% sequentially, above the guidance range of $31.8-33.0B, setting a new all-time high. In NTD terms, revenue was NT$989.9B, up 30% year over year and 6% sequentially.

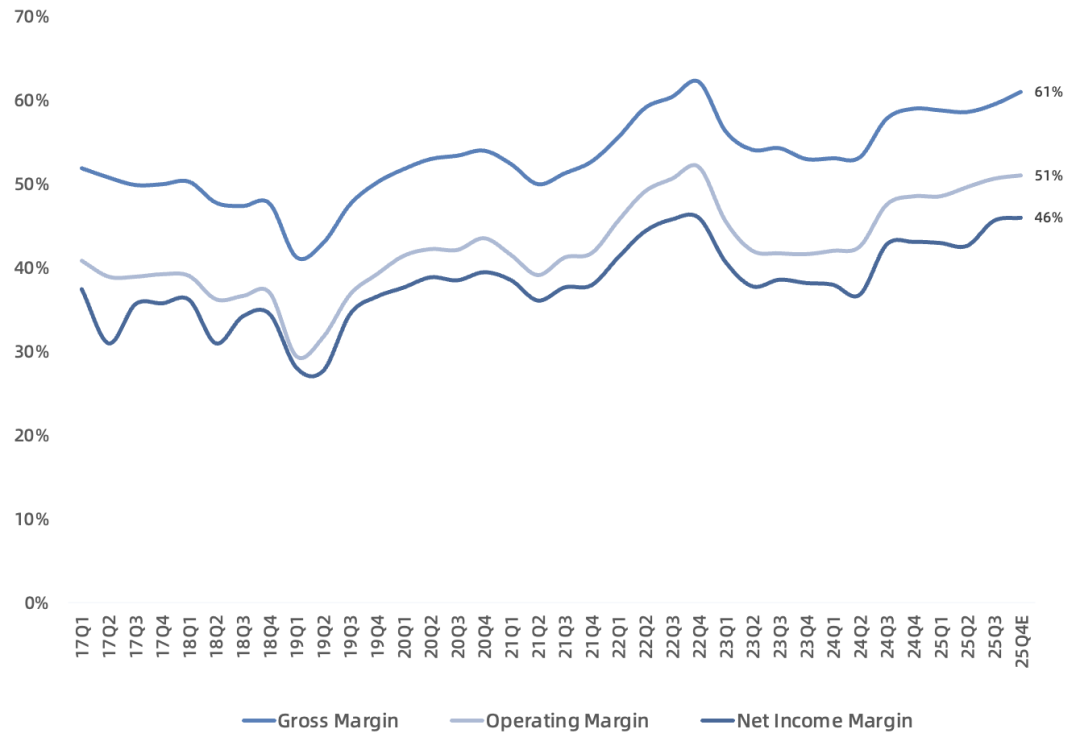

Gross margin was 59.5%, up 1.7 percentage points year over year and 0.9 percentage points sequentially, above the guidance range of 55.5-57.5%.

Operating margin was 50.6%, up 3.1 percentage points year over year and 1 percentage point sequentially.

Net income was $15.1B in USD terms, up 50% year over year and 18% sequentially. Net margin was 46%.

Equivalent 12-inch wafer shipments of 4.085M pieces (~1.36M pieces/month), up 22% year over year, marking the sixth consecutive quarter of year-over-year growth, and up 10% sequentially.

Capex of $9.7B in USD terms, up 52% year over year; full-year capex guidance of $40-42B (lower end raised, upper end unchanged).

Looking specifically at process technology and platforms in Q3:

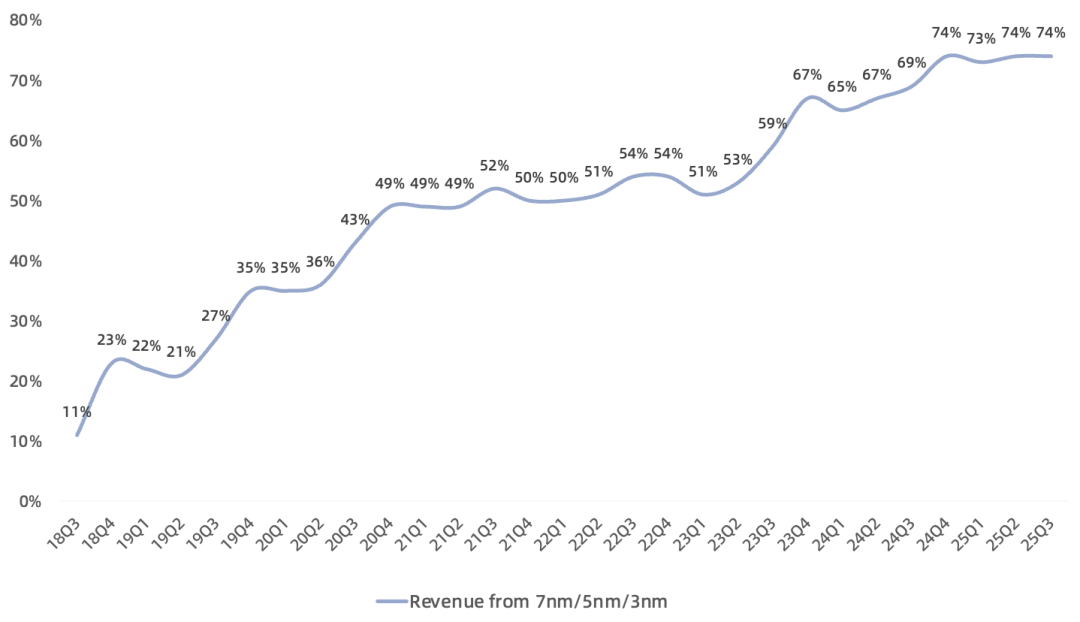

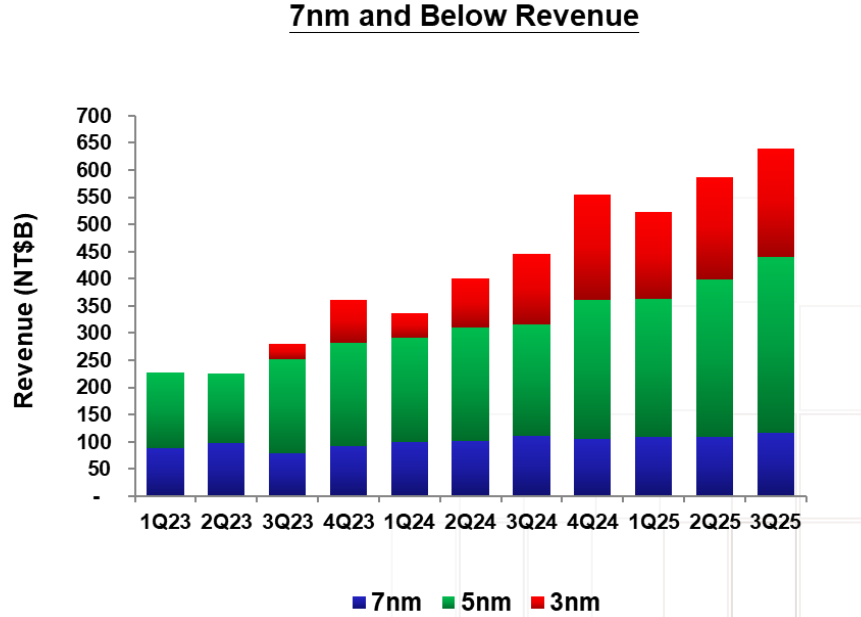

3nm accounted for 23% (Apple's core node), 5nm for 37% (NVIDIA's core node), 7nm for 14%, 16/20nm for 7%, 28nm for 7%, 40/45nm for 3%, 65nm for 4%, 90nm for 1%, 0.11/0.13um for 1%, and 0.15/0.18um for 3%. Advanced nodes (3nm/5nm/7nm) combined for 74%, with 3nm/5nm together at 60%.

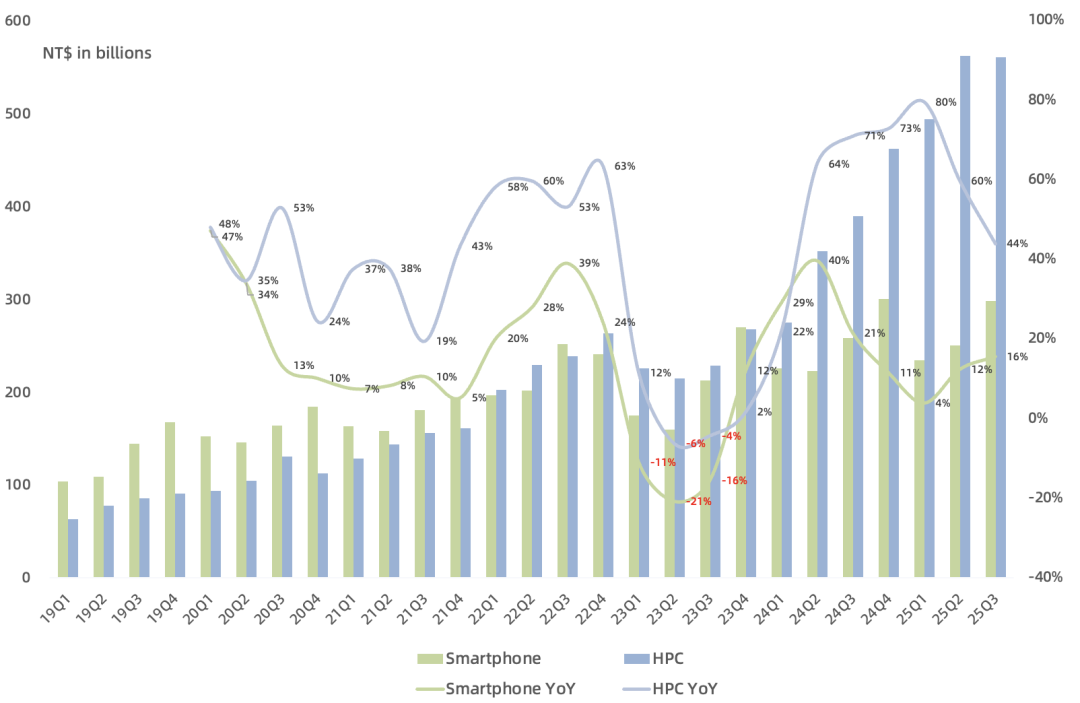

HPC accounted for 57%, smartphones 30%, IoT 5%, and automotive 5%. HPC has exceeded smartphones for 12 consecutive quarters. HPC grew ~44% year over year and was flat sequentially; smartphones grew 16% year over year and 19% sequentially; IoT grew 20% sequentially; automotive grew 18% sequentially.

Outlook:

Q4 revenue guided at $32.2-33.4B, up 20-24% year over year, driven primarily by strong HPC demand led by AI. Q4 gross margin guided at 59-61%, operating margin at 49-51%.

2025 full-year USD revenue growth guided at mid-30% year over year (raised); 2025 capex guided at $40-42B (lower end raised, upper end unchanged). Management indicated capex is unlikely to drop sharply in any given year going forward.

N2 will dilute 2026 gross margin; N3's dilutive effect is diminishing. Previously expected overseas fabs to dilute company-wide gross margin by nearly 2 percentage points in 2025; now seen at 1-2 points. Over the next few years, overseas fab ramp will dilute company-wide gross margin by 2-3 points, later widening to 3-4 points.

Advanced packaging revenue share approached 10%, but no update on future CoWoS capacity planning this quarter; management only stated:

CoWoS capacity continues to ramp; specific details will be provided next year. Both AI front-end and back-end capacity remain extremely tight. All mainstream AI chips currently rely on TSMC CoWoS capacity; one could say global AI chip supply depends on TSMC. Management noted it is collaborating with an OSAT building a fab in Arizona (ASE or Amkor?).

Previously guided AI revenue (GPU + ASIC + HBM controller) 2024-2029 CAGR of 44-46%; management now says it looks higher and will update the figure next quarter.

Management previously stated that across N7, N5, N3, and future N2, roughly 85-90% of equipment is common; conversion of some N5 capacity to N3 continues.

Nearly all TSMC revenue is USD-denominated while ~75% of costs are in NTD. NTD fluctuations materially impact revenue and profit: every 1% move in USD/NTD affects gross margin by 0.4 percentage points.

AI demand expected to remain strong, even stronger than three months ago; non-AI end markets seeing a mild recovery. Future AI infrastructure additions projected to sustain a 40-45% CAGR. Due to geopolitical risk, development-to-capacity timelines are being pulled forward by 2-3 years to maintain supply chain stability.

N2 pilot production this quarter with good yield; rapid volume production expected in 2026, covering smartphone and HPC/AI demand. N2P volume production expected in 2H 2026. N2/N2P/A16 will become TSMC's future major technology nodes.

The market previously worried Arizona fabs would drag TSMC profitability, but thanks to US government subsidies and high utilization, the Arizona fab unexpectedly turned profitable in Q2. Today TSMC formally announced NVIDIA Blackwell AI chips have achieved volume production at the Arizona fab for the first time. TSMC's second Arizona fab (N3 node) is complete; last quarter volume production was pulled forward by several quarters to 2027; this quarter management said it will accelerate introduction of the even more advanced N2 node. Management also noted it is actively securing a second large adjacent land parcel at the Arizona site to support existing expansion plans for strong AI-related demand.

Overall, as the ultimate picks-and-shovels play for global AI chips, TSMC's long-term earnings visibility is very high. OpenAI recently announced a series of massive compute procurements: 10GW with NVIDIA, 10GW with Broadcom, 6GW with AMD. OpenAI has drawn many pies, but all that compute relies on TSMC for manufacturing. Now TSMC management says future expansion will maintain discipline — a bit of a slap in the face to OpenAI. The long-term AI narrative is intact, but near-term one must watch quarterly scorecards, not pies, to support the stock.

Fundamentally, while Q3 growth looks optimistic, combining it with the full-year guidance implies Q4 revenue growth of only 6-21%, a notable deceleration. Management cited tariff uncertainty potentially impacting consumer electronics, and expects overall non-AI end markets to see only a mild recovery in 2025.

Based on current guidance, TSMC 2025 revenue projected around $122B, net income around $54B. At current market cap, PE ~28x. Given TSMC management's habit of conservative guidance and high certainty of long-term earnings growth, TSMC may be the lowest-valued company in the AI sector.