TSMC management significantly raised long-term growth guidance this quarter.

TSMC Q4 Earnings:

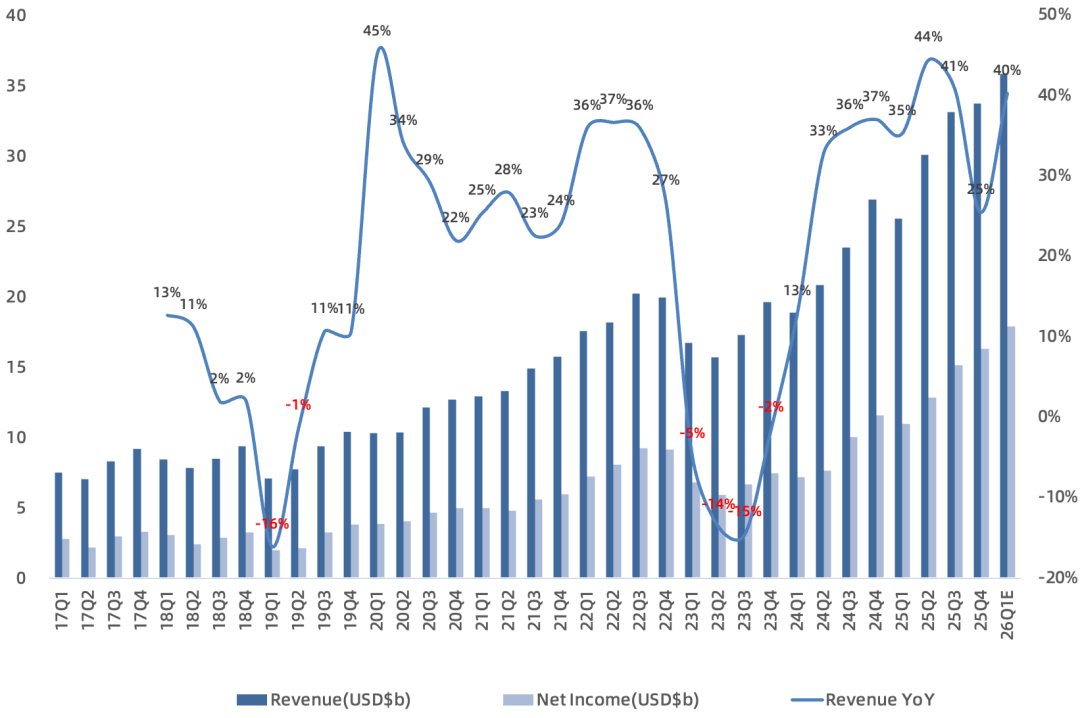

Revenue of $33.73B in USD terms, up 25% year over year, up 2% sequentially, above guidance range of $32.2-33.4B, a new all-time high. In NTD terms, NT$1,046B, up 20% year over year, up 6% sequentially.

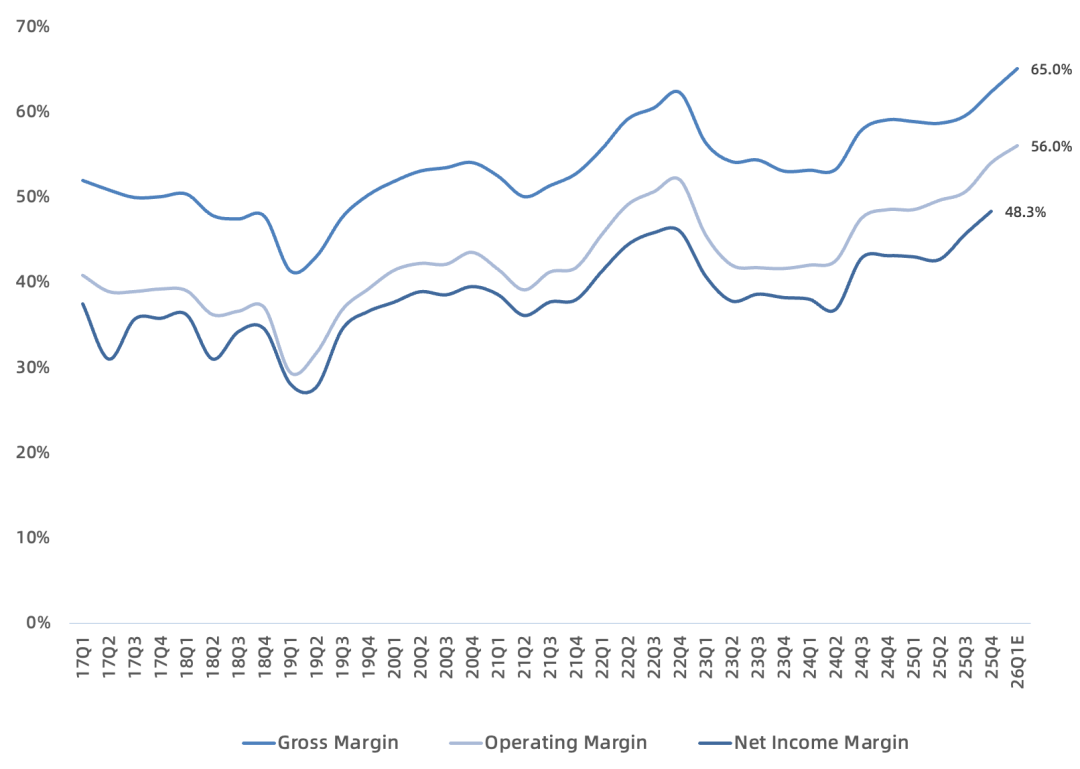

Gross margin 62.3%, up 3.3 pp year over year, up 2.8 pp sequentially, above guidance range of 59-61%.

Operating margin 54%, up 5.5 pp year over year, up 3.4 pp sequentially, above guidance range of 49-51%.

Net income of $16.3B in USD terms, up 41% year over year, up 8% sequentially, net margin 48.3%.

Equivalent 12-inch wafer shipments of 3.96M (approx. 1.32M/month), up 16% year over year, seventh consecutive quarter of year-over-year growth, down 3% sequentially.

Capex of $11.51B in USD terms, up 2% year over year. 2025 full-year capex $40.9B, at the midpoint of guidance range of $40-42B.

Technology and Platform Breakdown, Q4:

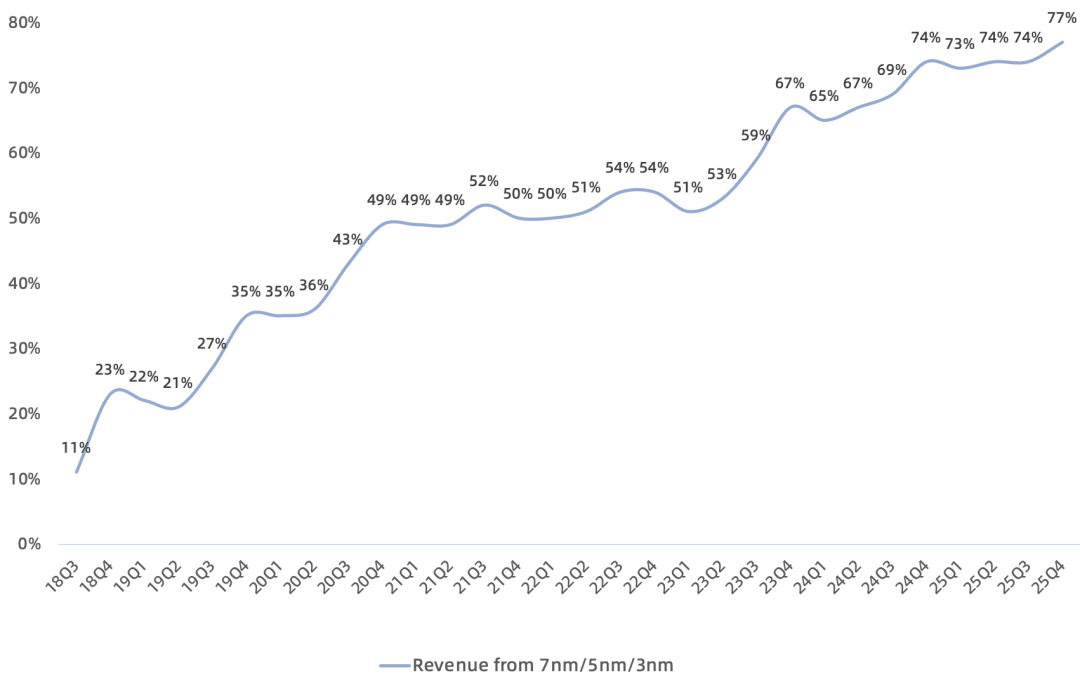

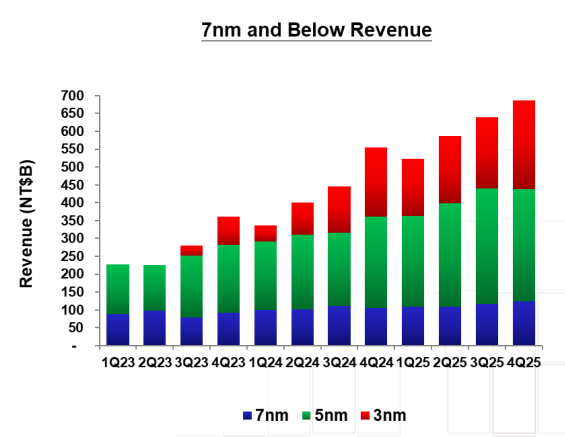

3nm 28% (Apple core node + NVIDIA Rubin core node), 5nm 35% (NVIDIA Hopper + Blackwell core node), 7nm 14%, 16/20nm 6%, 28nm 6%, 40/45nm 3%, 65nm 4%, 90nm 1%, 0.11/0.13µm 1%, 0.15/0.18µm 2%. Advanced nodes 3nm/5nm/7nm combined 77%, 3nm/5nm combined 63%, both record highs.

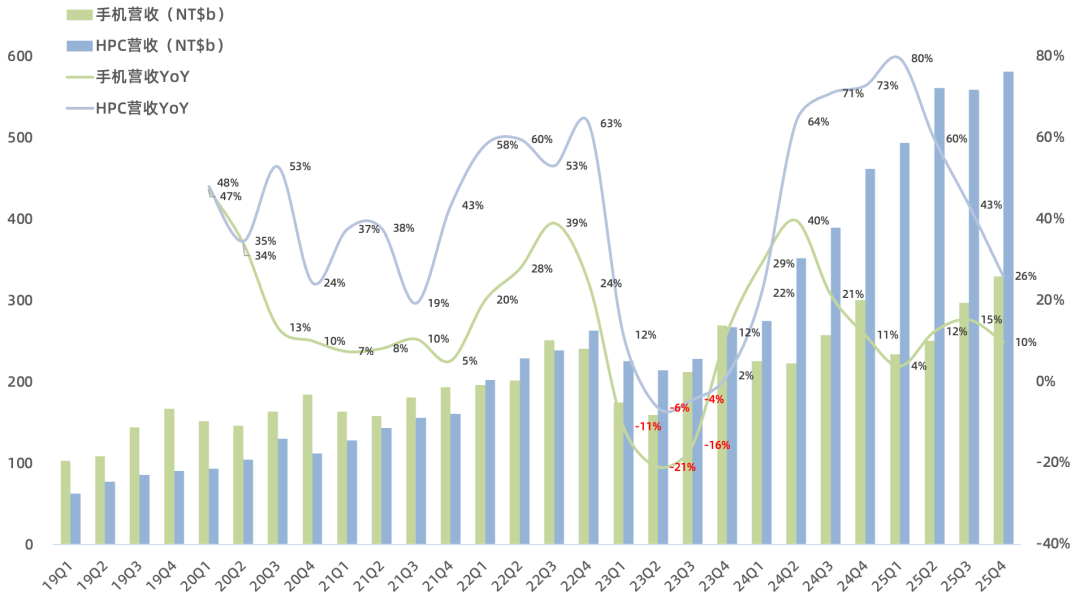

HPC accounted for 55%, smartphones 32%, IoT 5%, and automotive 5%. HPC has exceeded smartphones for 13 consecutive quarters. HPC grew about 26% year over year and 4% sequentially; smartphones grew 10% year over year and 11% sequentially, mainly due to seasonal iPhone new-model shipments; IoT grew 3% sequentially; automotive declined 1% sequentially.

Outlook:

Projected 2026 Q1 revenue of $34.6-35.8B, up 36-40% year over year, shattering prior market concerns of seasonal slowdown, driven by strong AI demand. Q1 gross margin 63-65%, operating margin 54-56%, implying net margin could challenge the 50% threshold.

Wafer IDM 2.0 industry grew 16% in 2025; projected 2026 industry growth of 14%. Driven by AI growth, TSMC 2026 full-year USD revenue projected up near 30% year over year. Projected 2026 capex of $52-56B—note Bloomberg consensus was only $45.4B. Management indicates capex scale over the next three years will significantly exceed the past three years.

N3 margin to exceed company average in 2026. N2 volume production in 2025 Q4, accelerating ramp in 2026 covering smartphone and HPC/AI demand. N2P/A16 SPR planned for H2 2026 volume production. N2/N2P/A16 will become TSMC's future major technology nodes. N2 ramp in H2 2026 to impact full-year margin by 2-3 percentage points.

Advanced packaging revenue share 8% in 2025, projected slightly above 10% in 2026, projected to grow for the next five years. All mainstream AI chips currently rely on TSMC CoWoS capacity; one could say global AI chip supply depends on TSMC.

Projected AI revenue (GPU + ASIC + HBM controller) 2024-2029 CAGR mid-to-high 50s% (previously 45%). Company overall revenue CAGR raised to 25% (previously 15-20%). Gross margin raised to 56% (previously 53%).

US Arizona Fab 1 (N4 node) has completed capacity ramp. Fab 2 (N3 + N2 nodes) construction complete, equipment move-in in 2026; due to strong customer demand, Fab 2 volume production accelerated, projected to complete capacity ramp by H2 2027. Fab 3, Fab 4, and advanced packaging fab construction begun. Arizona fab yields approaching Taiwan fabs; GigaFab cluster can effectively reduce costs.

PC/smartphone will indeed see shipment growth slow due to rising memory prices, but TSMC customers focus on high-end, so demand impact is relatively small.

Currently reducing 6/8-inch capacity, continuing conversion of N5 capacity to N3.

Overall, as the gatekeeper of AI chip capacity, TSMC's every move tugs at the nerves of global AI thematic investing. Given the pronounced cyclicality of semiconductors, TSMC has historically been very cautious on expansion plans unless seeing long-term sustainable demand. Therefore, this expansion and management's long-term AI demand guidance in the earnings report is undoubtedly a strong shot in the arm for the AI industry.

Actual 2025 results came in slightly above prior expectations. Based on management's current guidance, TSMC's 2026 revenue is projected at $160B, with net income conservatively estimated at $70B, implying a forward PE of under 20x at the current market cap.