Two days ago ASML held its ground, not only maintaining its 2023 full-year revenue growth target of 25% but raising it to 30%. It became a rare giant still growing in a severe semiconductor downcycle. TSMC, which previously failed to defend its full-year growth target, once again lowered its full-year guidance.

TSMC Q2 Earnings:

Revenue was $15.68B in USD terms, down 14% year over year and 6% sequentially, the first back-to-back quarterly declines since 2019 Q1. In NTD terms, revenue was NT$480.84B, down 10% year over year and 5% sequentially, the first decline since 2019 Q1.

Gross margin was 54.1%, down 5 percentage points year over year and 2.2 percentage points sequentially.

Operating income was $6.6B in USD terms, down 26% year over year and 13% sequentially; operating margin was 42%.

Net income was $5.9B in USD terms, down 26% year over year and 13% sequentially; net margin was 38%.

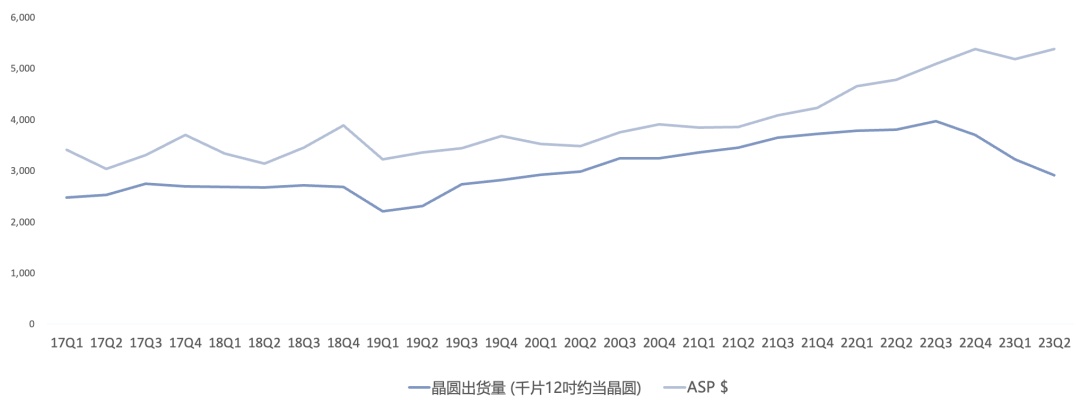

12-inch wafer shipments were 2,916K, down 23% year over year and 10% sequentially, declining for three consecutive quarters, last seen in 2018; ASP was approximately $5,377, up 13% year over year, the 14th consecutive quarter of year-over-year growth.

Free cash flow was -$2.7B in USD terms, mainly due to tax impact.

Capex was $8.2B in USD terms, up 11% year over year; full-year capex guidance maintained at $32-36B, with management leaning toward the lower end of the range.

Process and Platform Breakdown, Q2:

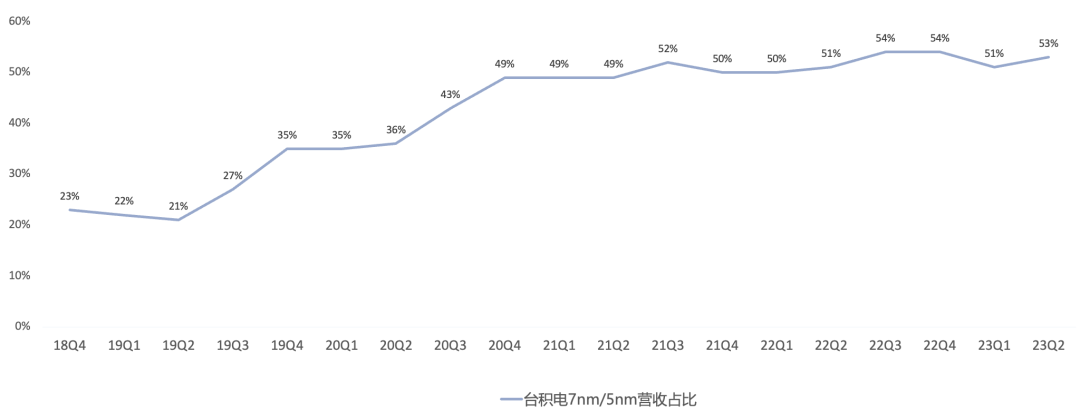

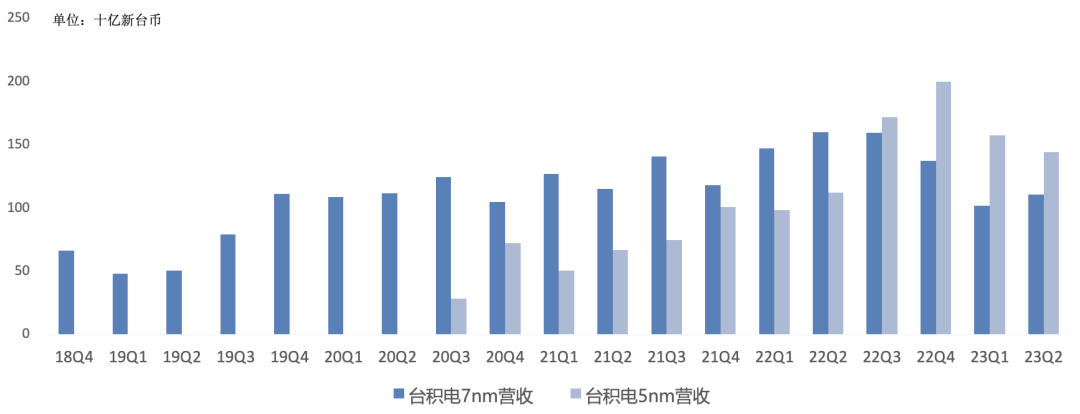

5nm accounted for 30%, 7nm 23%, 16nm 11%, 20nm 1%, 28nm 11%, 40/45nm 7%, 65nm 7%, 90nm 2%, 0.11/0.13um 2%, 0.15/0.18um 5%, 0.25um+ 1%; advanced nodes (5nm/7nm) accounted for 53%.

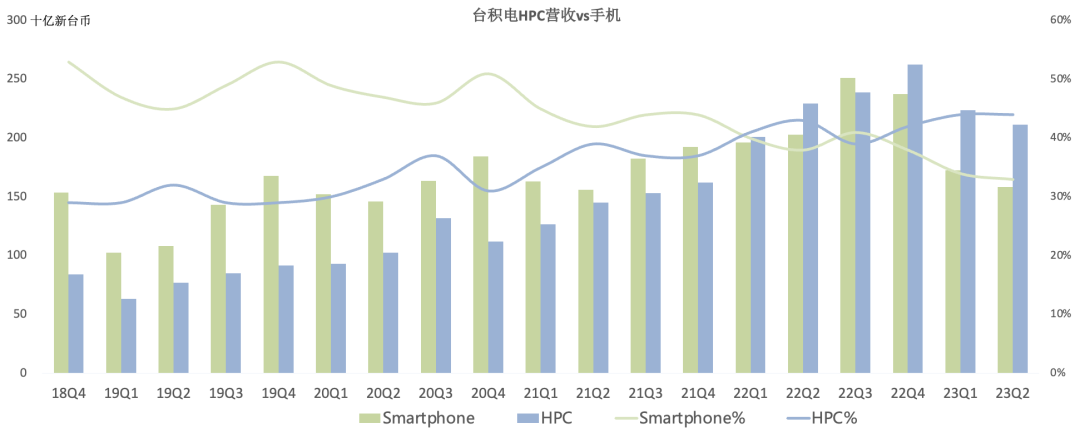

HPC accounted for 44%, smartphone 33%, IoT 8%, auto 8%; HPC share exceeded smartphone for three consecutive quarters. Smartphone declined 9% sequentially, HPC declined 5% sequentially, auto grew 3% sequentially.

Outlook:

Q3 revenue guided at $16.7-17.5B, down 12%-16% year over year; gross margin 51.5%-53.5%; operating margin 38%-40%; Q3 utilization improves, but N3 ramp impacts gross margin through Q4.

Fabless inventory expected to return to healthy levels in Q4, later than previously expected. TSMC full-year revenue now expected to decline 10%, guidance lowered again.

Global foundry industry revenue expected to decline high-teens (approximately 15%-17%) this year, worse than the previous estimate of high-single-digit decline.

Current AI revenue exposure is approximately 6%, with potential for 50% CAGR over the next five years, lifting exposure to low-teens (approximately 11%-13%); HPC is TSMC's largest future growth driver.

CoWoS capacity is tight in the near term, but capacity will increase 2x next year; by end of next year, capacity will not be an issue.

N3 yield is good; ramp begins in H2, early ramp impacts margin; applications include HPC and smartphone; N3X mainly for CPUs, N3E broader use, N3E volume production in Q4; 2023 N3 revenue contribution expected at mid-single digits (4%-6%).

N2 volume production in 2025; HPC backside power delivery version N2 in H2 2025, volume production in 2026; N3-to-N2 performance uplift smaller than N5-to-N3, focus primarily on power efficiency improvement.

US 4nm fab delayed to 2025 volume production; Japan fab on track for late 2024 volume production, Japan lines at 16nm/22nm/28nm; China 28nm continues expansion; Germany automotive specialty process capacity assessment to accelerate.

Long-term revenue CAGR target of 15%-20% in USD terms remains unchanged.

Overall, TSMC was not as "resilient" as ASML — it not only failed to defend full-year growth but continued to lower full-year guidance, which is normal for the semiconductor industry.

The market has been hyping tech stocks excessively, forgetting that aside from strong AI demand, everything else is weak. Many tech stocks (including semiconductors) will post ugly Q2 results; the global macro environment remains soft, and even within the same industry, performance divergence across companies will be wide. Truly cycle-proof tech stocks are few, scarcer, and deserve a valuation premium.