Strictly speaking, TSMC officially kicks off the semiconductor Q4 earnings season.

TSMC Q4 Earnings:

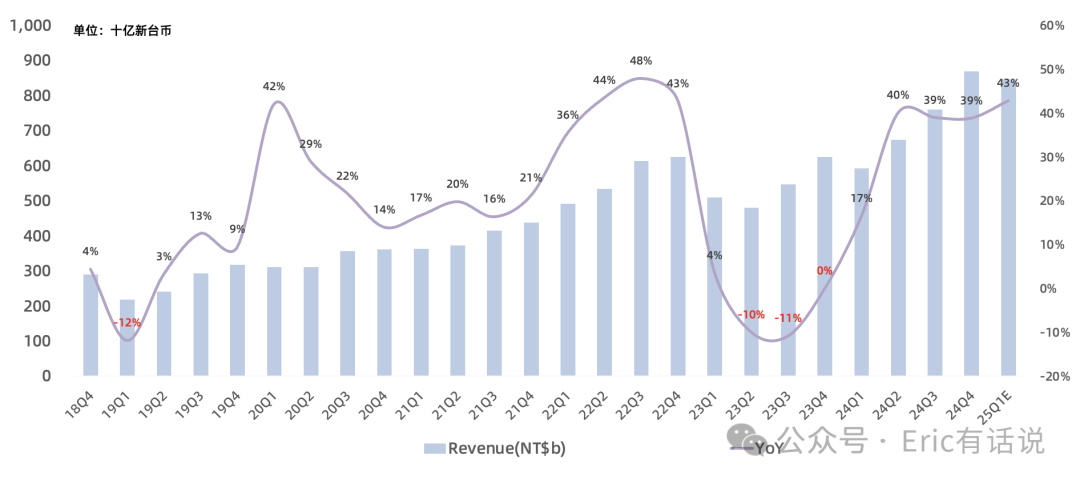

Revenue was $26.9B in USD terms, up 37% year over year and 14% sequentially. In NTD terms, revenue was NT$868.5B, up 39% year over year and 14% sequentially, both marking the third consecutive quarter of record highs.

Gross margin was 59%, up 6 percentage points year over year and 1.2 percentage points sequentially.

Operating income was $13.2B in USD terms, up 61% year over year and 18% sequentially, marking the second consecutive quarter of record highs. Operating margin was 48.5%.

Net income was $11.6B in USD terms, up 55% year over year and 15% sequentially, marking the second consecutive quarter of record highs. Net margin was 43%.

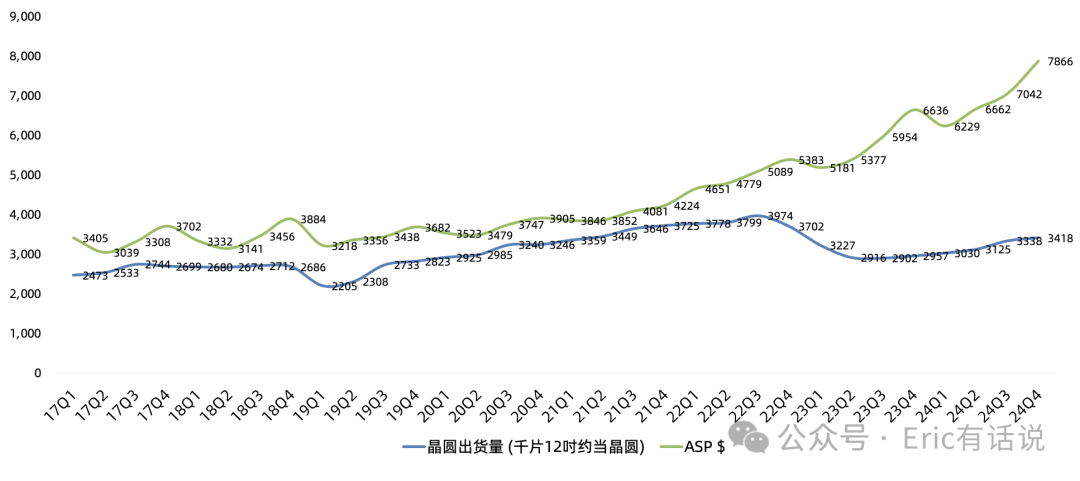

12-inch equivalent wafer shipments were 3.418M (approx. 1.14M/month), up 16% year over year and 2% sequentially, the third consecutive quarter of year-over-year growth. ASP was ~$7,866, up 19% year over year, the 20th consecutive quarter of year-over-year growth, setting another record high.

Capex was $11.23B in USD terms, up 114% year over year. Full-year 2024 capex was $29.76B, below the previous guidance of slightly above $30B.

Technology and Platform Breakdown, Q4:

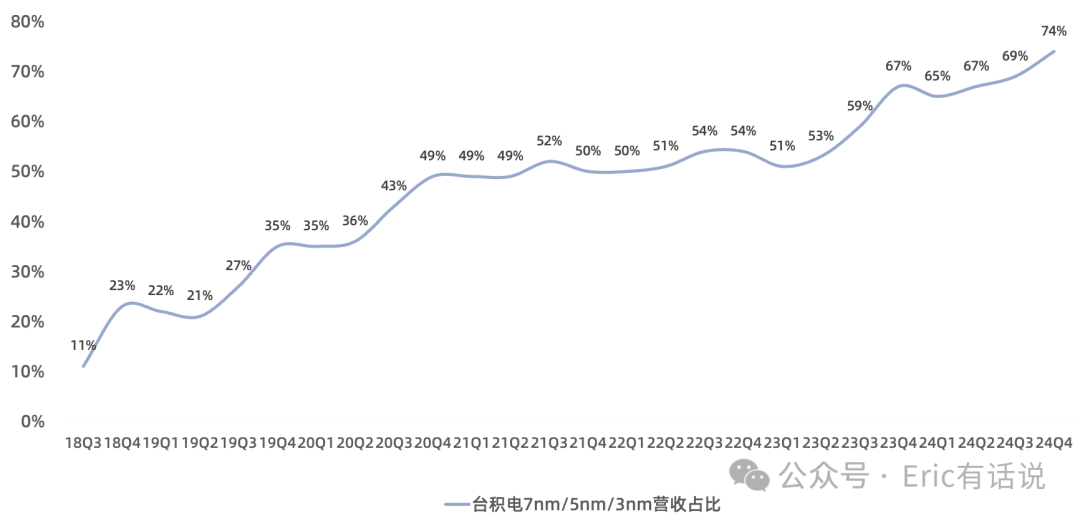

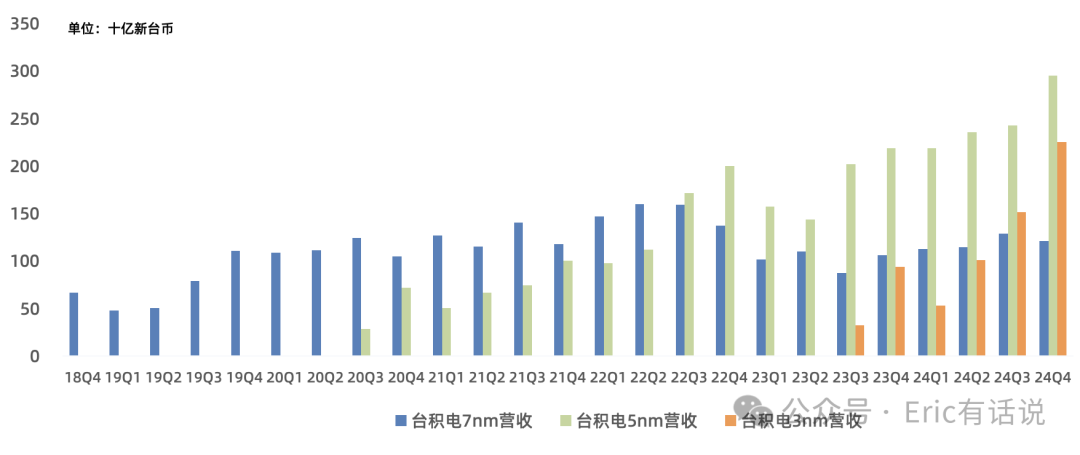

3nm accounted for 26%, 5nm 34%, 7nm 14%, 16nm 7%, 28nm 6%, 40/45nm 3%, 65nm 4%, 90nm 1%, 0.11/0.13µm 2%, 0.15/0.18µm 3%, 0.25µm+ 1%. Advanced nodes (3/5/7nm) combined for 74%, with 3/5nm together at 60%, both new highs.

3nm revenue grew 49% sequentially, marking the third consecutive quarter of record highs. 5nm revenue grew 35% year over year, marking the sixth consecutive quarter of record highs.

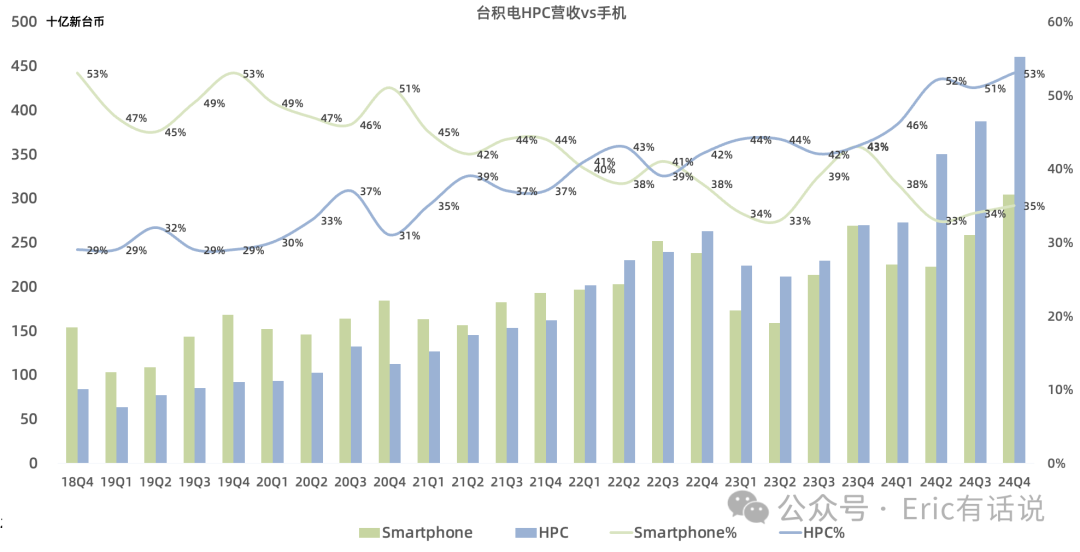

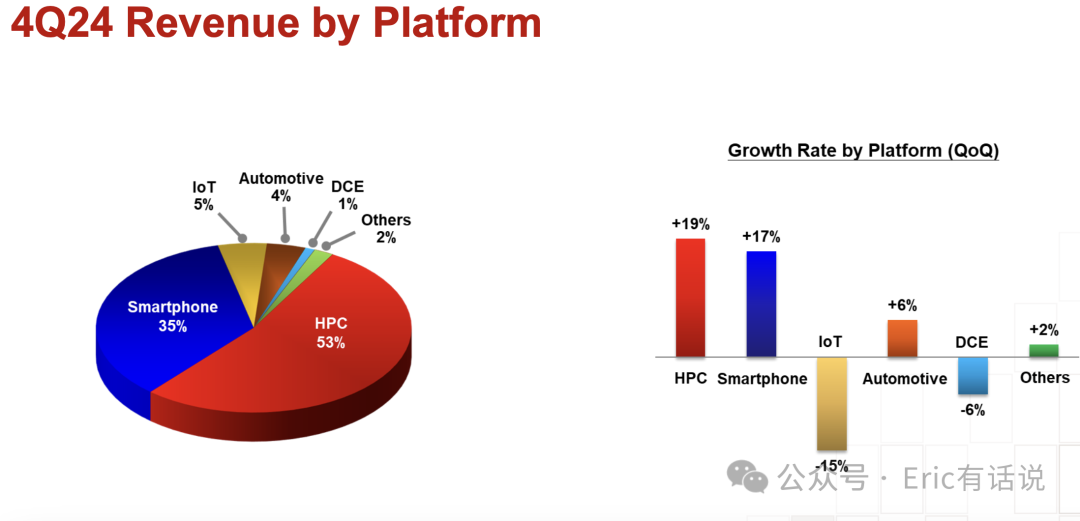

HPC accounted for 53%, smartphones 35%, IoT 5%, automotive 4%. HPC has exceeded smartphone share for nine consecutive quarters. HPC grew 58% year over year and 19% sequentially; smartphone grew 23% year over year and 17% sequentially; IoT declined 15% sequentially; automotive grew 6% sequentially. NVIDIA is on track to overtake Apple as TSMC's largest customer in 2024, pending TSMC's 20-F filing in April.

Outlook:

Q1 revenue is guided at $25.0-25.8B, up 32%-37% year over year. Strong AI demand smooths smartphone seasonality. Q1 gross margin guided at 57%-59%, operating margin at 46.5%-48.5%.

Full-year 2025 USD revenue is guided to grow 24%-26% year over year. 2024-2029 CAGR is guided at 20%. 2025 capex is guided at $38-42B.

2024 AI (GPU + ASIC + HBM controller) revenue accounted for 14%-16% ($12.6-14.4B). 2025 AI revenue is expected to double ($25.2-28.8B). 2024-2029 AI CAGR is guided at 44%-46%.

2024 advanced packaging revenue exceeded 8% ($7.2B). 2025 advanced packaging revenue is expected to exceed 10% ($11.3B). Gross margin continues to improve but remains below the corporate average.

2024 global foundry 2.0 industry revenue grew 6% year over year, below the previous 10% expectation. 2025 industry revenue is expected to increase 10%. TSMC continues to outperform the market.

Long-term gross margin guidance remains 53%+. Overseas fabs will dilute gross margin by 2-3 percentage points annually over the next five years.

N2 volume production in H2 2025, with first-two-year tape-outs exceeding N3/N5 at the same stage. N2P volume production in H2 2026 for smartphone and HPC. A16 SPR, optimized for HPC, volume production in H2 2026.

Arizona Fab 1 (N4) is in volume production with yields matching Taiwan fabs. Fab 2 construction complete, equipment move-in planned this year. Fab 3 process to be announced later; Fabs 2 and 3 will be more advanced than N4. Japan Kumamoto Fab 1 (28/22/16/12nm) in volume production. Fab 2 (focused on consumer, automotive, industrial, HPC) breaks ground this year. Germany automotive/industrial fab progressing well.

Overall, TSMC with its large AI exposure remains steady, providing a reassuring pill for investors recently rattled by supply-chain noise, especially those worried about long-term AI chip demand.

Based on the upper end of full-year guidance, TSMC's annual revenue would be $113.5B, net income ~$48B. At 30x PE, that implies a $1.44T market cap.