Updating the previous earnings note: ASML grew 2023 revenue 30% on mainland China DUV sales; TSMC, propped up by advanced nodes, saw 2023 revenue fall 9%; 2024 ASML growth may dip below 10% while TSMC could rebound 25%; this divergence may reflect logic recovering ahead of storage, or logic recovery being stronger than storage.

TSMC Q4 Earnings:

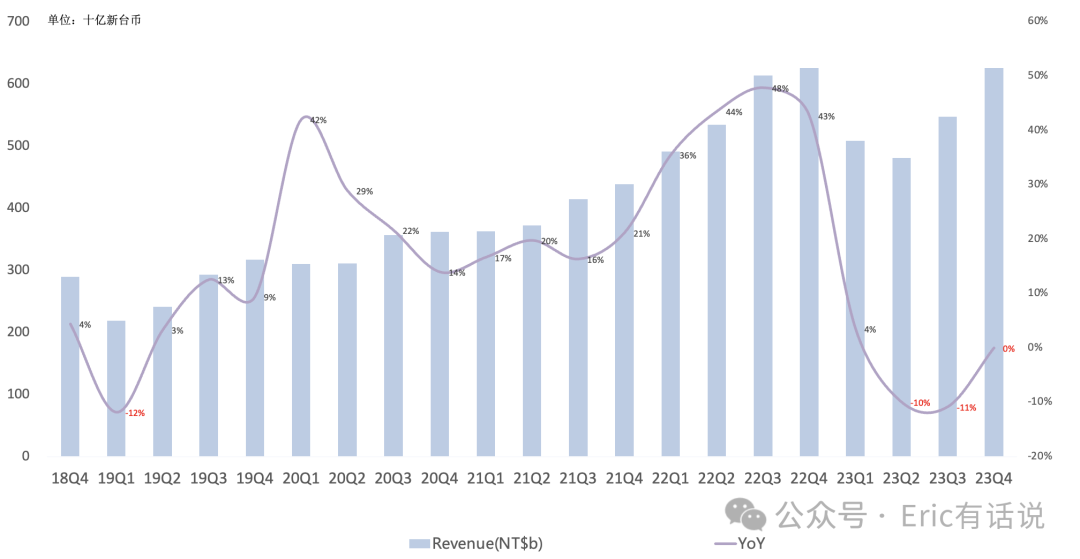

Revenue in USD was $19.62B, down 2% year over year and up 14% sequentially, the fourth consecutive quarter of year-over-year declines. In NTD it was NT$625.53B, flat year over year and up 14% sequentially, ending two consecutive quarters of year-over-year declines. Full-year revenue was $69.3B, down 9% year over year. The foundry industry revenue fell 13% year over year in 2023; TSMC continued to outperform the industry.

Gross margin was 53%, down 9.2 percentage points year over year and 1.3 percentage points sequentially.

Operating income in USD was $8.16B, down 21% year over year and up 13% sequentially; operating margin 42%.

Net income in USD was $7.5B, down 18% year over year and up 12% sequentially, the fourth consecutive quarter of year-over-year declines. Net margin 38%. Full-year net income was $26.9B, down 20% year over year.

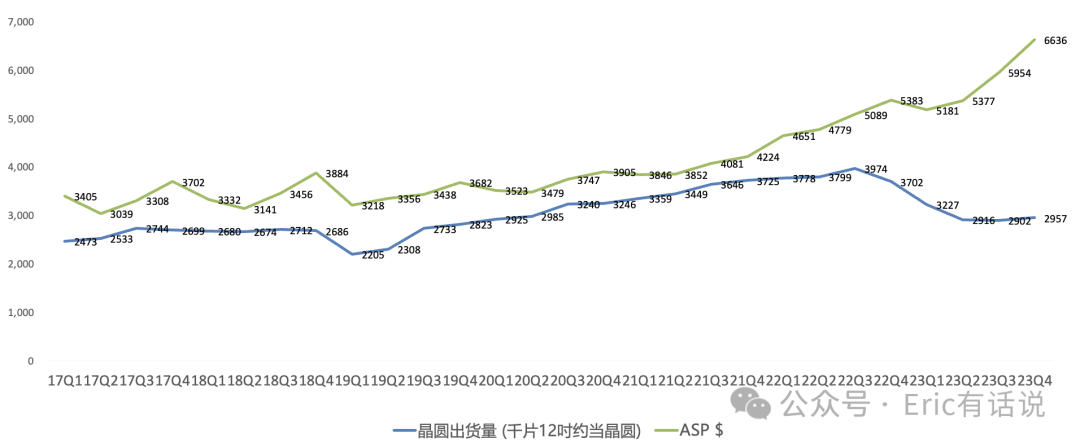

Equivalent 12-inch wafer shipments were 2,957K, down 20% year over year and up 2% sequentially, ending four consecutive quarters of sequential declines; ASP ~$6,636, up 23% year over year, the 16th consecutive quarter of year-over-year increases.

Capex in USD was $5.24B, down 49% year over year; 2023 capex was $30.45B, below prior guidance of $32-36B.

Technology and Platform Breakdown, Q4:

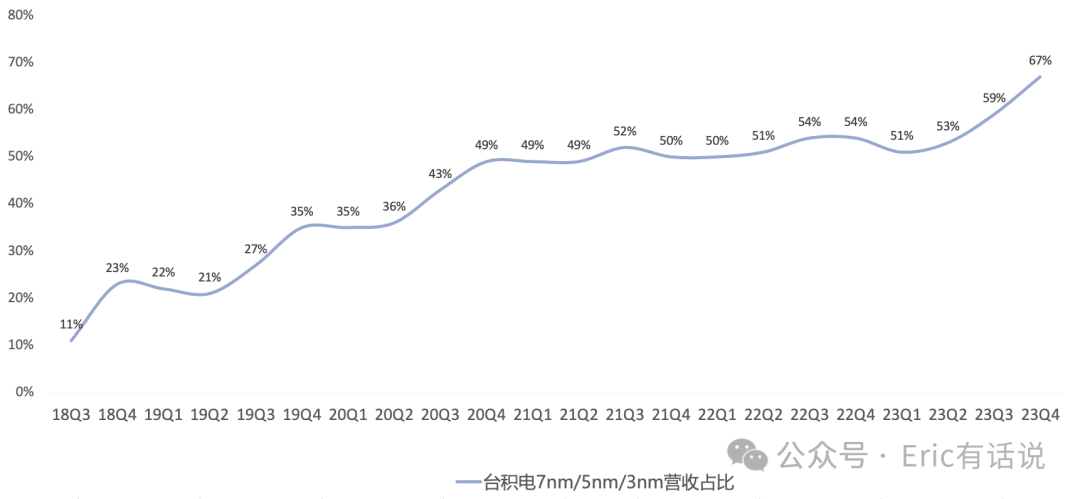

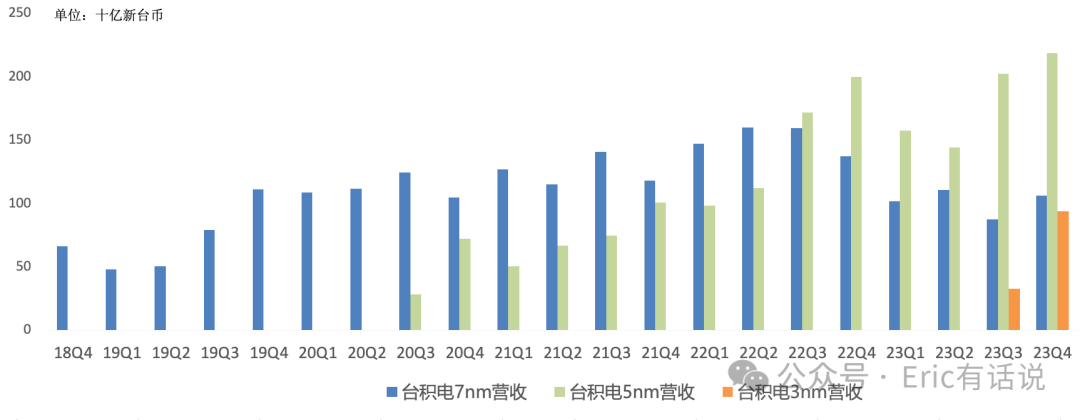

3nm accounted for 15%, 5nm 35%, 7nm 17%, 16nm 8%, 28nm 7%, 40/45nm 4%, 65nm 5%, 90nm 1%, 0.11/0.13um 3%, 0.15/0.18um 4%, 0.25um+ 1%; advanced nodes (3nm/5nm/7nm) combined 67%.

3nm revenue surged 186% sequentially, ramping nearly four quarters faster than 5nm and 7nm did at the time.

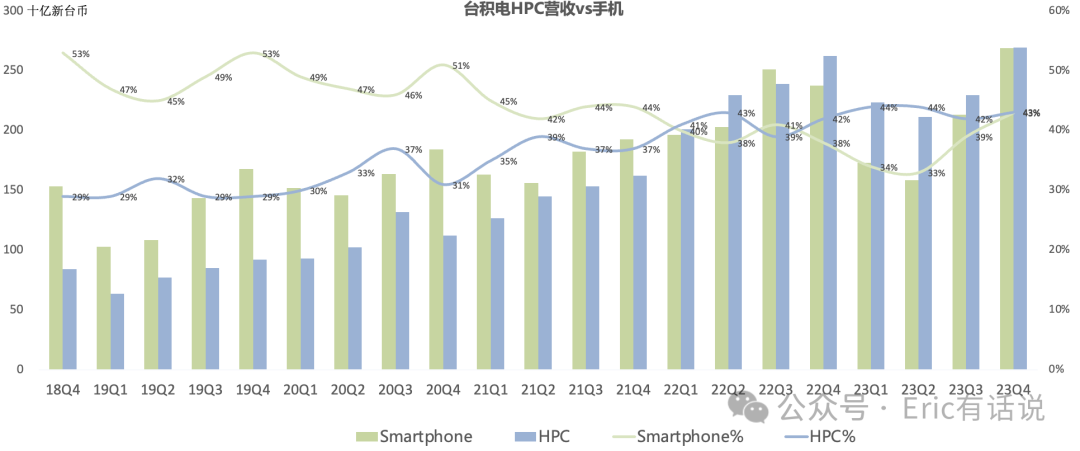

HPC 43%, Smartphone 43%, IoT 5%, Automotive 5%; HPC share may have exceeded Smartphone for the fifth consecutive quarter. Smartphone up 27% sequentially on iPhone 15 series strength (3nm currently only iPhone A17 Pro/M3 Mac); HPC up 17% sequentially; IoT down 29% sequentially; Automotive up 13% sequentially.

Outlook:

Guides Q1 revenue $18.0-18.8B, up 8%-12% year over year; 2024 revenue to grow quarter by quarter, full-year USD revenue up 21%-26% year over year; Q1 gross margin 52%-54%, operating margin 40%-42%.

Expects 2024 overall semiconductor industry (ex-memory) revenue up 10%+ year over year; foundry industry revenue up 20% year over year.

N3E volume production in 23Q4; N3P and N3X coming soon; expects N3 family to become a long-lived node; 2024 N3 revenue up 3x year over year, revenue share reaching 14%-16% ($12-14B); N3P PPA comparable to Intel 18A but earlier release and lower cost.

Q1 Smartphone to decline seasonally; HPC to drive growth; full-year Smartphone to return to growth; HPC growth particularly pronounced; 2024 gross margin headwinds from N3 ramp and partial N5-to-N3 migration.

AI demand robust; related revenue can compound at 50% annually; 5-year revenue share to reach 17%-19% ($20-27B); TSMC long-term revenue growth target CAGR 15%-20%, gross margin 53%+, unchanged.

CoWoS capacity tight near-term; 2024 target to double capacity unchanged; supply-demand imbalance to persist through 2025; advanced packaging revenue to compound at 50%+.

Expects 2024 capex $28-32B; 70%-80% for advanced nodes, 10%-20% for mature nodes, 10% for advanced packaging and test; expects capex intensity to remain in the mid-30% range for the next several years.

N2 volume production in 2025; customers primarily HPC and Smartphone; HPC backside power N2 H2 2025 tape-out, 2026 volume; at N2 node, virtually everyone chooses to partner with TSMC.

Germany fab for auto/industrial 12/16/22/28nm, breaks ground 24Q4; US N4 fab 25H1 volume, N3 fab possibly 27/28; Japan Kumamoto fab 12/16/22/28nm opens late Feb 2024, Q4 volume; Tainan N3 fab expansion; N2 fabs in Hsinchu and Kaohsiung; given strong phone and HPC demand for N2, planning Kaohsiung phase 3 expansion.

C.C. Wei: AI is still in early stages; we see only the tip of the iceberg. I want to give the industry an optimistic signal; even if reaching 1nm or below is challenging, we are using AI to accelerate breakthroughs.

Overall, TSMC remains very steady; first to confirm 2024 semiconductor industry recovery; TSMC's better-than-expected N3 performance again proves advanced nodes are not lacking demand, while mature nodes face oversupply risk.

At the same time, signaling sustained long-term AI demand.