Apple's FY26Q1 earnings correspond to the actual period of October/November/December 2025.

Apple FY2026 Q1 Earnings Summary:

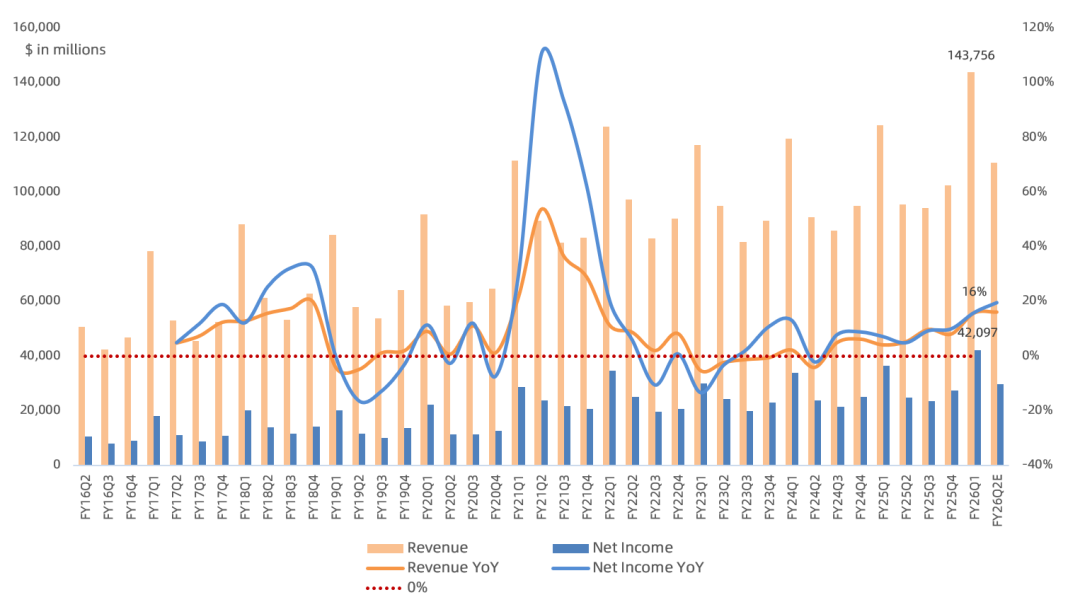

Revenue of $143.8B, up 16% year over year, above consensus of $138.4B; prior guidance was 10-12% year-over-year growth.

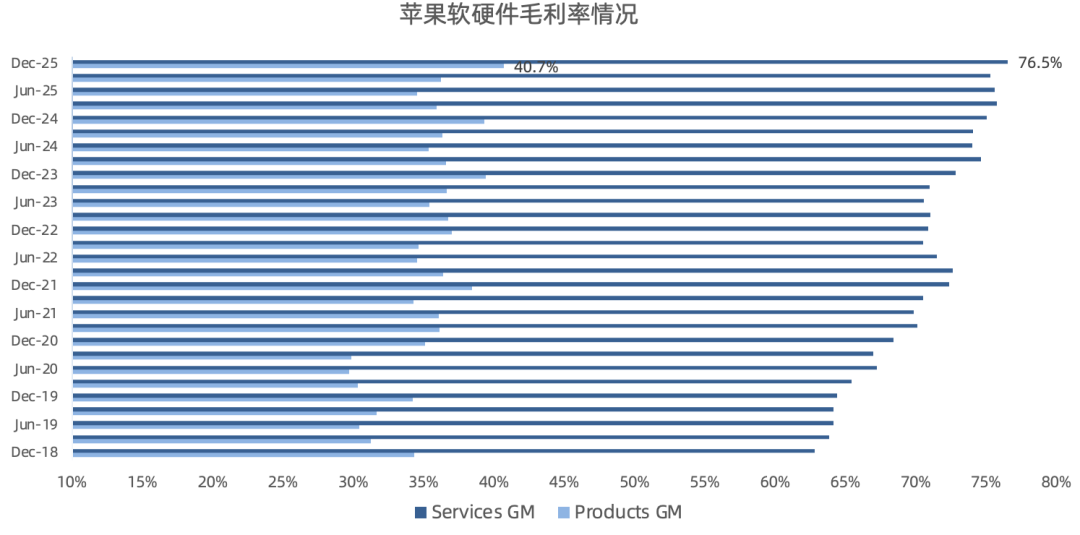

Gross margin of 48.2%, up 1.3 percentage points year over year; hardware gross margin of 40.7%, up 1.4 percentage points year over year, a record high; software gross margin of 76.5%, up 1.5 percentage points year over year.

Net income of $42.1B, up 16% year over year, above consensus of $39.4B; net margin of 29.3%.

Global active installed base across all products exceeded 2.5B devices, a new high (active defined as having used an Apple service within 90 days; FY25Q1 was over 2.35B).

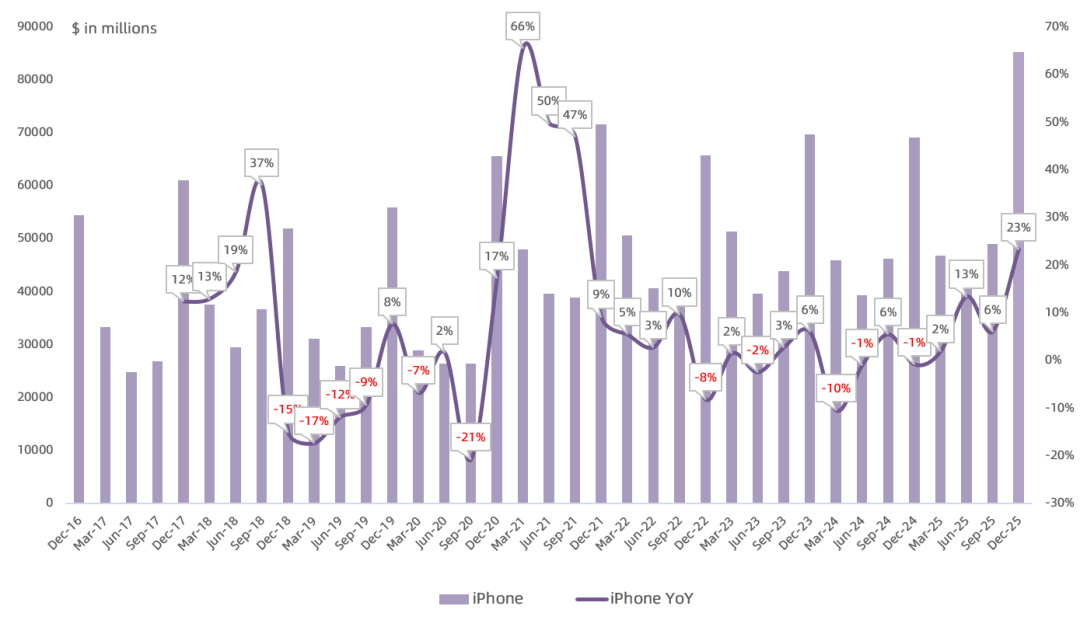

iPhone revenue of $85.3B, up 23% year over year, the fastest growth since 2021, above consensus of $78.2B. iPhone revenue set all-time records in the Americas, Greater China, Latin America, Western Europe, Middle East, Australia and South Asia, and a quarterly record in India; management even marveled at the strength of iPhone demand. iPhone active installed base grew to a new high.

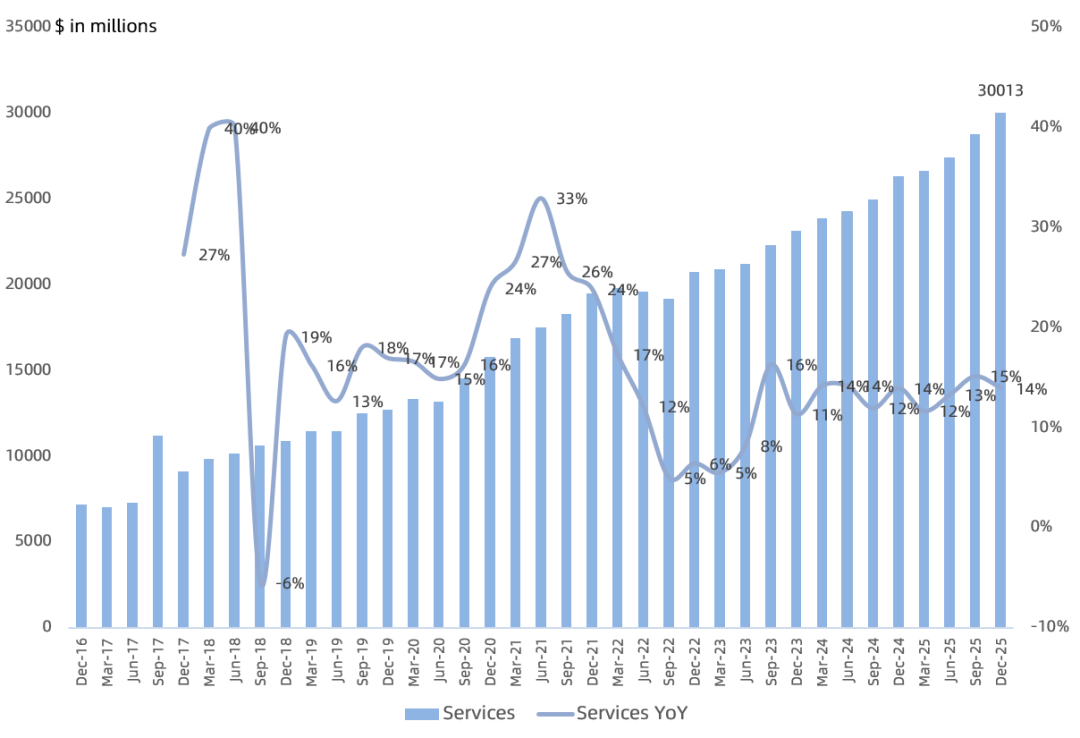

Services revenue of $30.0B, up 14% year over year, slightly below consensus. Services transacting accounts and paid accounts hit all-time highs. Global paid subscriptions exceed 1B (unchanged for 9 quarters); customer engagement continues to grow. Revenue hit records in advertising, cloud services, music, and payment services. Introducing more new ad placements in the App Store; App Store weekly active users at 850M.

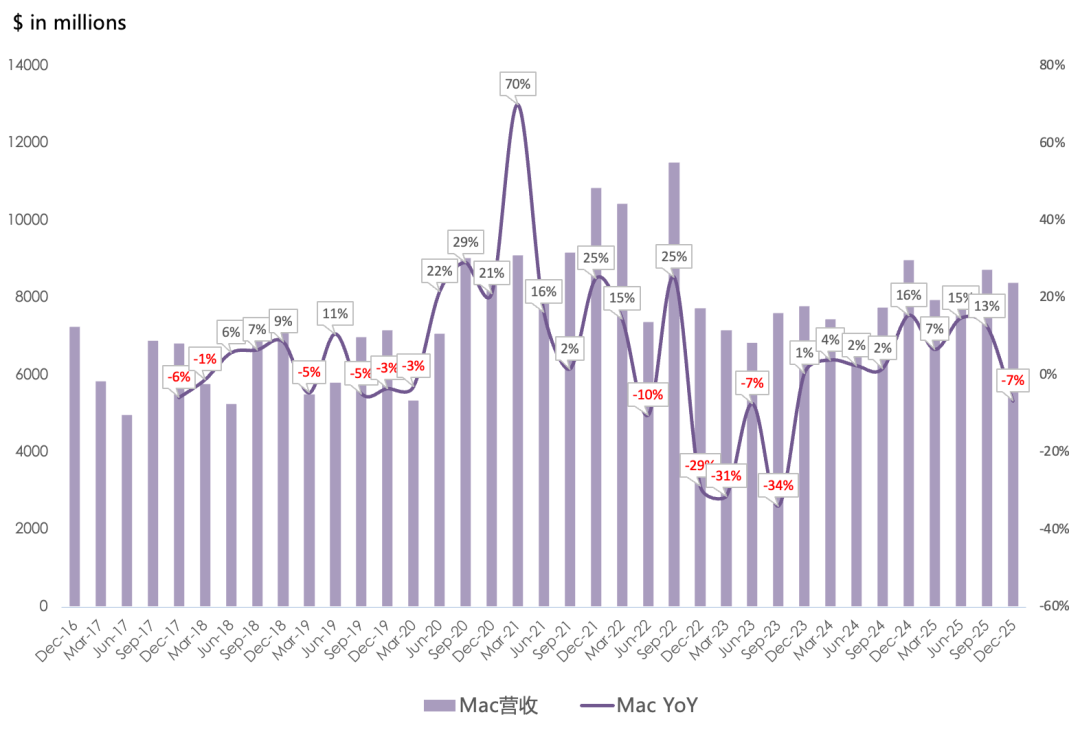

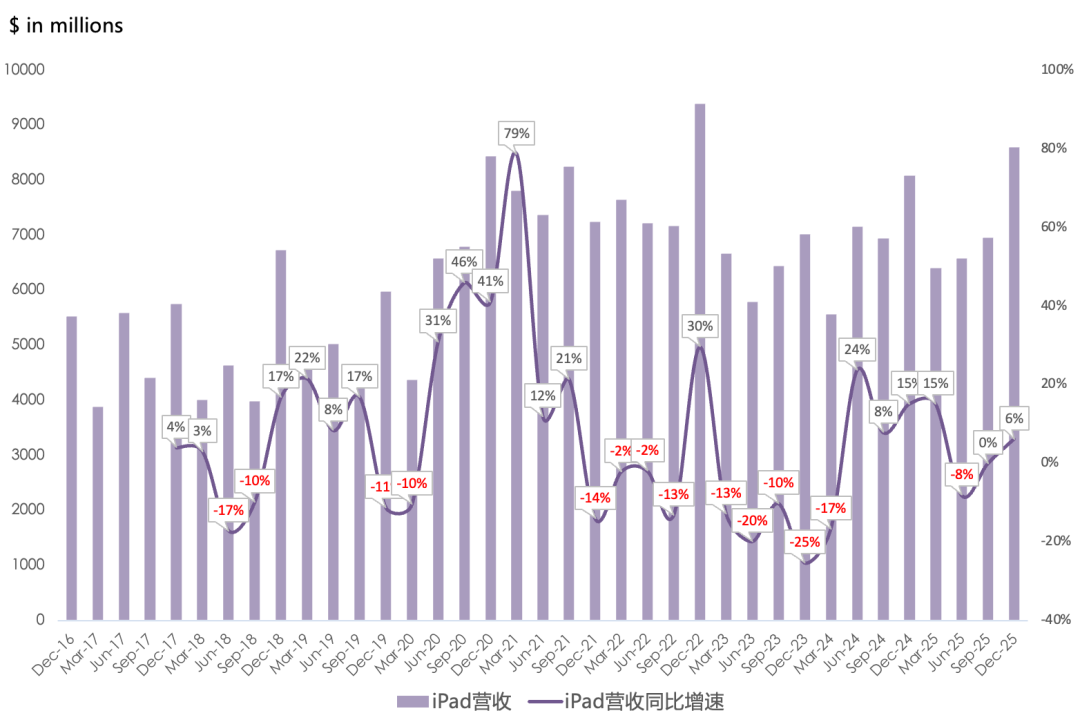

Mac revenue of $8.4B, down 7% year over year, below consensus of $9.1B. Mac installed base hit a record high; nearly half of Mac buyers were new to the product. Growth achieved in emerging markets including Brazil, India, Malaysia, and Vietnam. iPad revenue of $8.6B, up 6% year over year, above consensus of $8.2B. iPad installed base hit a record high; switchers also hit a record high.

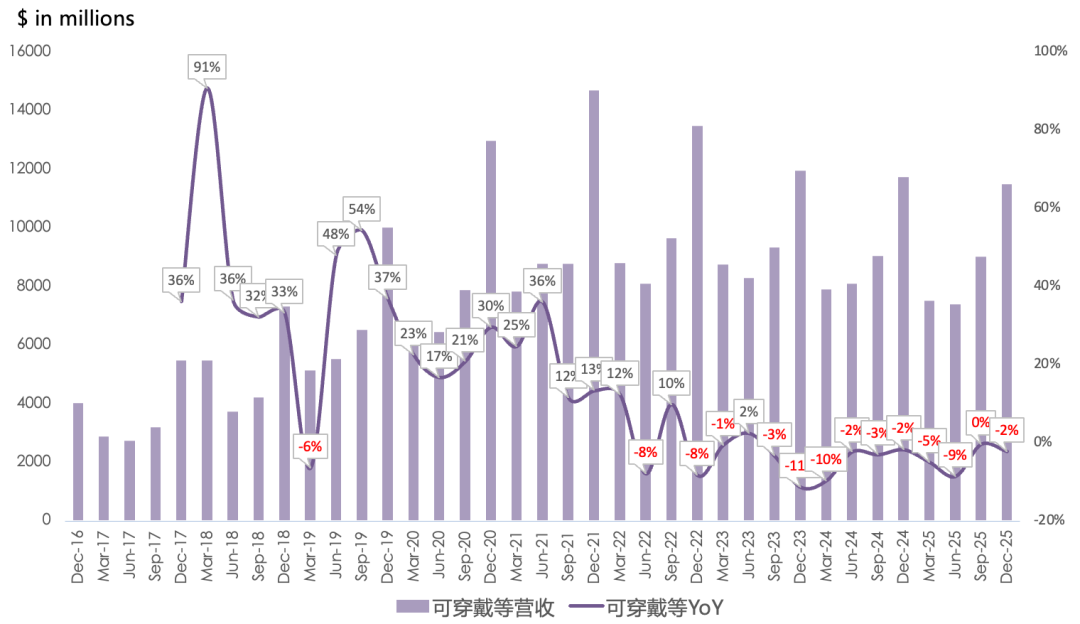

Wearables, Home and Accessories revenue of $11.5B, down 2% year over year, the 10th consecutive quarter of year-over-year decline, below consensus of $12.1B. AirPods Pro 3 supply constrained; otherwise the category would have grown.

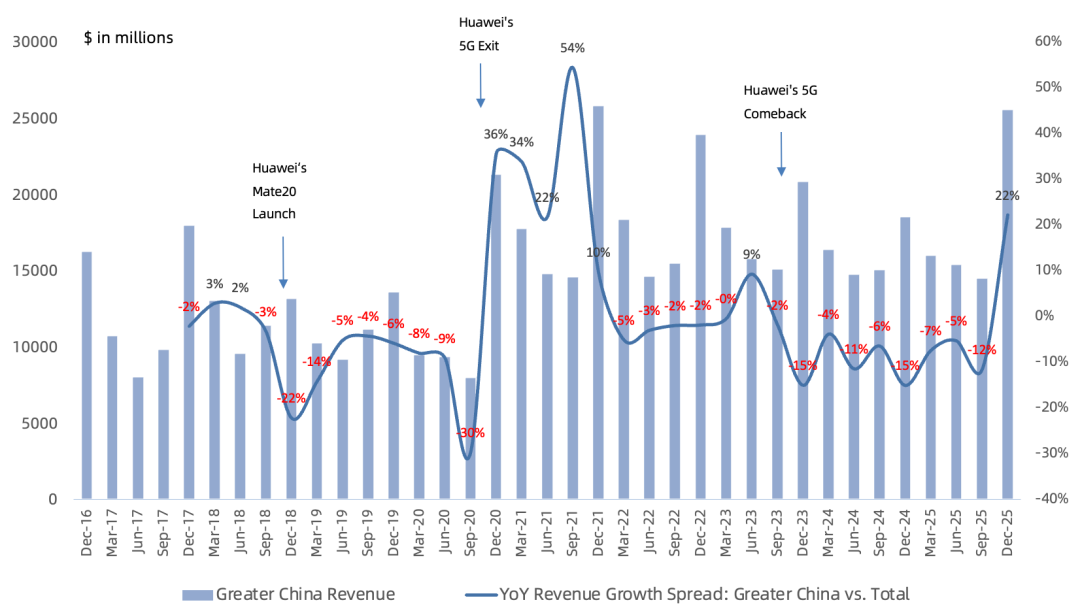

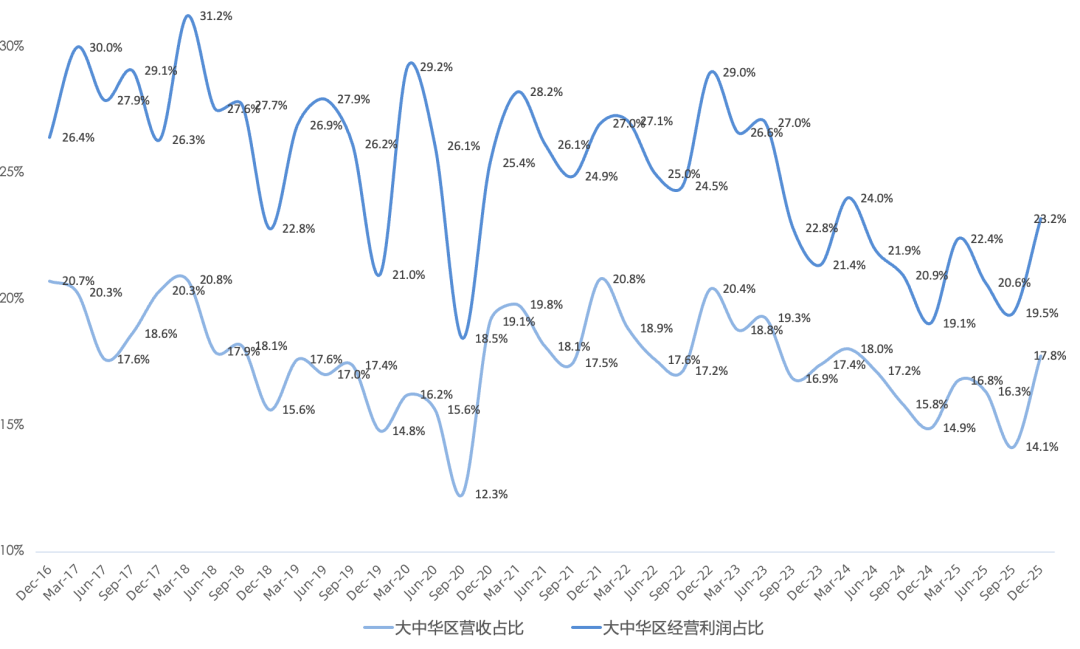

Greater China revenue of $25.5B, up 38% year over year, the fastest growth since 2021, ending nine consecutive quarters of growth lagging the company average. Driven primarily by government subsidies, Greater China was the biggest contributor to this quarter's beat. Retail store traffic in China grew strong double digits year over year. Greater China operating margin of 46.2%, up 2.1 percentage points year over year.

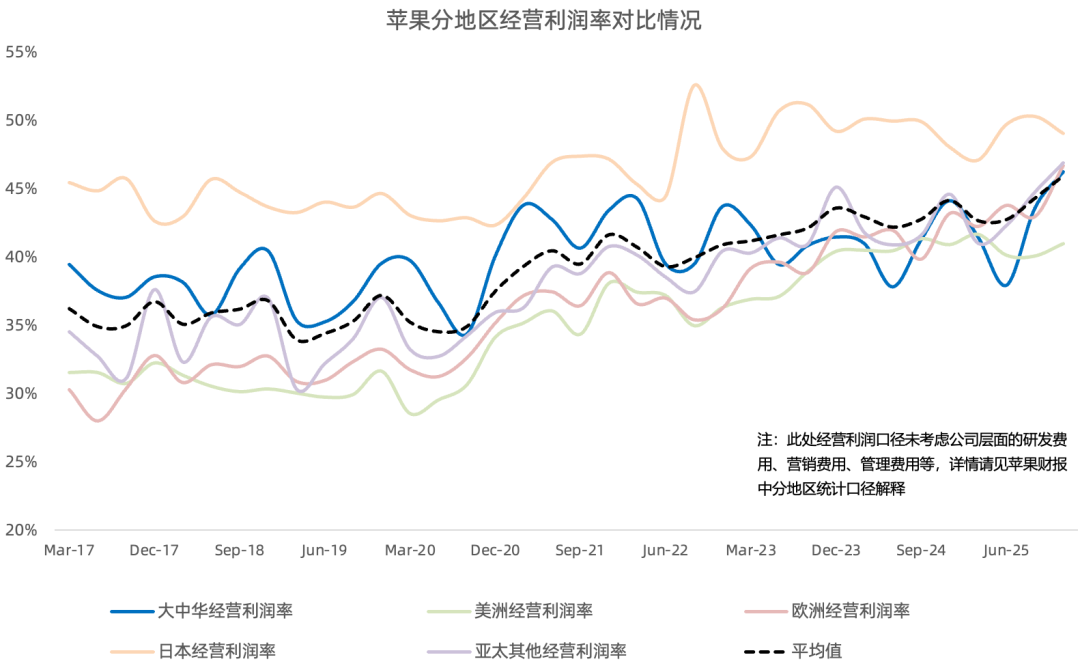

Apple's global progress: Revenue hit all-time records in the Americas, Europe, Japan, and Rest of Asia Pacific. Emerging markets continued to grow, including India (reported under Europe) with strong double-digit revenue growth. This quarter: Americas gross margin 45.6%, down 0.3 pp year over year; Europe 50.0%, up 3.3 pp; Greater China 49.0%, up 1.7 pp; Japan 52.1%, up 1.0 pp; Rest of Asia Pacific 50.0%, up 1.8 pp.

Projected FY26Q2 revenue growth of 13-16% year over year; iPhone supply constrained; Services growth consistent with this quarter (14%); gross margin 48-49%; operating expenses $18.4-18.7B; implying Q2 net income ceiling up ~20% year over year (~$29.6B), the fastest profit growth since FY22Q1.

This quarter repurchased $24.7B, paid $3.9B in dividends; net cash of $54.0B.

This quarter Enterprise won Snowflake for over 9,000 Mac devices and AstraZeneca for over 5,000 M5-powered iPad Pros.

iPhone supply constraints mainly due to advanced process (TSMC N3 node) capacity limits. Memory price increases expected to impact gross margin starting next quarter, but guidance is actually quite optimistic.

Collaborating with Google on next-generation Apple foundation models; the technology driving a more personalized Siri is understood to be the Google collaboration, while true foundation models will still be developed independently.

CapEx follows a hybrid model; CapEx may fluctuate and does not necessarily track in step with business scale and performance.

Overall, this earnings report relied heavily on strong iPhone and Greater China performance, with next-quarter growth guidance above expectations, delivering a long-absent 20% profit growth rate. As for the market's top concern—memory price impact—the gross margin guidance suggests no effect, but the second half remains uncertain. One might end up judging the storage cycle peak by when Apple can no longer hold the line.

Apple's Core Growth Formula:

AAPL = active installed base (2.5 billion devices) x customer engagement (Services revenue)

Although both sides of Apple's core growth formula are still growing, Services growth remains persistently soft, and valuation is not cheap (10-year average PE midpoint 22.7x).