Ten charts to understand Apple's latest earnings

Apple FY2022 Q3 Earnings Summary:

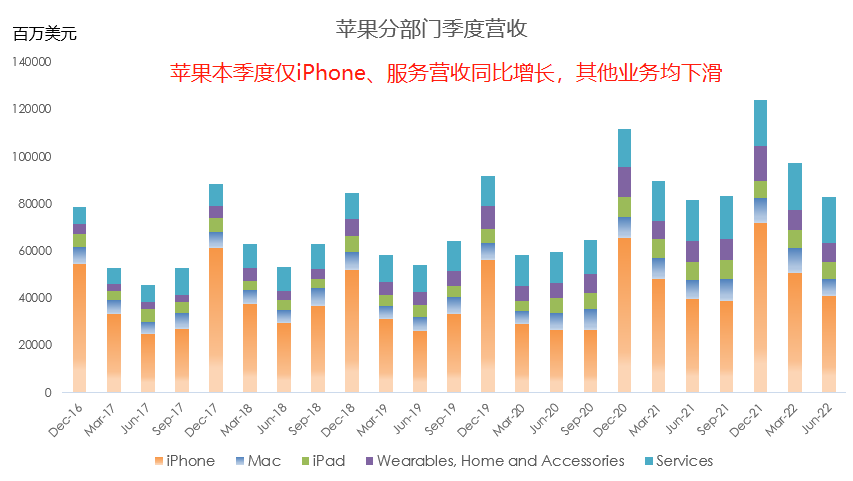

Revenue was $82.96B, up 1.9% year over year. Net income was $19.44B, down 10.6% year over year, the first profit decline in seven quarters.

Global active installed base of iPhone, Mac, iPad, and wearables hit new highs. Apple's future strategy: installed base × customer engagement.

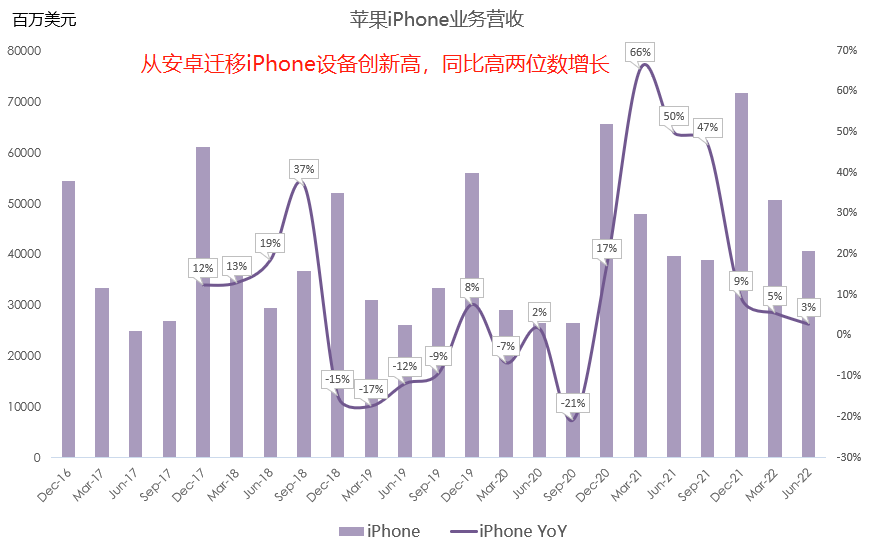

iPhone revenue was $40.67B, up 3% year over year. Android-to-iPhone switchers hit a record, up high double digits year over year.

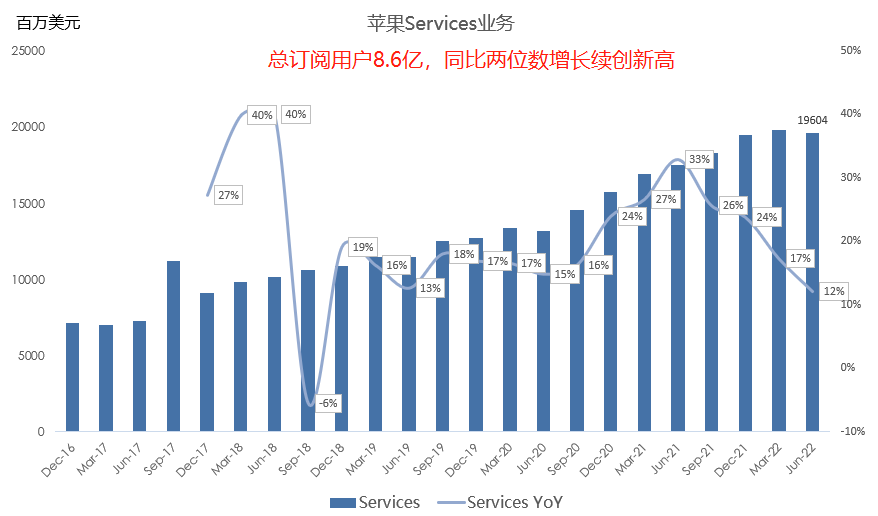

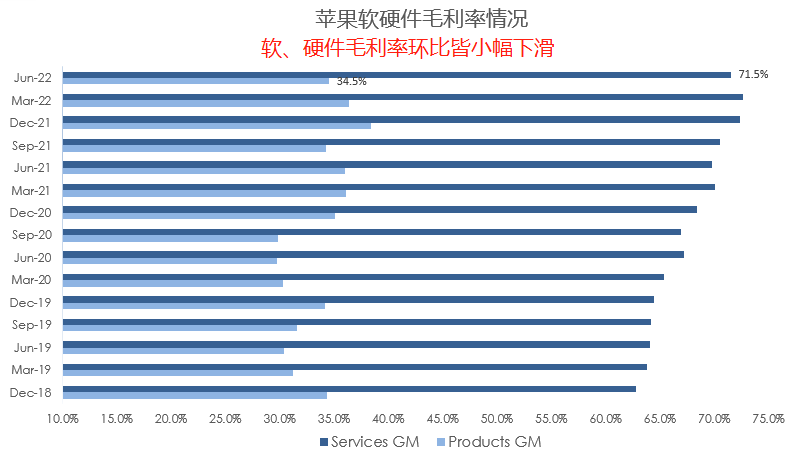

Services revenue was $19.6B, up 12% year over year, the 15th consecutive quarter of double-digit growth. Services gross margin was 71.5% this quarter. Paid subscriptions reached 860M, up double digits year over year, a new record. Apple Music, iCloud, Apple Care, and Apple Pay revenue hit records in the U.S., Mexico, Brazil, Korea, and India.

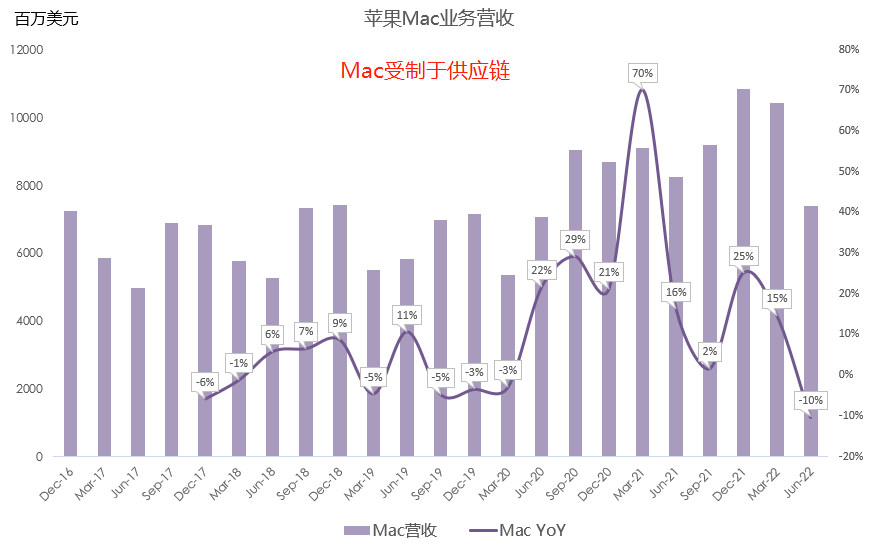

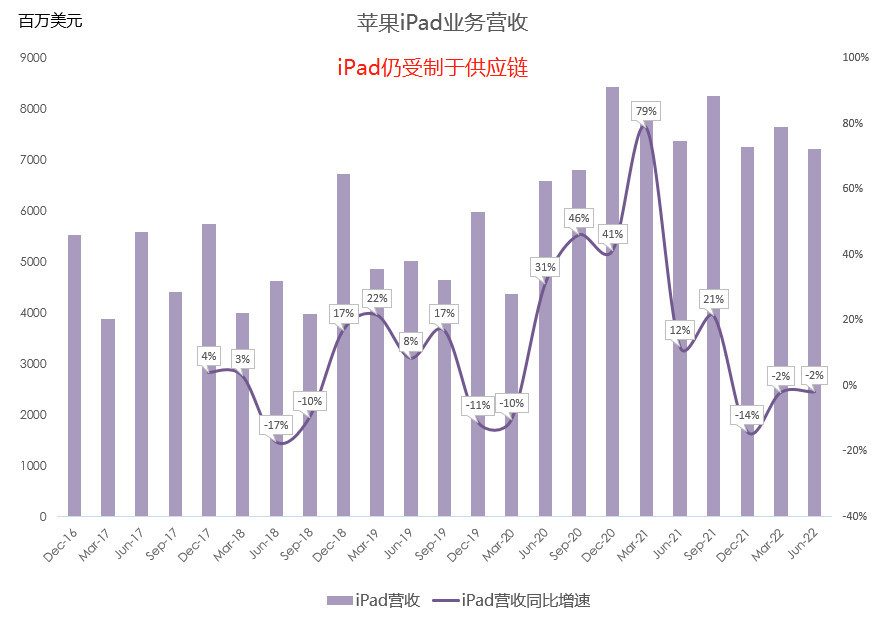

Mac revenue was $7.38B, down 10% year over year, the first decline in nine quarters. iPad revenue was $7.22B, down 2% year over year, the third consecutive quarterly decline. Demand for iPad and Mac remains strong; the declines were supply-constrained.

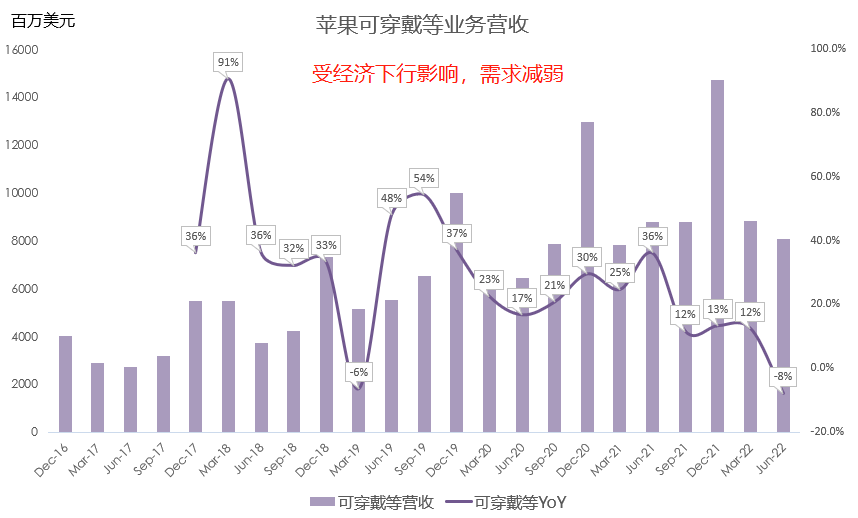

Wearables, Home and Accessories revenue was $8.08B, down 8% year over year, the first decline in 13 quarters. Apple acknowledged a material demand impact from the economic slowdown on this segment.

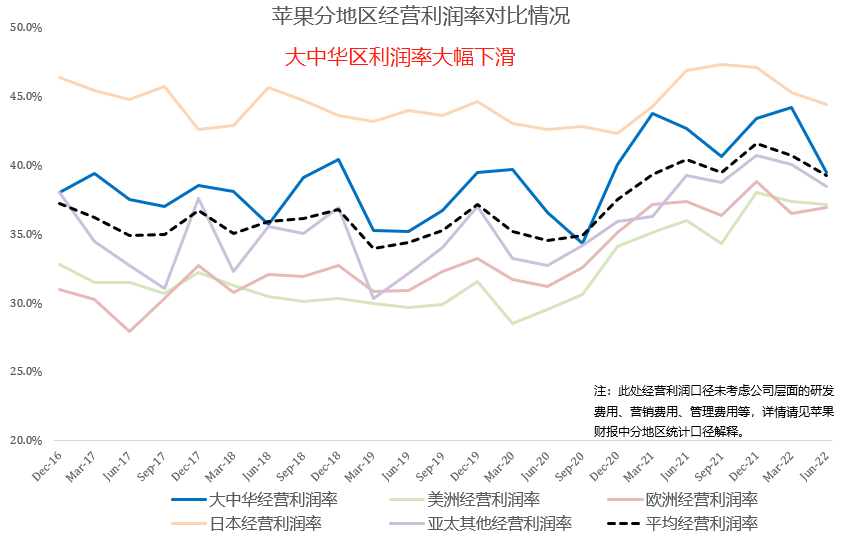

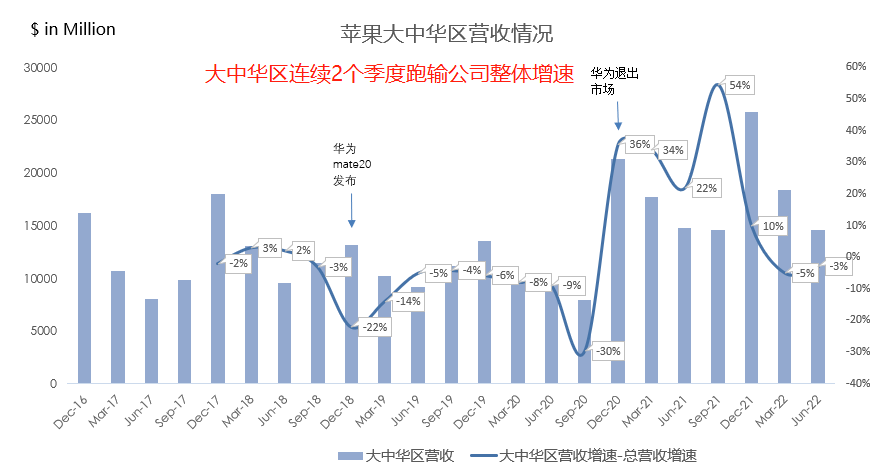

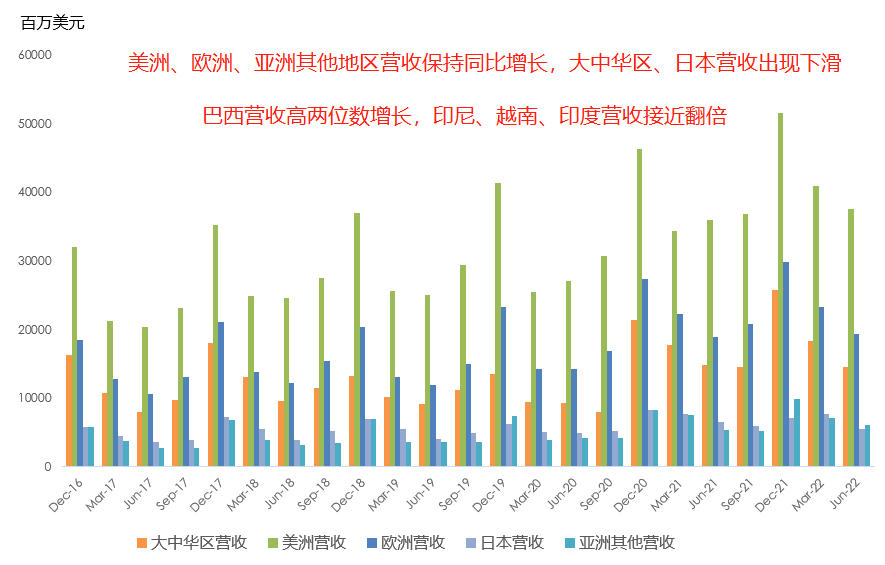

Greater China revenue was $14.6B, down 1% year over year, underperforming total Apple growth for the second consecutive quarter; FX had some impact. iPhone declined; Services grew. Greater China operating margin was 39.4%, down 480 bps sequentially. Americas and Europe revenue grew 4% and 2% year over year respectively; Europe's resilience was surprising.

Brazil revenue grew high double digits; Indonesia, Vietnam, and India revenue nearly doubled. Apple is gaining ground in emerging markets; BNPL is also planned for emerging markets. Enterprise wins included Bank of America and Wipro.

Apple stated that iPhone, Mac, and iPad demand was not affected by the economic slowdown; only wearables and the advertising portion of Services were impacted. It guided for Q4 revenue to grow sequentially despite a 6-point FX headwind. Services revenue is expected to grow year over year, albeit at a slower pace than Q3. Consolidated gross margin guided at 41.5%-42.5%.

Overall, this report slightly beat expectations. iPhone remained resilient amid the slowdown, while emerging markets' strength offers future upside. Services' importance is highlighted in this environment, akin to Amazon's AWS Marketplace. The installed base × customer engagement formula has a massive left-hand side; Apple must keep pushing the right-hand side.