Apple FY24Q3 corresponds to the actual period of April/May/June 2024.

Apple FY2024 Q3 Earnings Summary:

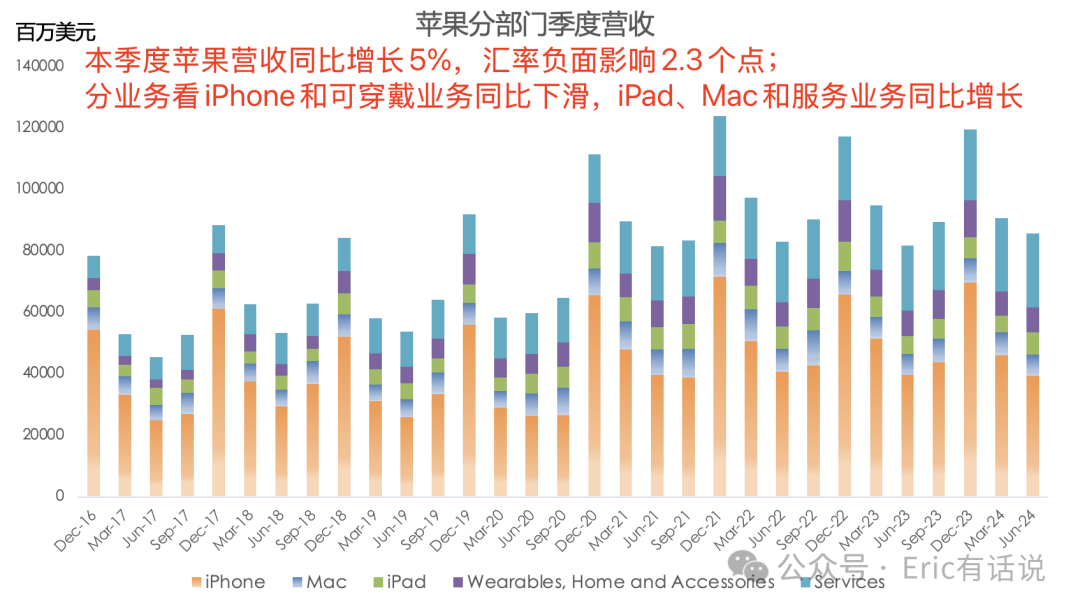

Revenue was $85.777B, up 4.9% year over year, with a 2.3-percentage-point FX headwind; net income was $21.448B, up 7.9% year over year; EPS was up 11.1% year over year.

Active devices across all products and regions globally reached an all-time high (devices that have used Apple services within 90 days are considered active; the figure was not updated this quarter, but stood at over 2.2B in FY24Q1).

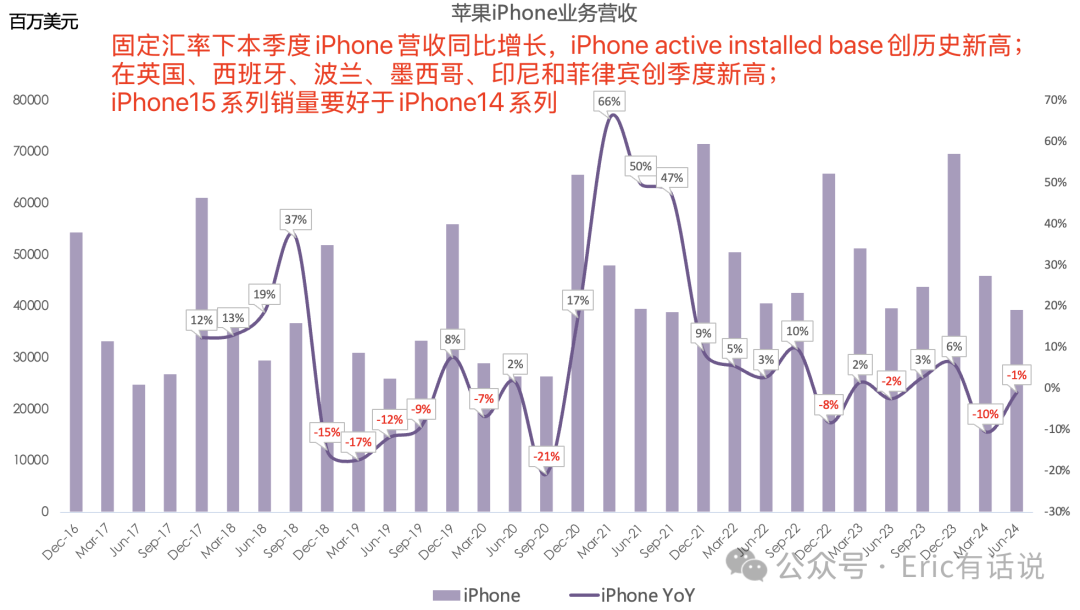

iPhone revenue was $39.3B, down 1% year over year, but up on a constant-currency basis; iPhone active installed base hit an all-time high; quarterly records were set in the UK, Spain, Poland, Mexico, Indonesia, and the Philippines; iPhone 15 series sell-through was better than iPhone 14 series.

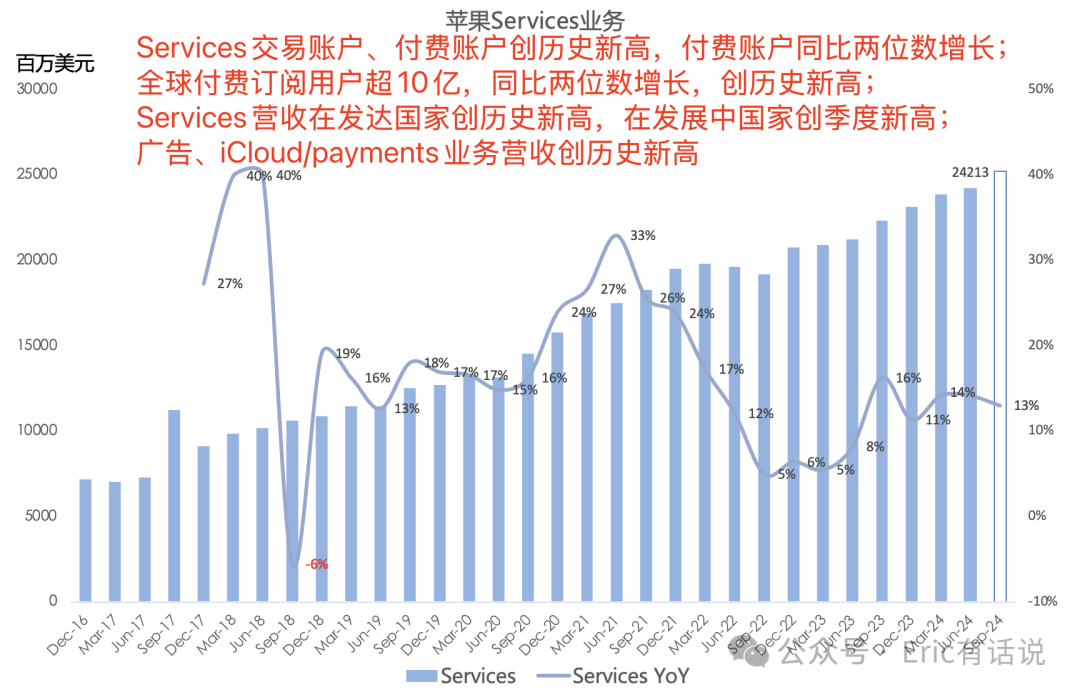

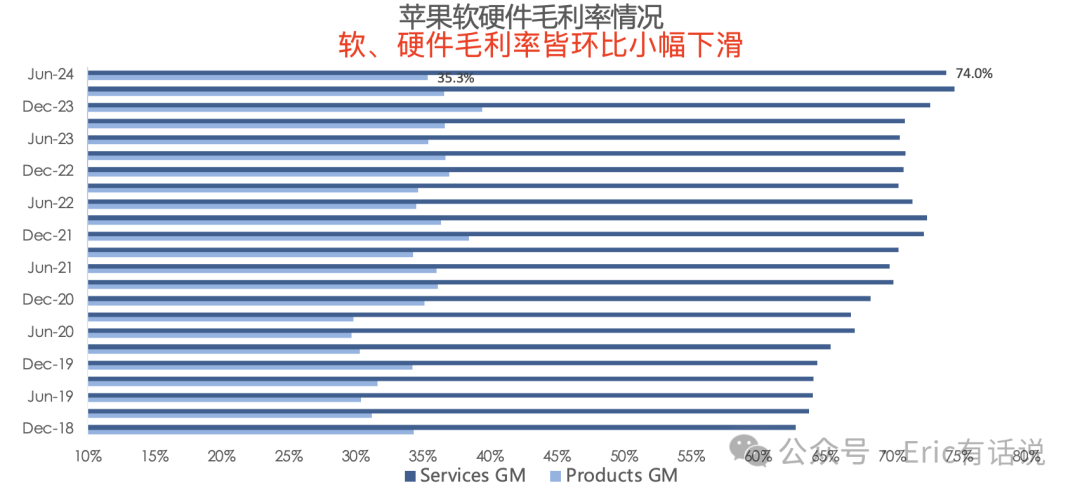

Services revenue was $25.2B, up 14% year over year, marking the seventh consecutive quarterly record; Services gross margin was 74%, down 0.6 percentage points sequentially; Services transacting accounts and paid accounts hit all-time highs, with the latter up double digits year over year; global paid subscriptions exceeded 1B, up double digits year over year, an all-time high.

Services revenue hit all-time highs in developed markets and quarterly records in emerging markets; advertising, iCloud, and payments revenue hit all-time highs; EU App Store revenue accounted for 7% of total App Store revenue.

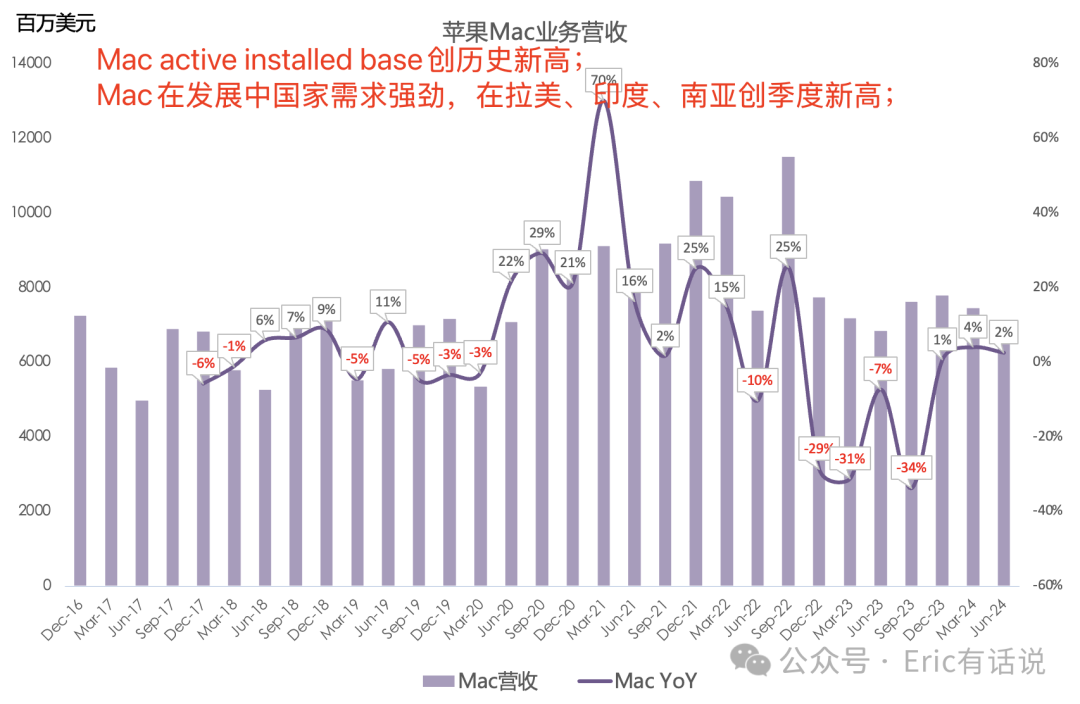

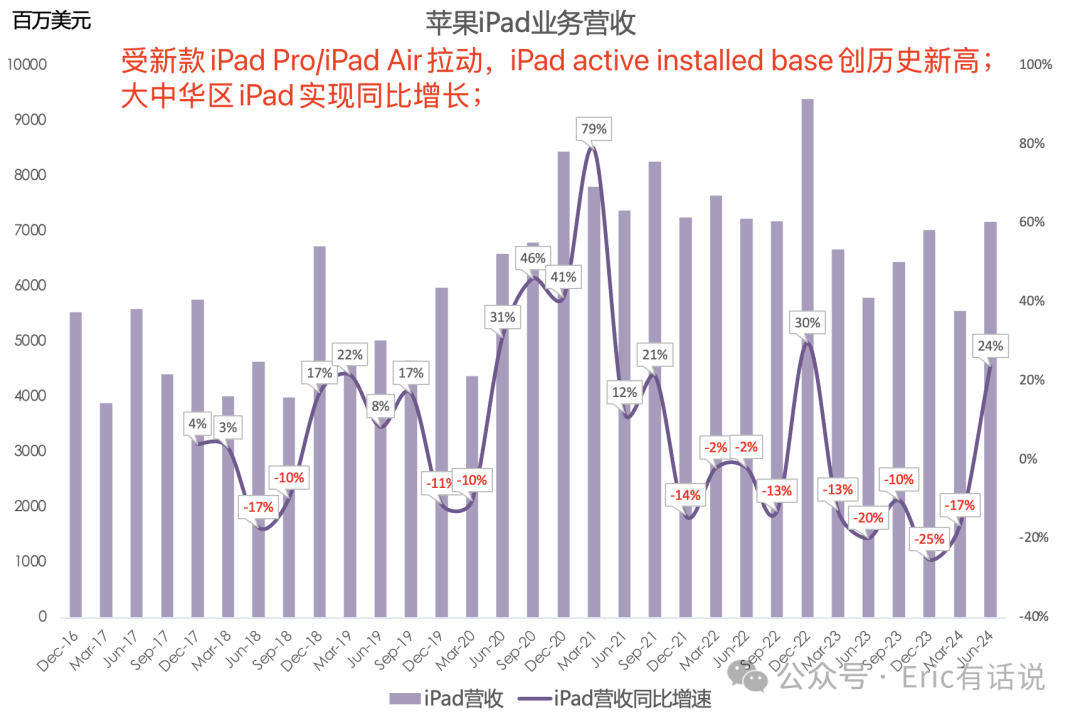

Mac revenue was $7.0B, up 2% year over year; Mac active installed base hit an all-time high; Mac demand was strong in emerging markets, with quarterly records in Latin America, India, and South Asia; iPad revenue was $7.2B, up 24% year over year driven by new iPad Pro and iPad Air models, ending five consecutive quarters of double-digit year-over-year declines; Greater China iPad also grew year over year; iPad active installed base hit an all-time high.

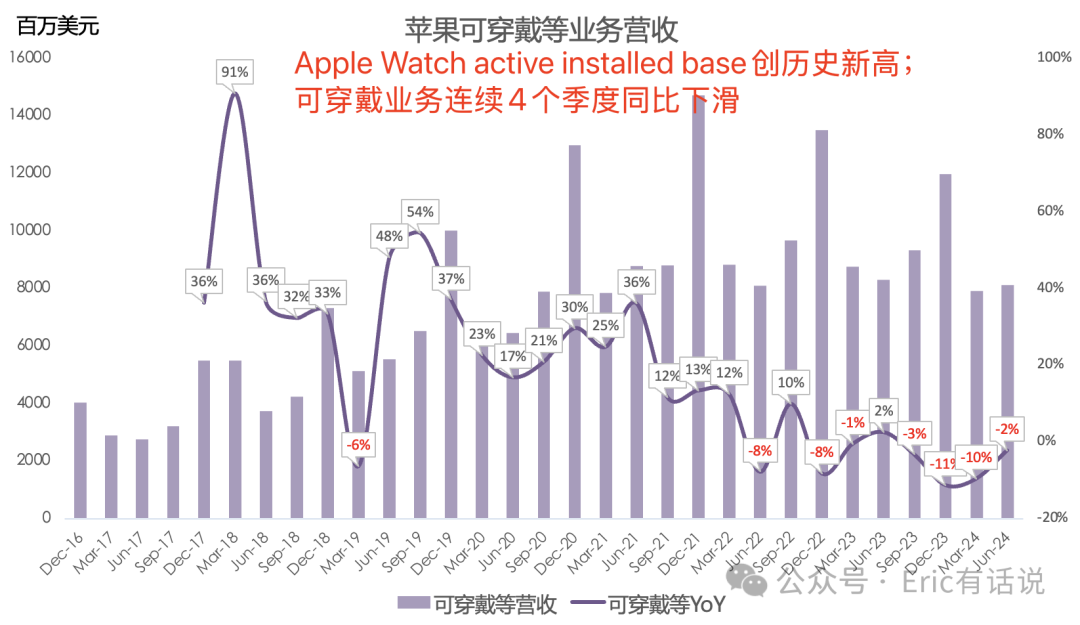

Wearables, Home and Accessories revenue was $8.1B, down 2% year over year, the fourth consecutive quarterly decline; Apple Watch active installed base hit an all-time high.

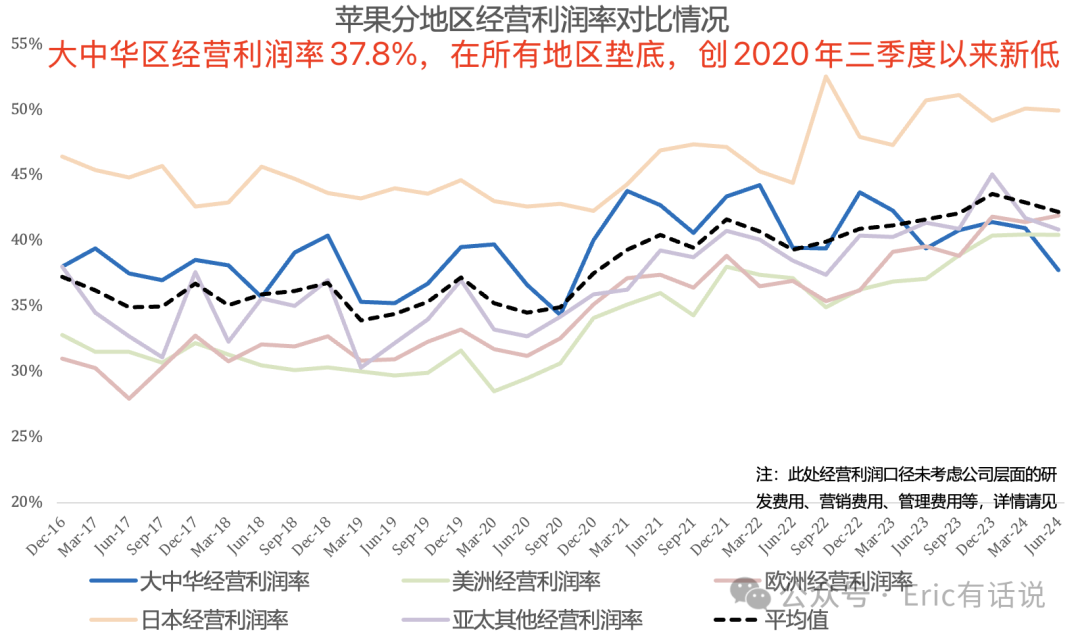

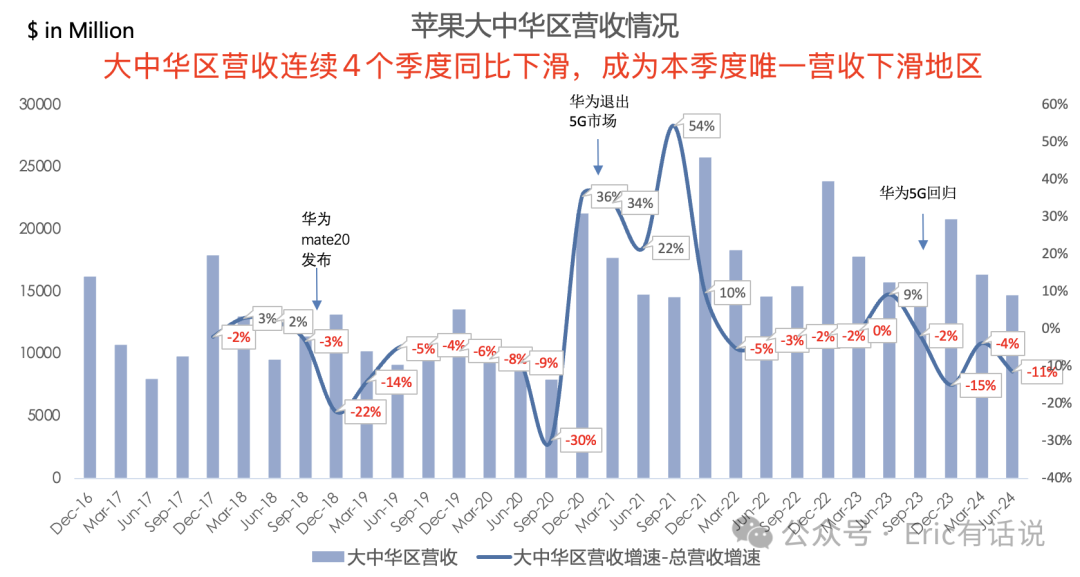

Greater China revenue was $14.7B, down 7% year over year, down 3% on a constant-currency basis, the fourth consecutive quarterly decline; Greater China operating margin was 37.8%, the lowest of all regions, a new low since Q3 2020; this quarter only Greater China revenue declined year over year, while the rest of Asia-Pacific posted the fastest growth.

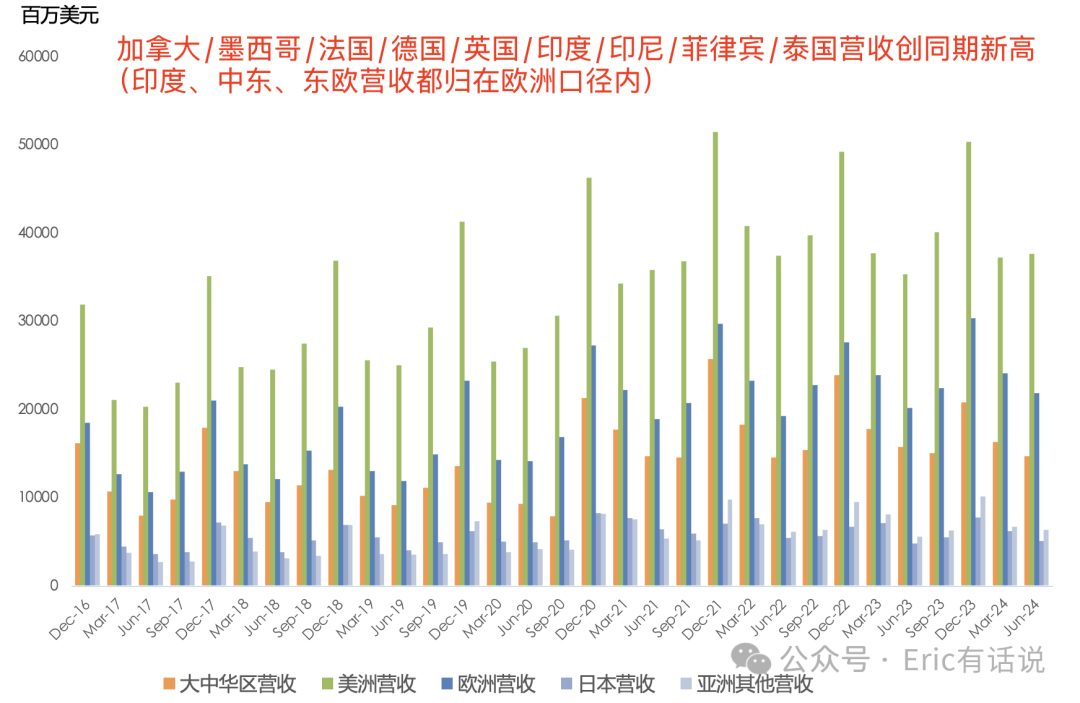

Apple continued to gain share in numerous markets globally, setting same-period revenue records this quarter in Canada, Mexico, France, Germany, the UK, India, Indonesia, the Philippines, and Thailand.

The EU's App Store sideloading mandate took effect in March; this quarter EU App Store revenue accounted for 7% of the company's total App Store revenue, and the impact appears limited so far.

FY24Q4 revenue is guided to grow 5% year over year, with a 1.5-percentage-point FX headwind; Services revenue growth is expected to be consistent with the first three quarters; gross margin 45.5%-46.5%, opex $14.2B-$14.4B, implying Q4 revenue growth of ~5% year over year and net income growth of ~5% year over year.

The company repurchased $26B of shares and paid $3.9B in dividends this quarter.

Cook believes Apple Intelligence will drive an iPhone upgrade cycle.

Overall, this Apple earnings report was mediocre; its growth rates (revenue YoY +5%, net income YoY +8%) lagged the other three mega-cap peers—Microsoft (revenue YoY +15%, net income YoY +10%), Google (revenue YoY +14%, net income YoY +29%), and Amazon (revenue YoY +10%, net income YoY +100%). Microsoft, Google, and Amazon all delivered solid profit results despite massive AI investment, yet the market still worries that overinvestment will hurt profits, while pinning outsized hopes on Apple's AI despite its currently smaller spend—an ironic dynamic.

Apple's core growth formula: AAPL = active installed base * customer engagement (active installed base at new high * paid subscribers at new high).

Both sides of Apple's core growth formula are still expanding, but management has not updated specific figures this quarter. The Apple flywheel remains hardware-weak, software-driven, with software still below 30% of revenue; the runway for further growth bears watching. Will Greater China remain weak? Although Cook cited signs of recovery in the second half, is the market overly optimistic about AI driving iPhone 16 series volume growth?