Apple FY24Q4 corresponds to calendar July/August/September 2024.

Apple FY2024 Q4 Earnings Summary:

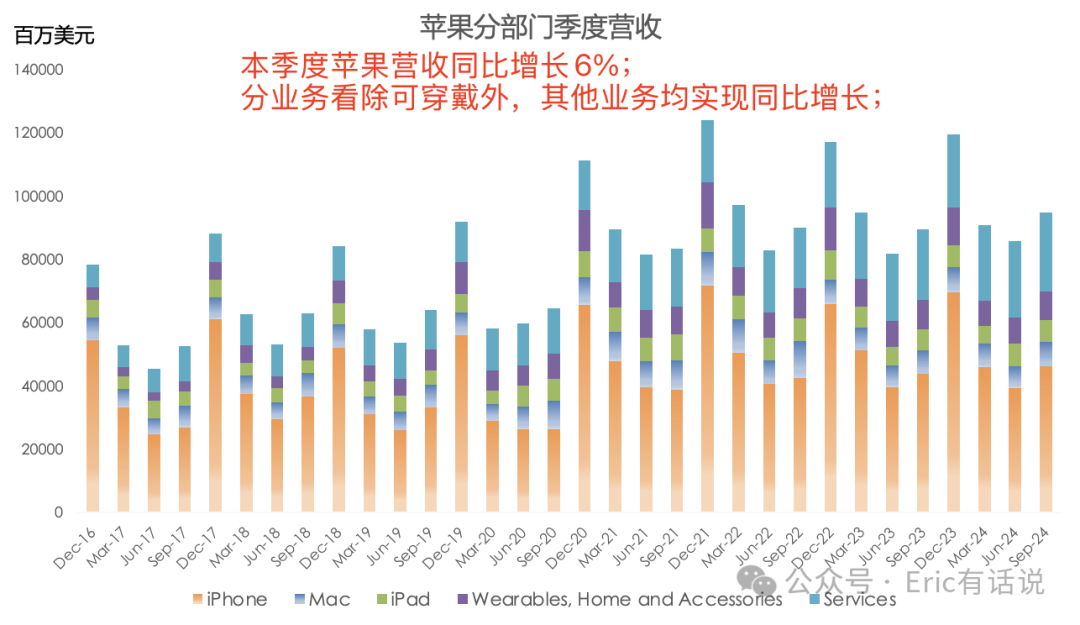

Revenue $94.93B, up 6.1% year over year; net income $14.736B, excluding one-time tax impact net income $24.982B, up 8.8% year over year; adjusted EPS up 12.3% year over year.

Active installed base across all products and regions hits record high (device used Apple services within 90 days = active; FY24Q1 was 2.2B+, not updated for 3 quarters).

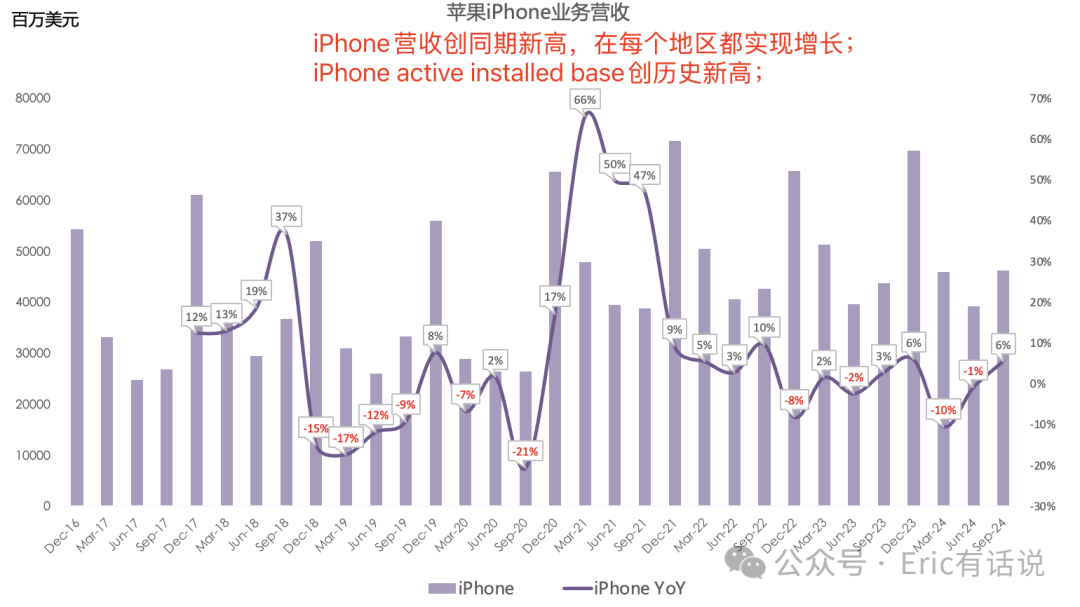

iPhone revenue $46.222B, up 6% year over year, record for the period; iPhone active installed base at record high.

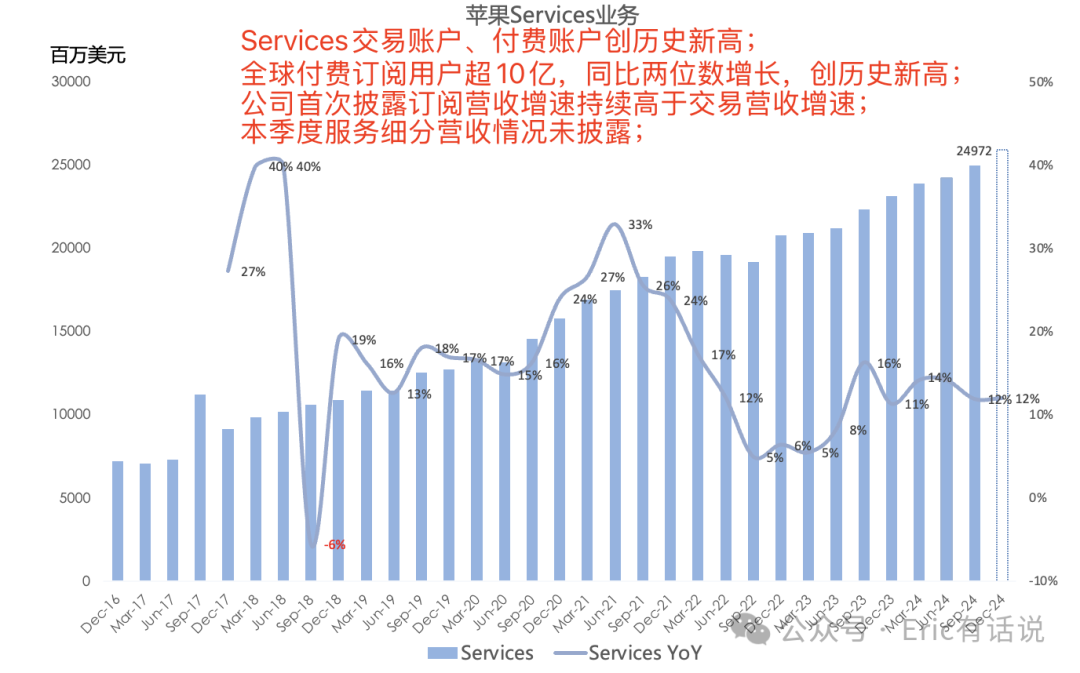

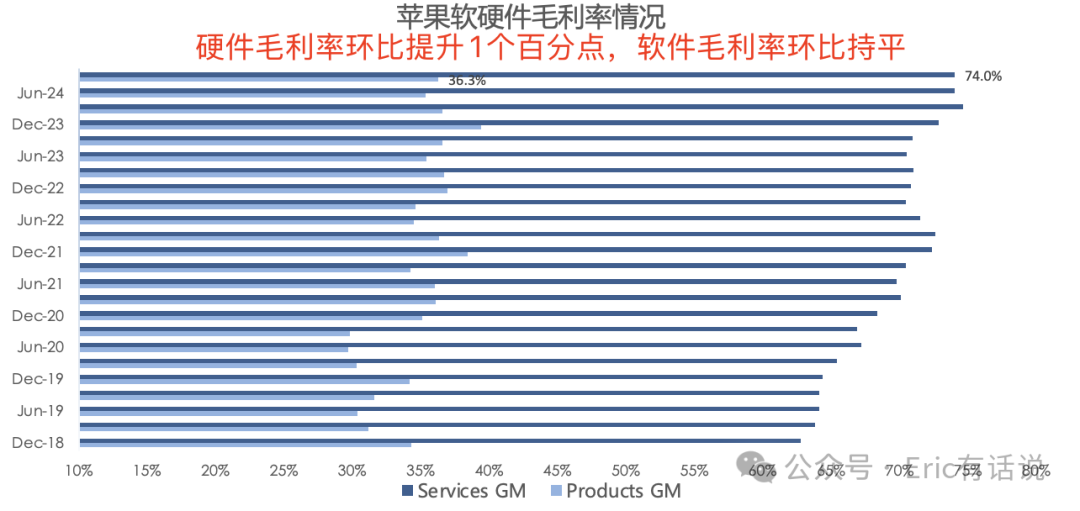

Services revenue $24.972B, up 12% year over year, 8th consecutive quarterly record; services gross margin 74%, flat sequentially; Services transacting and paid accounts at record highs; global paid subscriptions 1B+ (not updated for 4 quarters), up double digits year over year, record high; company disclosed for first time that subscription revenue growth consistently exceeds transaction revenue growth; services revenue breakdown not disclosed this quarter.

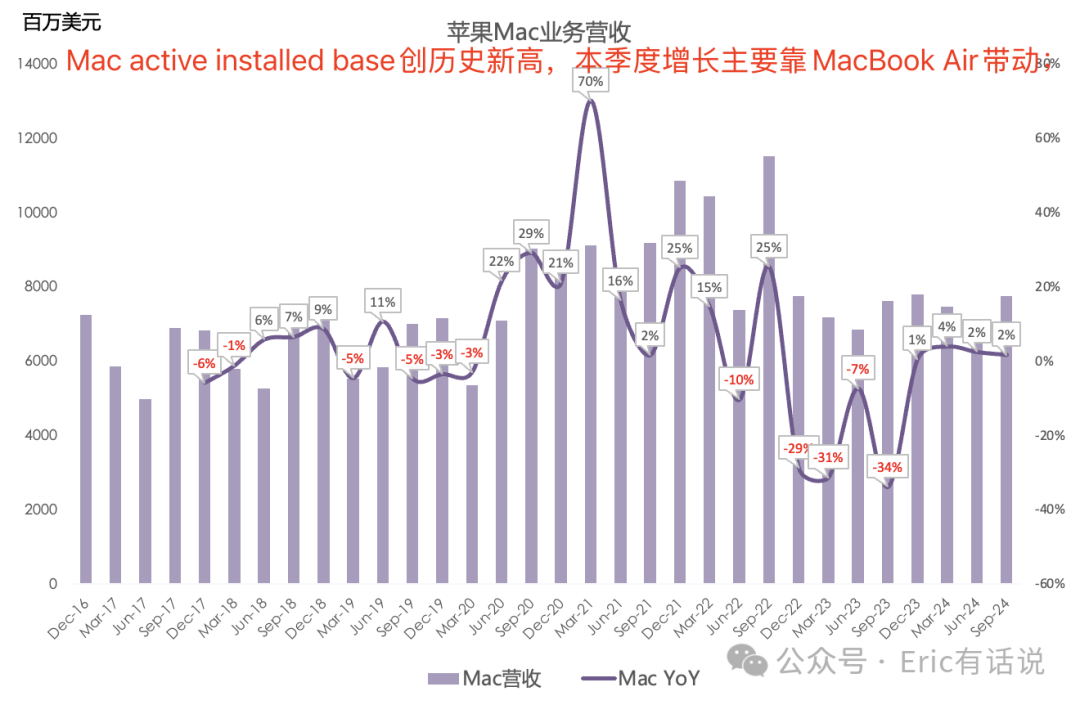

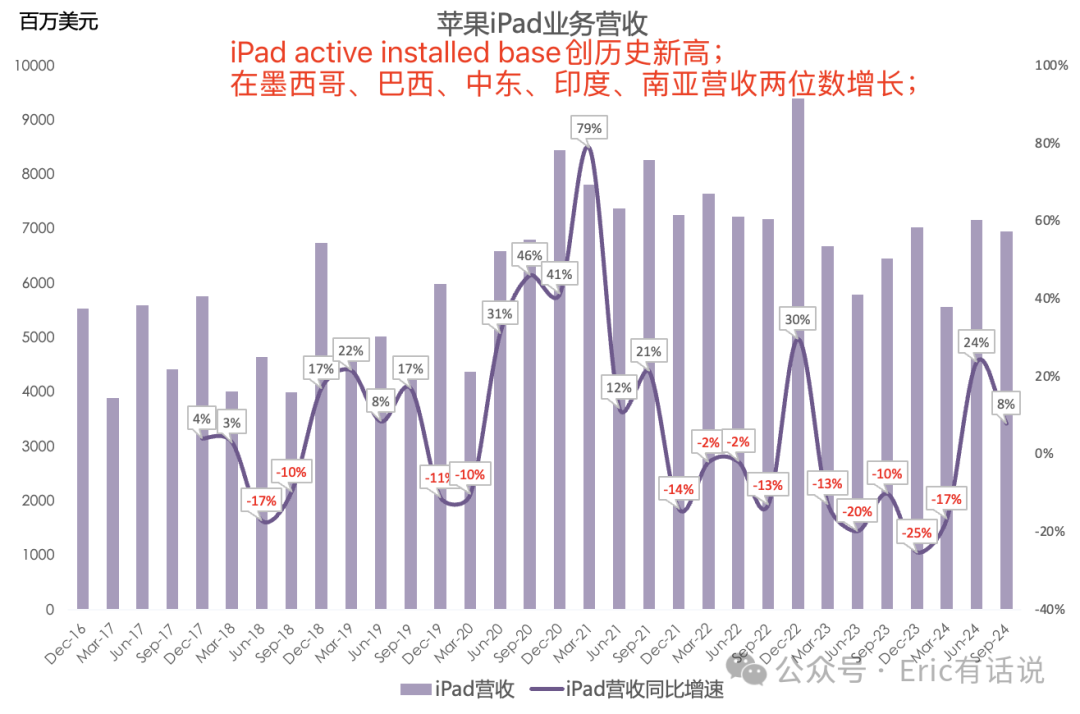

Mac revenue $7.744B, up 2% year over year, Mac active installed base record high, growth driven by MacBook Air; iPad revenue $6.95B, up 8% year over year, iPad active installed base record high, double-digit revenue growth in Mexico, Brazil, Middle East, India, South Asia.

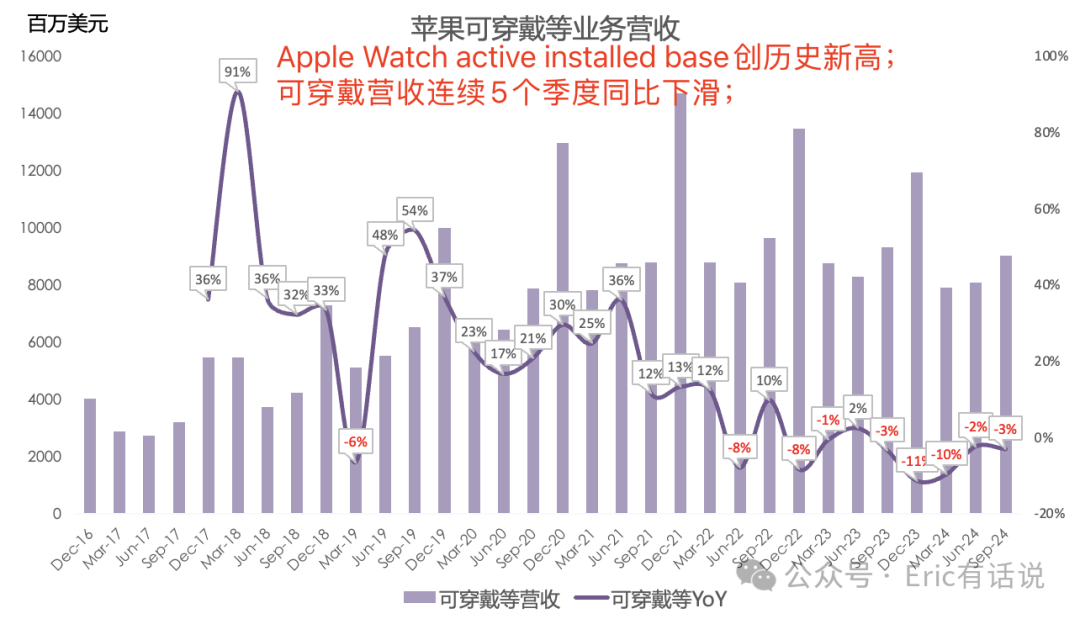

Wearables, Home & Accessories revenue $9.042B, down 3% year over year, 5th consecutive quarterly decline; Apple Watch active installed base record high.

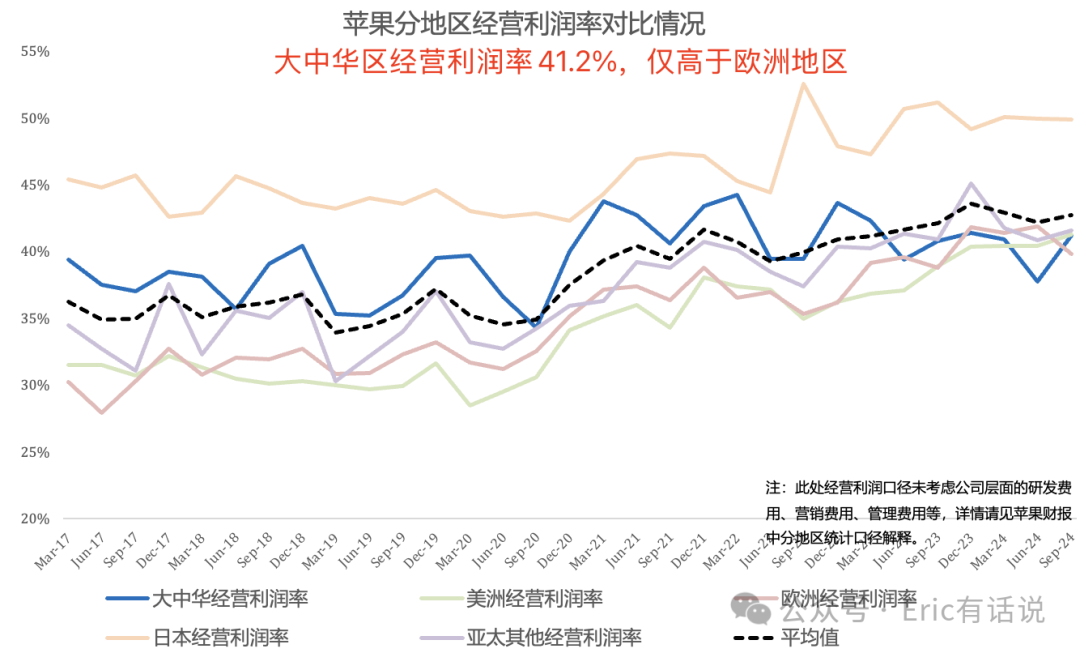

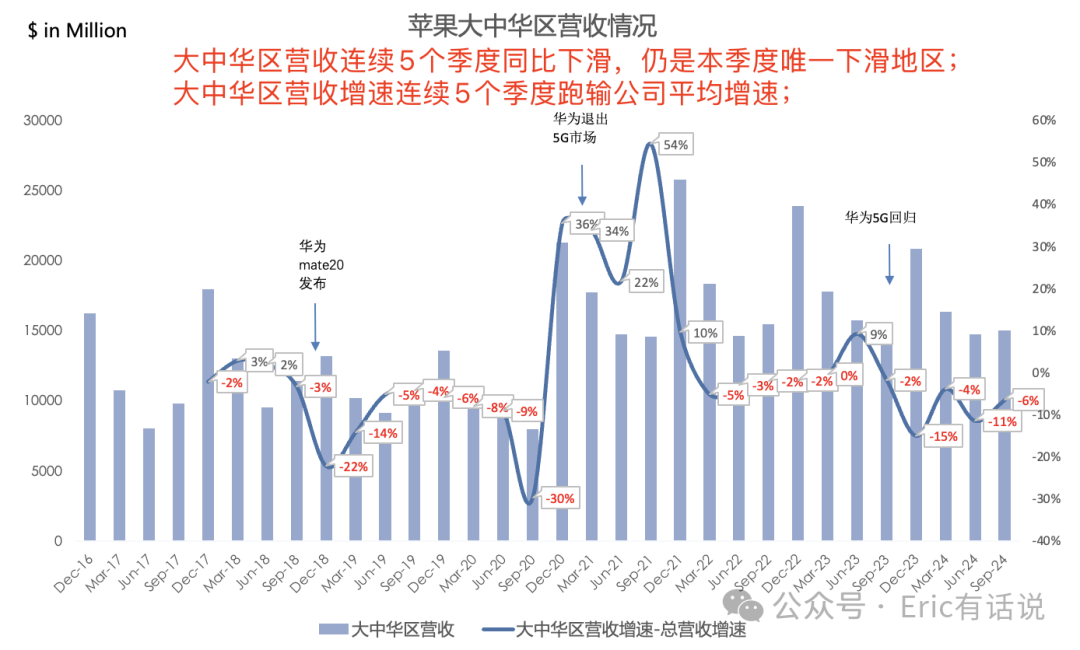

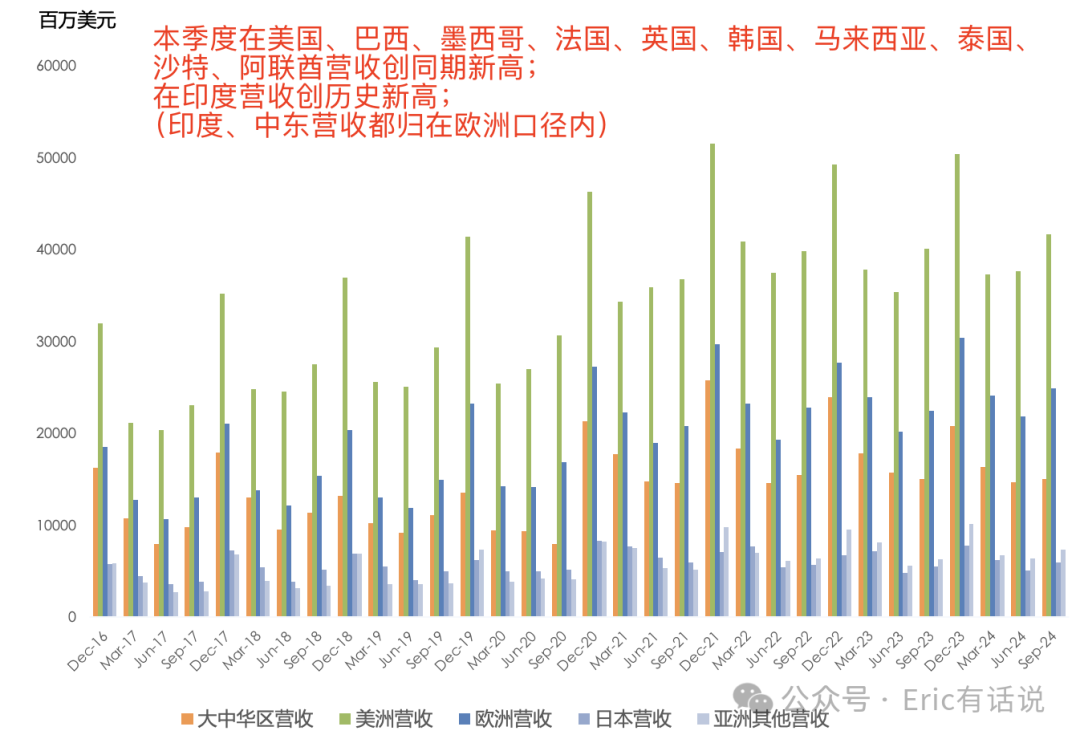

Greater China revenue $15.033B, down 0.3% year over year, 5th consecutive quarterly decline; Greater China operating margin 41.2%, only above Europe; this quarter only Greater China revenue declined year over year; Europe grew fastest.

Apple continued to gain ground in numerous global markets. This quarter, revenue hit period highs in the US, Brazil, Mexico, France, the UK, South Korea, Malaysia, Thailand, Saudi Arabia, and the UAE, and reached an all-time high in India.

Enterprise services landed a large NVIDIA order this quarter, purchasing 10,000 Macs.

FY25Q1 revenue is guided to grow low- to mid-single digits year over year; services revenue growth is expected to be consistent with the prior fiscal year (12%-13%); gross margin 46%-47%; opex $15.3-15.5B. This implies Q4 revenue growth of roughly 3% year over year and net income growth of roughly 3% year over year.

The company repurchased $25B of shares and paid $3.8B in dividends this quarter.

Greater China's sequential growth improvement this quarter was primarily driven by FX; Europe's higher growth was mainly due to strong performance in the Middle East and India, while Western Europe also grew.

Non-English versions of Apple Intelligence will launch in April next year; capex does not reflect the company's AI investment, which is primarily funded through internal resource allocation.

Overall, Apple's earnings were mediocre. Its growth rates (revenue YoY +6%, net income YoY +9%, forward PE 30.5x) remained at the bottom among the four mega-cap peers: Microsoft (revenue YoY +16%, net income YoY +11%, forward PE 32.5x), Google (revenue YoY +15%, net income YoY +34%, forward PE 21.3x), and Amazon (revenue YoY +11%, net income YoY +55%, forward PE 39.1x). Next-quarter guidance was also uninspiring. How can Buffett tolerate this? Microsoft, Google, and Amazon all delivered solid profit results despite massive AI spending, yet the market worries their overinvestment will hurt profits, while simultaneously harboring great expectations for Apple's AI, which currently involves far less investment.

Apple's core growth formula: AAPL = active installed base * customer engagement (active installed base at new high * paid subscribers at new high).

Both sides of Apple's core growth formula are still expanding, but management has not updated the numbers in a long time. The flywheel remains hardware-weak, with growth entirely dependent on software; software's share of revenue has yet to reach 30%, so the runway for further growth bears watching. Will Greater China stay weak? CAICT data showed iPhone shipments fell 40% year over year in September (assuming all foreign-brand shipments are Apple). The market remains overly optimistic that AI will drive iPhone 16 series volume growth.