Apple's FY25 Q3 results correspond to the actual period of April/May/June 2025.

Apple FY2025 Q3 Earnings Summary:

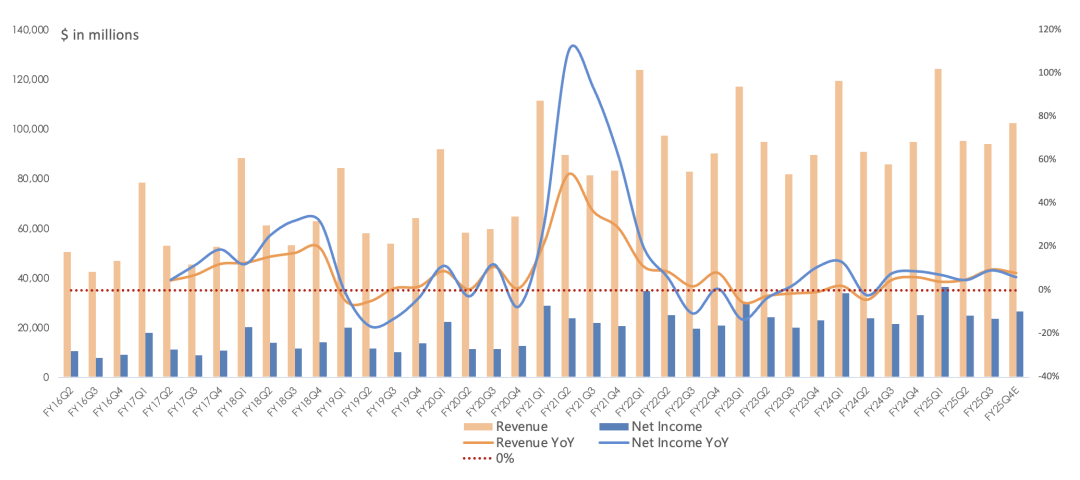

Revenue of $94B, up 10% year over year; this quarter tariffs pulled forward demand by approximately one percentage point; net income of $23.4B, up 9% year over year.

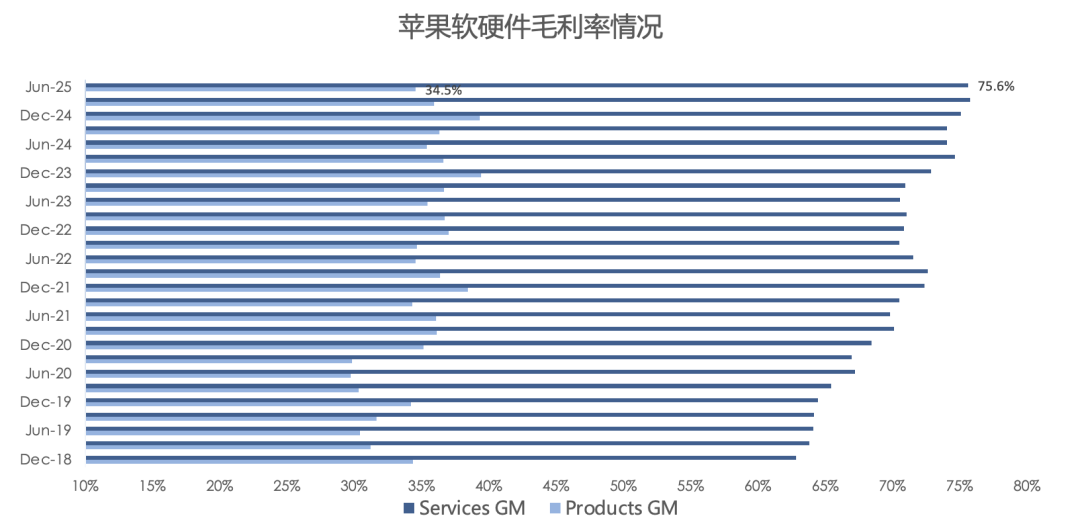

Gross margin of 46%, up 0.4 percentage points year over year; hardware gross margin of 34.5%, down 0.8 percentage points; software gross margin of 75.6%, up 1.6 percentage points.

Operating margin of 30%, up 0.4 percentage points year over year; net margin of 25%, down 0.1 percentage points.

Active installed base of all products globally reached a new all-time high (devices that have used Apple services within 90 days are considered active; FY25 Q1 was over 2.35B).

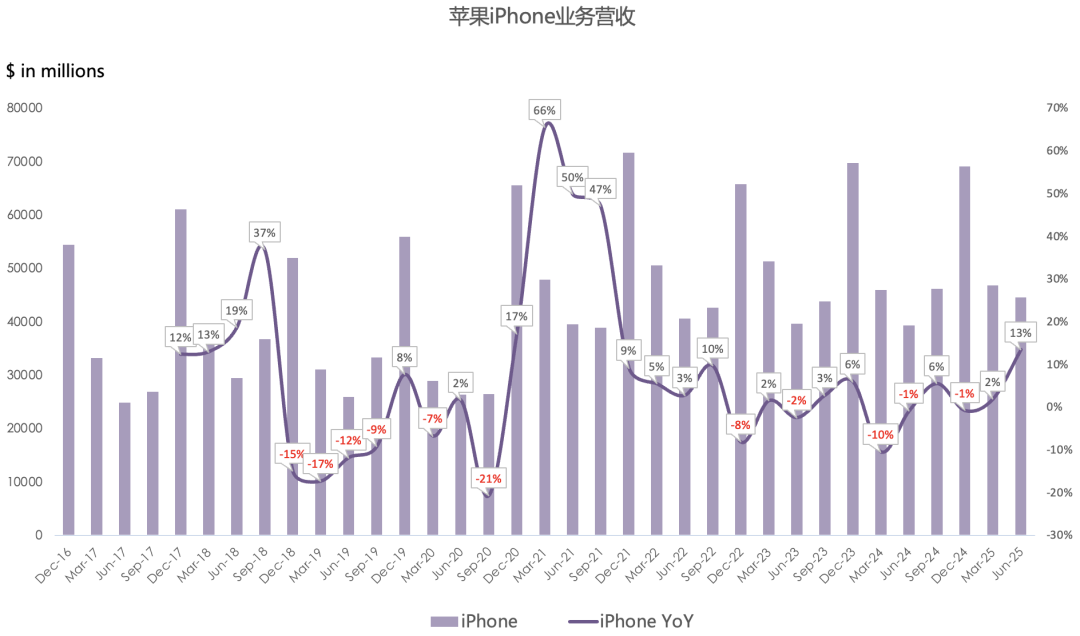

iPhone revenue of $44.6B, up 13% year over year, marking the first double-digit growth in 10 quarters (last seen in FY22 Q4); iPhone grew year over year in every geography, with emerging markets (India, Middle East, South Asia, Brazil, etc.) posting double-digit growth; the iPhone 16 series grew double digits versus the 15 series; cumulative iPhone shipments have surpassed 3 billion units since its 2007 launch.

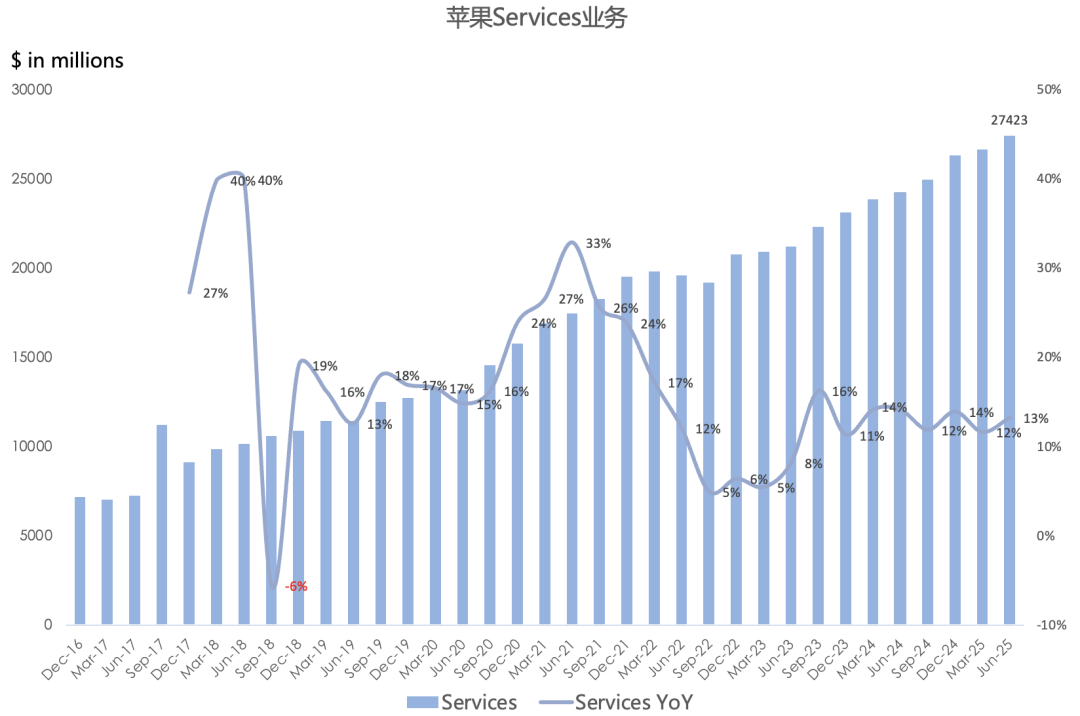

Services revenue of $27.4B, up 13% year over year, setting a record for the 11th consecutive quarter; Services transacting accounts and paid accounts both hit all-time highs, each growing double digits year over year; global paid subscriptions exceed 1 billion (unchanged for 7 quarters), with customer engagement continuing to rise; US App Store revenue grew double digits year over year to a quarterly record; most Services subcategories grew sequentially, led by cloud services revenue hitting a record, driven by year-over-year growth in iCloud paid accounts.

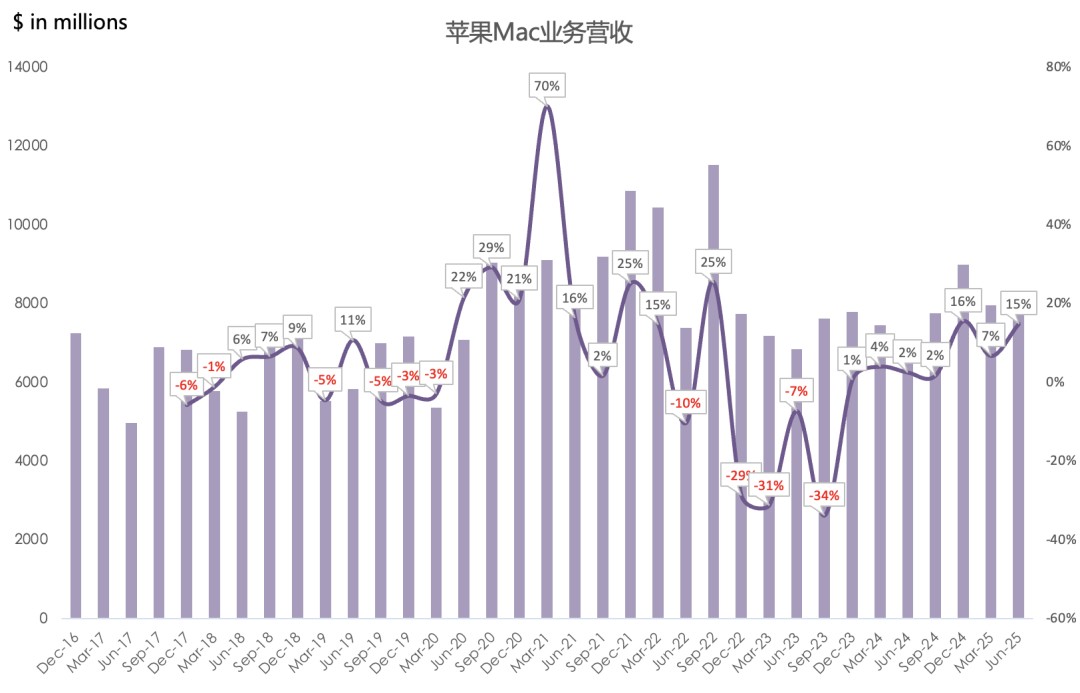

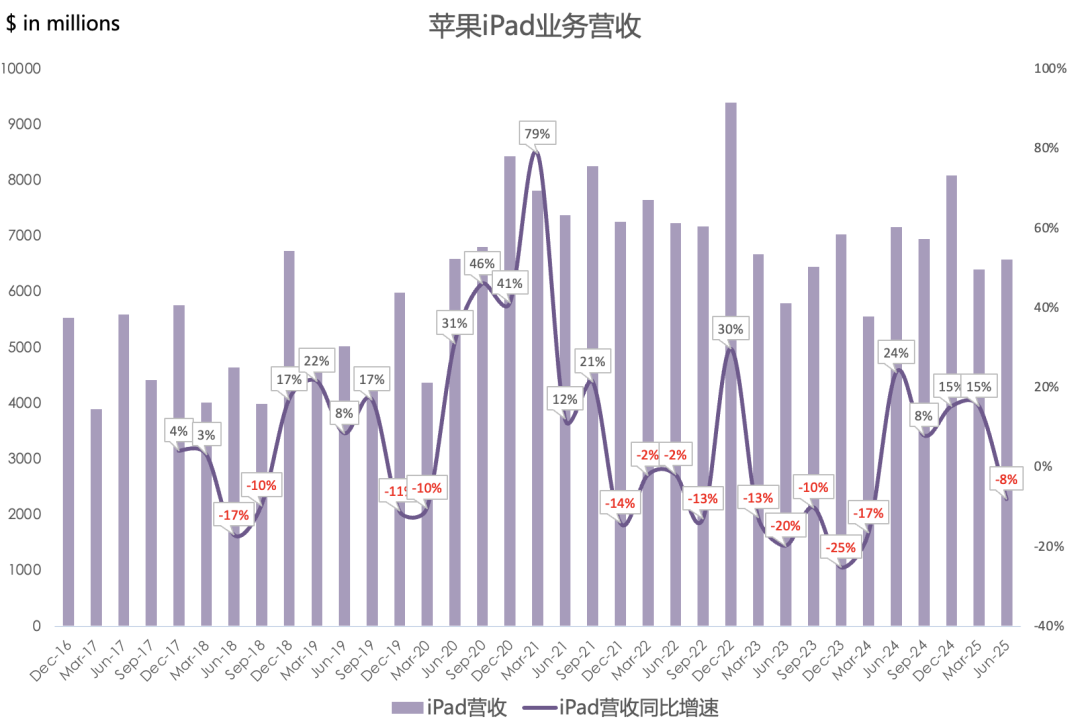

Mac revenue of $8B, up 15% year over year, driven primarily by strong demand for the M4 MacBook Air; Mac upgraders hit a quarterly record, with double-digit growth in Europe, Greater China, and the rest of Asia Pacific; iPad revenue of $6.6B, down 8% year over year.

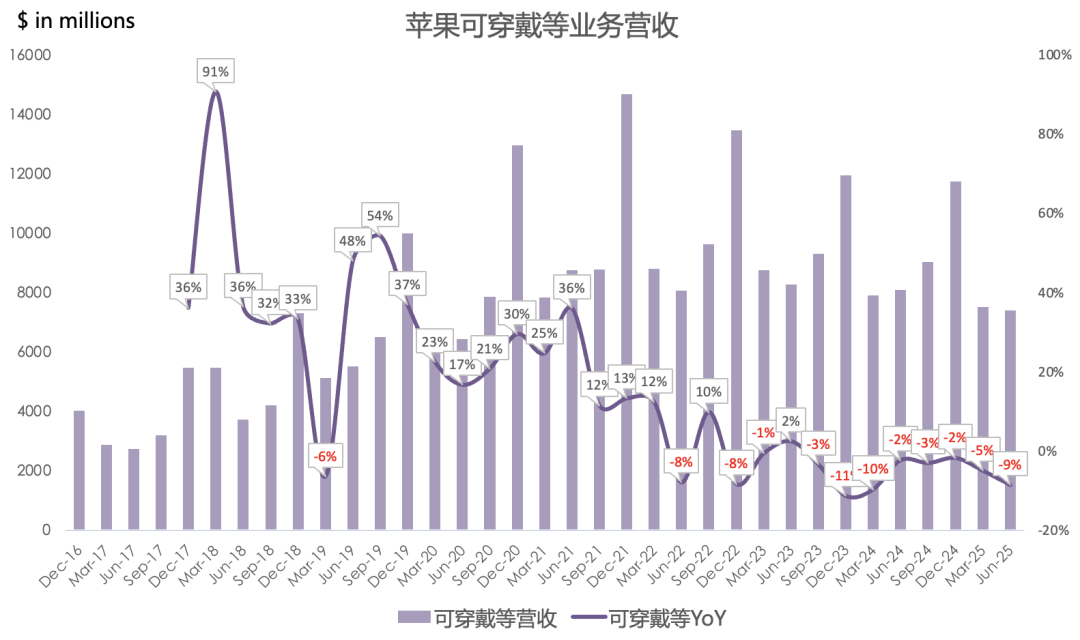

Wearables, Home and Accessories revenue of $7.4B, down 9% year over year, declining for the 8th consecutive quarter.

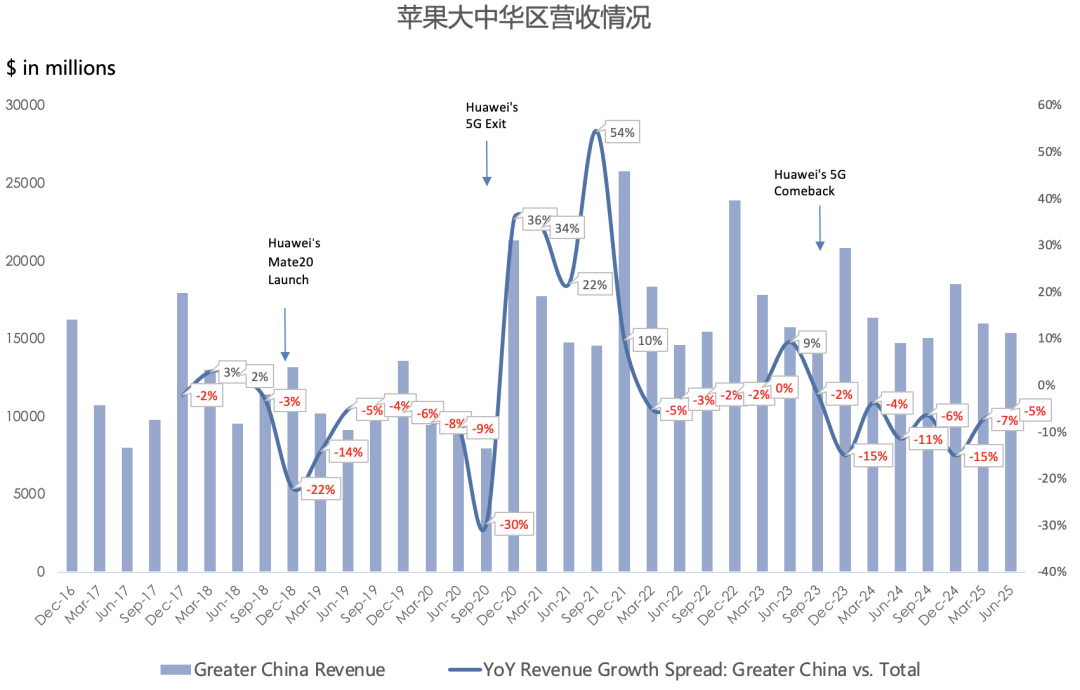

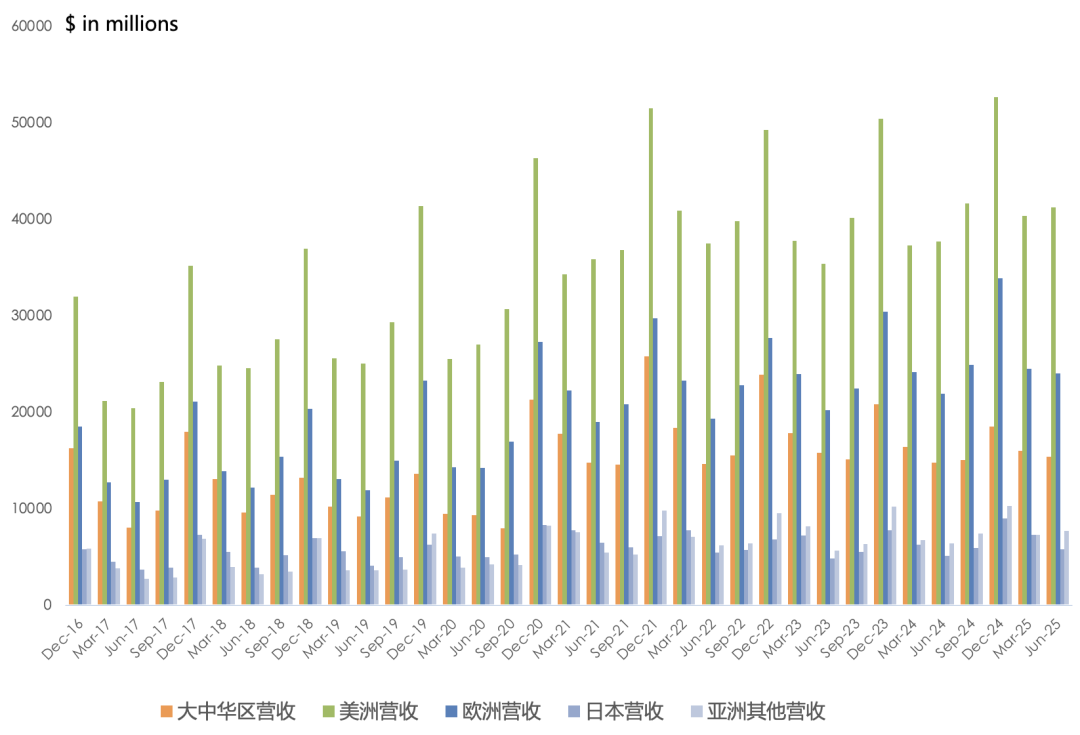

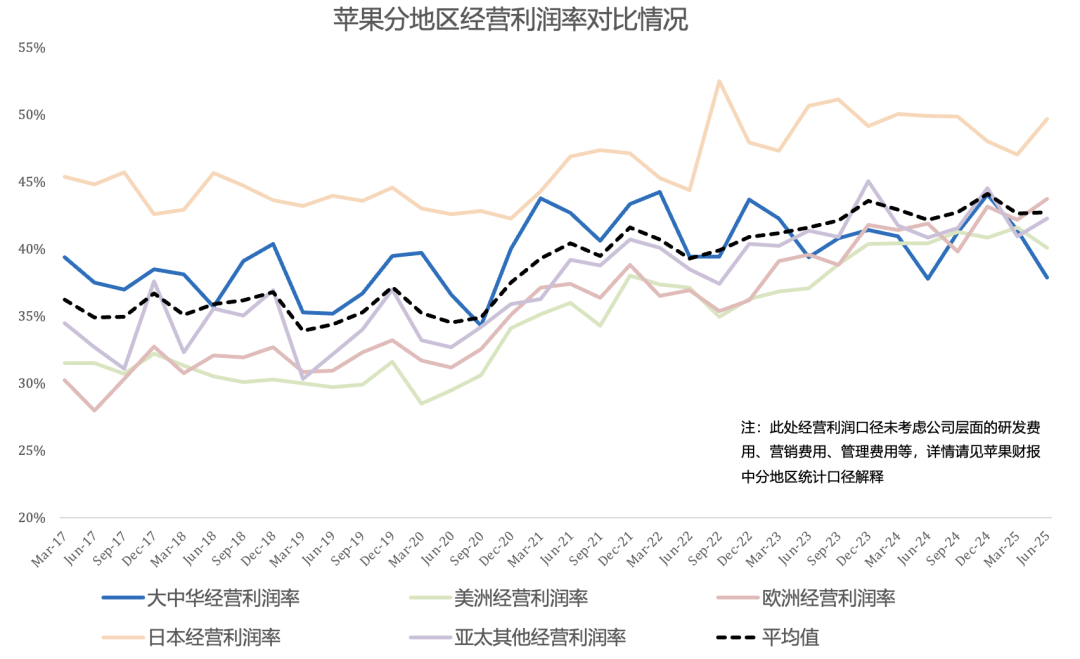

Greater China revenue of $15.4B, up 4% year over year, ending 7 consecutive quarters of year-over-year declines, but marking the 8th consecutive quarter of growth trailing the company average; Greater China growth was driven by government subsidies on select iPhone and Mac products; Greater China operating margin of 37.9% ranked last.

Apple expanded across numerous global markets: it grew in the vast majority of markets, including Greater China and many emerging markets, and set quarterly records in over 20 countries and regions (including the US, Canada, Latin America, Western Europe, the Middle East, India, and South Asia).

Assuming tariff policy and the Google agreement remain unchanged, FY25Q4 revenue is expected to grow in the mid-to-high single digits year over year. Services growth should remain at last quarter's 13%, with gross margin of 46%-47%, including $1.1B of tariff costs, and opex of $15.6B-$15.8B. This implies roughly 8% revenue growth and 7% non-GAAP net income growth; prior-year GAAP net income is not comparable because of a one-time tax item.

The company repurchased $21B of shares this quarter, a 6-quarter low, paid $3.9B in dividends, and ended with $31B in net cash.

Announced continued increases in AI investment. Data center investment will follow a hybrid strategy of self-build plus third-party.

Overall, Apple's report was characteristically uninspiring, but it beat lowered expectations by a wide margin. However, its growth rates (revenue +10% YoY, net income +9% YoY, forward P/E 26.7x) remain at the bottom among the four mega-cap peers: Microsoft (revenue +15%, net income +24%, forward P/E 35.1x), Google (revenue +14%, net income +19%, forward P/E 18.4x), and Amazon (revenue +13%, net income +35%, forward P/E 31.0x). As previously emphasized: Microsoft, Google, and Amazon all delivered solid profit results despite massive AI spending, yet the market frets over their over-investment hurting profits, while harboring outsized fantasies about Apple's AI — which currently involves far less investment. Last year's WWDC Apple Intelligence promises remain unfulfilled, and this year's WWDC brought no meaningful change.

Apple's Core Growth Formula:

AAPL=active installed base * customer engagement

Although both sides of Apple's core growth formula are still expanding, the pace is slow, and the valuation is not cheap (10-year average P/E midpoint of 22.7x). Notably, beyond hardware weakness, the software flywheel is also decelerating.