Ten charts to understand Apple's latest earnings

Apple FY2022 Q4 Earnings Summary:

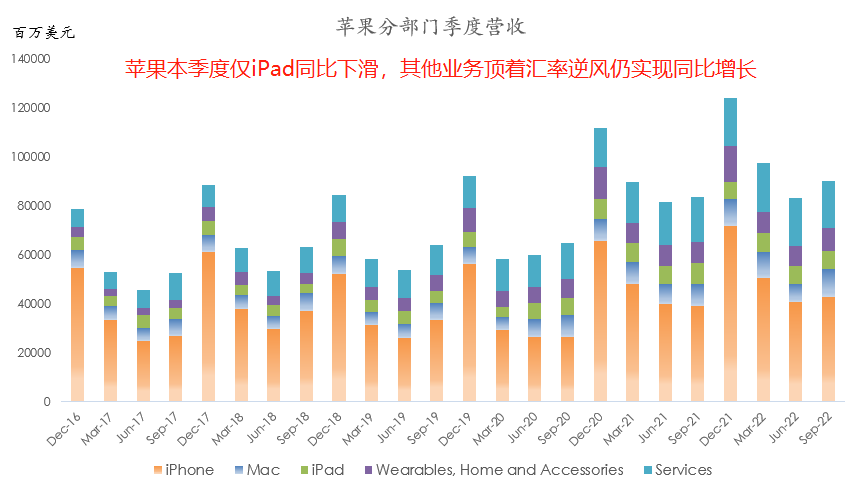

Revenue was $90.146B, up 8.1% year over year, with a 6-point FX headwind. Net income was $20.721B, up 0.8% year over year, versus a 10.6% decline last quarter.

Global active installed base of iPhone, Mac, iPad, and wearables hit new highs. Apple's strategy: installed base × customer engagement.

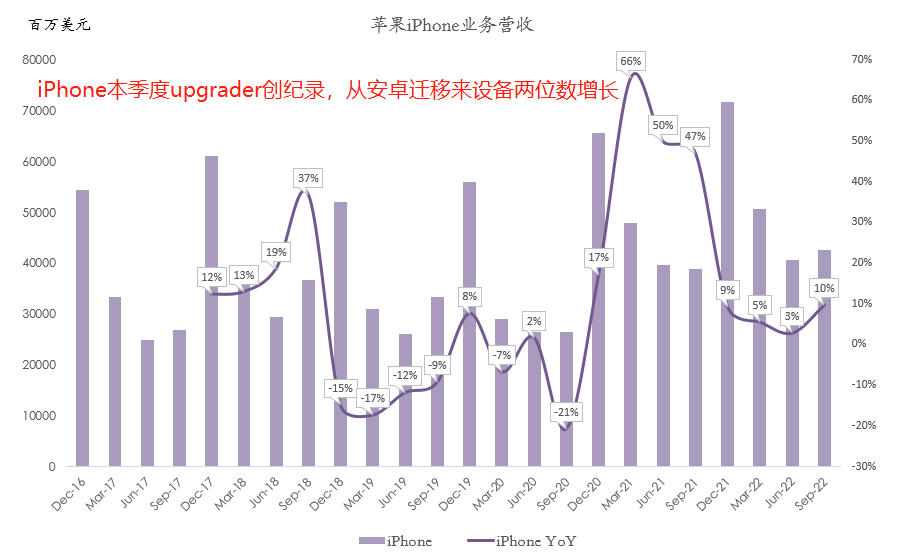

iPhone revenue was $42.626B, up 10% year over year. Quarterly iPhone upgraders hit a record; Android-to-iPhone switchers continued double-digit year-over-year growth.

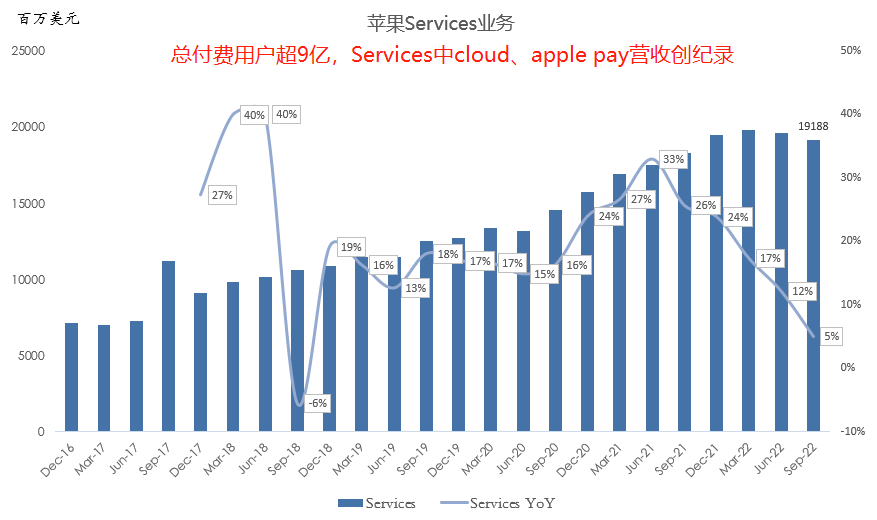

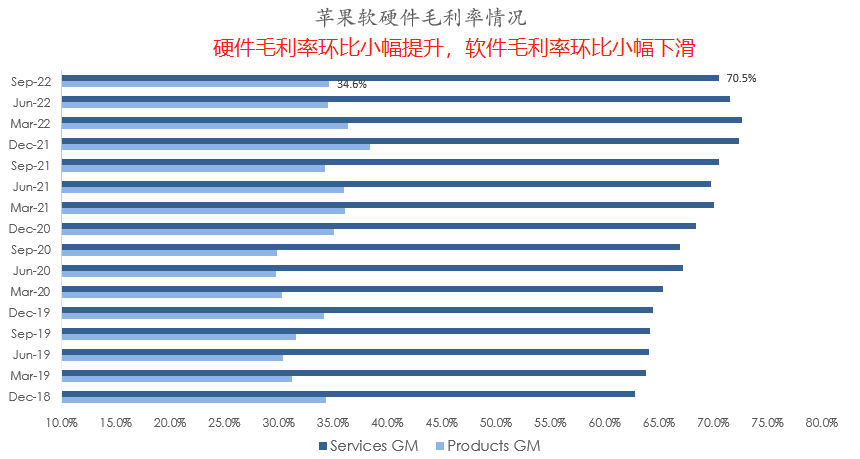

Services revenue was $19.188B, up 5% year over year, the first single-digit growth quarter in 16 quarters. Services gross margin was 70.5% this quarter. Paid subscriptions topped 900M, a new record. iCloud and Apple Pay revenue hit records, but digital advertising and gaming were weak.

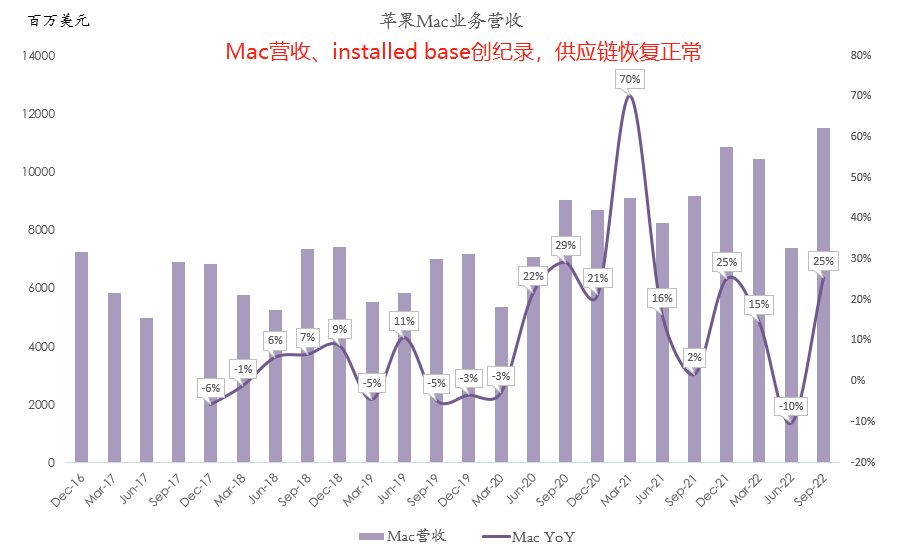

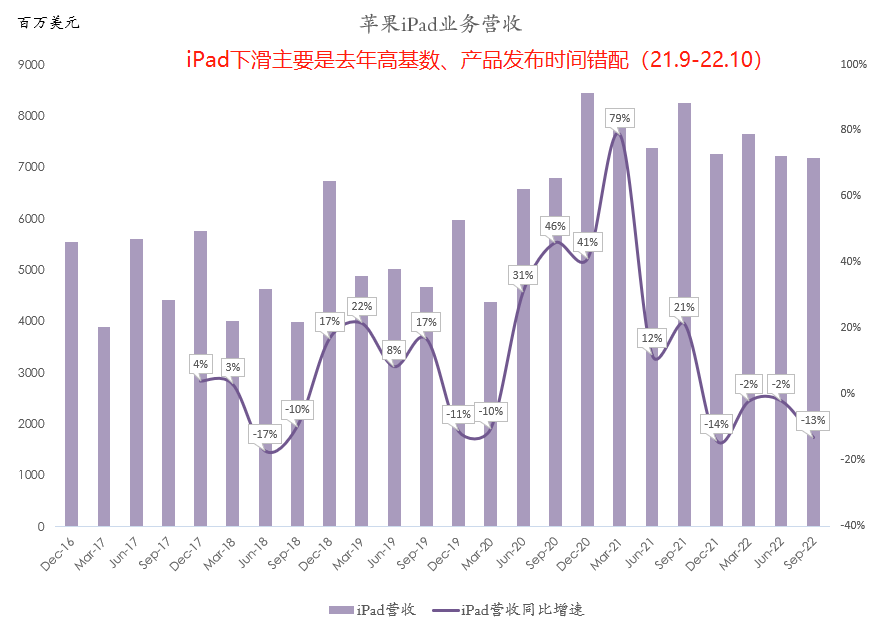

Mac revenue was $11.508B, up 25% year over year, a new record. iPad revenue was $7.174B, down 13% year over year, the fourth consecutive quarterly decline. Supply chain issues have been resolved.

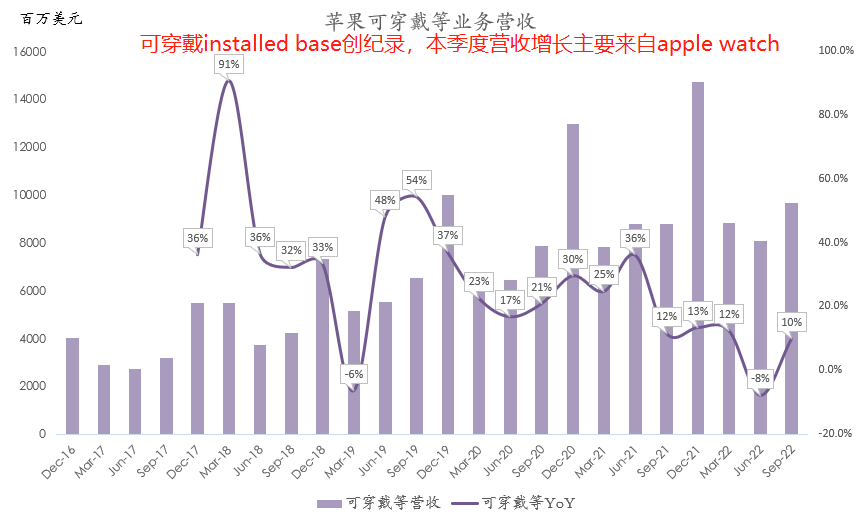

Wearables, Home and Accessories revenue was $9.65B, up 10% year over year, driven by new Apple Watch launches.

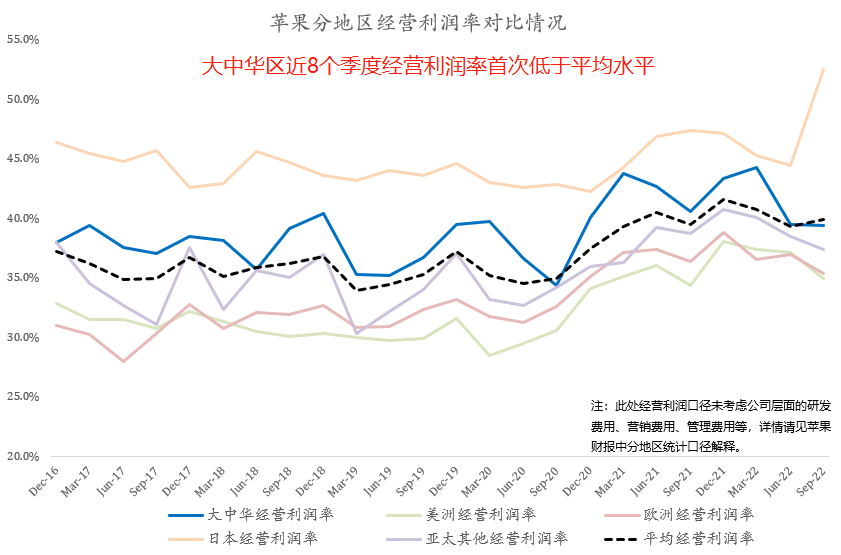

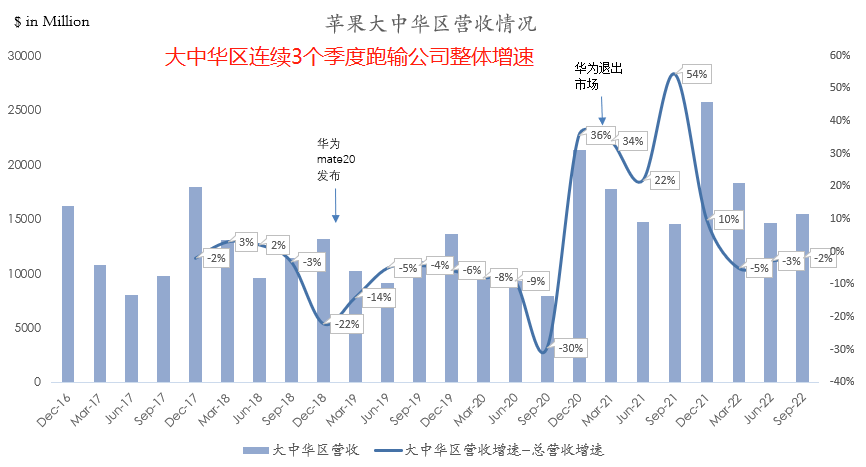

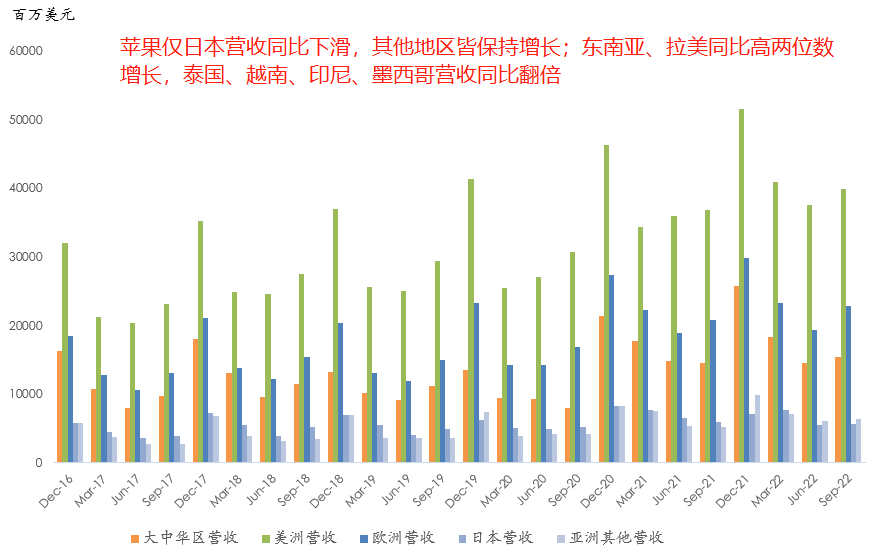

Greater China revenue was $15.47B, up 6% year over year, underperforming total Apple revenue growth for the third consecutive quarter; FX had some impact. Greater China operating margin was 39.4%, below the corporate average of 39.9%. Americas and Europe revenue grew 8% and 10% year over year respectively; Europe's resilience was surprising. Japan revenue fell 5% year over year. Rest of Asia Pacific grew 23% year over year, the second consecutive quarter of double-digit growth.

India iPhone revenue grew high double digits year over year, hitting a record. Southeast Asia and Latin America grew high double digits; Thailand, Vietnam, Indonesia, and Mexico revenue nearly doubled. Enterprise wins included Ford and Cisco.

Apple guided for Q1 revenue growth to decelerate, with a 10-point FX headwind. Services revenue is expected to grow year over year; Mac growth will decelerate sharply due to a tough compare (M1 MacBook Pro). Consolidated gross margin is guided at 42.5%-43.5%, with a 3.3-point FX impact.

On the closely watched advertising business, Apple said the current scale is not material and it will not disclose figures for now.

Overall, this earnings report maintained Apple's leadership posture, weathering FX headwinds. Apple repurchased $24.4B this quarter, the second consecutive quarter where buybacks exceeded net income. Fiscal year-to-date buybacks exceed $89.4B, a new record.

iPhone held up relatively well amid the economic slowdown, while emerging markets' strong performance offers future upside. Services, however, faces the same growth deceleration as the cloud hyperscalers. The installed base × customer engagement formula has a massive left-hand side; Apple must keep pushing the right-hand side.