Ten charts to understand Apple's latest earnings

Apple FY2023 Q3 Earnings Summary:

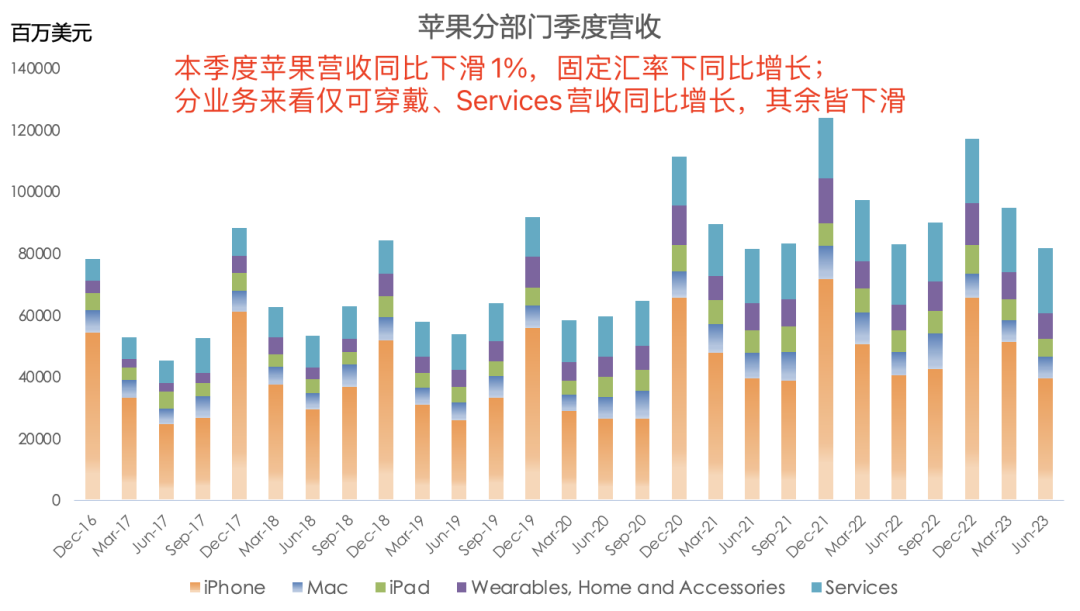

Revenue was $81.797B, down 1.4% year over year, the first time since 2016 with three consecutive quarterly declines; FX impact was 4 points, and on a constant-currency basis revenue grew year over year; net income was $19.881B, up 2.3% year over year, ending two consecutive quarterly declines.

Global active iPhone installed base hit a new high (other devices not mentioned this quarter), with over 2B total active devices, of which iPhone exceeds 1B.

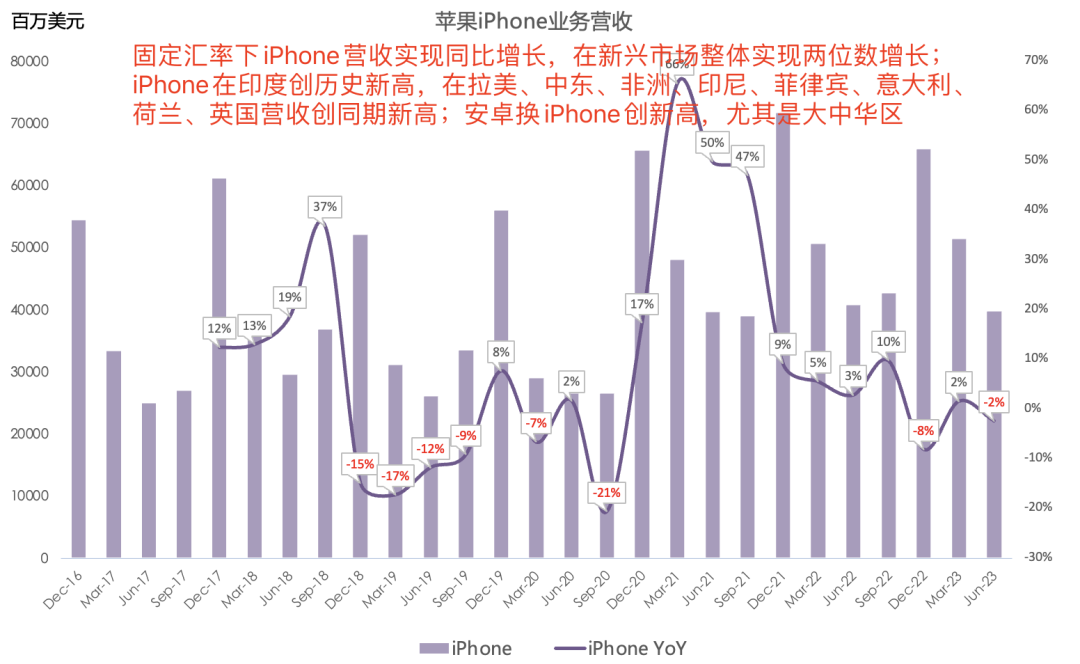

iPhone revenue was $39.7B, down 2% year over year, with emerging markets overall posting double-digit growth; iPhone revenue hit all-time highs in India, and period highs in Latin America, Middle East, Africa, Indonesia, Philippines, Italy, Netherlands, and UK; Android-to-iPhone switching hit a new high, especially in Greater China; over 50% of global iPhone purchases used installment or trade-in programs.

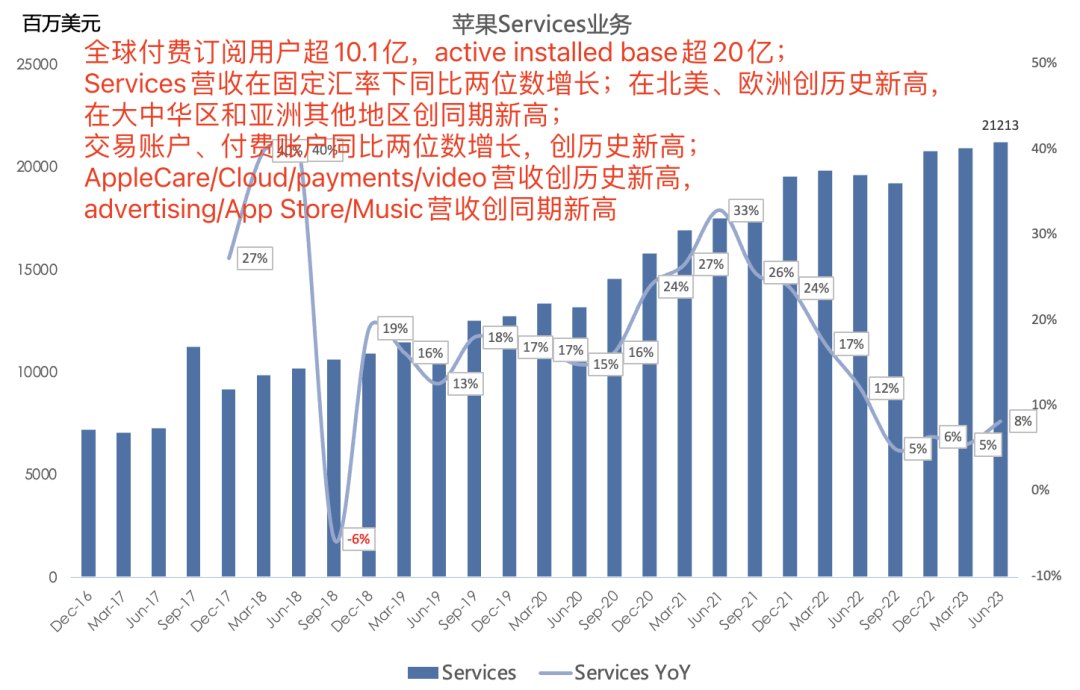

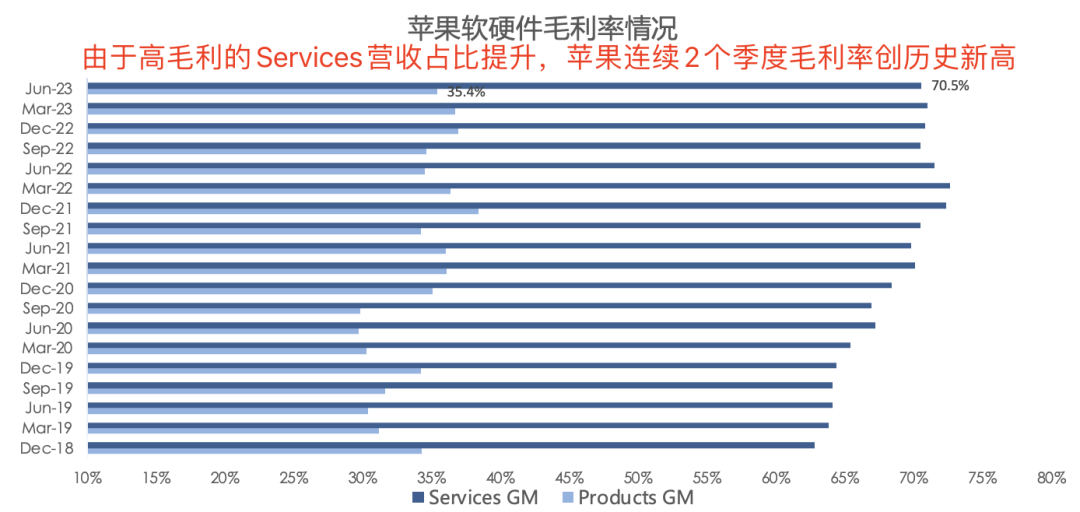

Services revenue was $21.2B, up 8% year over year, a new all-time high, with double-digit growth on a constant-currency basis; services gross margin was 71% this quarter; paid subscriptions exceeded 1.01B, a new all-time high; North America and Europe hit all-time highs, Greater China and rest of Asia hit period highs; transacting accounts and paid accounts both grew double-digits year over year to all-time highs; AppleCare, Cloud, Payments, and Video revenue hit all-time highs; Advertising, App Store, and Music revenue hit period highs; the online Apple Store launched in Vietnam this quarter; Apple's savings-account-like product reached $10B in deposits.

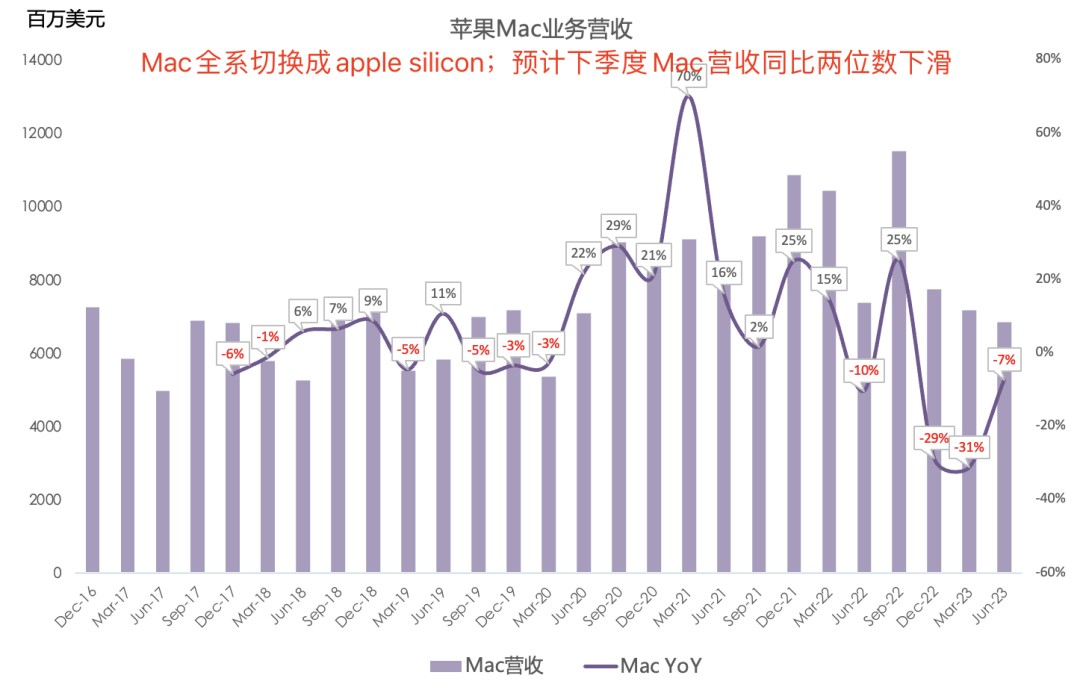

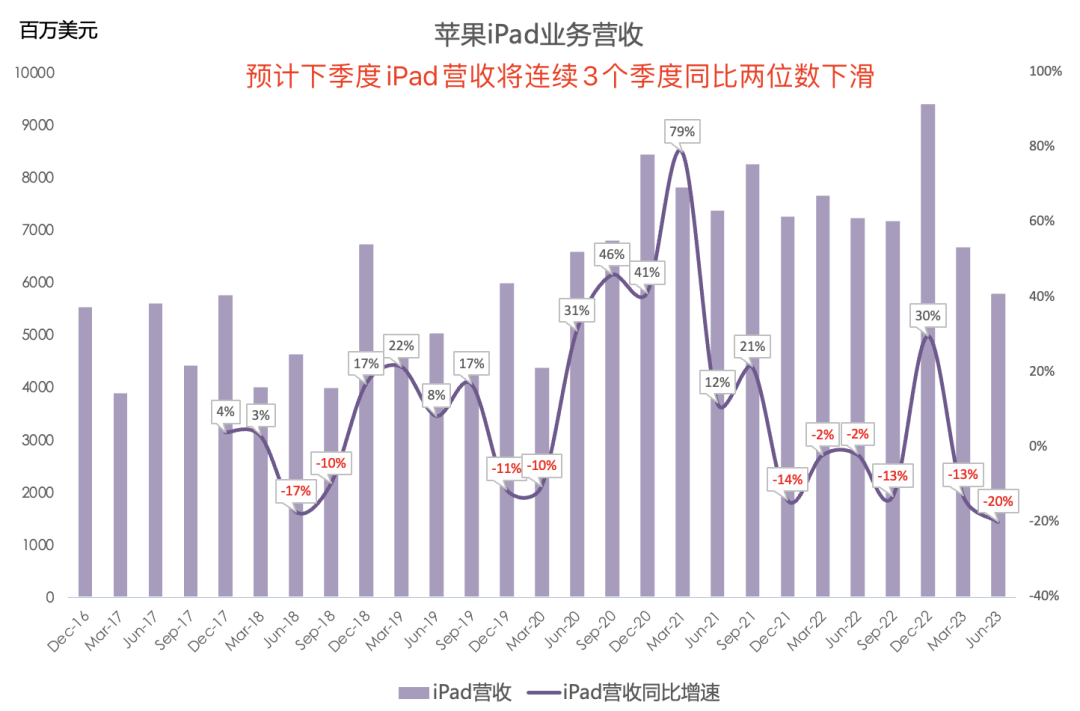

Mac revenue was $6.8B, down 7% year over year, with the full Mac lineup now on Apple silicon; iPad revenue was $5.8B, down 20% year over year on weak demand; Q4 Mac/iPad revenue expected to decline double-digits year over year, with Mac worse.

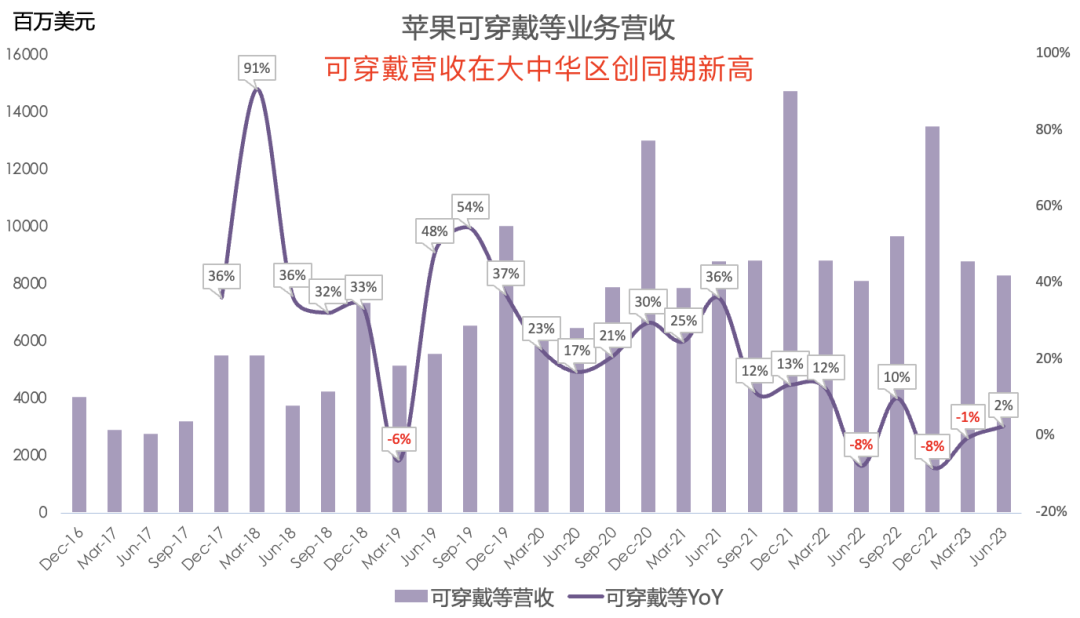

Wearables, Home and Accessories revenue was $8.3B, up 2% year over year; wearables revenue hit a period high in Greater China.

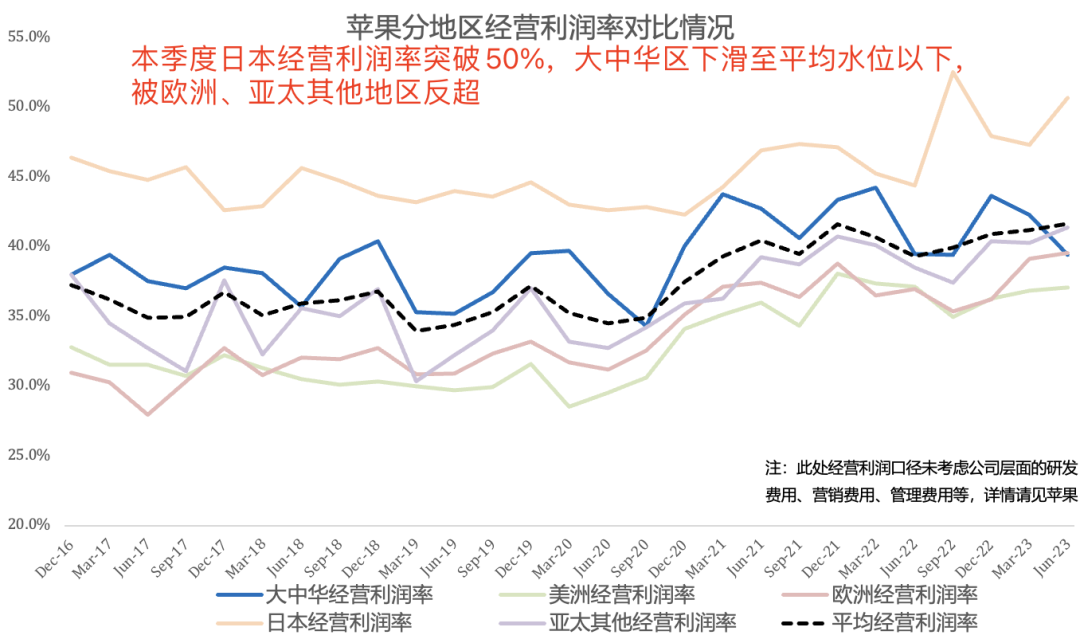

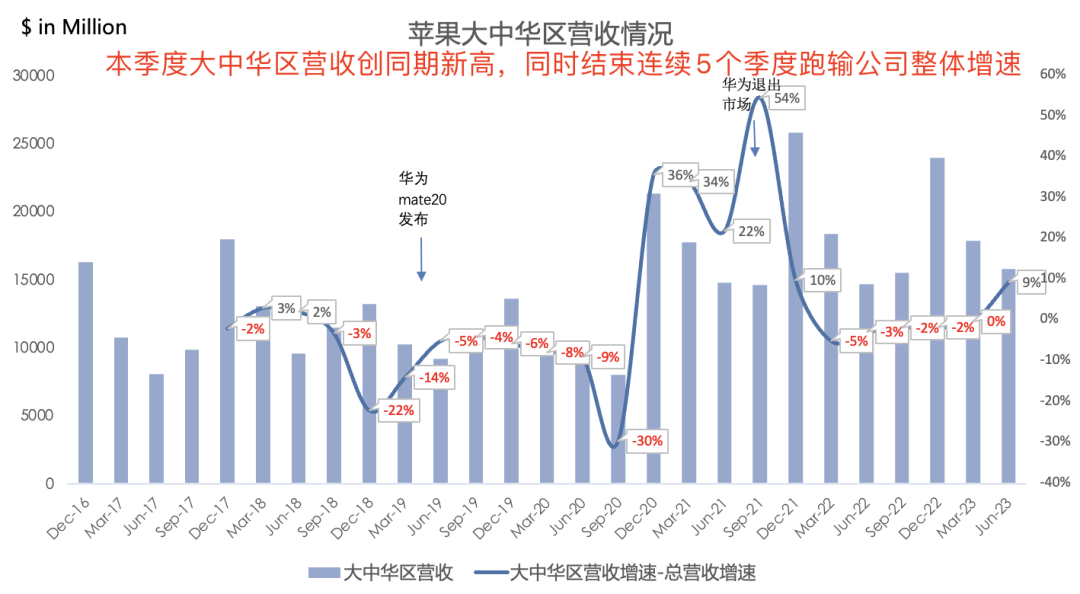

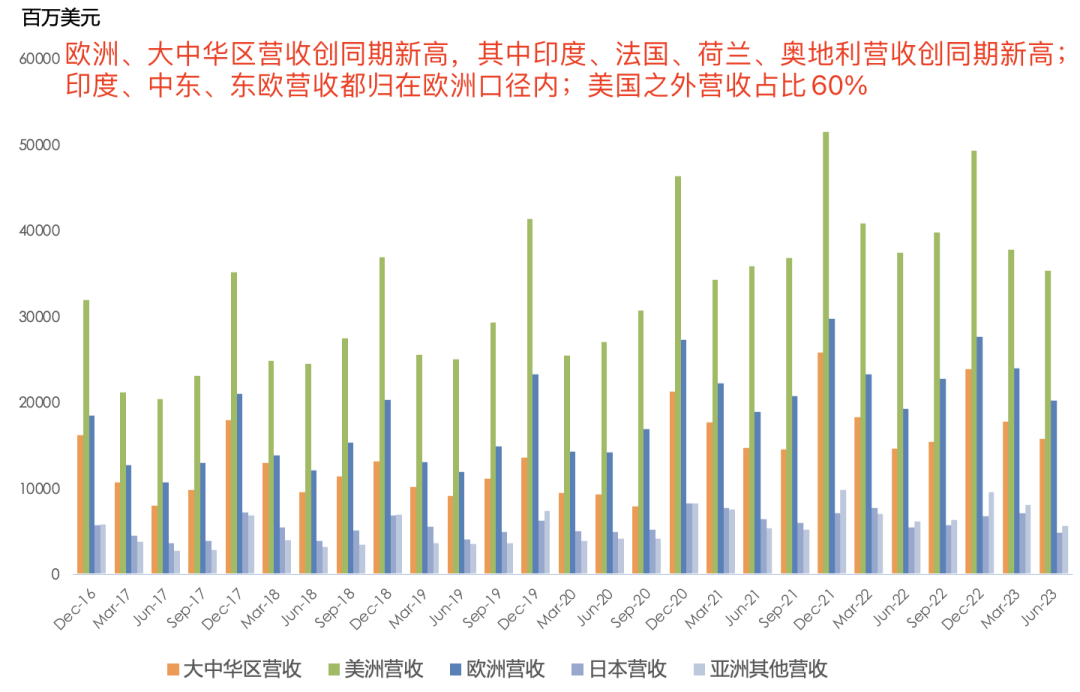

Greater China revenue was $15.8B, up 8% year over year, ending five consecutive quarters of underperforming Apple's total revenue growth; Greater China operating margin was 39.4%, down both year over year and sequentially; only Greater China and Europe grew year over year this quarter, both hitting period highs; Apple noted for the first time that India, Middle East, and Eastern Europe revenue are included in the Europe segment.

Apple continues to expand in emerging markets, with period revenue highs in India, France, Netherlands, and Austria; iPhone grew double-digits overall in emerging markets; this quarter enterprise services won large deals with Blackstone and Gilead—Blackstone equipping all employees with iPhone and M2 MacBook Air, Gilead equipping sales teams with iPad and MacBook Air.

Q4 revenue growth expected to be consistent with Q3 (down 1% year over year), with 2 points of FX headwind; iPhone and services revenue growth expected to improve versus Q3; gross margin 44–45%, on track for a third consecutive quarterly record; $18B in buybacks and $3.8B in dividends this quarter.

Apple's delayed Q3 earnings release date relative to tradition led the market to expect weak results; TSMC and Qualcomm earnings were also soft, lowering expectations for Apple.

Overall this earnings was mediocre; among the four mega-caps it cannot compare with Microsoft, Google, or Amazon. Emerging markets are still growing but growth is visibly decelerating; no more regions with doubling revenue; active installed base records are now limited to iPhone, whereas previously iPhone, Mac, iPad, and wearables all hit records for at least four straight quarters.

Apple's core growth formula: AAPL = active installed base × customer engagement (active installed base 2B+ × paid subscriptions 1.01B+).

The left-side variable of Apple's core growth formula has begun to loosen near-term, but the flywheel model remains sound long-term; near-term hardware revenue volatility weighs on revenue growth, while rising software mix boosts profit growth, so Apple's profit growth will likely outpace revenue growth for the for the foreseeable future; combined with massive ongoing buybacks, the software mix shift amplifies EPS growth.

On hardware, long-term bull case: Vision Pro is a call option that could open another sizable revenue line like wearables did.