Ten charts to understand Apple's latest earnings

Apple FY2023 Q1 Earnings Summary:

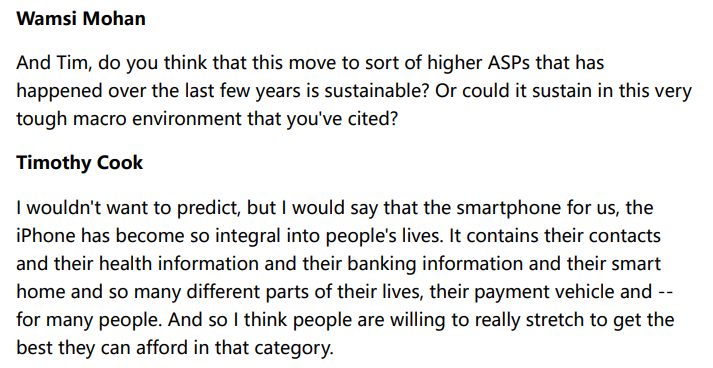

Revenue $117.154B, down 5.5% year over year, first decline since 2019; FX impact 8 points, constant-currency revenue grew year over year; net income $29.998B, down 13.4% year over year.

Global active installed base of iPhone, Mac, iPad, and wearables hit a new high, surpassing 2B devices.

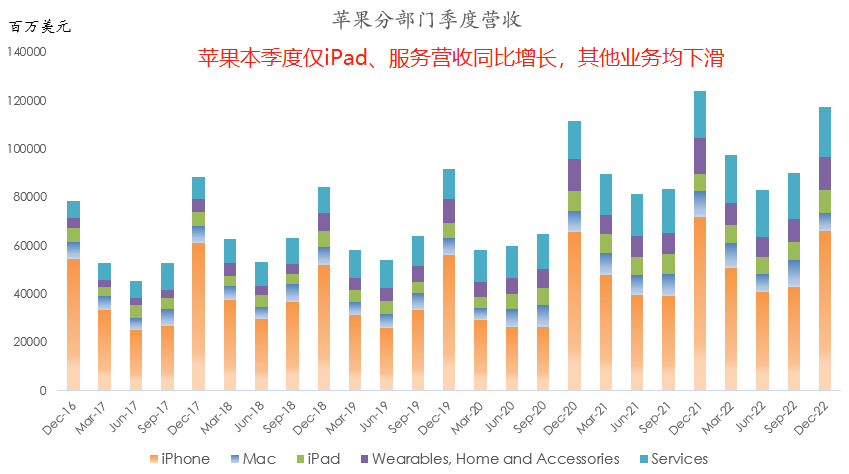

iPhone revenue $65.8B, down 8% year over year, flat year over year on constant currency. November COVID disruptions constrained iPhone 14 Pro/Pro Max supply through late December; but Canada, Italy, Spain, India, Vietnam iPhone revenue hit records; India and Mexico upgrades hit records.

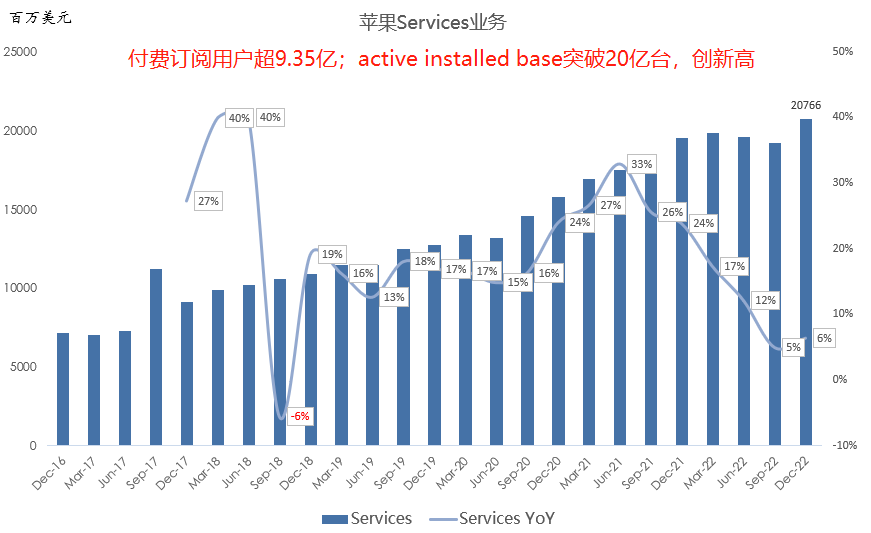

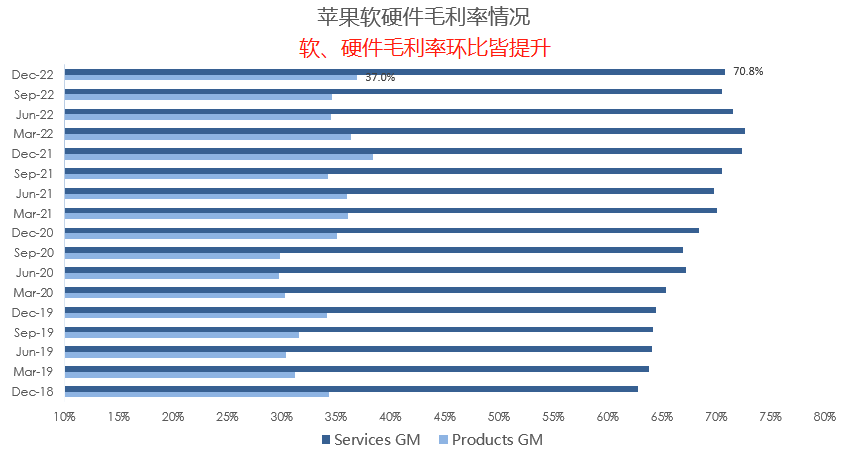

Services revenue $20.8B, up 6% year over year, double-digit growth on constant currency; services gross margin 70.8% this quarter. Paid subscriptions >935M, up double digits year over year, a new high. Apple Music, iCloud, Apple Pay revenue hit records; App Store and AppleCare revenue hit quarterly records; digital advertising and gaming weak. Services hit records in Americas, Europe, Rest of Asia Pacific; Greater China hit quarterly record.

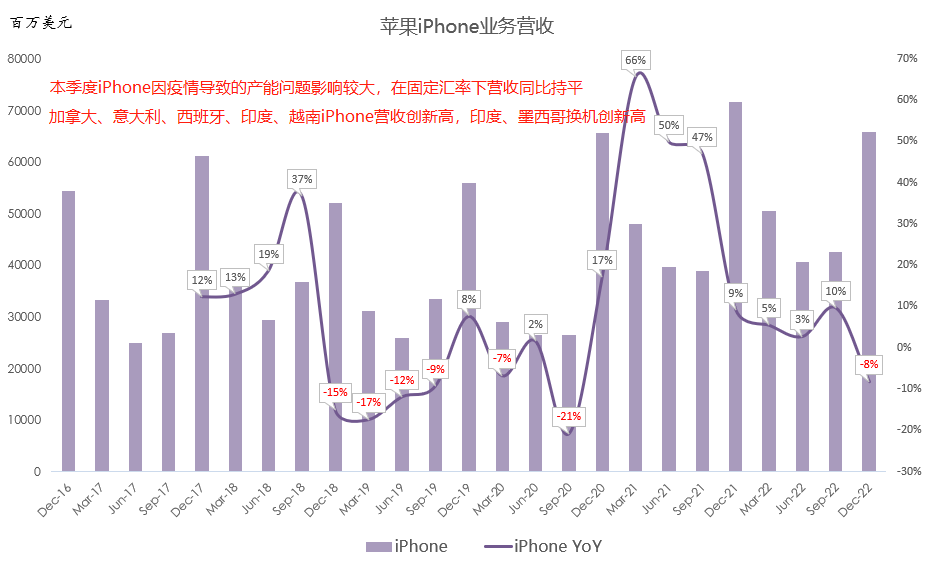

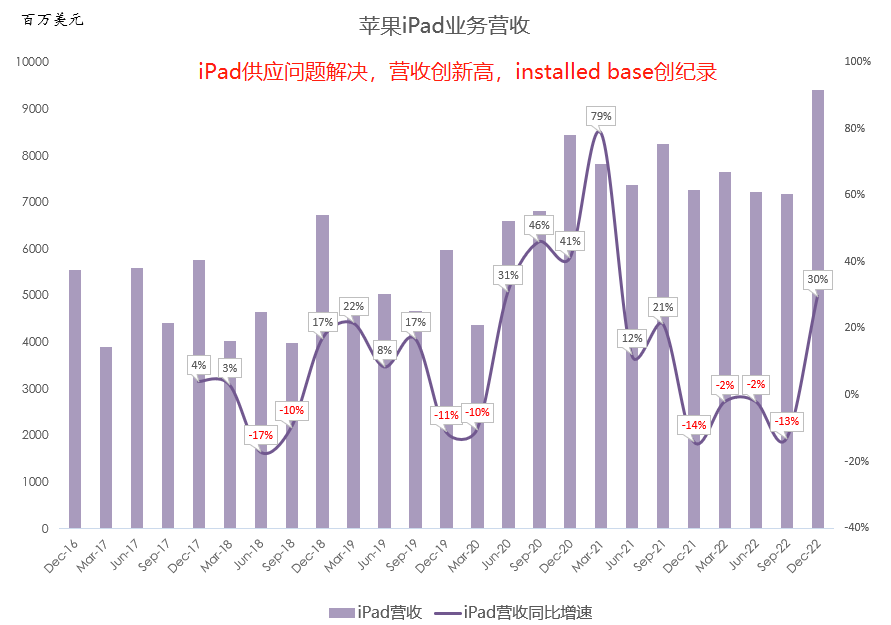

Mac revenue $7.7B, down 29% year over year; iPad revenue $9.4B, up 30% year over year, a record high, mainly due to resolution of prior capacity constraints.

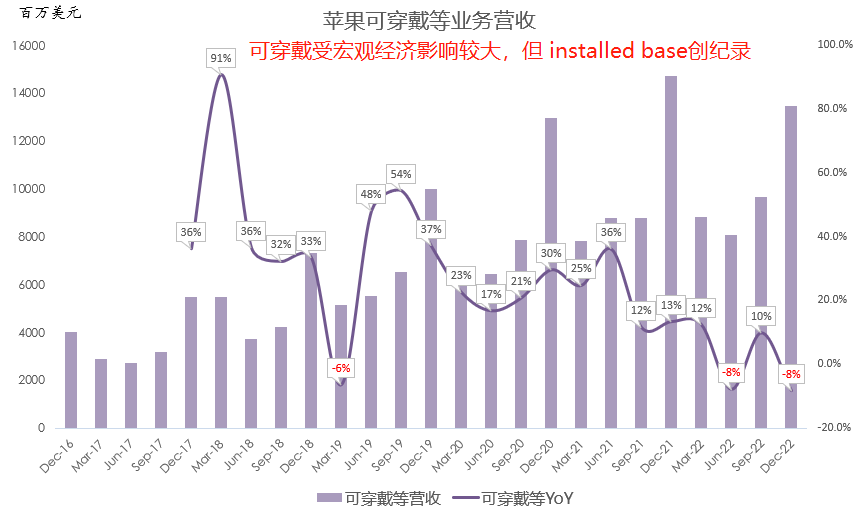

Wearables, Home and Accessories revenue $13.5B, down 8% year over year; Apple continues to cite macro weakness as a significant demand headwind for this business.

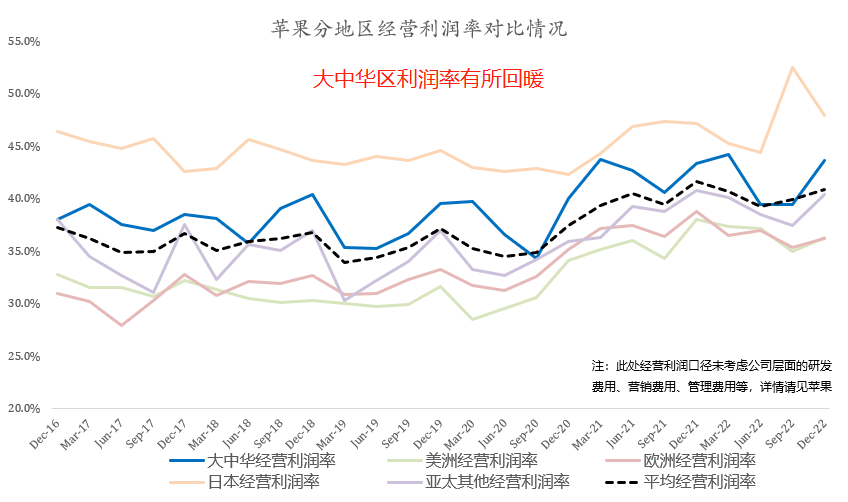

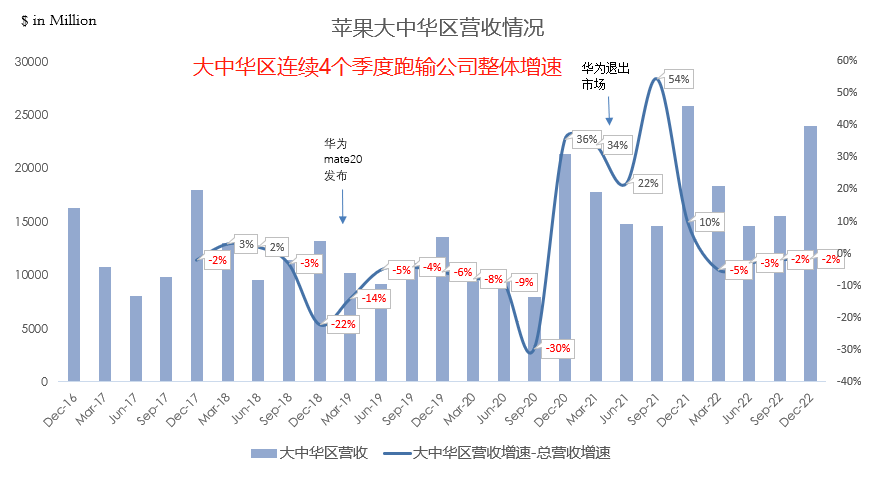

Greater China revenue $23.9B, down 7% year over year, underperforming total Apple revenue growth for the fourth consecutive quarter; Greater China operating margin 43.7%, improved both year over year and sequentially. Americas, Europe, Japan, and Rest of Asia Pacific all declined, with Americas, Japan, and Rest of Asia Pacific outperforming the company overall.

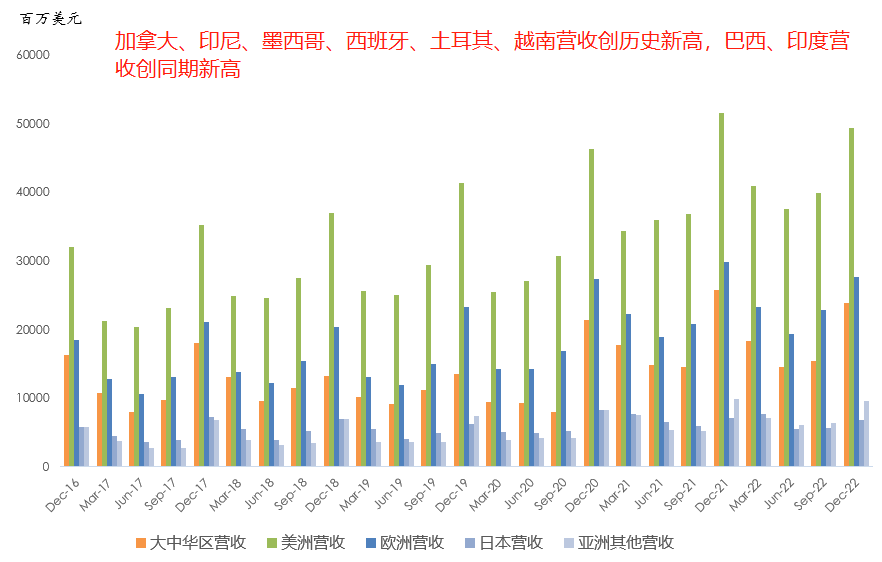

Apple is accelerating its push in emerging markets; Canada, Indonesia, Mexico, Spain, Turkey, Vietnam hit records; Brazil, India hit quarterly records. Cook remains bullish on India. Apple's current enterprise offerings include Apple Business Essentials, AppleCare, Tap to Pay, Apple Financial Services.

Apple said macro weakness impacts Mac and wearables most, iPhone least. Guides Q2 revenue growth in line with Q1, FX impact 5 points; services revenue expected up year over year, iPhone year-over-year growth to improve, Mac and iPad double-digit year-over-year declines; gross margin 43.5%-44.5%.

Overall, Apple's earnings were decent; iPhone held up relatively well in a weak macro, with the revenue decline mainly supply-driven, not demand-driven. Our long-emphasized emerging-market thesis is gradually converting to revenue; we believe emerging markets will inevitably undergo consumption upgrade, and Cook is very bullish on India.

Recap the Apple formula: AAPL = installed base × customer engagement. Both core metrics keep growing (active installed base 2B+ × paid subscribers 935M+).