Ten charts to understand Apple's latest earnings

Apple FY2024 Q1 earnings summary:

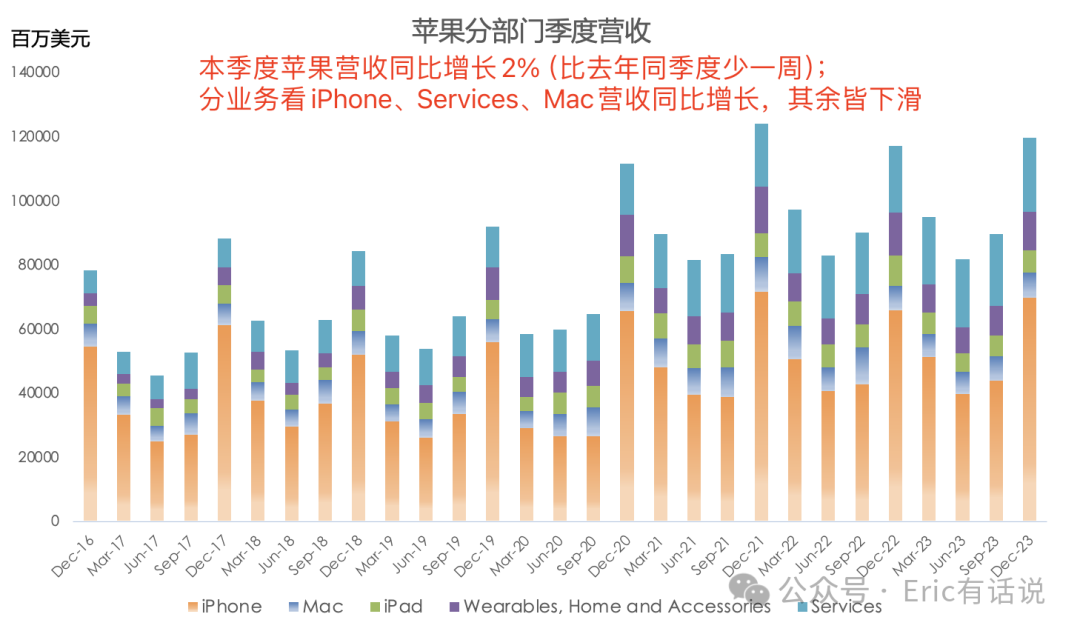

Revenue was $119.575B, up 2.1% year over year, ending four consecutive quarters of decline; this quarter had one fewer week than the year-ago period; net income was $33.916B, up 13.1% year over year, marking the second consecutive quarter of double-digit year-over-year growth; EPS up 16% year over year, a record high.

Active devices across all products and regions globally reached a record high, exceeding 2.2B (devices that have used Apple services within 90 days are considered active).

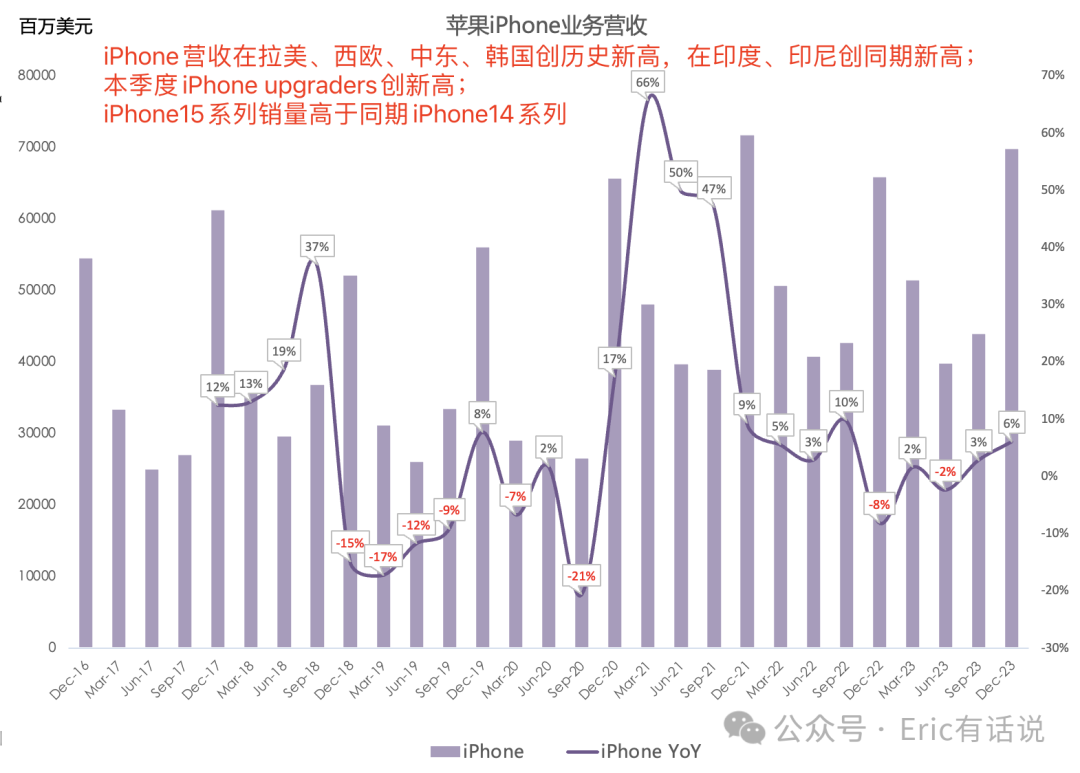

iPhone revenue was $69.7B, up 6% year over year; record highs in Latin America, Western Europe, Middle East, and Korea; period records in India and Indonesia; iPhone upgraders hit a record this quarter; iPhone 15 series sell-through exceeded the iPhone 14 series in the comparable period.

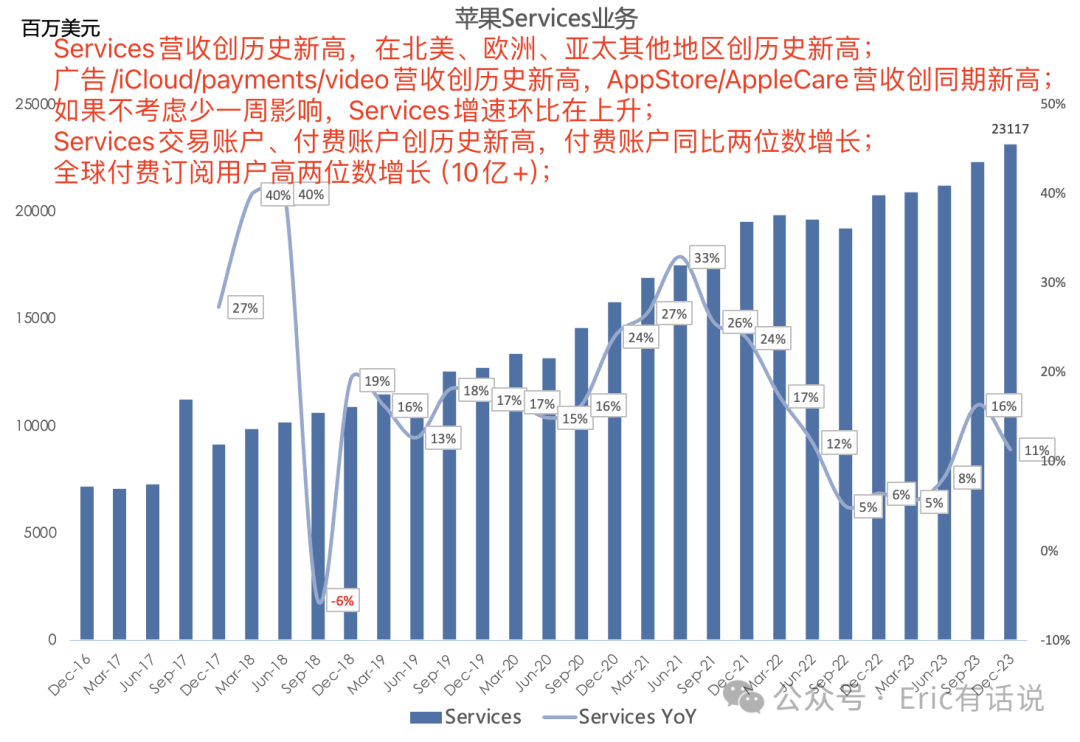

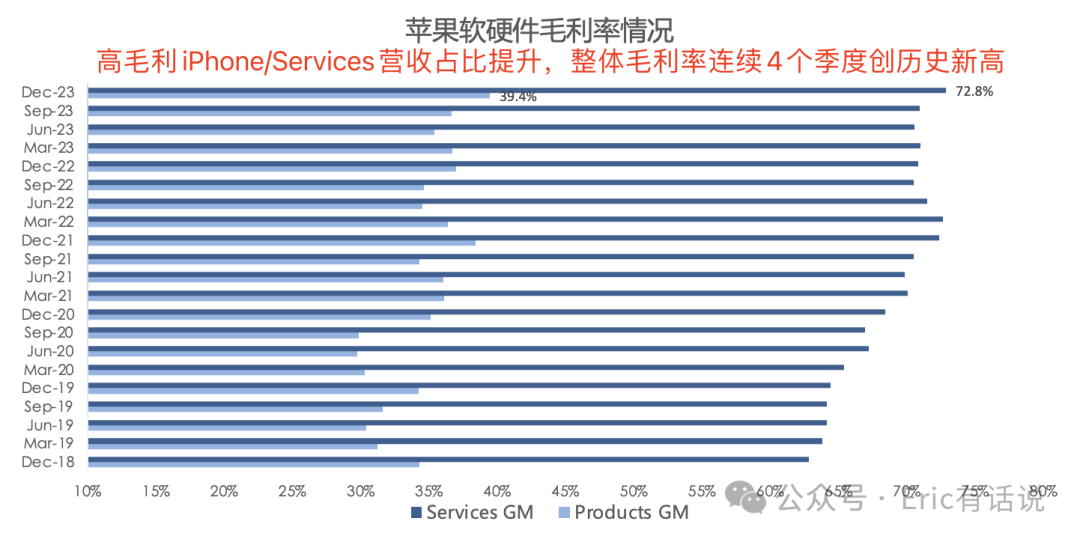

Services revenue was $23.1B, up 11% year over year, a record for the fifth consecutive quarter; records in North America, Europe, and Asia Pacific ex-China; Services gross margin was 73% this quarter. Services transacting accounts and paid accounts hit records; paid accounts grew double digits year over year; global paid subscriptions grew high double digits, exceeding 1B.

Advertising, iCloud, payments, and video revenue hit records; App Store and AppleCare revenue hit period records; excluding the one-week impact, Services growth accelerated sequentially; Apple TV+ has garnered nearly 2,050 nominations and won 450 major awards over four years.

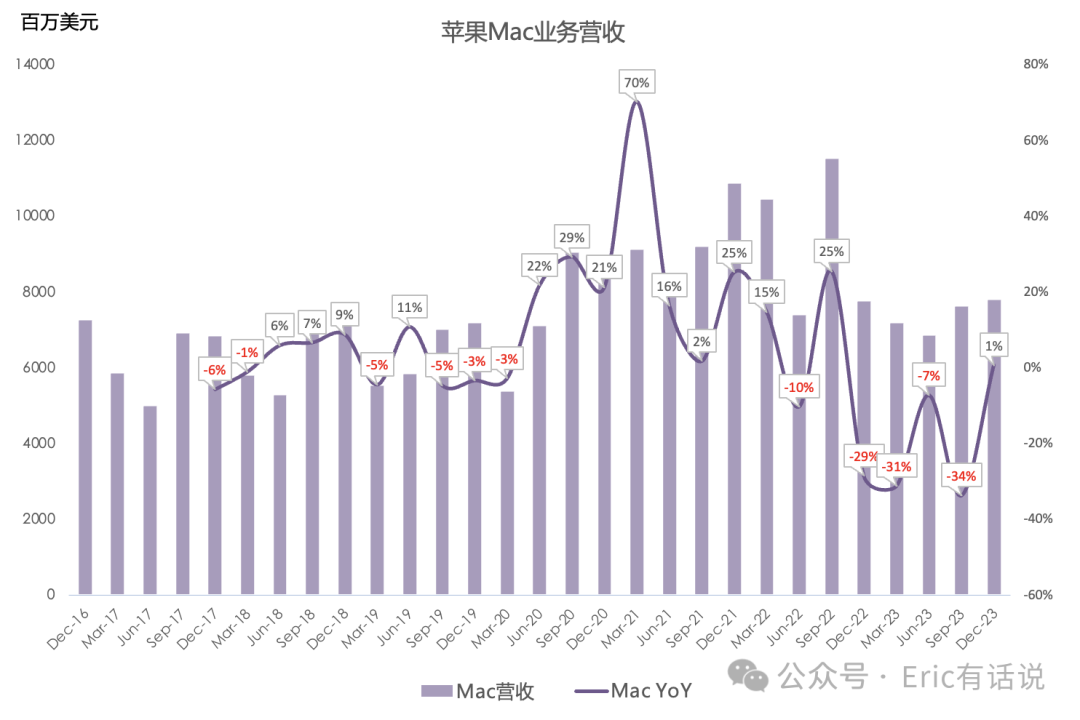

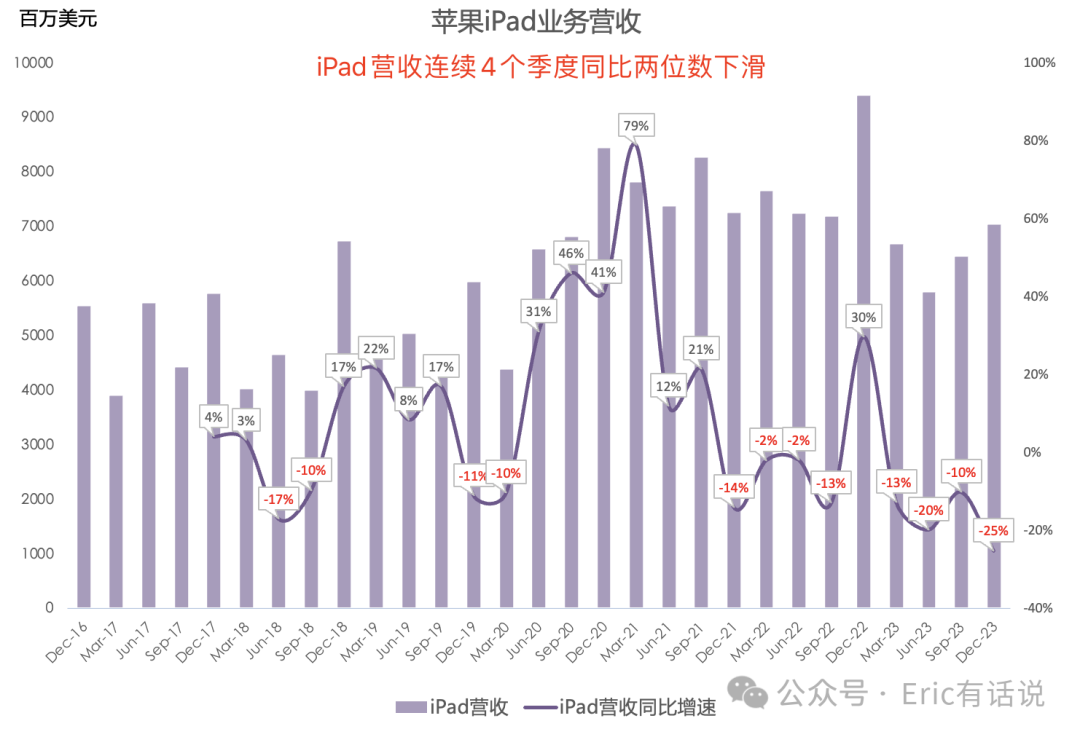

Mac revenue was $7.8B, up 1% year over year; iPad revenue was $7.0B, down 25% year over year, the fourth consecutive quarter of double-digit year-over-year declines.

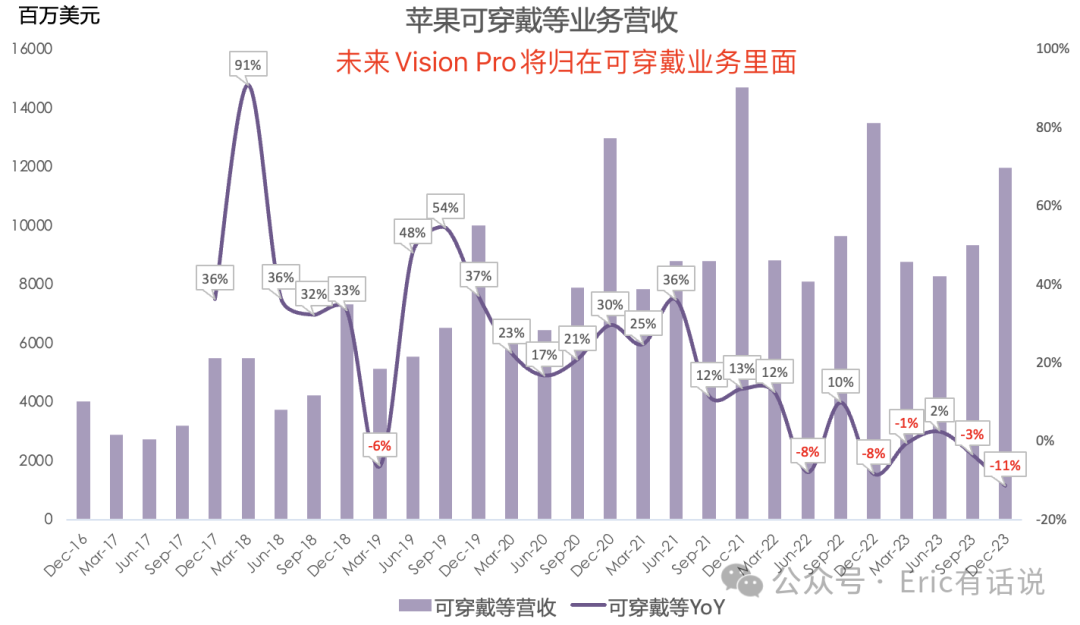

Wearables, Home and Accessories revenue was $12.0B, down 11% year over year; Vision Pro will be included in this segment going forward.

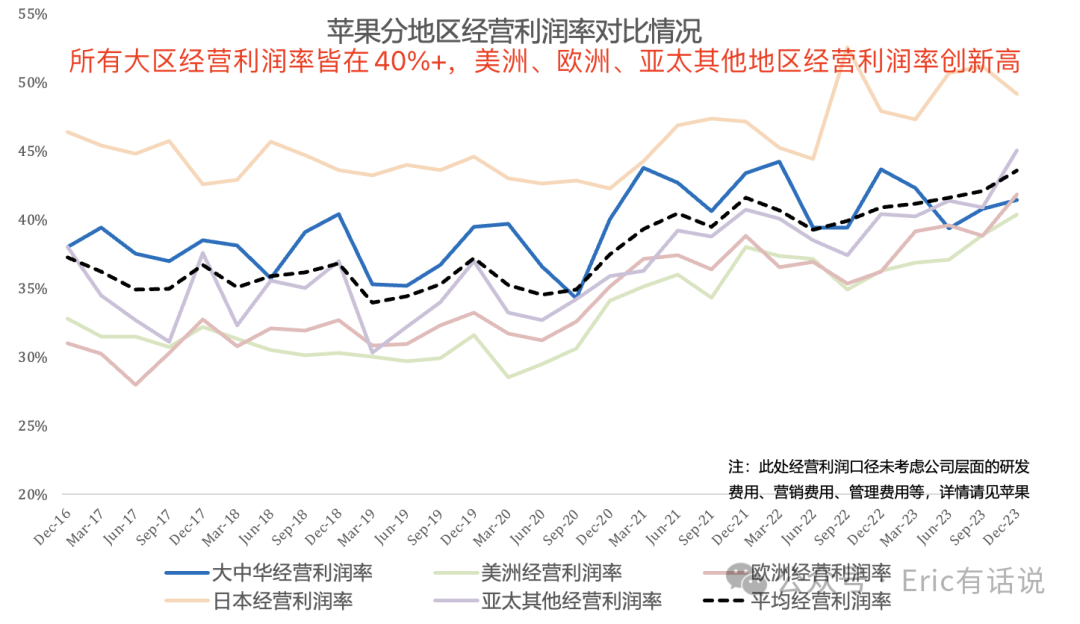

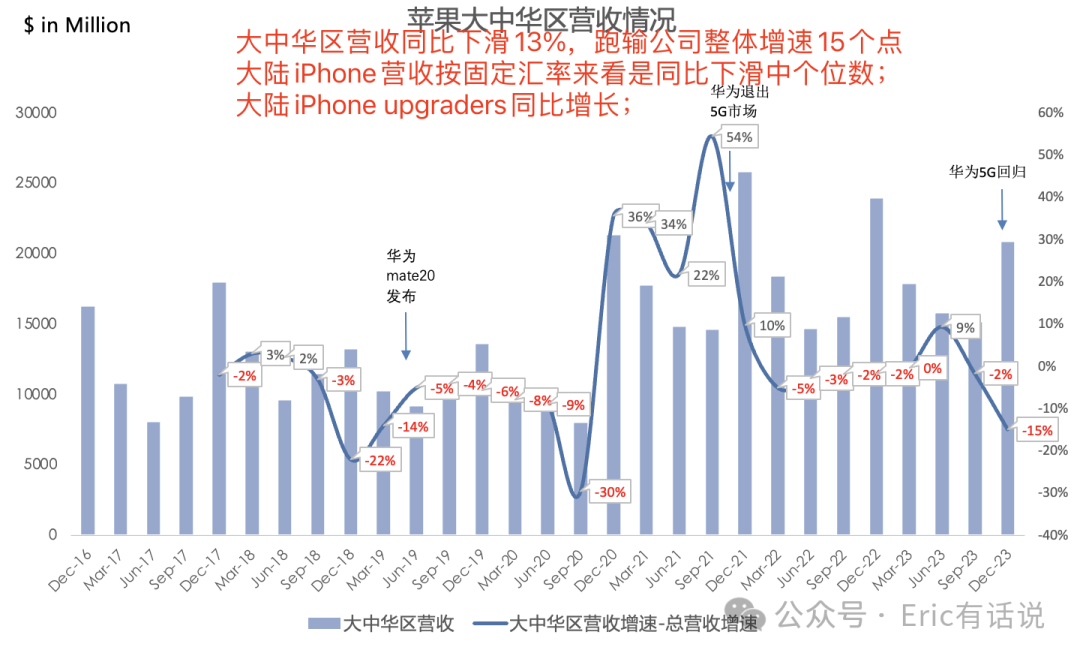

Greater China revenue was $20.8B, down 13% year over year; Greater China operating margin was 41.4%, higher only than the Americas; Greater China was the only region with year-over-year revenue decline; mainland iPhone revenue declined only mid-single digits year over year on a constant-currency basis; mainland iPhone upgraders grew year over year.

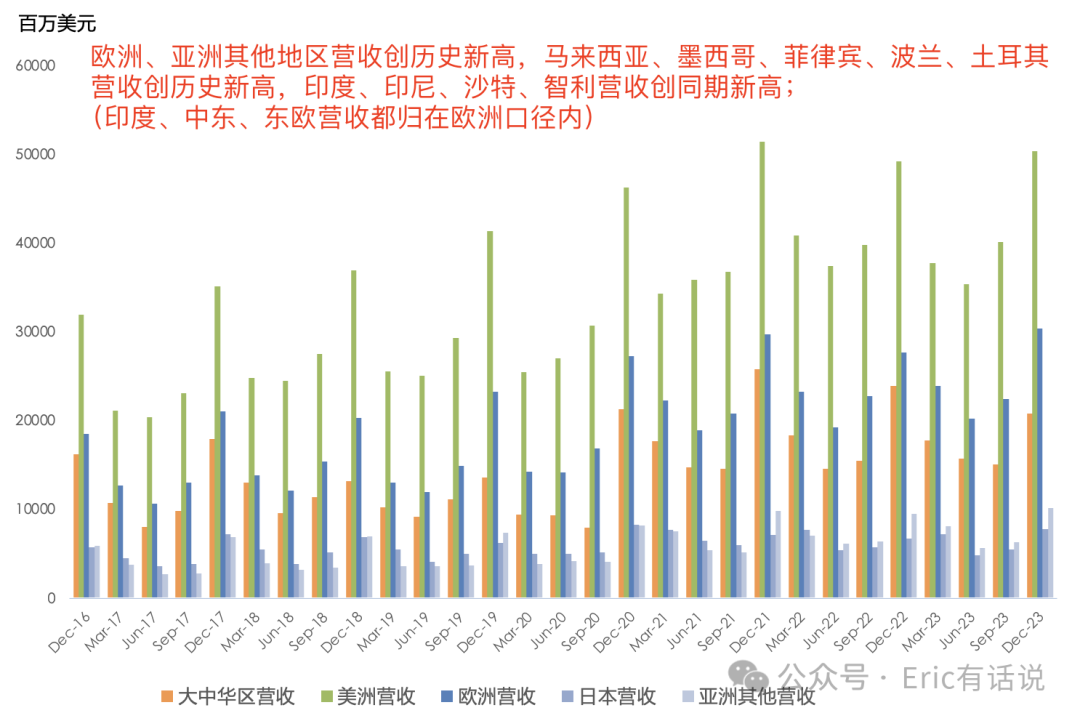

Apple continues to gain share globally, with Europe and Asia ex-China hitting revenue records; Malaysia, Mexico, Philippines, Poland, and Turkey hit revenue records; India, Indonesia, Saudi Arabia, and Chile hit quarterly records; enterprise wins this quarter included Target and Zoho; Target deployed thousands of M3 MacBook Pros; 80% of Zoho's 15,000 employees use iPhone for work, with two-thirds using Mac as their primary computer; Walmart, Nike, Vanguard, Stryker, Bloomberg, SAP, and other enterprise customers have expressed interest in Vision Pro.

EU App Store sideloading takes effect in March 2024; EU App Store revenue accounts for 7% of total App Store revenue.

Q2 revenue guided flat year over year (excluding the ~$5B iPhone supply chain impact from last year), 2-percentage-point FX headwind; iPhone revenue expected flat year over year; Services growth consistent with Q1; gross margin 46%-47%, on track for a fifth consecutive quarterly record; this implies Q2 revenue up ~3% year over year, net income up ~10% year over year, a third consecutive quarter of double-digit net income growth, with EPS growth even faster; Q1 repurchases of $20.5B, dividends of $3.8B.

Overall, Apple's earnings were unremarkable; performance still cannot compare with Microsoft, Google, and Amazon among the four giants. Microsoft and Google have AI, Amazon has AWS and advertising, while Apple's story is relatively flat; the next major variable may be Vision Pro.

Apple's core growth formula: AAPL = active installed base × customer engagement (active installed base at record high × paid subscribers growing high double digits).

Both sides of Apple's core growth formula performed well this quarter; Cook also stated Apple aims to become a ToC + ToB company; the Apple flywheel remains intact long-term. Although Greater China weakness was offset by growth elsewhere, Greater China will remain a focus for some time. Whether EU sideloading spreads to other regions is another key concern.