Marvell FY26Q2 corresponds to actual calendar months May/June/July 2025.

Marvell FY26Q2 Results:

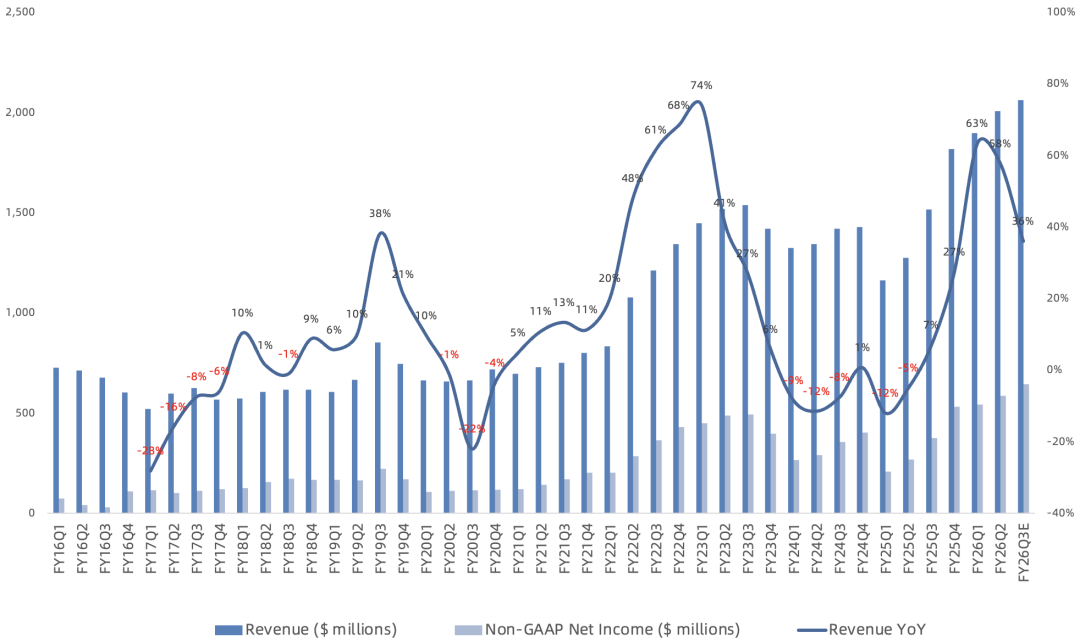

Revenue of $2.006B, up 58% year over year and 6% sequentially. Q3 revenue guided at $2.06B, up 36% year over year.

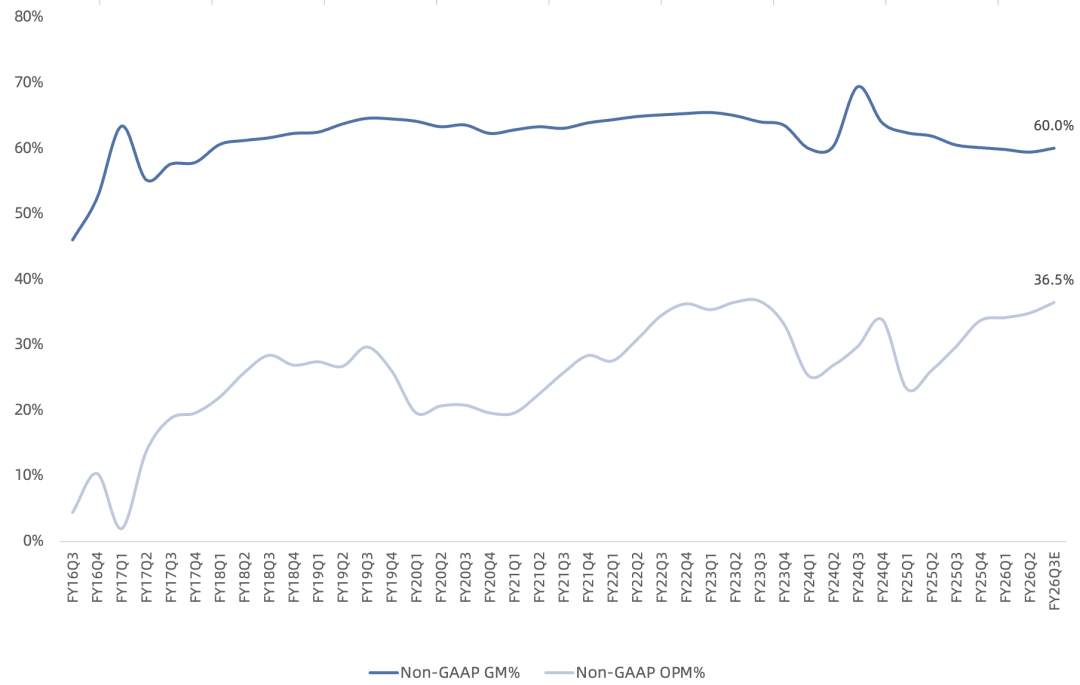

GAAP gross margin of 50.4%, up 4.2 percentage points year over year. Non-GAAP gross margin of 59.4%, down 2.5 percentage points year over year and 0.4 points sequentially, marking the seventh consecutive quarter of sequential decline. Q3 non-GAAP gross margin guided at 60%, down 0.5 points year over year.

Non-GAAP operating income of $699M, up 111% year over year. Non-GAAP operating margin of 34.8%, up 8.7 points year over year and 0.6 points sequentially. Q3 non-GAAP operating income guided at $751M, up 67% year over year, operating margin of 36.5%.

Non-GAAP net income of $586M, up 120% year over year. Non-GAAP net margin of 29.2%. Q3 non-GAAP net income guided at $644M, up 73% year over year, net margin of 31.3%.

GAAP days in inventory of 96 days, down 8 days sequentially.

$200M in share repurchases this quarter, $51.7M in dividends; $2B remaining in repurchase authorization.

Revenue mix this quarter: China 29%, Taiwan 27%, US 15%, Singapore 7%, Malaysia 4%, Netherlands 3%, Japan 3%, Finland 3%, Thailand 2%.

By business, Q2:

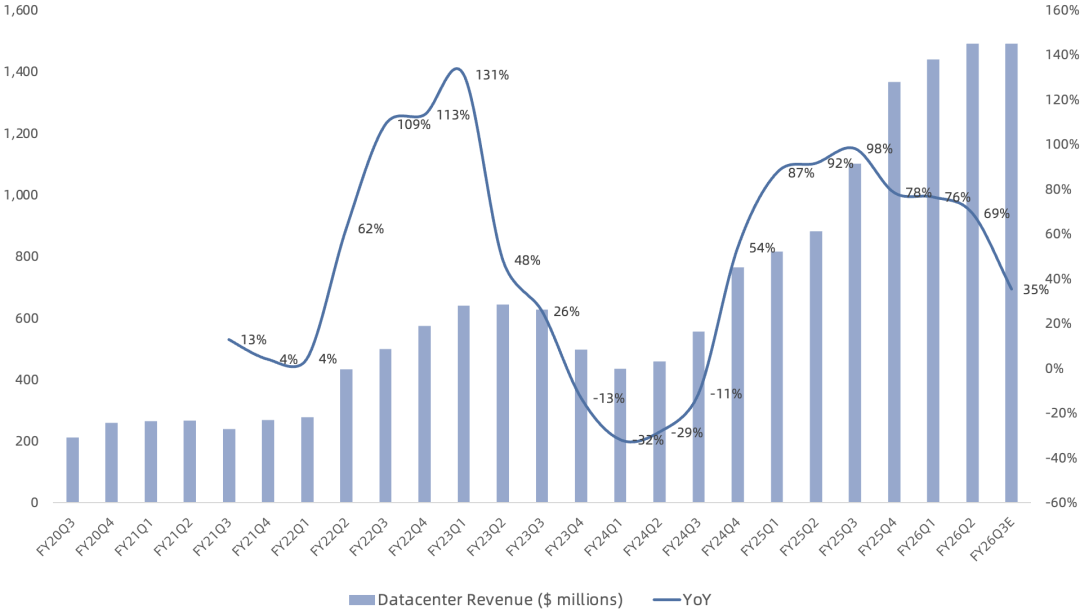

Data center revenue of $1.491B, up 69% year over year and 4% sequentially, accounting for 74% of revenue, a new high. AI and cloud remain the primary drivers, accounting for over 90% of data center revenue; the remainder comes from on-premise data center end markets (revenue run rate ~$500M).

Led by custom XPU (Amazon Trainium2 XPU + Google Axion CPU) and XPU Attach products, plus the electro-optics interconnect portfolio. Data center storage revenue grew. Custom XPU and electro-optics now together account for over 3/4 of total data center revenue; the rest is primarily data center storage, switching, and security portfolios. This quarter won Microsoft server security chip HSM order; total of 18 design wins in hand, expected to bring $75B (unchanged) in lifetime revenue potential.

In the electro-optics interconnect portfolio, PAM and DCI businesses continue to grow. Customer demand for 800G PAM DSP remains strong; its product lifecycle remains long. Also begun volume shipping next-gen 200G-per-lane, 1.6T aggregate PAM DSP to multiple customers; adoption expected to accelerate over the next several quarters. 51.2 Tbps switch continues to ramp. Won Microsoft server security chip HSM order. Launched industry's first 2nm custom SRAM service.

Marvell's full interconnect portfolio includes: DSPs for AEC and AOC; retimers for PCIe, Ethernet, and UALink; and silicon photonics for NPO and CPO XPU optics. AEC and AOC DSP products are already in market; retimers undergoing customer evaluation.

Enterprise networking revenue of $194M, up 28% year over year, 9% of revenue. Carrier infrastructure revenue of $130M, up 71% year over year, 6% of revenue. Enterprise networking and carrier markets continue to recover.

Consumer revenue of $63M, up 30% year over year, 6% of revenue. Game console demand and its seasonality remain the primary driver.

Automotive/industrial revenue of $76M, down 0.3% year over year, 4% of revenue. Marvell announced sale of automotive Ethernet business to Infineon on April 7 for $2.5B; transaction has closed.

Outlook:

Q3 data center revenue guided flat (~$1.5B, ~38% of Intel's projected Q3 data center revenue, ~36% of AMD's data center revenue, ~24% of Broadcom's AI revenue). Electro-optics sequential double-digit growth offsets XPU decline. XPU business expected to achieve sequential H2 vs H1 growth in the second half; growth expected to be non-linear, with Q4 far stronger than Q3.

Q3 carrier and enterprise networking combined revenue guided up ~30% sequentially.

Q3 automotive/industrial combined revenue guided at $35M, flat sequentially.

Q3 consumer revenue guided down low-single-digits% sequentially.

Starting Q4, non-data-center end markets will be consolidated into a single new "Communications & Other" end market.

Still no mention of the >$2.5B full-year 2025 AI revenue target.

Overall, Marvell missed expectations this quarter. Management remains optimistic on future growth but refuses to give concrete guidance. Its ASIC "pie" is less aggressive than arch-rival Broadcom, and ASIC shows clear seasonality. Post-Broadcom earnings, the market increasingly believes both GPU and ASIC will be winner-take-all for incumbents, leaving little for second-place players like AMD and Marvell.

Although official Q3 guidance shows non-GAAP net margin already reaching 31%, with full year potentially above 30%, the weak Q3 data center guidance makes Q4 performance uncertain, casting doubt on whether full-year non-GAAP net income can hold the previously projected $2.6B.