Marvell's FY27Q1 covers February through April 2026.

Marvell FY27Q1 Results:

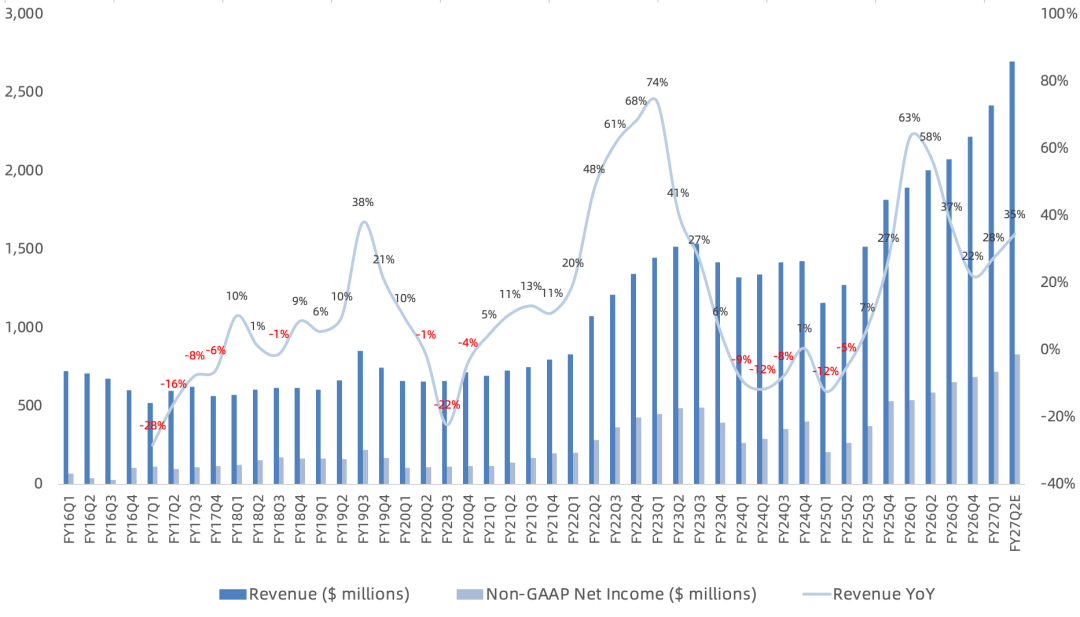

Revenue reached $2.42B, up 28% year over year and 9% sequentially, slightly above the $2.41B consensus estimate. Q2 revenue is expected to reach $2.7B, up 35% year over year.

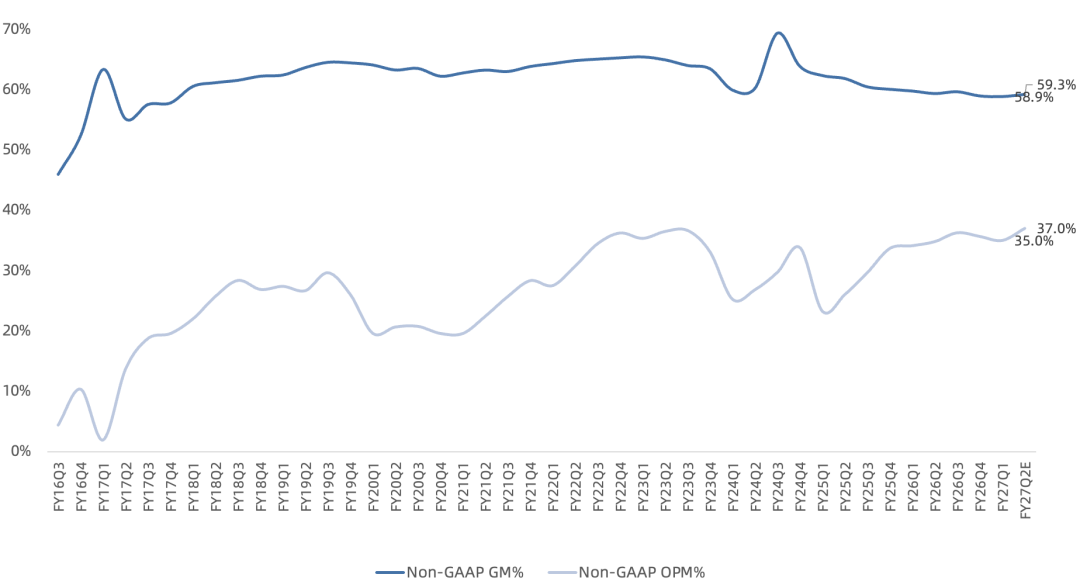

GAAP gross margin was 52.1%, up 1.8 percentage points year over year. Non-GAAP gross margin was 58.9%, down 0.9 points. FY27Q2 non-GAAP gross margin is expected to reach 59.3%, down 0.1 points year over year.

Non-GAAP net income reached $720M, up 33% year over year and slightly above the $710M consensus estimate. Non-GAAP net margin was 29.7%. FY27Q2 non-GAAP net income is expected to reach $830M, up 42%, with a 30.8% net margin.

GAAP days inventory outstanding fell seven days sequentially to 110.

Marvell repurchased $200M of stock and paid $53.8M in dividends this quarter.

Q1 Business Detail:

Data center revenue reached $1.83B, up 27% year over year and 11% sequentially, representing 76% of total revenue and remaining Marvell's largest business. Growth was driven primarily by optical interconnect. Communications and other revenue reached $585M, up 29% year over year and 3% sequentially, representing 24% of revenue.

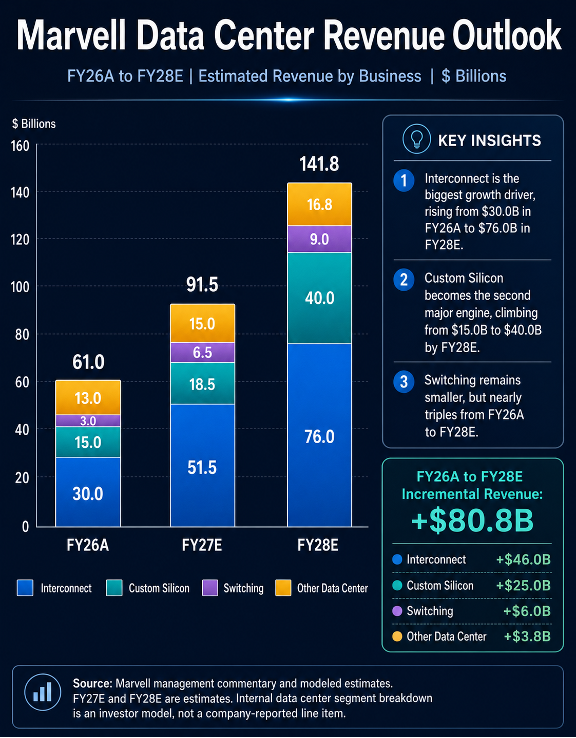

Data center interconnect is now Marvell's largest business. Revenue is expected to grow more than 70% in FY27 and remain the main FY28 growth driver across scale-out, scale-across, and scale-up networks.

In scale-out PAM, demand for 800G products continues to strengthen, while 200G-per-lane 1.6T solutions are ramping rapidly in FY27 after entering production in the second half of FY26. Management expects another major step-up in 1.6T revenue in FY28. Marvell continues to benefit from being first to market across multiple PAM4 generations and aims to lead the next 400G-per-lane generation. Beyond DSPs, the company is expanding quickly in broadband analog, TIAs, and drivers, with combined TIA and driver revenue expected to exceed a $1B run rate over the next several quarters.

In scale-across DCI, coherent-lite technology should move deeper into the data center as a complement to shorter-reach PAM. Marvell has begun shipping its first 200G-per-lane 1.6T coherent-lite products. The emergence of scale-across networks is driving a major DCI architecture shift that should expand the market for pluggable DCI modules over the next several years. Marvell now ships DCI solutions to all five major U.S. hyperscalers. Traditional DCI deployments are moving from 400G to 800G, while scale-across architectures are expected to adopt 1.6T rapidly. Marvell has the industry's first secure 1.6T ZR and ZR+ DCI modules, powered by an all-2nm coherent DSP introduced earlier this year, with sampling scheduled to begin this year. DCI revenue was about $500M in FY26 and is expected to reach a $1B annualized run rate in FY28.

In scale-up optics, Marvell supports both NPO and CPO implementations through a broad silicon-photonics platform covering MZM, EAM, and MRM modulators, backed by leading broadband analog, TIA, and driver products. It is also investing in emerging approaches such as microLED and microVCSEL. Marvell is working closely with several Tier 1 customers on third-generation 6.4T light engines for NPO and CPO. Scale-up optics should ramp meaningfully in FY28, with revenue now expected to more than double the prior $150M outlook and exceed $300M. The earlier outlook reflected Celestial AI alone.

The data center switching business continues to benefit from sustained demand for 12.8T products and a strong ramp in next-generation 51.2T switches for scale-out networks. Both existing and new customers are showing strong interest in Marvell's 51.2T platform and its new 100T platform.

FY27 scale-out switch revenue is still expected to exceed $600M and could surpass a $1B annualized run rate in FY28. Scale-up switching is an emerging market where Marvell has increased investment through internal development and the XConn acquisition. Some customers currently use PCIe switches for this generation of scale-up networks, but PCIe limitations in radix and bandwidth should drive a rapid transition toward purpose-built, high-radix, high-bandwidth UALink, ESUN, and NVLink solutions. Marvell can support all of these protocols, and each partnership represents a multi-billion-dollar lifetime revenue opportunity given the size of the scale-up TAM.

Data center custom silicon revenue is still expected to grow more than 20% in FY27, led by a flagship XPU program that should drive multi-year growth across several generations. Multiple XPU-attach programs, including CXL and NIC products, are also ramping in FY27.

Custom silicon revenue is still expected to more than double in FY28. Growth should be split roughly evenly among existing programs, including Amazon Trainium 2 and 3 XPUs and Google's Axion CPU, XPU-attach products, and new programs. More than ten XPU-attach projects are moving into higher-volume phases, and a new Tier 1 XPU program entering production has firm demand visibility for the entire next fiscal year. Management remains confident in the FY29 custom silicon target of more than $10B, consistent with a 20% share of a $55B ASIC TAM including XPU attach. One custom program that was cut significantly in prior forecasts is now progressing well and should contribute one-third of FY28 custom silicon growth. Management did not update last quarter's XPU-attach revenue framework of roughly $200M in FY26, $500M in FY27, $1B in FY28, and $2B in FY29.

Other data center products, including AECs and retimers, are ramping after design wins at three Tier 1 U.S. hyperscalers and several additional customers. Combined revenue is still expected to more than double in FY27 and continue growing rapidly in FY28.

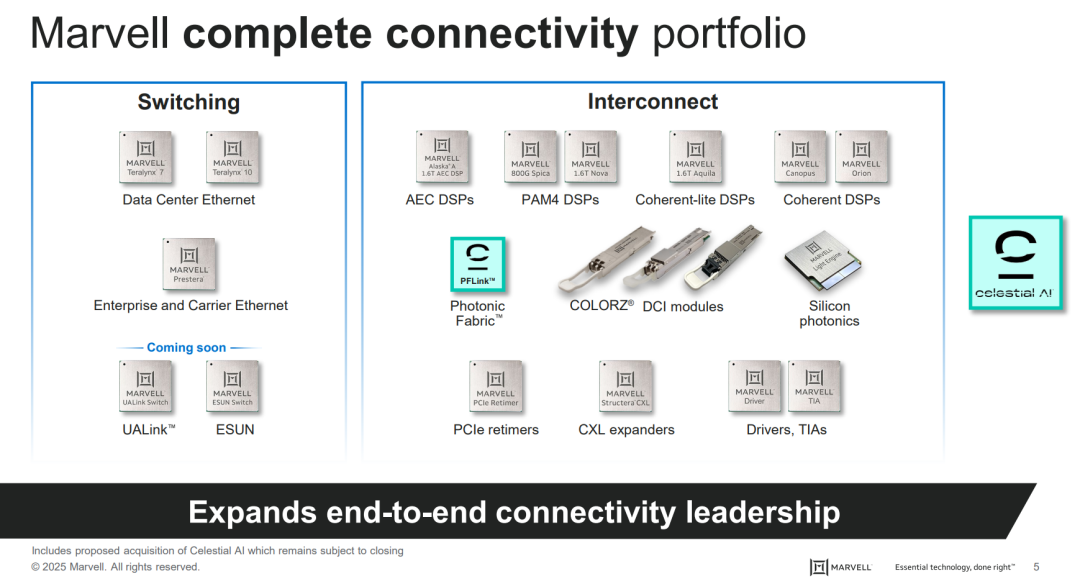

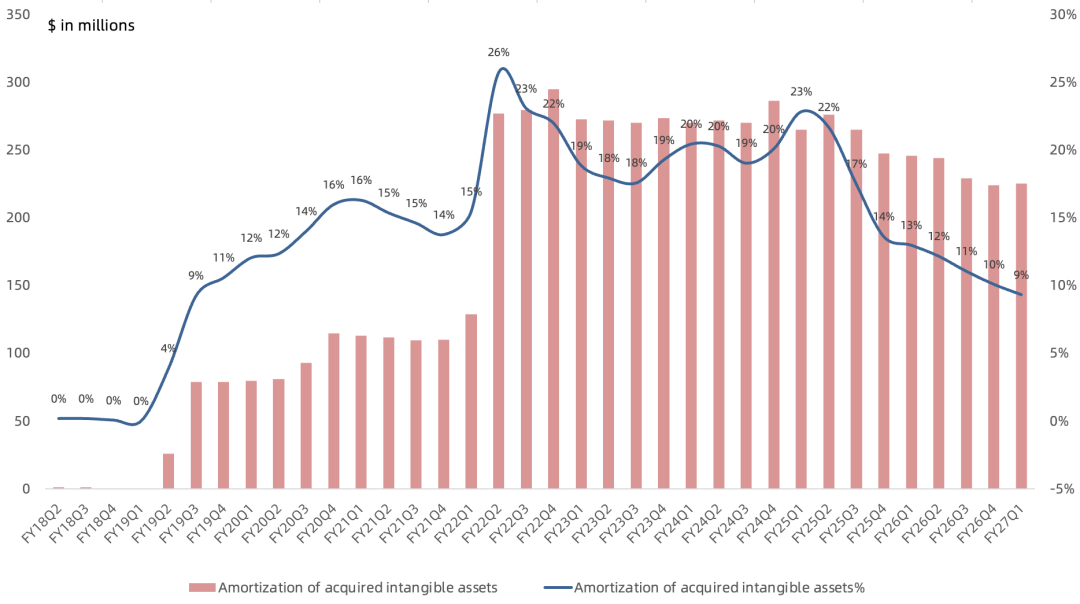

Since 2019, Marvell has reshaped its data center portfolio through acquisitions while divesting Wi-Fi and automotive Ethernet. The purchases of Avera, Aquantia, Inphi, Innovium, Celestial AI, and XConn created substantial intangible amortization that once exceeded 20% of revenue, but revenue growth has reduced that ratio to 9%. This quarter Marvell announced the acquisition of Polariton, a developer of high-speed, low-power plasmonic silicon-photonics devices. Polariton has demonstrated plasmonic modulator bandwidth above 1 THz, up to ten times that of current silicon-photonics and thin-film lithium-niobate solutions. Marvell plans to integrate the technology into its DCI and coherent-lite roadmaps, extending the platform to 3.2T and beyond.

Outlook:

Marvell now expects quarterly revenue to reach $3B in FY27Q3, one quarter earlier than previously guided. Year-over-year growth should accelerate each quarter and approach 50% in FY27Q4. Full-year FY27 revenue guidance rises to $11.5B from $11B, implying roughly 40% growth, while FY28 revenue guidance increases to $16.5B from $15B, implying 45% growth.

FY27 data center revenue growth is raised to 50% from 40%, while interconnect growth rises to 70% from 50%. Custom silicon remains guided to 20% growth, and communications and other markets remain at 10%. For FY28, data center growth is raised to 55% from 50%, while communications end markets stay at low-single-digit growth. Interconnect should grow materially faster than cloud capex, which is expected above 30%, reflecting strong 1.6T scale-out demand and contributions from scale-up and scale-across. Custom silicon is still expected to at least double. Management did not raise last quarter's FY28 EPS outlook of more than $5.

FY27 non-GAAP operating expenses are expected to be about $2.45B, including the impact of the Celestial AI and XConn acquisitions completed in FY27Q1. FY28 non-GAAP operating expenses should grow at a mid-to-high-teens rate, while operating margin reaches the top of the 38%-40% target range.

The NVIDIA partnership has three core pillars:

1. Optical collaboration: Marvell has long been a key supplier of DSPs, TIAs, and drivers to NVIDIA. The companies will jointly develop silicon-photonics technology, which is expected to become critical for scale-up networks.

2. NVLink Fusion integration: Marvell can build custom silicon and networking chips that connect seamlessly with the NVIDIA ecosystem. This gives hyperscalers more flexibility to combine custom and merchant capabilities within their platforms and should create new opportunities for both companies.

3. AI RAN: Marvell will enhance its OCTEON base-station processors to work directly with NVIDIA GPUs, combining AI and wireless infrastructure on a single software-defined computing platform. Telecom operators will be able to run 5G and 6G radio workloads alongside high-performance AI applications on the same hardware.

Overall, Marvell still faces a relatively long earnings gap before FY28, but management continues to edge guidance higher and emphasize strong growth across optical interconnect, scale-up, scale-out, scale-across, and XPU-attach products. That message aligns closely with investor enthusiasm around optical networking and the long-term potential of custom XPUs.

Marvell shares surged after the previous earnings report. Under the latest guidance, FY27 revenue of $11.5B still implies roughly $3.5B of net income, while FY28 revenue of $16.5B and EPS above $5 imply approximately $4.5B-$5B of net income. The current valuation is about 50 times FY27 earnings and 35 times FY28 earnings. The fundamental outlook has not changed dramatically, but the valuation has doubled since last quarter, helped by the first hints of FY29 potential.