Marvell's FY25Q1 corresponds to the February/March/April 2024 period.

Marvell FY25Q1 Results:

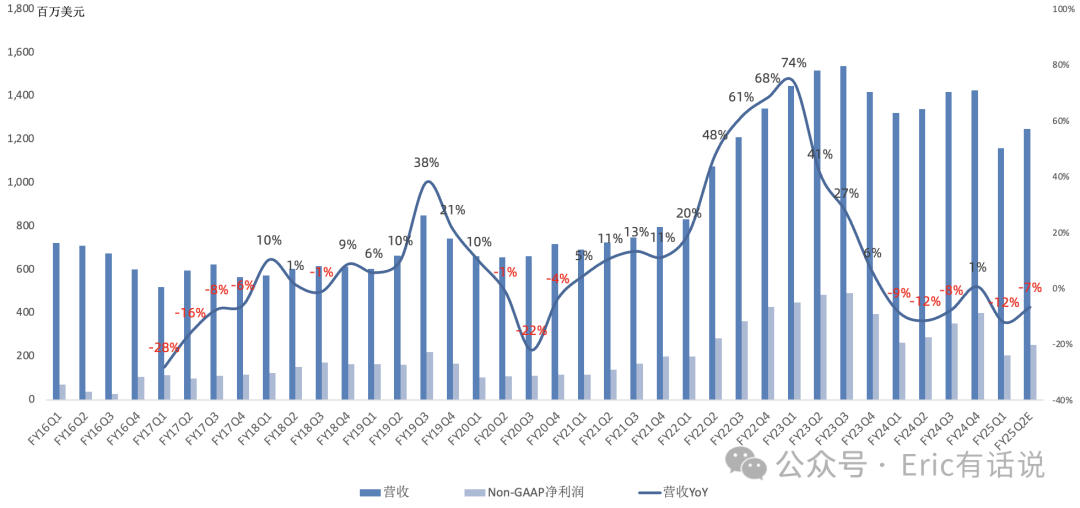

Revenue was $1.161B, down 12% year over year and 19% sequentially, a low since Q2 2021.

GAAP gross margin was 45.5%, up 3.3 percentage points year over year and down 1.1 percentage points sequentially; non-GAAP gross margin was 62.5%, up 2.5 percentage points year over year and down 1.4 percentage points sequentially.

Non-GAAP operating profit was $270M, down 19% year over year, with a non-GAAP operating margin of 23.3%.

Non-GAAP net income was $207M, down 22% year over year, a low since Q2 2021; non-GAAP net margin was 17.8%.

GAAP days in inventory was 117 days, up 9 days sequentially, marking the second consecutive quarterly increase.

Mainland China accounted for 46% of revenue, US 19%, Singapore 9%, Thailand 5%, Malaysia 5%, Taiwan 4%, Finland 2%, Japan 1%.

$150M in share repurchases and $51.8M in dividends this quarter; repurchase pace is expected to increase next quarter.

Q1 Business Detail:

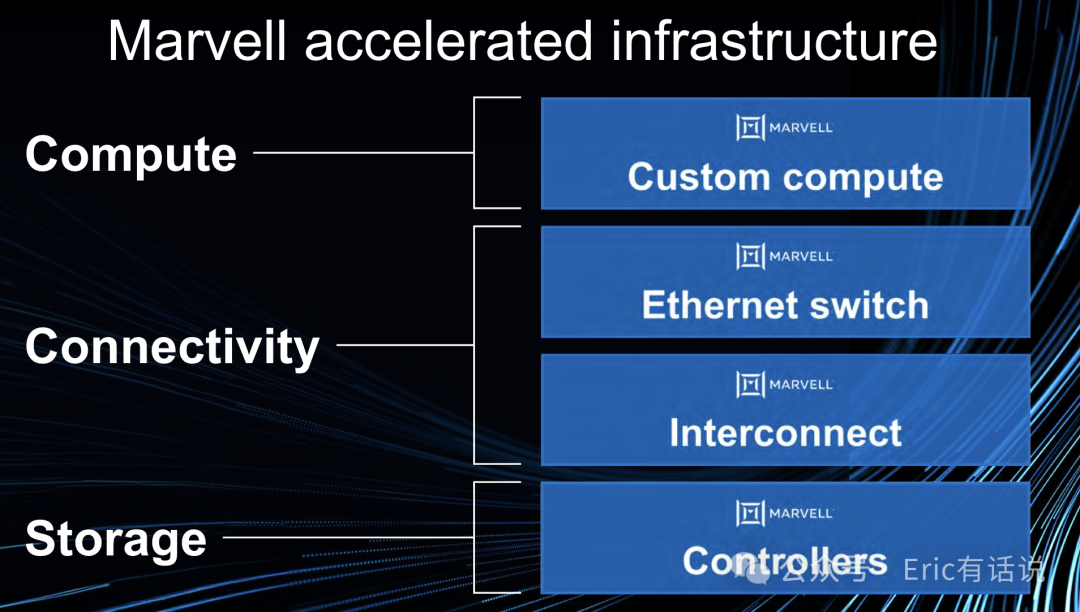

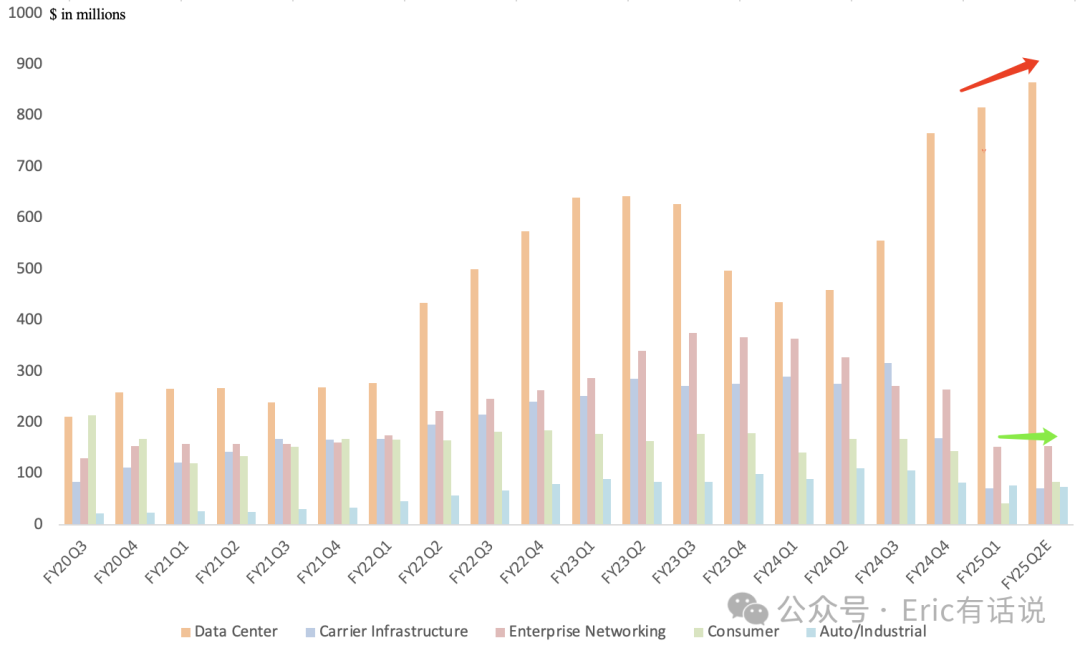

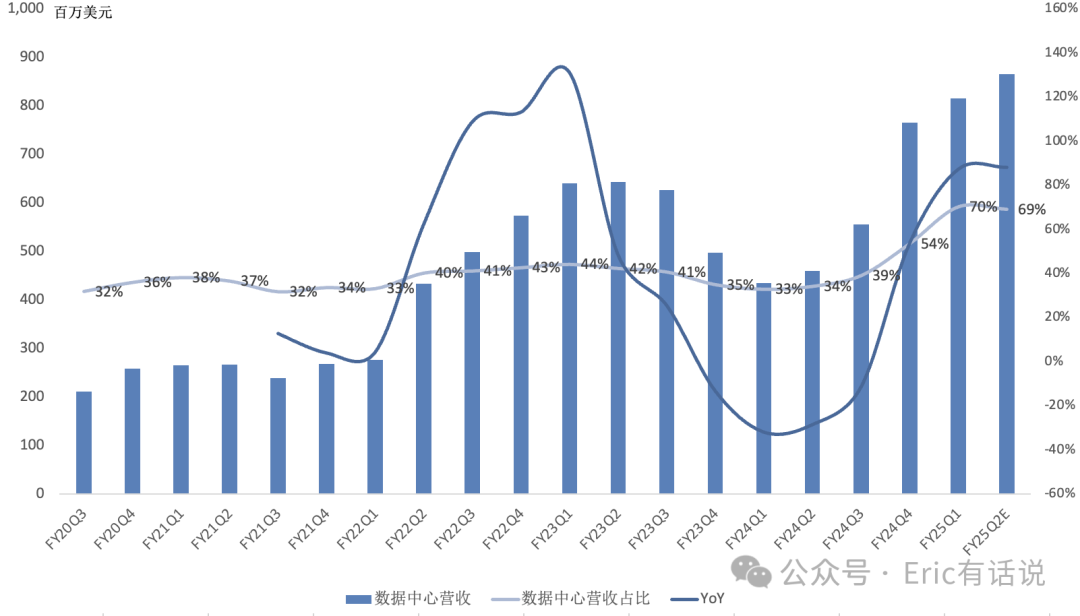

Data center revenue was $820M, up 87% year over year, accounting for 70% of revenue.

Driven by cloud data center demand for PAM/DSP/TIA optical products and ZR DCI products; cloud data center posted double-digit growth, both AI and non-AI, while on-premise enterprise declined sequentially; 1.6T PAM products are in customer qualification; 400G DCI module shipments are strong, 800G DCI has won multiple customers, and a new coherent DSP unlocks a future $1B market, with DCI products expected to reach $3B revenue by 2028; PAM DSP products for the AEC market have begun shipping, primarily to Tier 1 cloud, unlocking another future $1B market; officially entered the PCIe Gen6 Retimer market, with 8/16-lane PAM4-based PCIe Gen6 Retimer products sampling; next-gen 51.2T products slated for volume production by year-end.

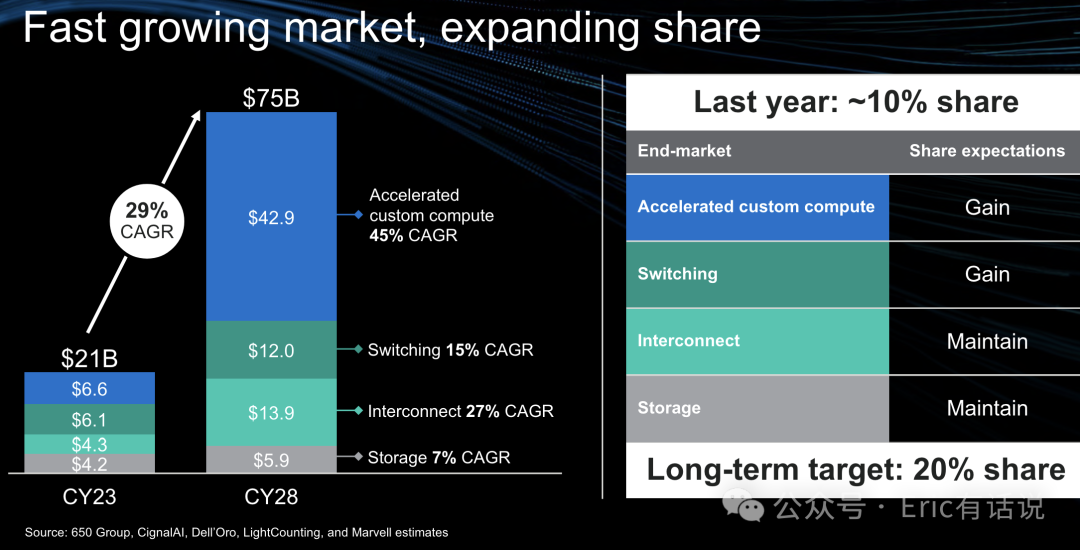

Custom silicon began shipping, with volume ramp in the second half; the total custom silicon TAM is expected to grow from $7B this year to over $40B by 2028 (45% CAGR), with 2025 TAM of $10B; the company's share is near 10%, targeting 20%; the total data center TAM is expected to grow from $21B last year to $75B by 2028 (29% CAGR), with the company's share rising from 10% to a target of 20%.

Non-data center businesses bottomed in H1, with recovery in H2; the second-half custom silicon volume ramp is expected to drive revenue growth while pressuring gross margin; second-half recovery is expected, with Q3 and Q4 revenue accelerating.

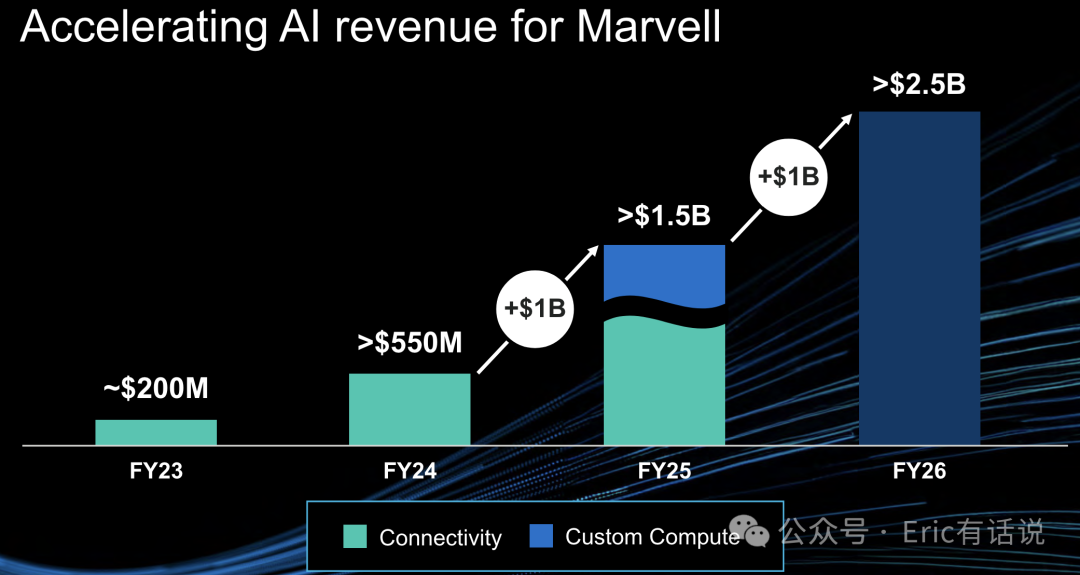

Full-year 2024 AI revenue is expected to exceed $1.5B, with 2/3 from optical products and 1/3 from custom silicon; 2025 AI revenue is expected to be at least $2.5B.

Enterprise networking revenue was $150M, down 58% year over year, accounting for 13% of revenue; enterprise networking customers continue to destock, with positive signals but still a distance from recovery.

Carrier infrastructure revenue was $70M, down 75% year over year, accounting for 6% of revenue; the market remains weak, but the wireless business has new products ramping, with bookings and demand recovering, providing confidence for a second-half recovery.

Consumer revenue was $40M, down 70% year over year, accounting for 4% of revenue; demand remains weak.

Automotive/industrial revenue was $80M, down 13% year over year, accounting for 7% of revenue, primarily due to automotive inventory correction.

Outlook:

Q2 data center revenue is expected to grow mid-single-digits sequentially, driven primarily by custom silicon, with optical products flat to slightly up sequentially.

Q2 carrier infrastructure revenue is expected to be flat sequentially.

Q2 enterprise networking revenue is expected to be flat sequentially.

Q2 automotive/industrial revenue expected to be flat sequentially.

Q2 consumer revenue is expected to double sequentially.

Second-half recovery is expected, with Q3/Q4 revenue accelerating.

Overall, Marvell's results were still somewhat ugly: AI is indeed growing, but traditional businesses continue to decline sharply, though the good news is they have bottomed.

In the previous earnings article, I noted: "Optimistically assuming a second-half recovery, 2024 revenue is expected around $5.3-5.9B, at most single-digit growth, still below the prior memory cycle peak. Margins pressured by weak high-margin traditional businesses, non-GAAP net income could trough around $1.1B (at the current $57B market cap, that's 52x P/E), well below the historical peak of $1.8B (32x P/E at the same market cap)." Management is still banking on a full-throttle 2025.