Marvell's FY25Q2 fiscal quarter corresponds to actual months of May/June/July 2024.

Marvell FY25Q2 Earnings:

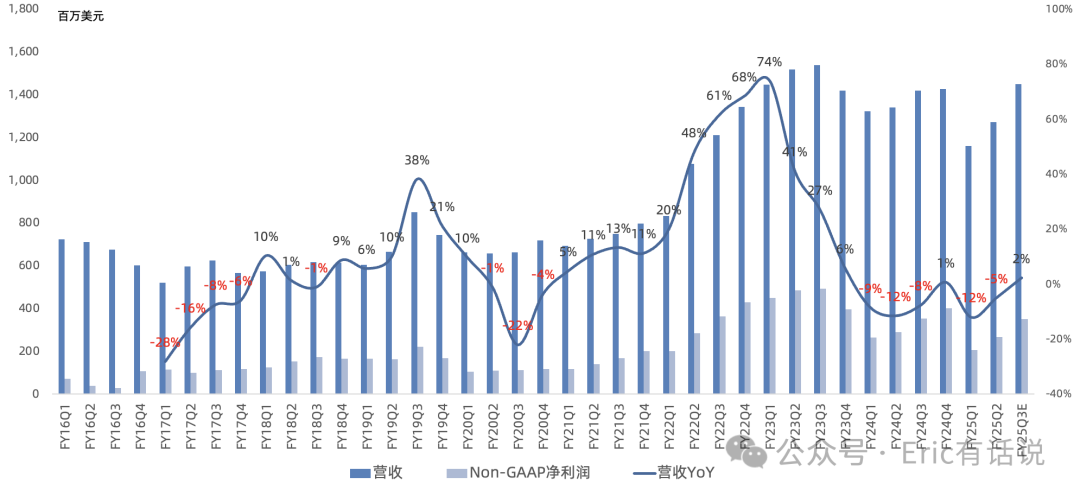

Revenue $1.273B, down 5% year over year, up 10% sequentially, beginning to bottom and recover.

GAAP gross margin 46.2%, up 7.3 percentage points year over year and 0.7 percentage points sequentially; Non-GAAP gross margin 61.9%, up 1.6 percentage points year over year, down 0.5 percentage points sequentially.

Non-GAAP operating income $332M, down 8% year over year, declining for the 2nd consecutive quarter; Non-GAAP operating margin 26.1%.

Non-GAAP net income $266M, down 8% year over year, declining for the 2nd consecutive quarter; Non-GAAP net margin 20.9%.

GAAP days in inventory 107 days, down 10 days sequentially, ending 2 consecutive quarters of sequential increases.

Mainland China revenue share 46%, US 16%, Singapore 11%, Thailand 7%, Taiwan 3%, Japan 3%, Philippines 3%, Malaysia 2%, Finland 2%. Top customer 13% of revenue; second largest customer 10%.

$175M in share repurchases this quarter; $52M in dividends.

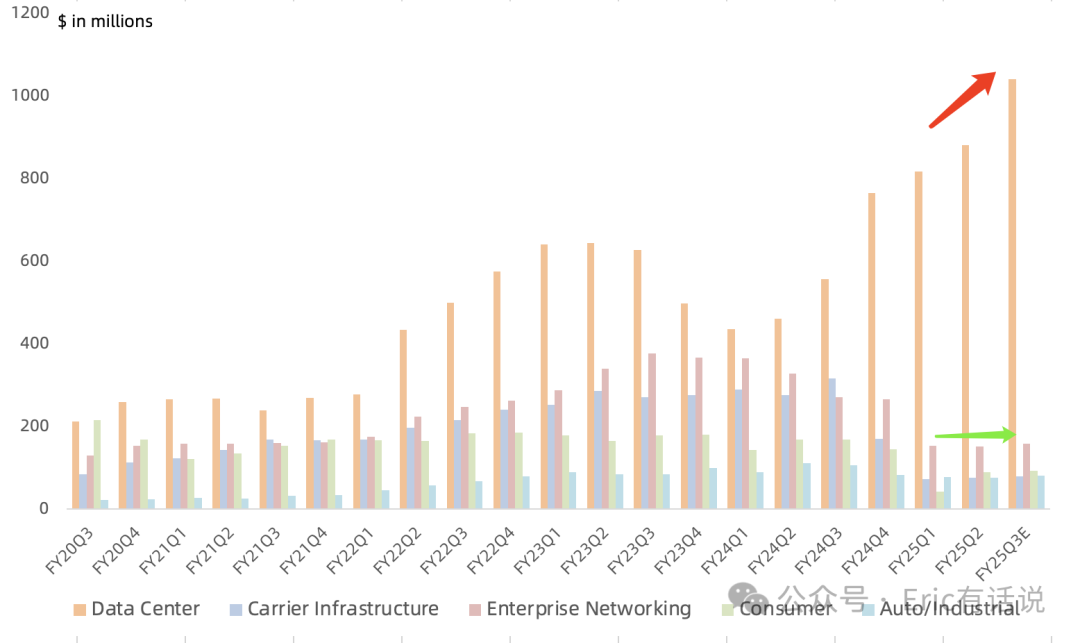

By business, Q2:

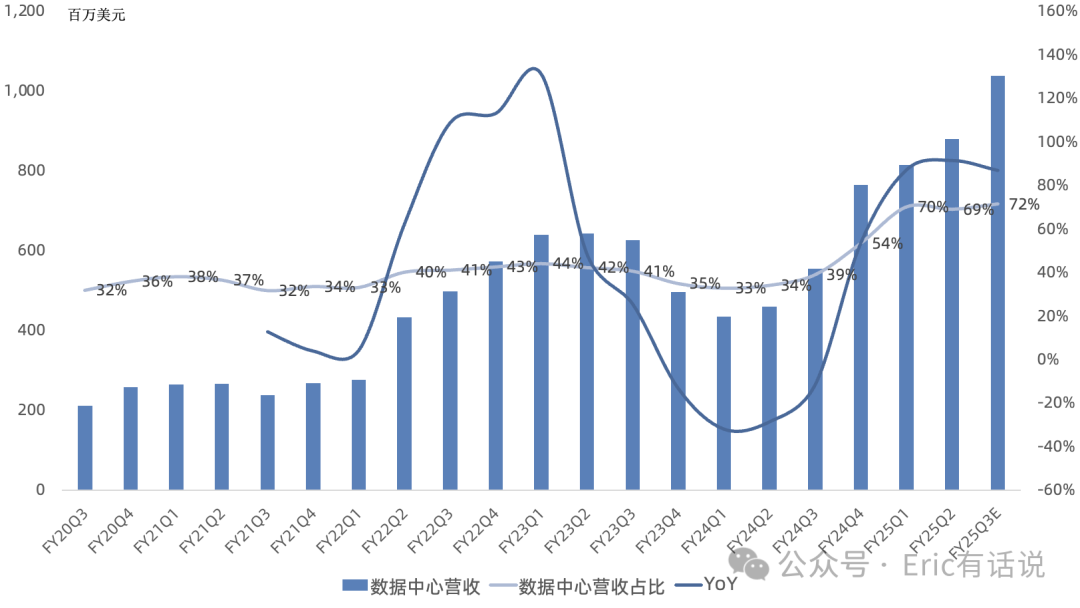

Data center revenue $881M, up 92% year over year, 69% of total revenue.

Driven by strong optical demand, custom silicon ramping on schedule, and growth in storage and switch chips. 1.6T PAM DSP began shipping in Q3; optical products expected to grow each quarter in the second half. 800G PAM DSP for AEC market began shipping; 1.6T PAM DSP sampling started. The company now has four new data center interconnect products: AEC DSP, PCIe retimer, silicon photonics, and long-haul DCI modules. Data center storage recovering, quarterly revenue approaching $200M run rate.

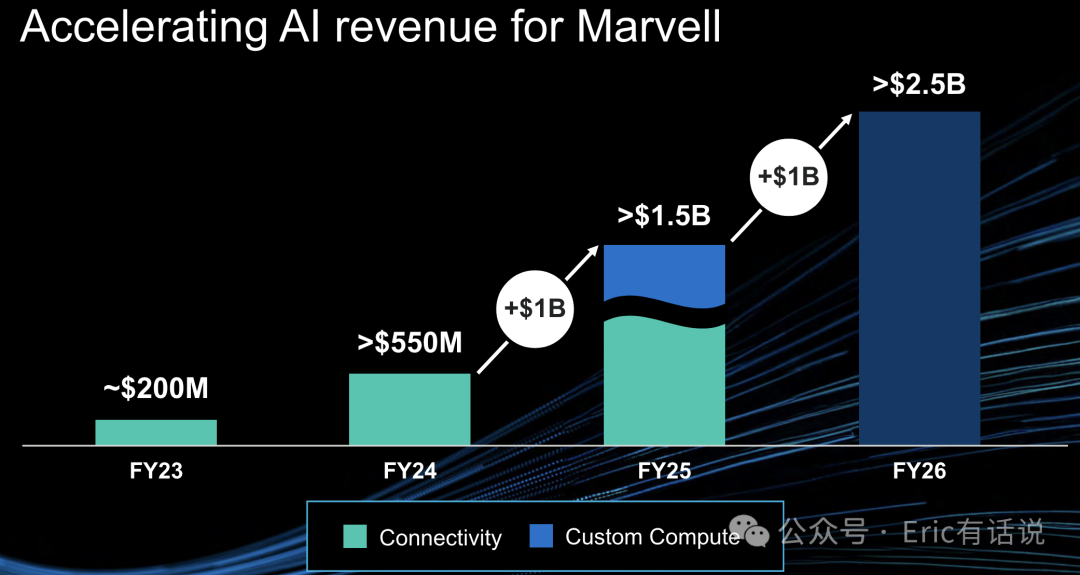

First two custom silicon products entered volume production, contributing significant revenue in Q3. Custom silicon ramp in the second half will drive revenue growth while pressuring gross margin, but by eliminating NRE expenses it will reduce opex and improve operating margin.

Guidance unchanged: 2024 full-year AI revenue over $1.5B (2/3 optical, 1/3 custom silicon); 2025 AI revenue over $2.5B.

Enterprise networking revenue $151M, down 54% year over year, 12% of revenue. Carrier infrastructure revenue $76M, down 73% year over year, 6% of revenue. Both markets bottomed in the first half and are showing recovery signals: carrier customers placing orders for 5nm Octeon DPU; enterprise networking customer orders growing. Q3 combined enterprise networking and carrier revenue expected up mid-single digits sequentially; Q4 sequential acceleration. Long-term, each business expected to reach >$1B annualized, combined >$2.2B, with mid-single-digit growth.

Consumer revenue $89M, down 47% year over year, 7% of revenue. Future consumer market annualized revenue expected around $300M, mostly from game console SSD controllers.

Automotive/industrial revenue $76M, down 31% year over year, 6% of revenue, mainly due to automotive inventory correction.

Outlook:

Q3 data center revenue expected up high-teens% sequentially (over $1B, approaching 1/3 of Intel/AMD data center revenue), driven mainly by custom silicon with optical continuing to grow.

Q3 carrier and enterprise networking combined revenue expected up mid-single digits sequentially.

Q3 automotive/industrial revenue expected up mid-single digits sequentially.

Q3 consumer revenue expected up slightly sequentially.

Q4 revenue expected to accelerate; gross margin trajectory over the next few quarters similar to Q3 guidance.

North American cloud giants are indeed focused on geopolitical risk in the optical module supply chain.

Overall, Marvell's traditional business has finally bottomed, giving confidence to other traditional-heavy semiconductor companies for a second-half recovery. With traditional business returning, management hopes for a full-throttle 2025.

In the previous earnings article, I noted: "Optimistically assuming a second-half recovery, 2024 revenue around $5.3-5.9B, at best single-digit growth, still below the prior memory cycle peak." Given management's comment that low-margin custom silicon actually carries good operating margins, I optimistically estimate Non-GAAP net income around $1.2-1.4B (current $66B market cap implies 47-55x P/E). The historical peak of $1.8B net income (37x P/E at current cap) could be reached next year.

As an aside, the market lately is interesting: unwilling to give high valuations to truly high-growth, high-certainty companies, but willing to give high valuations to companies with historically rare high growth, even applying different standards for what counts as high growth.