Marvell FY24 Q3 Earnings:

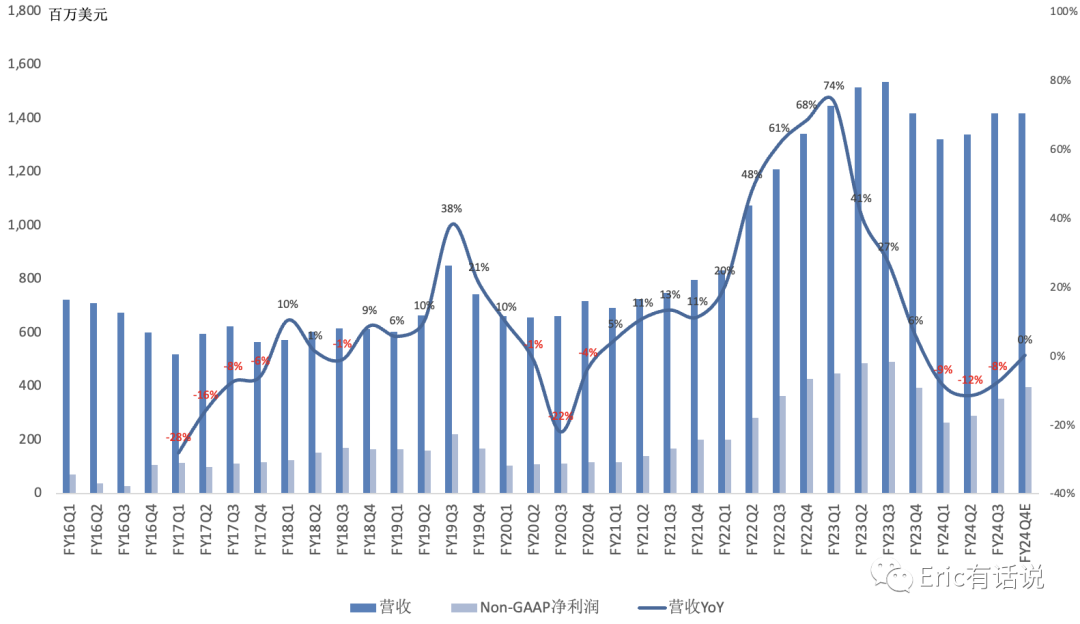

Revenue $1.419B, down 8% year over year, third consecutive quarter of year-over-year decline, up 6% sequentially.

GAAP gross margin 39%, down 11.7 percentage points year over year, flat sequentially; Non-GAAP gross margin 64%, flat year over year, up 0.5 percentage points sequentially.

Non-GAAP operating income $422M, down 25% year over year, up 17% sequentially; Non-GAAP operating margin 29.8%.

Non-GAAP net income $354M, down 28% year over year, up 22% sequentially; Non-GAAP net margin 25%.

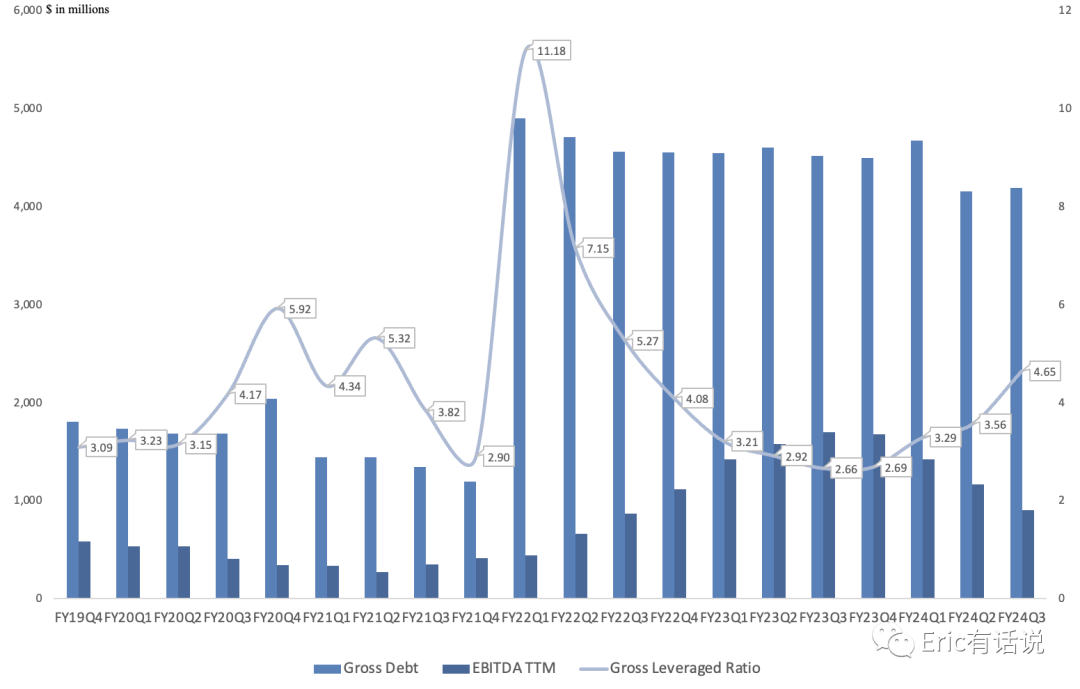

GAAP days in inventory 98 days, down 16 days sequentially, third consecutive quarter of sequential decline.

Mainland China revenue share 43%, US 15%, Finland 11%, Thailand 7%, Singapore 5%, Taiwan 2%, Malaysia 2%, Japan 3%.

Segment Detail, Q3:

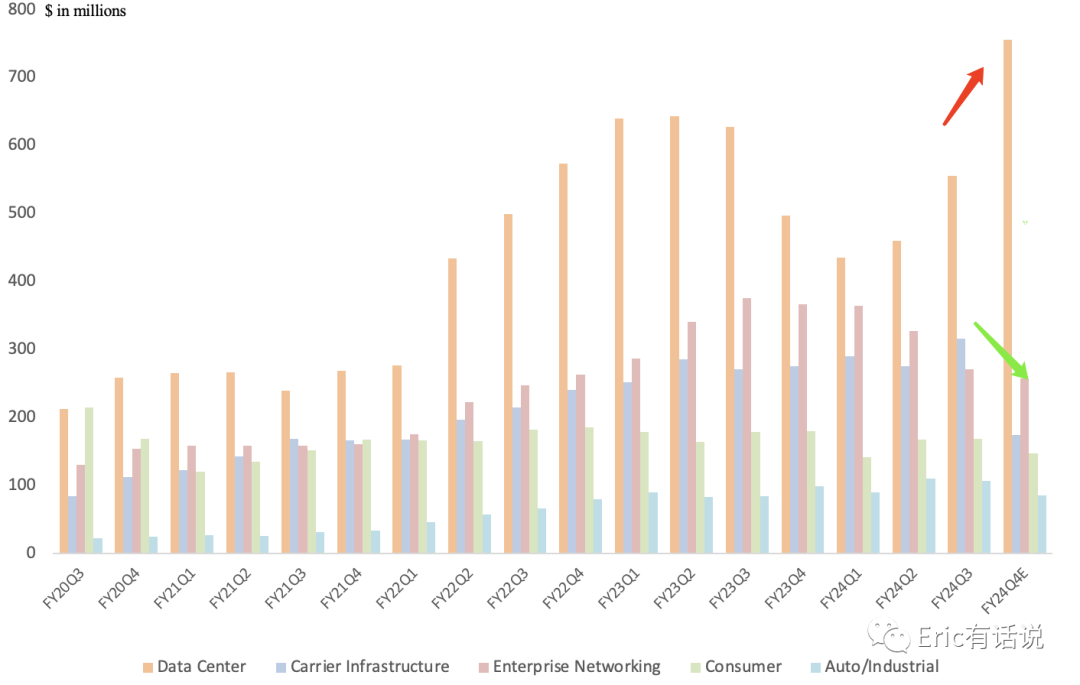

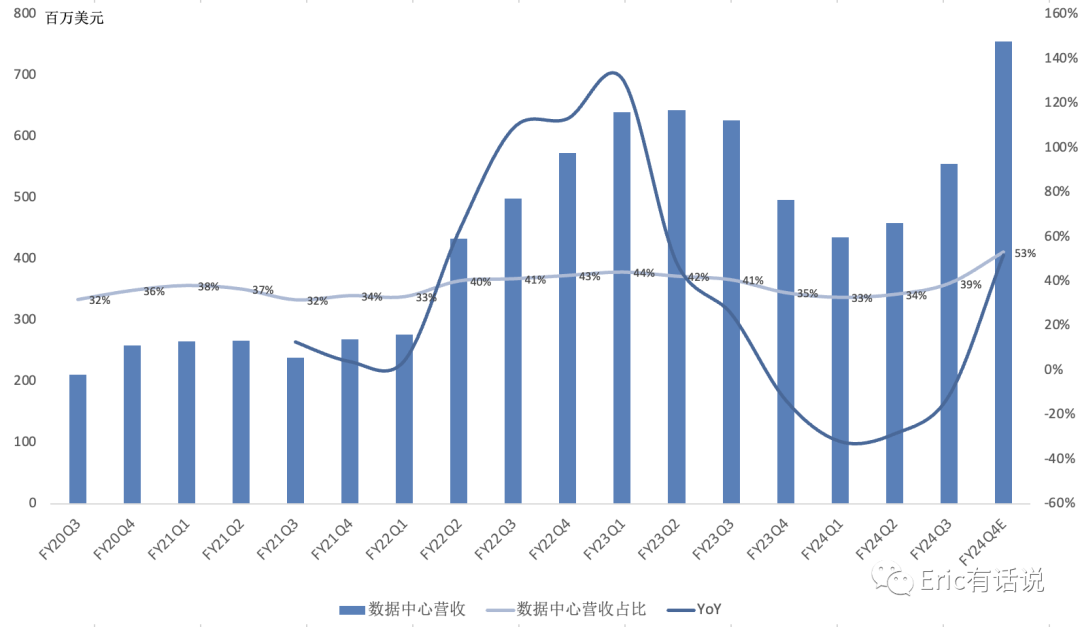

Data center revenue $560M, down 11% year over year, 39% of revenue; AI revenue beat expectations; Q4 AI revenue expected to exceed $200M, annualized run rate over $800M; prior management guidance was $400M AI revenue for the year, almost all optical products; FY25 AI revenue expected to be significantly larger than the $800M run rate, but management cannot provide specific guidance on magnitude or custom silicon scale.

Cloud revenue grew over 30% sequentially, with both AI and non-AI growing sequentially, AI faster; growth driven by PAM4 optical products, Teralynx Ethernet switches, data center interconnects; 800G PAM optical product demand strong; 1.6T PAM products sampled in April, customer qualification underway, volume production planned for next year; PAM DSP for AEC market ramping next year, primary customers tier-1 cloud; 400G DCI modules continue to ramp; custom silicon ramping next year.

Enterprise networking revenue $270M, down 28% year over year, 19% of revenue; industry demand weak, still digesting inventory.

Carrier infrastructure revenue $320M, up 17% year over year, 22% of revenue; wired market remains weak, growth entirely from wireless; but with first wave of 5G deployment complete, Q4 will begin to decline; long term, data traffic continues to grow, wired and wireless capex will return to normal levels; company will benefit long term from market share gains and 5nm baseband chip design wins pending delivery; recovery will come but needs time.

Consumer revenue $170M, down 5% year over year, 12% of revenue.

Automotive/industrial revenue was $110M, up 27% year over year, accounting for 8% of revenue.

Outlook:

Q4 data center revenue overall is expected to grow mid-30s% sequentially, with cloud and AI revenue growing sequentially and AI growing faster.

Q4 carrier infrastructure revenue expected to decline mid-40% sequentially, both wireless and wired down sharply.

Q4 enterprise networking revenue expected to decline mid-single digits sequentially.

Q4 automotive/industrial revenue expected to decline 20% sequentially; industrial aerospace/defense demand declining.

Q4 consumer revenue expected to decline mid-teens sequentially.

Q1 next year expected to see continued weakness in enterprise networking and carrier infrastructure; consumer revenue to decline sharply due to seasonality and Q4 end-of-life program deliveries, but management says it will eventually recover.

In the previous 'Earnings' article, we noted 'At the peak of the last storage cycle, Marvell's Non-GAAP net income TTM was $1.8B (current market cap $47B, ~26x PE). But the first three quarters of this year are ~$900M, full year at most $1.3B.' Currently full year is indeed $1.3B, but the issue is management is only optimistic about next year's AI performance; when asked about traditional business recovery, they lacked conviction. Even whether Q1 next year AI growth can offset traditional business decline (~50% of revenue), management would not commit. Probability of significant overall revenue growth next year appears low. Per management, need to wait until Q1 next year to assess.

Overall, Marvell's earnings are awkward: AI business is growing but offset by traditional business declines; traditional weakness (mainly carrier infrastructure and enterprise networking) exceeded market expectations, raising concerns about Broadcom's post-VMware-acquisition performance, as Broadcom last quarter also had AI growth but traditional stagnation.

On AI, I maintain my prior view: Marvell's AI earnings realization is premature; its AI benefit is still less than Broadcom's.