Marvell's earnings bring the global semiconductor reality into sharper focus: aside from AI, nothing has rebounded; it has merely bottomed.

Marvell FY24 Q2 Earnings:

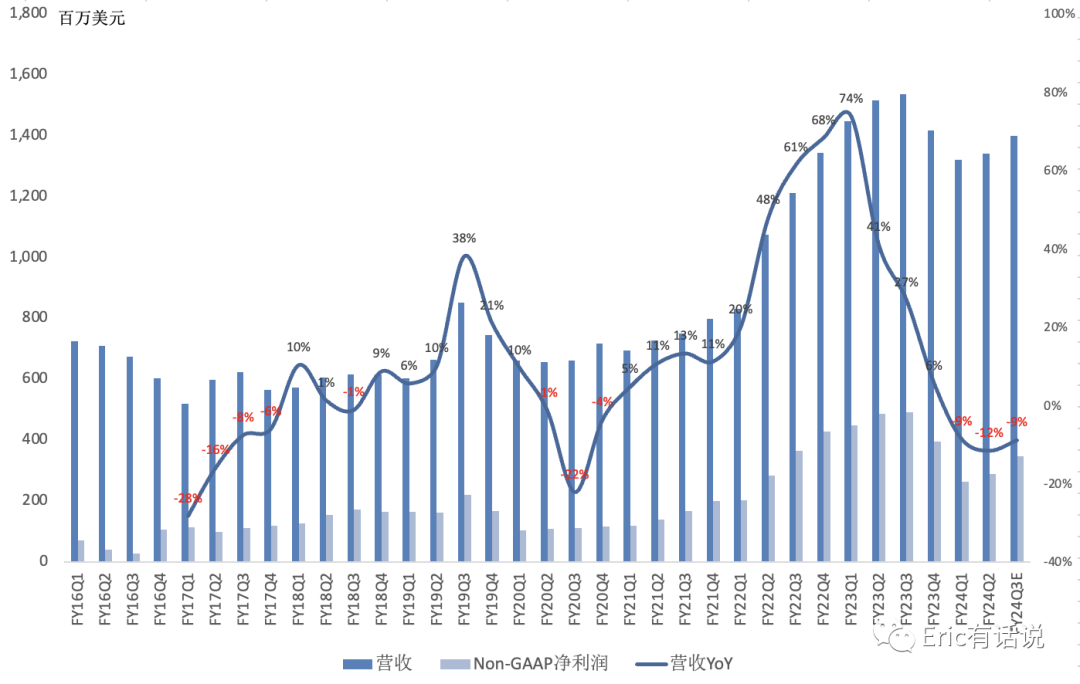

Revenue was $1.341B, down 12% year over year, marking the second consecutive quarter of year-over-year decline, and up 2% sequentially.

GAAP gross margin was 46.8%, down 5 percentage points year over year and up 1.7 percentage points sequentially; non-GAAP gross margin was 61%, down 4.5 percentage points year over year and up 1 percentage point sequentially.

Non-GAAP operating income was $360M, down 35% year over year and up 8% sequentially; non-GAAP operating margin was 26.9%.

Non-GAAP net income was $290M, down 40% year over year and up 10% sequentially; non-GAAP net margin was 22%.

GAAP days in inventory was 114 days, down 7 days sequentially, marking the second consecutive quarter of sequential decline.

Mainland China accounted for 42% of revenue, the US 15%, Finland 9%, Thailand 6%, Singapore 5%, Taiwan 4%, Malaysia 3%, and Japan 3%.

On the product front in Q2: the 800G optical module DSP Orion was launched, paired with a 5nm 112G SerDes; the industry's first 800G DCI ZR module, COLORZ 800, was released with integrated Orion DSP, supporting 51.2T switches; in copper connectivity, the industry's first 5nm multi-gigabit PHY platform was launched for the growing enterprise networking market; in automotive, the Brightlane Ethernet switch with 90Gb/s bandwidth was introduced.

By business, Q2:

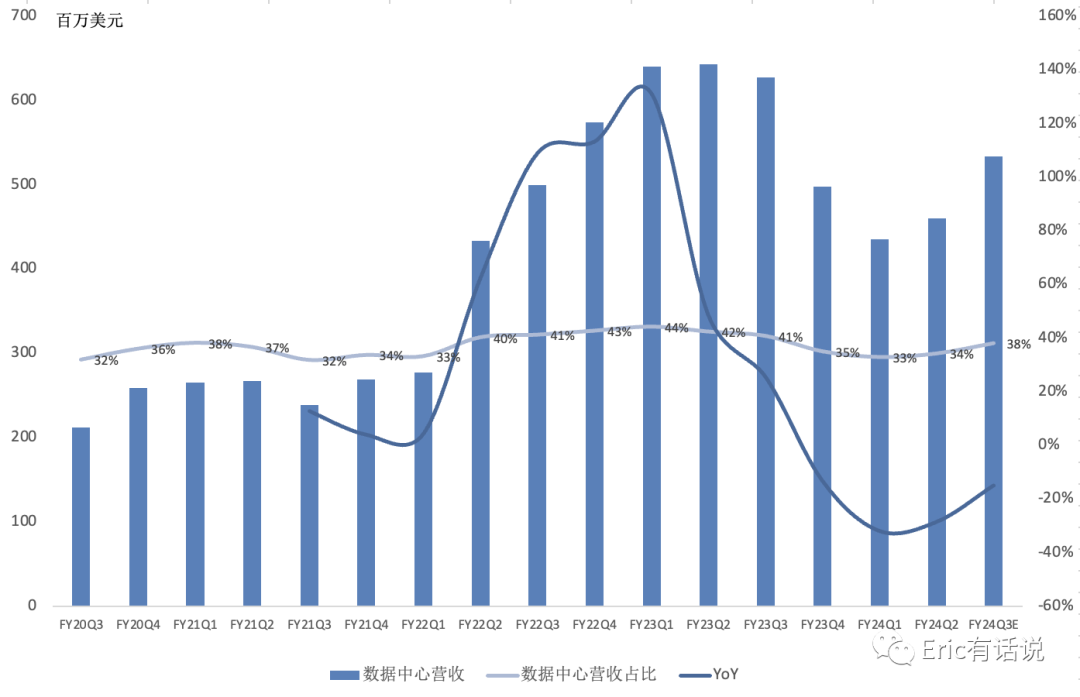

Data center revenue was $460M, down 29% year over year, representing 34% of revenue; optical product demand was strong, with cloud revenue up over 20% sequentially, driven by both cloud AI and standard cloud; enterprise on-premise revenue declined sharply sequentially as enterprise demand remains weak; storage revenue grew sequentially, at a scale of roughly $100M, but end demand remains soft and customer inventory levels remain high.

Enterprise networking revenue was $330M, down 4% year over year, representing 24% of revenue; the enterprise networking market is still digesting inventory.

Carrier infrastructure revenue was $280M, down 3% year over year, representing 21% of revenue; the wired market remains soft as customers digest inventory; the wireless market continues to grow, contributing 25%+ of the sequential growth.

Consumer revenue was $170M, up 2% year over year, representing 13% of revenue.

Automotive/industrial revenue was $110M, up 32% year over year, representing 8% of revenue; automotive revenue continues to grow year over year, with Ethernet design wins from top-10 automotive OEMs increasing.

Outlook:

Q3 data center revenue overall is expected to grow mid-teens sequentially, with storage growing sequentially, cloud revenue accelerating sequentially, and enterprise on-premise revenue continuing to decline.

Q3 carrier infrastructure revenue is expected to decline low-single-digits sequentially; wireless will accelerate, but will decline sharply sequentially in Q4.

Q3 enterprise networking revenue is expected to decline low-teens sequentially.

Q3 automotive/industrial revenue is expected to be flat sequentially and grow roughly 30% year over year.

Q3 consumer revenue is expected to grow low-teens sequentially.

Storage recovery is progressing slower than expected, now anticipated in H1 next year; it still needs to be monitored, but will eventually recover.

At the peak of the last storage cycle, Marvell's TTM non-GAAP net income reached $1.8B (current market cap $47B, ~26x P/E). For the first three quarters of this year it is roughly $900M, with full year at most $1.3B. The company is optimistic about next year, driven by a storage recovery plus AI ramp.

Turning to the market's top focus, AI: this quarter AI demand exceeded expectations; Q4 AI revenue is expected to be $200M, annualizing to $800M, mostly from optical products, with custom silicon still minimal and ramping mainly next year; next year AI revenue will be significantly higher than the previous $800M guide; current AI shipments are primarily 800G DSPs, with 1.6T coming next year, while sub-800G products serve traditional cloud and are also showing signs of recovery; custom silicon carries lower gross margins.

Overall, Marvell's earnings bring investors back to semiconductor reality: traditional semiconductor companies remain weak, with revenue declining year over year for a third consecutive quarter, and the flagship data center business posting double-digit year-over-year declines for a third straight quarter. I maintain my prior view: Marvell's AI earnings realization is still early, and its AI benefit is not yet on par with Broadcom's.