Broadcom's FY25Q1 covers November 2024 through January 2025.

Broadcom FY25Q1 Results:

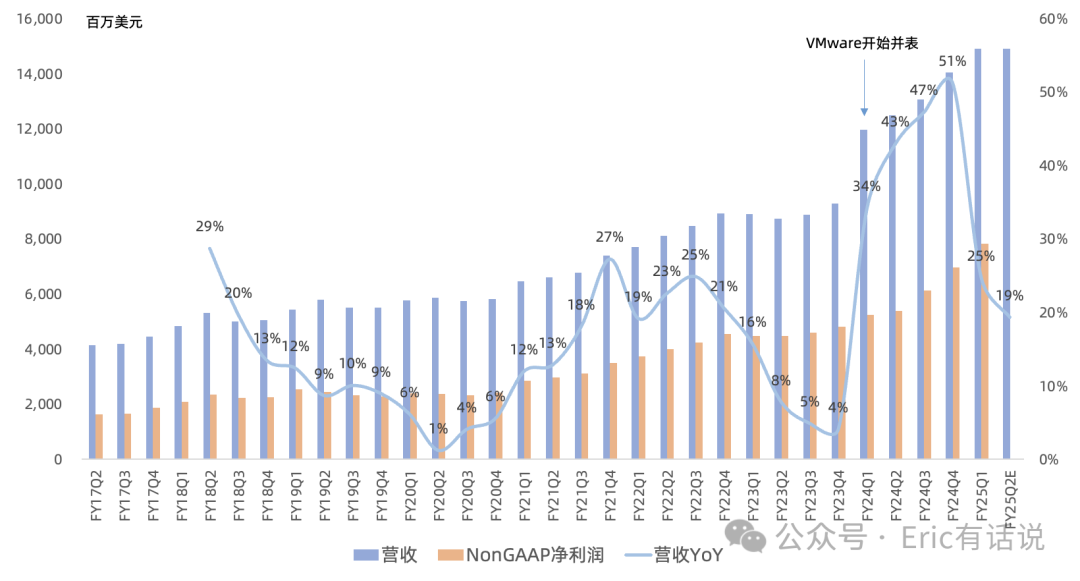

Revenue $14.916B, up 25% year over year, up 6% sequentially, a new all-time high;

GAAP gross margin 65%, operating margin 42%; Non-GAAP gross margin 79%, operating margin 66%;

GAAP net income $5.503B, up 56% year over year; Non-GAAP net income $7.823B, up 63% year over year, up 12% sequentially, a new all-time high, Non-GAAP net margin 52% (vs. 50% last quarter);

$2B in share repurchases and $2.8B in dividends this quarter;

By Business, FQ1:

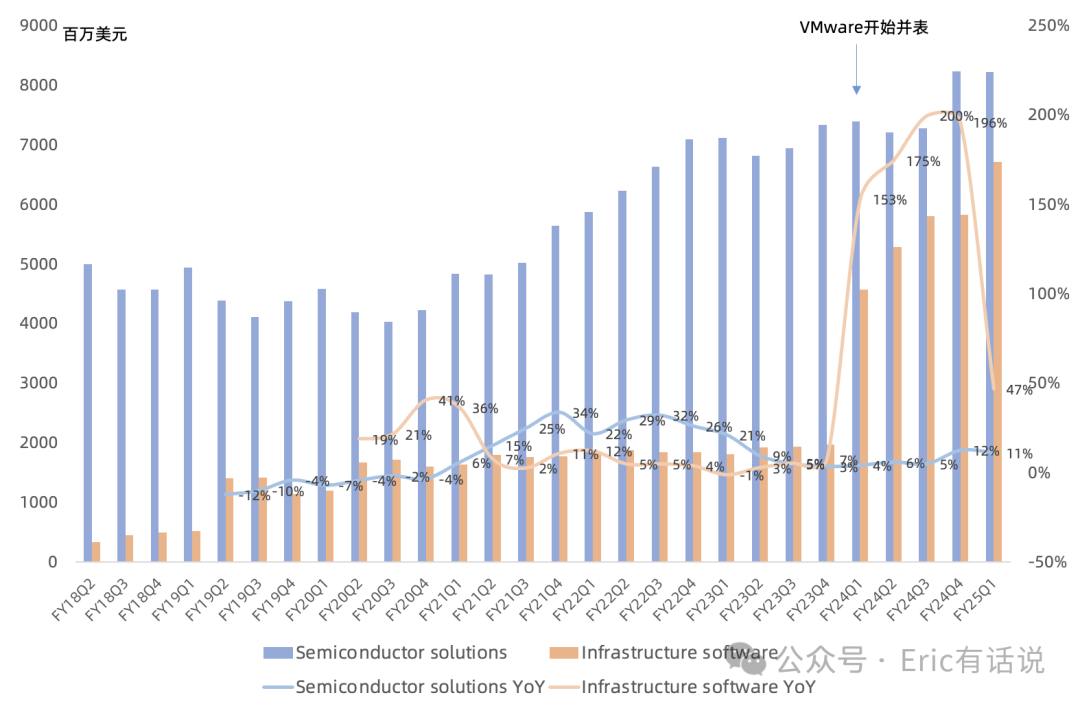

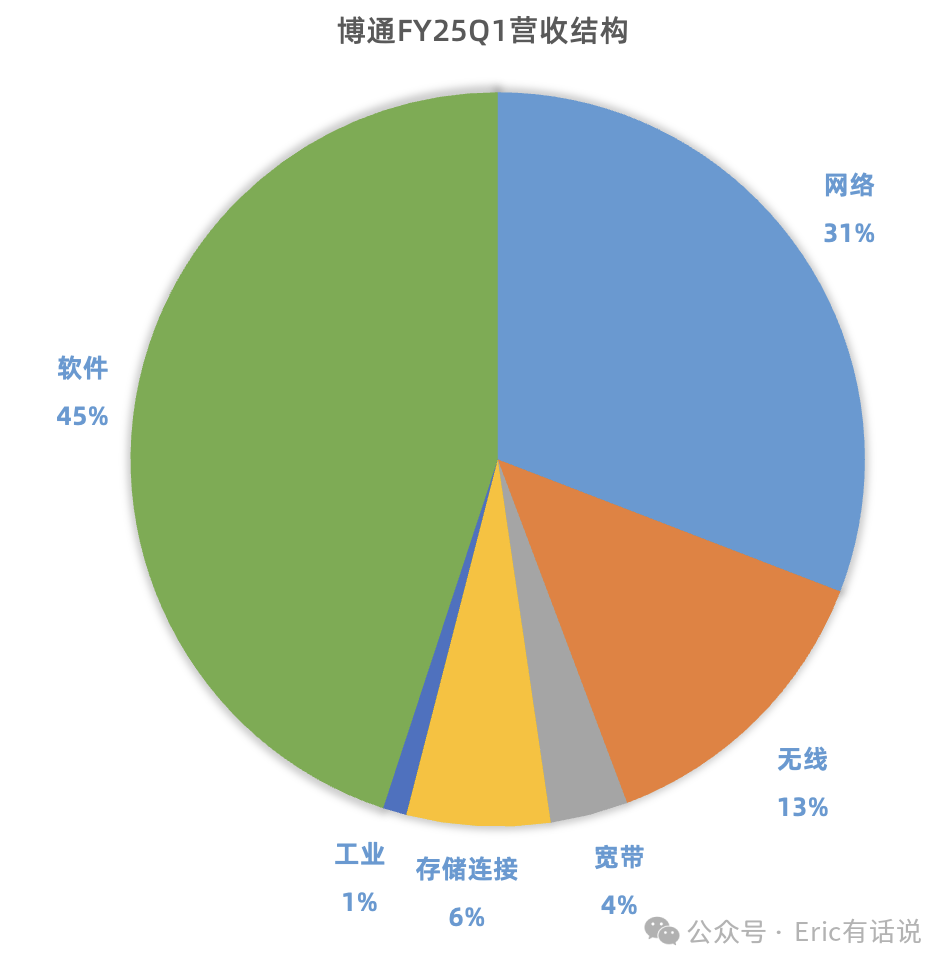

Semiconductor revenue $8.212B, up 11% year over year, revenue share fell to 55%; semiconductor gross margin 68%, up 0.7 percentage points year over year, operating margin 57%;

Software revenue $6.7B, up 47% year over year, revenue share rose to 45%; VMware subscription transition progressing well, now 60% converted to subscription; ~70% of top 10,000 customers subscribe to full-stack VCF; Q2 software revenue guided to $6.5B, up 23% year over year; (note: this earnings release did not directly disclose VMware revenue scale)

Semiconductor Segment Detail FQ1:

Broadband recovered double-digits sequentially; Q2 growth expected in line with Q1 as carriers begin spending;

Server storage down single-digits sequentially; Q2 guided up high-single-digits sequentially; enterprise networking revenue flat in FY25H1 as customers continue destocking;

Wireless down sequentially but flat year over year; Q2 guided flat year over year;

Industrial revenue down double-digits sequentially; Q2 expected to continue declining; (note: this earnings release did not directly disclose revenue by segment for the first time)

AI Exposure FQ1:

Semiconductor AI revenue $4.1B, up 11% sequentially, only $300M above prior guidance, representing 50% of semiconductor revenue; growth driven primarily by networking chips; this quarter custom AI chips and networking chips split 60%/40% ($2.46B/$1.64B, versus Marvell's ~$700M custom AI chip revenue in the same quarter); networking chips may settle at ~30% long-term; semiconductor non-AI revenue $4.1B, down 19% year over year, declining for multiple consecutive quarters, dragged down by the smartphone market;

Guiding FY25Q2 semiconductor AI revenue $4.4B, up 7% sequentially; non-AI semiconductor recovery slow, guiding Q2 non-AI semiconductor revenue flat sequentially, though bookings continue to grow year over year;

Broadcom's custom AI chip exposure is concentrated in three hyperscalers (Google, Meta, ByteDance); this quarter, beyond the two new partners added last quarter (OpenAI, rumored Apple), two more partners were added;

Taping out the industry's first 2nm 3.5D-packaged XPU, targeting 10 PFLOPS; aiming to build 500k-card clusters; 1.6T Tomahawk 6 switch chip taping out, customer samples in coming months; custom AI chip customer production typically takes 6-12 months; per-customer volume no less than 5,000 cards; will not choose startups as customers; Broadcom ASICs lean more toward training, with inference present but a lower share;

Outlook:

Guiding FY25 Q2 revenue $14.9B, up 19% year over year, of which semiconductor revenue $8.4B, up 17% year over year, including AI revenue $4.4B, up 42% year over year, non-AI revenue $4.0B, down 2% year over year; software revenue $6.5B, up 23% year over year; gross margin down 0.2 percentage points sequentially; adjusted EBITDA $9.8B;

Not considering acquiring Intel or other companies;

Overall, judging purely from the earnings, Broadcom's report was middling: AI revenue beat guidance by only $300M, and next-quarter AI guidance was also middling, but the market liked the addition of two new ASIC partners.

However, the entire US equity valuation center has shifted down significantly, with some semiconductor names trading in the low-20s P/E, and Broadcom's earnings release is non-linear with considerable uncertainty. Recent acceleration in LLM innovation means how far the ASIC path can run remains to be seen.