Broadcom's FY24Q3 corresponds to May/June/July 2024 results.

Broadcom FY24Q3 Earnings:

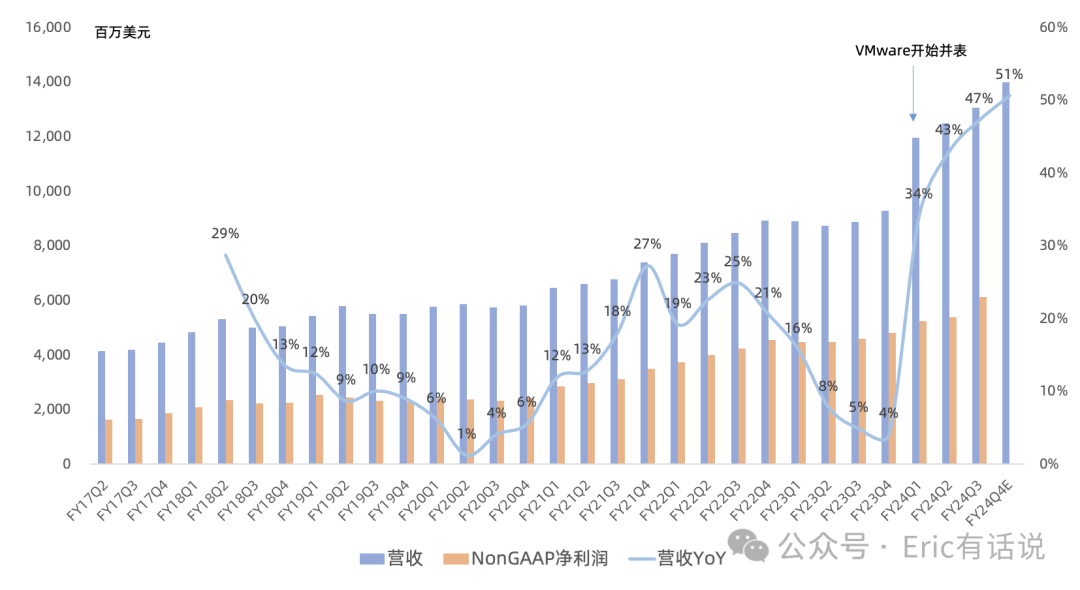

Revenue reached $13.072B, up 47% year over year and 5% sequentially for a fourth straight record quarter; excluding VMware, growth was 4%.

GAAP gross margin 64%, operating margin 29%; Non-GAAP gross margin 77%, operating margin 61%.

GAAP net loss of $1.432B due to a tax adjustment; Non-GAAP net income $6.12B, up 36% year over year and 14% sequentially, marking the 5th consecutive quarter of record highs; Non-GAAP net margin 47% (vs. 43% last quarter).

No share repurchases this quarter; dividends of $2.452B.

By business, FQ3:

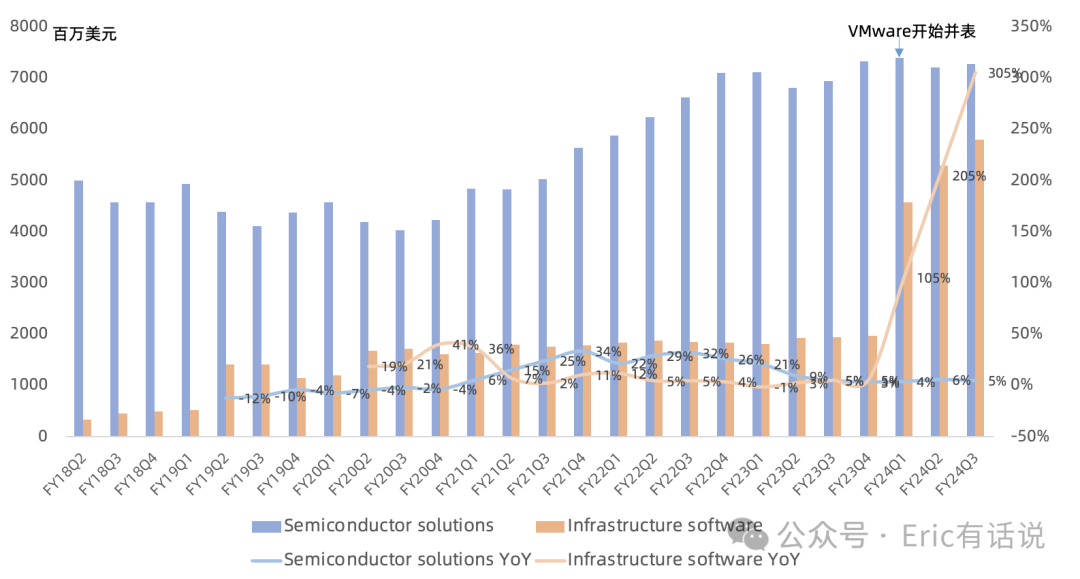

Semiconductor revenue $7.274B, up 5% year over year, marking the 6th consecutive quarter of only single-digit growth; revenue share fell to 56%, a new record low. Semiconductor gross margin 68%, down 2 percentage points year over year due to custom AI accelerators; operating margin 56%.

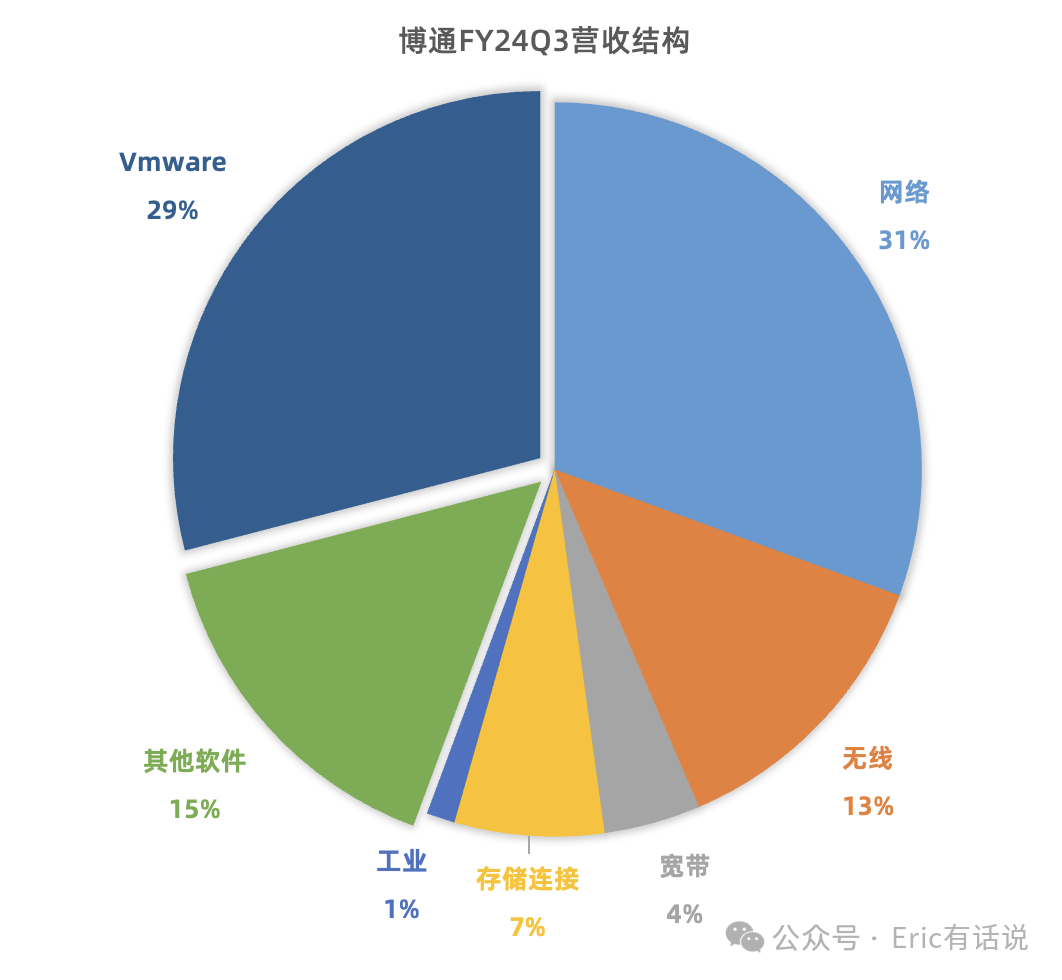

Software revenue $5.8B, up 200% year over year; revenue share rose to 44%, a new record high. VMware contributed $3.8B in revenue; subscription transition progressing well, especially full-stack VCF subscriptions, with strength continuing into FY25. Software gross margin 90%, operating margin 67%, or 69% excluding integration costs. Excluding VMware, software revenue was $2B, up only 5% year over year, and non-VMware software revenue has reached a steady state.

VMware is approaching the quarterly $4B revenue target; Annualized Booking Value rose from $1.9B in FQ2 to $2.5B in FQ3. Future overall software gross margin will stabilize at 90%+.

Semiconductor Segment Detail FQ3:

Networking revenue $4B, up 43% year over year, representing 69% of semiconductor revenue, driven by strong hyperscaler demand for AI networking chips and custom AI chips, the latter up 3.5x year over year. Ethernet switch chips Tomahawk 5 and Jericho 3 up over 4x year over year; PCIe switches up over 2x; 5nm 400G NIC and 800G DSP shipping at scale. Non-AI networking bottomed in FQ2; FQ3 revenue up 17% sequentially but still down 41% year over year. FQ4 revenue expected to hold at this level, down 30% year over year. FQ4 total networking revenue expected up 40%+ year over year.

Notably, per NVIDIA's Q2 earnings (same period as Broadcom FQ3), NVIDIA Q2 networking revenue was ~$3.67B, already far exceeding Broadcom's networking chip portion (~$2B) and approaching Broadcom's total networking revenue. Its Spectrum-X for traditional Ethernet users doubled sequentially in Q2 and is expected to contribute several billion dollars for the full year, far exceeding Broadcom's scale.

Wireless revenue $1.7B, up 1% year over year, 29% of semiconductor revenue. FQ4 revenue expected up 20%+ sequentially, driven by the Apple product launch, but only flat year over year.

Broadband revenue $557M, down 49% year over year, 10% of semiconductor revenue. Telco and service provider business remains weak; FQ4 broadband revenue expected down over 40% year over year; recovery not expected until 2025.

Storage connectivity revenue $861M, down 25% year over year, 15% of semiconductor revenue. FQ4 storage connectivity revenue expected up mid-to-high single digits sequentially, down high single digits year over year.

Industrial revenue $164M, down 31% year over year, 3% of semiconductor revenue. FQ3 near bottom; FQ4 expected to begin sequential recovery but still down 20% year over year.

Outlook:

FQ4 revenue guided at $14B, up 51% year over year, with semiconductor revenue of $8B, up 9% year over year, and software revenue of $6B. Gross margin down 1 percentage point sequentially; adjusted EBITDA $9B.

FY24 full-year revenue guidance raised from $51B to $51.5B; adjusted EBITDA raised from $31.1B to $31.7B.

AI Exposure:

FQ3 AI revenue $3.1B, flat sequentially, representing 43% of semiconductor revenue, unchanged from last quarter. Within AI revenue, custom AI chips and networking chips split roughly 2/3 and 1/3; same mix expected next quarter. FQ4 AI revenue guided at $3.5B, up over 10% sequentially.

FY24 AI revenue target raised from over $11B to over $12B; FY25 AI revenue expected to remain strong. Company-wide non-AI revenue bottomed in FQ3; bookings up 20%.

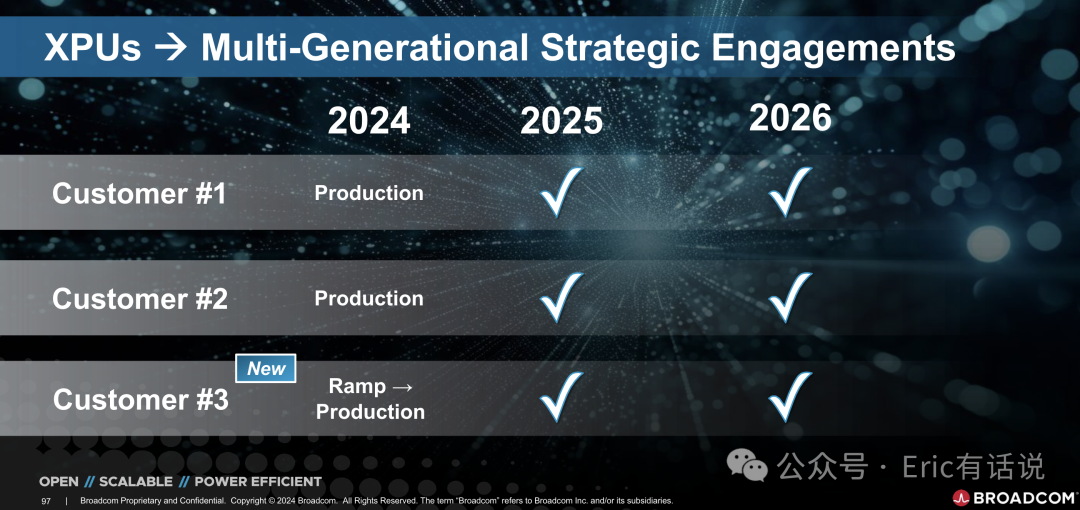

Broadcom's AI revenue exposure is almost entirely concentrated in three large technology giants; enterprise AI involvement is minimal.

Overall, this was a mediocre report. Excluding the consolidated VMware and the AI business, the traditional business recovery is slow and unlikely to return to former peak levels — a cold shower for investors.

Regarding the most-watched AI business, management only raised guidance by $1B, just as AMD only raised by $500M. Notably, Broadcom's FY24 full-year AI revenue guidance of $12B already exceeds AMD's data center revenue guidance of $11B for 23Q4-24Q3. Broadcom's custom AI chip FY24 revenue guidance is roughly $7.2B, also exceeding AMD's full-year data center GPU guidance of $4.5B.

In data center networking chips, Broadcom's dominant position is a thing of the past. Its AI growth now comes mainly from custom AI chips, but NVIDIA may enter that custom chip market in the future — worth monitoring.

On valuation, Broadcom's software business now accounts for nearly half the company, bringing very high margins, but its non-VMware business growth has clearly hit a bottleneck. Conservatively applying a 45% non-GAAP net margin to FY24 revenue of $51.5B yields $23.2B net income. At Broadcom's 5-year average 38x P/E, that implies a market cap of $881.6B, with a path to becoming the third semiconductor company to exceed a $1T market cap. The concern is future revenue growth.