Broadcom FY26 Q1 corresponds to the November/December 2025 through January 2026 period.

Broadcom FY26 Q1 Earnings:

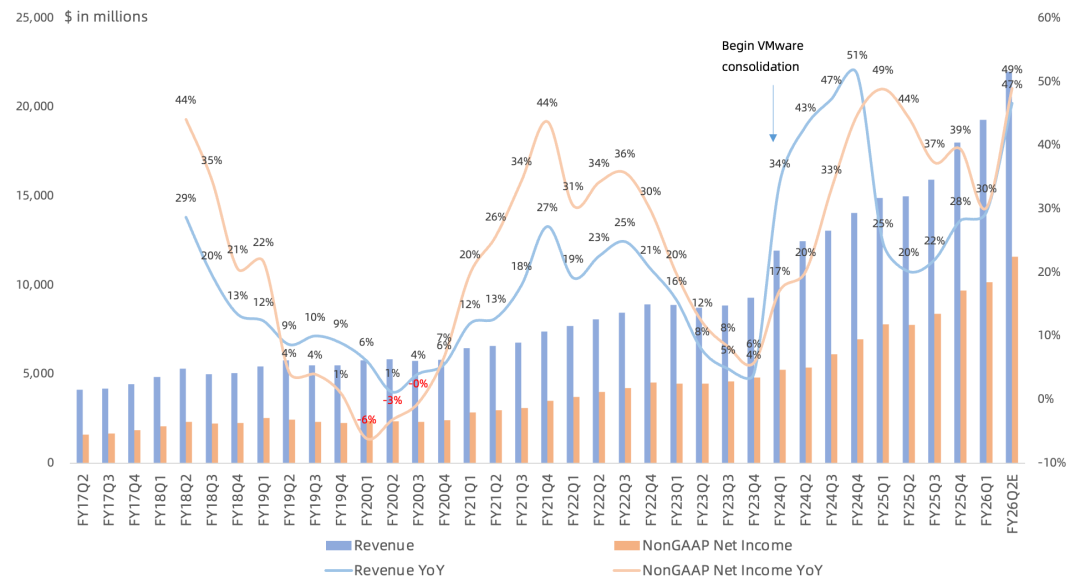

Revenue was $19.31B, up 30% year over year and 7% sequentially, slightly above the consensus estimate of $19.17B.

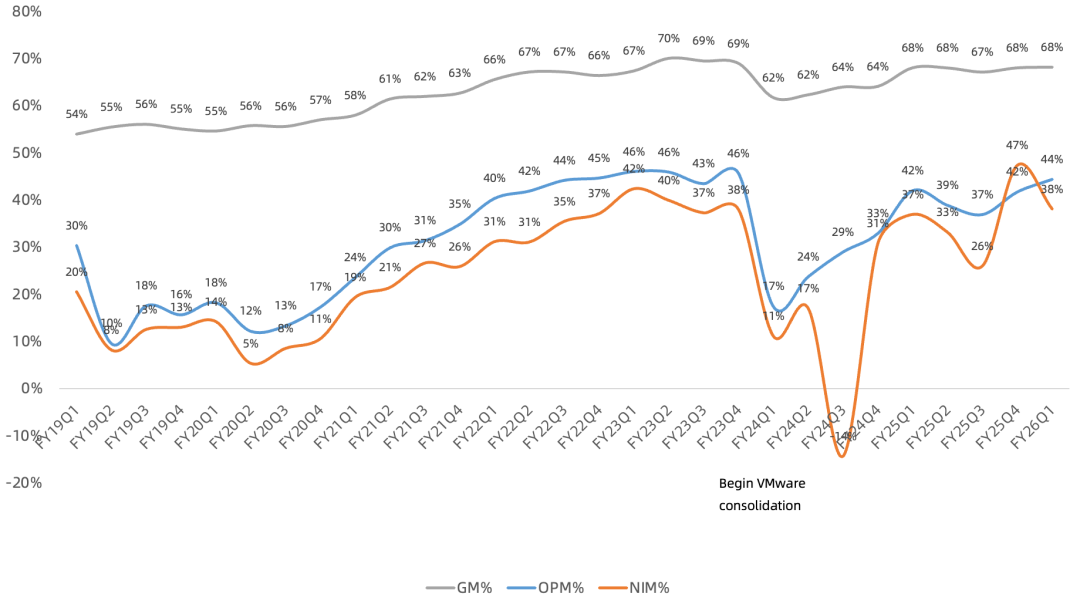

GAAP gross margin was 68.1%, up 0.1 percentage points year over year and sequentially. Operating margin was 44.3%, up 2.3 percentage points year over year and 2.6 percentage points sequentially. Non-GAAP operating margin was 66.4%, up 0.5 percentage points year over year and 0.2 percentage points sequentially.

GAAP net income was $7.35B, up 34% year over year and down 14% sequentially, above the consensus estimate of $7.05B. Non-GAAP net income was $10.19B, up 30% year over year. Non-GAAP net margin was 53% (54% last quarter).

The company finally repurchased $7.85B in shares this quarter, after zero repurchases in the prior two quarters, and announced an additional $10B buyback program. Dividends paid were $3.1B this quarter.

By Business, FQ1:

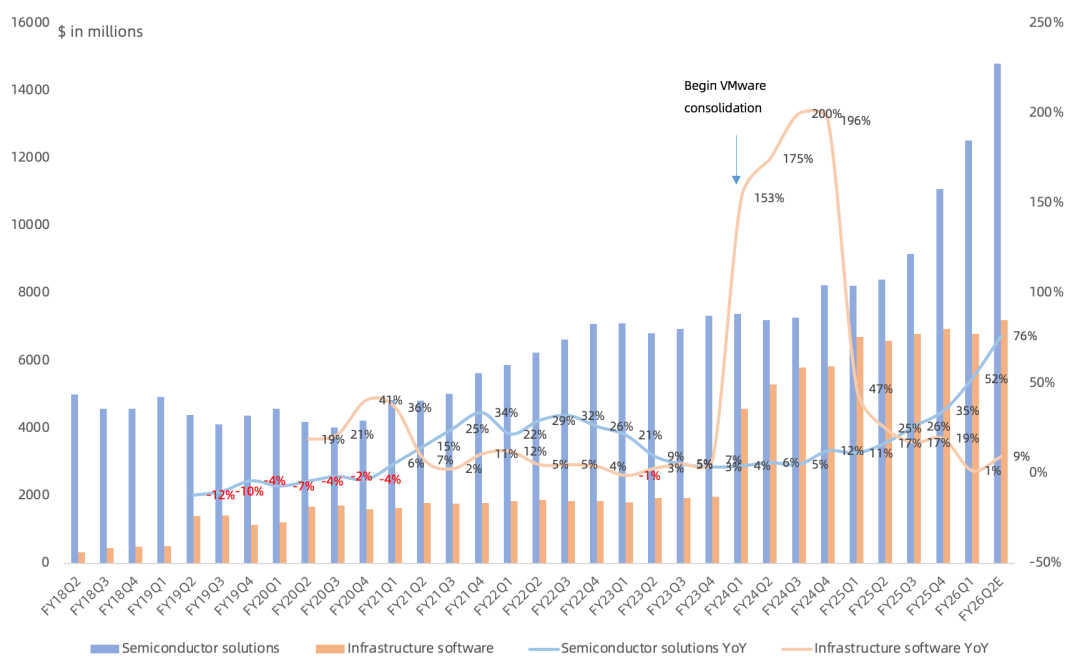

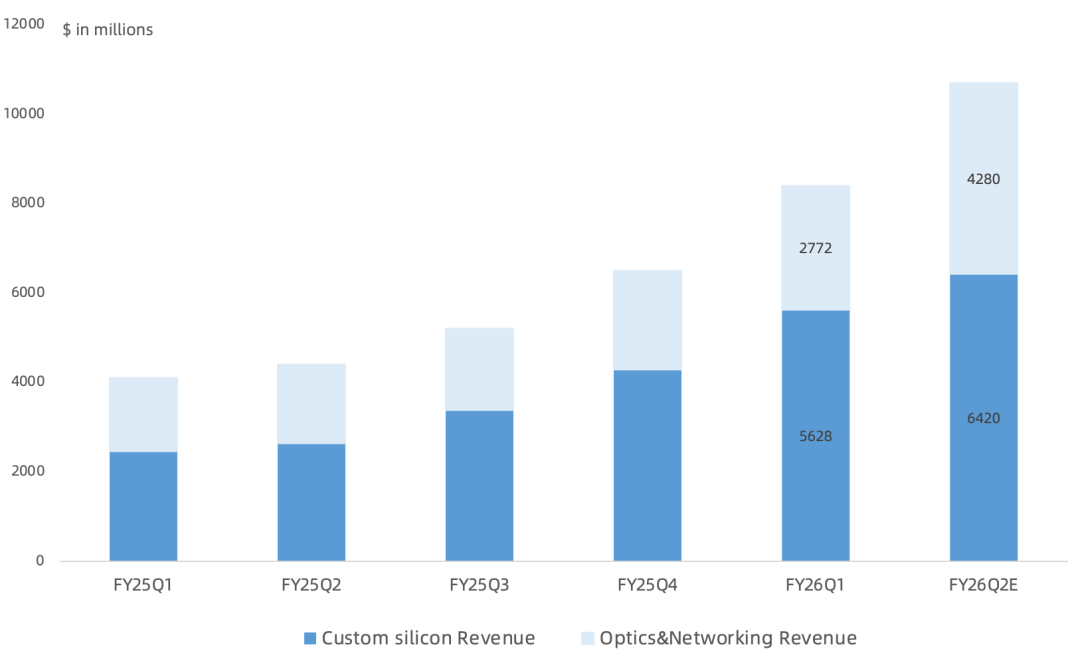

Semiconductor revenue, represented by networking, wireless, broadband, storage connectivity, industrial, and XPU chips, was $12.52B, up 52% year over year, representing 65% of revenue. Semiconductor gross margin was 68%, up 0.3 percentage points year over year; operating margin was 60%, up 2.6 percentage points year over year. FQ2 semiconductor revenue guided at $14.8B, up 76% year over year.

Software revenue, represented by VMware, Symantec, CA, and Brocade, was $6.8B, up 1% year over year, representing 35% of revenue. Software gross margin was 93%; operating margin was 78%, up 1.9 percentage points year over year. VMware revenue grew 13% year over year this quarter; TCV was $9.2B, down $1.2B sequentially. On market concerns about AI displacing software, management explicitly stated Broadcom's infrastructure software business is not being replaced or disrupted by AI; VCF cannot be bypassed or replaced, and generative AI and Agentic AI growth will stimulate more VMware demand. FQ2 software revenue guided at $7.2B, up 9% year over year. (VMware revenue scale no longer disclosed separately since FY25 Q1.)

Semiconductor Detail, FQ1: (Note: Since FY25 Q1, segment revenue is no longer disclosed; only semiconductor AI and non-AI are reported.)

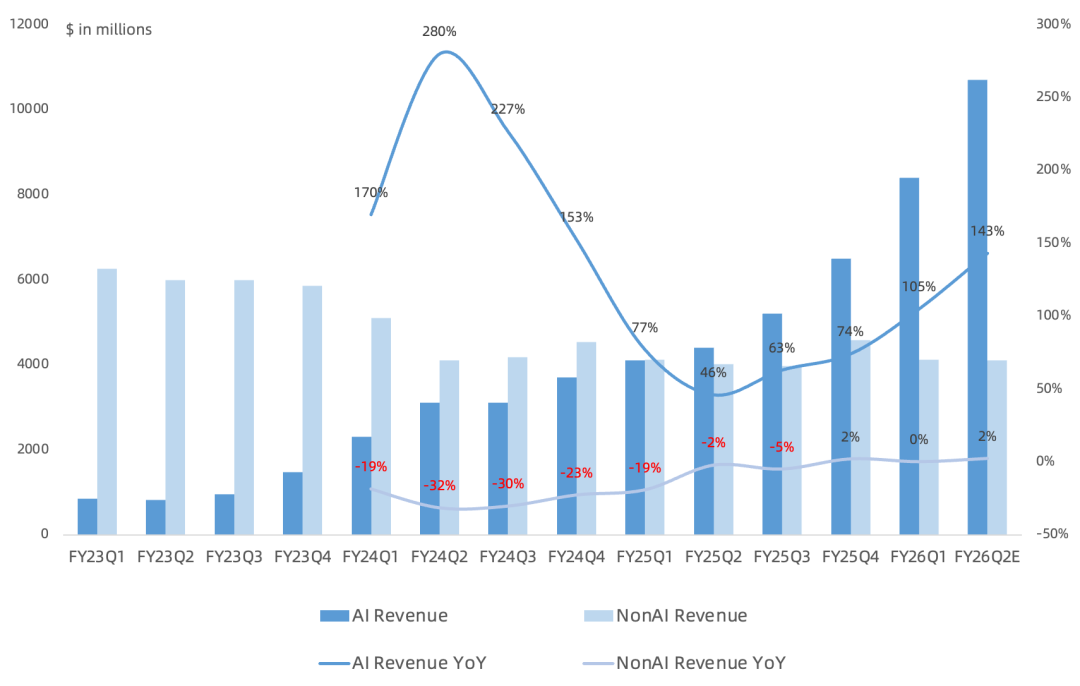

Semiconductor AI revenue was $8.4B, up 105% year over year and 25% sequentially, slightly above prior guidance of $8.2B, representing 67% of semiconductor revenue. Custom XPU revenue was approximately $5.6B, doubling year over year.

Broadcom's six major XPU chip customers publicly confirmed are Google, Meta, Anthropic, and OpenAI; ByteDance and Apple are the two rumored additional customers. Custom AI accelerator ramps are progressing very well across these customers. Google TPU v7 Ironwood demand is strong, expected to maintain growth trajectory in 2026, with next-gen TPU demand expected to be even stronger in 2027 and beyond. Anthropic has 1 GW demand in 2026 and 3+ GW in 2027 and beyond. Meta's MTIA roadmap is on track, with shipments underway; next-gen MTIA in 2027 expected to scale to multiple GW. For the other two customers (market speculation: ByteDance and Apple), 2026 shipments are very strong, and 2027 is expected to more than double on that base. OpenAI is expected to begin large-scale deployment of its first-gen XPU in 2027, corresponding to 1+ GW of compute.

Ethernet-based AI networking chip revenue was under $2.8B (NVIDIA's AI networking revenue exceeded $10B this quarter, shipped primarily as full server systems, while Broadcom ships in chip form). AI networking chip revenue accounts for one-third of AI revenue.

On the scale-out networking side, the Tomahawk 6 switch chip delivers 100 Tbps bandwidth, combined with 200G SerDes; this leadership will extend through 2027, when Tomahawk 7 will double performance again. In scale-up, as cluster and customer scales expand, 200G SerDes enables customers to continue using direct-attach copper cables (DAC). By 2028, upgrading to 400G SerDes, XPU customers will likely still remain on direct-attach copper solutions, as the optical interconnect alternative is higher cost and significantly higher power. FQ2 AI networking revenue is expected to accelerate further, rising to 40% of total AI revenue. Long-term, AI networking revenue share is expected to fluctuate between 33% and 40%.

Semiconductor non-AI revenue was $4.1B, flat year over year. Enterprise networking, broadband, and server storage grew year over year but were offset by seasonal decline in wireless.

Outlook:

FY26 Q2 revenue guided at $22B, up 47% year over year. Semiconductor revenue guided at $14.8B, up 76% year over year, of which AI revenue guided at $10.7B, up 140% year over year, and non-AI revenue guided at $4.1B, up 2% year over year. Software revenue guided at $7.2B, up 9% year over year. Gross margin guided flat sequentially; adjusted EBITDA margin guided at 68%.

Management continued to near-term "talk down CPO," stating CPO will arrive in its own time, but not this year, and maybe not next year either.

Management expects FY27 AI chip revenue (including XPU and networking chips) to exceed $100B, and stated that all critical component capacity needed for FY26 through FY28 has been locked in.

Management believes FY28 can still deliver growth. Dollar value per GW varies by customer and can differ significantly. Based on 2027 GW figures, the total is approaching 10 GW.

Market concerns that CSPs and hyperscalers are advancing their own internal XPU/TPU designs (so-called Customer-Owned Tooling, or COT) to take ASIC share. Management maintains this is unlikely.

Most customers start with inference, as it is often the easiest path; inference requires less compute than training.

Management shifted tone on future gross margins versus last quarter, claiming that as more AI products ship, company gross margin will not be materially dragged down. However, they declined to comment when asked by Wall Street whether Anthropic orders are for rack-level systems.

Overall, the report did not show NVIDIA-style or memory-style explosive growth. The main positive surprise was that gross margin did not decline as the market feared, and management guided FY27 AI revenue above $100B. While this pales next to NVIDIA's $500B+ revenue guidance, it bolstered confidence in ASICs. Broadcom's valuation still exceeds NVIDIA's and other tech giants.

Long term, given that cloud computing is the highest-ROI AI monetization venue, the cloud AI capex pie is large enough, and enterprise and sovereign AI are just beginning, there remains substantial growth runway for all players.

Using the $100B-plus AI revenue framework, I raise my FY27 revenue estimate to more than $145B. At a 53% non-GAAP net margin, that implies over $77B of net income and roughly 20 times FY27 earnings.