The previous Marvell review argued that its AI benefit would take time to reach earnings, while Broadcom's similar portfolio could monetize sooner.

Broadcom FY23 Q2 Earnings:

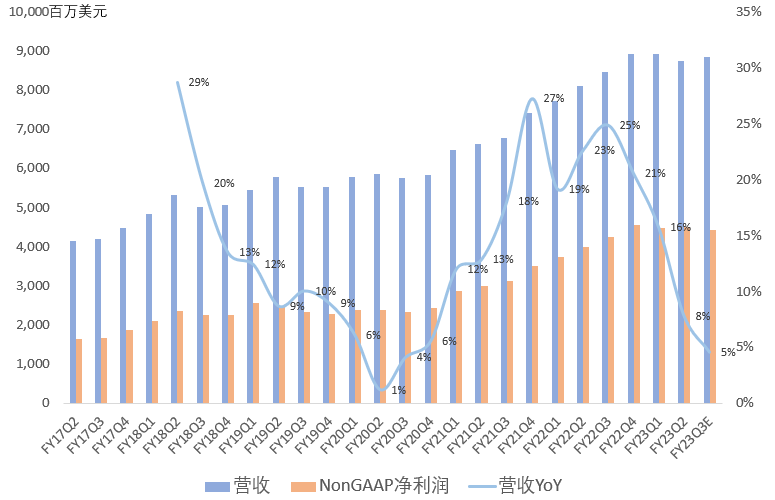

Revenue $8.733B, up 8% year over year, down 2% sequentially; first time since 2020 Q3 year-over-year growth slowed to single digits;

GAAP gross margin 70%, up 2.9 percentage points year over year and 2.7 percentage points sequentially, a record high;

GAAP net income $3.481B, up 45% year over year, down 8% sequentially, GAAP net margin 39.9%; non-GAAP net income $4.489B, up 20% year over year, up slightly sequentially, non-GAAP net margin an extraordinary 51.4%;

$2.8B share repurchases this quarter, $1.9B dividends, $9B repurchase authorization remaining.

Broadcom's net margin is firmly in the top tier of semiconductors (TSMC 41%, Texas Instruments 39%).

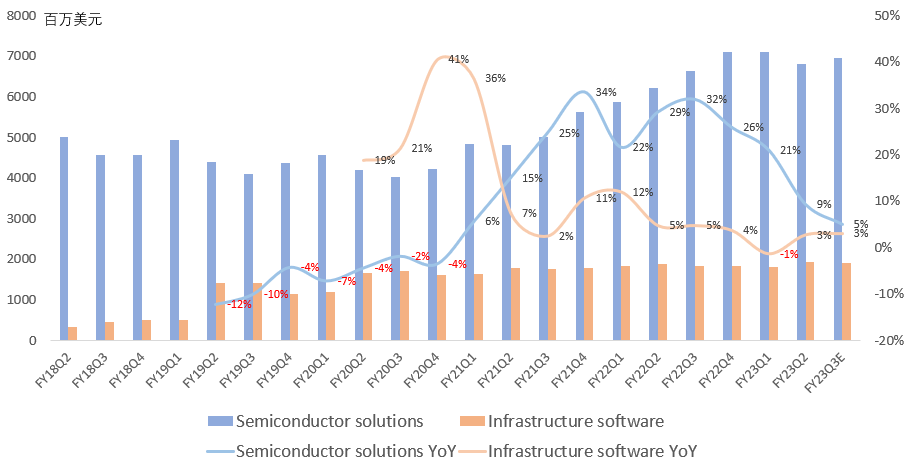

Q2 by Segment:

Semiconductor revenue $6.808B, up 9% year over year, 78% of revenue; infrastructure demand driven primarily by hyperscalers, service providers and enterprise holding back, overall infrastructure demand up mid-teens year over year, growth was 30% for the past five quarters.

Software revenue $1.925B, up 3% year over year, 22% of revenue; core software revenue up year over year, Brocade enterprise and business down year over year; Q2 ARR $5.3B, up 2% year over year.

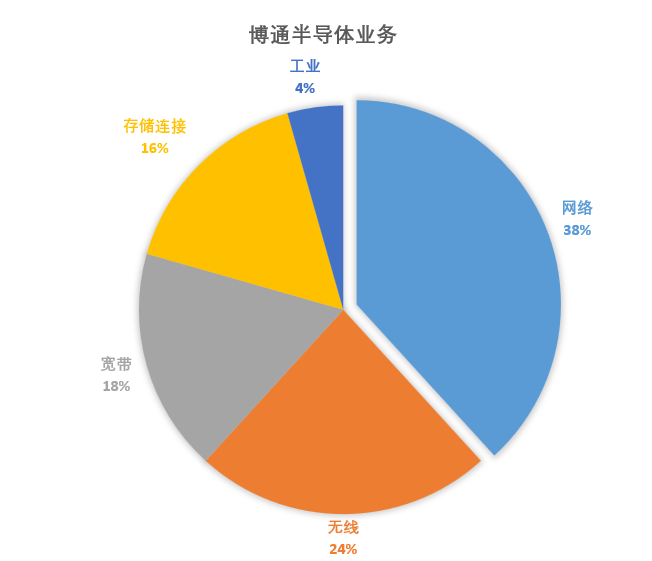

Semiconductor Segment Detail Q2:

Wireless revenue $1.6B, down 9% year over year, 23% of semiconductor revenue; signed wireless connectivity/5G components supply agreement with Apple, not a renewal but an extension;

Networking revenue $2.6B, up 20% year over year, 39% of semiconductor revenue; Tomahawk strong shipments in traditional commercial switching, Jericho strong in telecom routing, hyperscale AI infrastructure compute offload/networking growing strongly;

Broadband revenue $1.2B, up 10% year over year, 18% of semiconductor revenue; growth driven by telco 10G PON demand and WiFi 6/6E driving cable operator demand;

Storage connectivity revenue $1.1B, up 20% year over year, 17% of semiconductor revenue;

Industrial revenue $260M, up 2% year over year, mainly due to weak China demand, but overseas new energy and robotics demand strong;

Outlook:

Q3 wireless revenue expected up low-single-digits sequentially, flat year over year; networking revenue up 20% year over year; broadband revenue up low-single-digits year over year; storage connectivity revenue up low-single-digits year over year; industrial revenue flat year over year, Asia demand remains weak, Europe demand strong; Q3 semiconductor revenue overall up mid-single-digits year over year;

Q3 software revenue expected up low-single-digits year over year; core software sold directly to enterprise, typically multi-year contracts, current backlog ~$17B, average 2.5-3 years;

Primary foundry remains TSMC, will not switch fabs for price;

Inventory levels healthy, DOI under 86 days, consistent with past eight quarters;

VMware acquisition approved by Australia, Brazil, Canada, South Africa, Taiwan; expected to close by end of FY23;

Most product lead times remain around 50 weeks.

AI Revenue Composition:

Broadcom AI revenue currently ~15% of semiconductor revenue, was 10% in FY22, expected to reach 25% in FY24;

FY23 Q4 AI quarterly revenue expected to double year over year;

FY23 custom solutions for compute offload accelerators (ASIC) revenue >$3B, AI Ethernet switching revenue up to $800M; this guidance (given in FY23 Q1) unchanged; implies FY23 AI revenue $3.8B;

AI-related products require over 6 months from production to delivery;

Long-term growth half from traditional business, half from AI;

AI opportunity mainly from networking; networking product growth to exceed offload computing; offload computing currently has one customer, will remain limited to a few customers in the future.

Overall, Broadcom's earnings were decent; AI growing but still small scale, traditional business growth decelerating but moderately, margins remain industry benchmark. Broadcom is one of the few companies to successfully weather the semiconductor downcycle, achieving a so-called soft landing due to sufficiently diversified product exposure.

But this is certainly not the report the market wants; they want NVIDIA-like AI revenue explosion, but there is only one NVIDIA. They seem to have forgotten we are still in a semiconductor downcycle; realize how hard it is for NVIDIA to deliver such results in this environment.

Broadcom's exposure is mostly traditional compute; CEO believes traditional and AI compute will advance in parallel, AI growing faster, not traditional compute disappearing. Future growth half from traditional, half from AI. Feels like Broadcom CEO is still taking a wait-and-see approach.