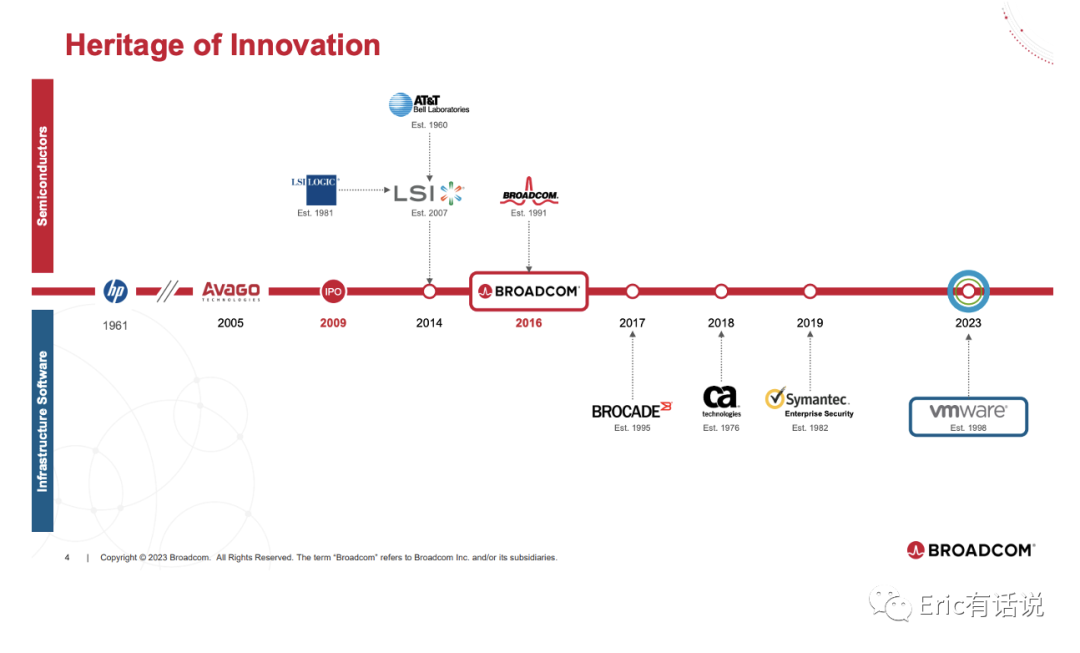

Broadcom FY24Q4 covers August/October 2024 results.

Broadcom FY24Q4 Results:

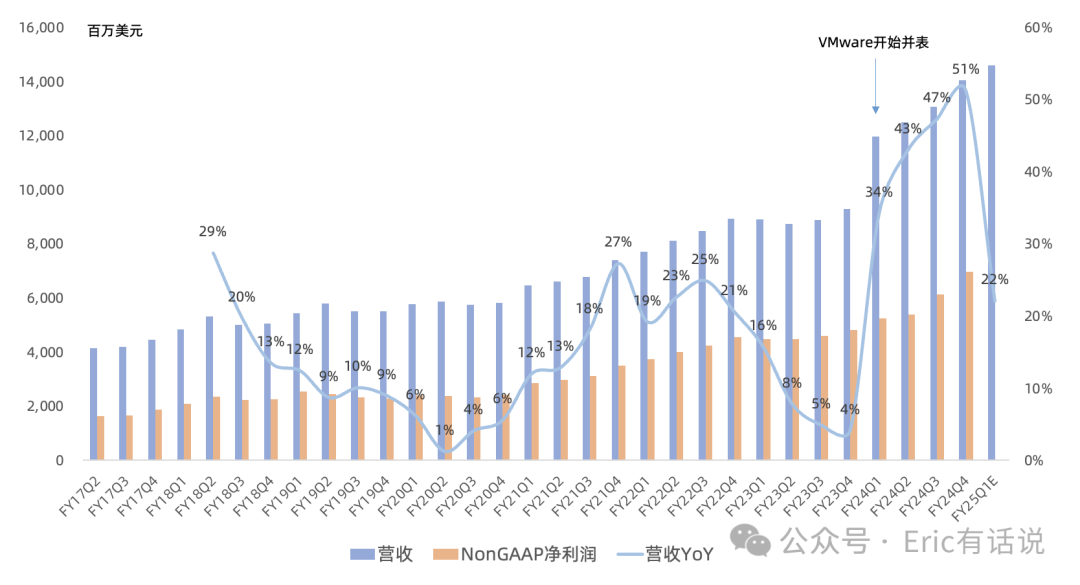

Revenue reached a record $14.054B, up 51% year over year and 8% sequentially; excluding VMware, organic growth was 11%.

GAAP gross margin 64%, operating margin 33%. Non-GAAP gross margin 77%, operating margin 63%.

GAAP net income $4.324B, up 31% year over year. Non-GAAP net income $6.965B, up 52% year over year and 14% sequentially, a new record high. Non-GAAP net margin 50% (vs. 47% last quarter).

$1.2B in share repurchases this quarter; $2.5B in dividends. FY25 dividend expected to increase another 12%.

Segment FQ4:

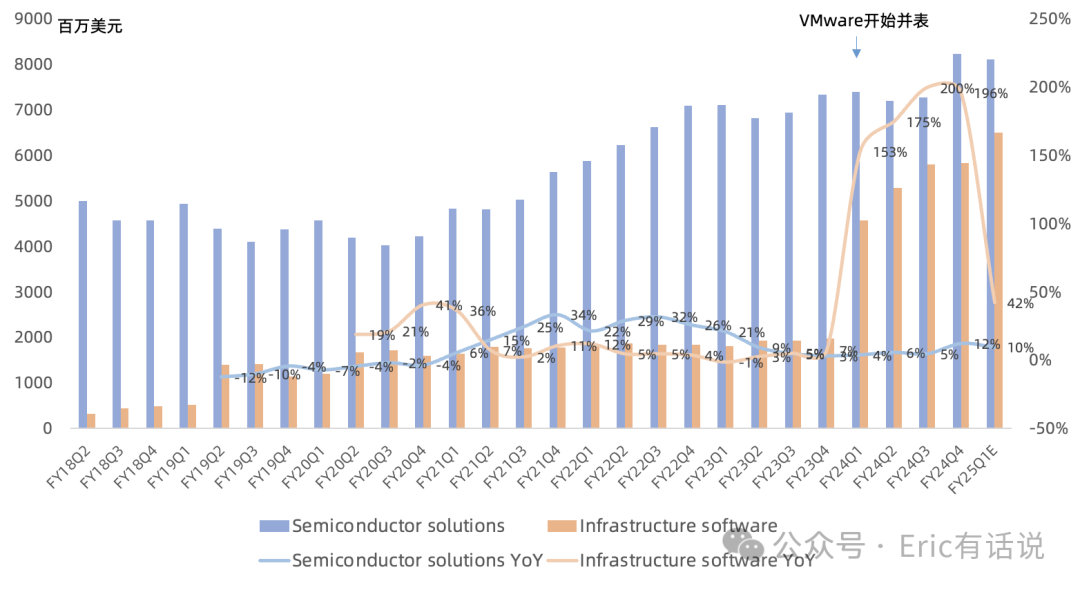

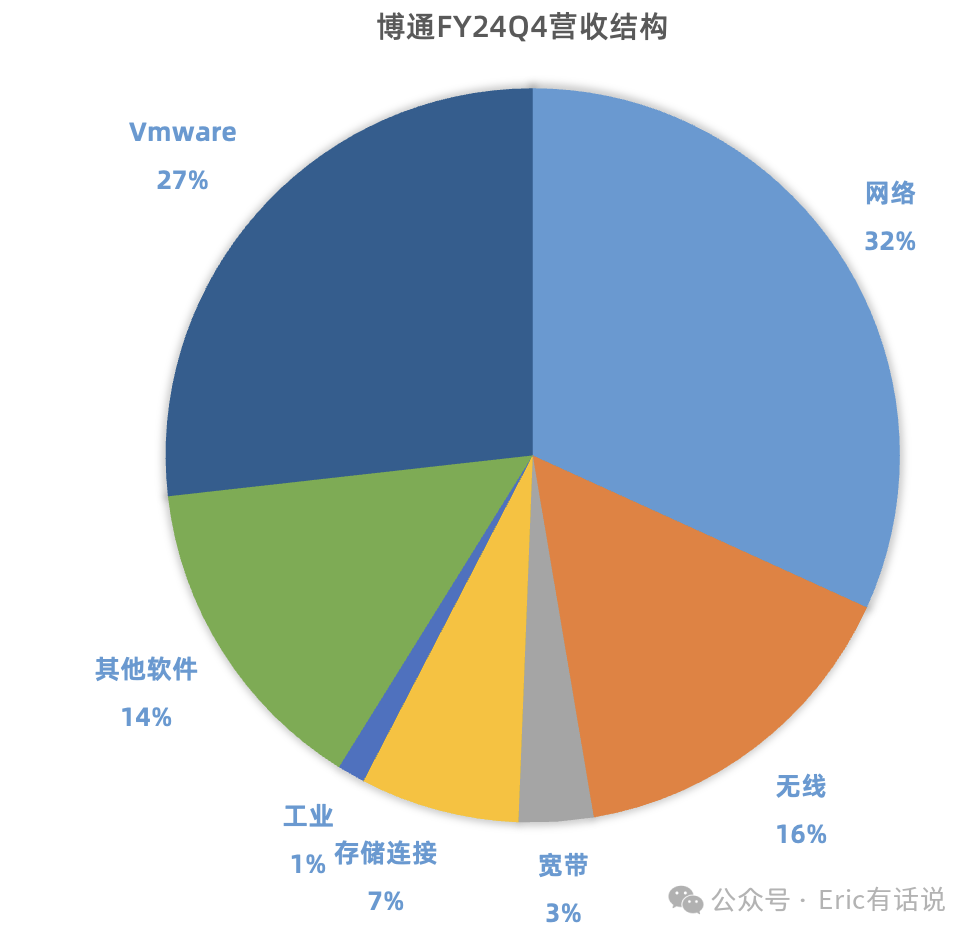

Semiconductor revenue $8.23B, up 12% year over year, rising to 59% of total revenue. Semiconductor gross margin 67%, down 2 percentage points year over year due to custom AI chips. Operating margin 56%.

Software revenue $5.8B, up 196% year over year, falling to 41% of total revenue. VMware contributed $3.8B revenue; subscription transition on track, with >4,500 of top 10,000 customers on full-stack VCF. Momentum continues into FY25. Software gross margin 91%, operating margin 72% (73% excluding integration costs). Excluding VMware, software revenue ~$2B, roughly flat year over year.

VMware Annualized Booking Value rose from $2.5B in FQ3 to $2.7B in FQ4.

Semiconductor Segment Detail FQ4:

Networking revenue $4.5B, up 45% year over year, 55% of semiconductor revenue. Custom AI chip shipments doubled year over year. AI connectivity chips (including Tomahawk 5/Jericho3) grew 4x year over year. FY25Q1 AI connectivity growth expected to remain strong. Ahead of next-gen 3nm custom AI chip shipments in FY25H2, connectivity chip growth will continue to outpace custom AI chip growth.

Wireless revenue $2.2B, up 7% year over year, benefiting from iPhone 16 launch, up 30% sequentially, 27% of semiconductor revenue. FY25Q1 revenue expected to decline sequentially and be flat year over year.

Broadband revenue $465M, down 51% year over year, 6% of semiconductor revenue. Telco/operator orders showing recovery this quarter. FY25Q1 broadband revenue expected to begin recovery.

Storage connectivity revenue $992M, down 1% year over year, 12% of semiconductor revenue. FY25Q1 storage connectivity revenue expected to continue growing sequentially.

Industrial revenue $173M, down 27% year over year, 2% of semiconductor revenue. FY25H2 recovery expected.

Outlook:

FY25Q1 revenue guided at $14.6B, up 22% year over year. Semiconductor revenue $8.1B, up 10% year over year, of which AI revenue $3.8B, up 65% year over year. Non-AI semiconductor revenue down mid-teens% year over year. Software revenue $6.5B. Gross margin up 1 percentage point sequentially. Adjusted EBITDA $9.6B.

FY24 non-AI semiconductor revenue of $17.8B represents a trough; FY25 expected to grow mid-single-digits.

AI Exposure:

FQ4 semiconductor AI revenue $3.7B, up 19% sequentially, only $200M above prior guidance, 45% of semiconductor revenue. Non-AI revenue $4.5B, down 23% year over year. FY24 semiconductor AI revenue $12.2B, $200M above prior guidance.

FY25Q1 semiconductor AI revenue guided at $3.8B, up 3% sequentially. Next-gen 3nm custom AI chips to ship in FY25H2.

By FY27, each of three customers' compute clusters expected to reach 1M custom AI chips. Custom AI chip + networking interconnect SAM at $60-90B, with networking at 15-20% and the rest custom AI chips. Company expects to maintain leading share. For reference, FY24 SAM was $15-20B, implying ~70% share. Scale-up + scale-out trends expected to lift AI networking interconnect value share from 5-10% to 15-20%.

Broadcom's custom AI chip exposure is concentrated in three hyperscalers (Google, Meta, ByteDance). Two new customers added (rumored OpenAI, Apple), shipment timing unknown but before FY27. Custom AI chips do not address Enterprise/Sovereign AI.

Overall, the earnings themselves were unremarkable: AI revenue beat guidance by only $200M, and next-quarter AI guidance was also modest. But the FY27 SAM of $60-90B is a large pie, and the market bought it, as everyone wants to find the next NVIDIA; ASIC attention is at an all-time high.

As noted previously, Broadcom's custom AI chip revenue scale actually far exceeds AMD's data center GPU (Broadcom FY24 ~$8B vs. AMD FY24 ~$5.3B).

Future Broadcom AI growth hinges on custom AI chips, which carry two key uncertainties: ByteDance custom AI chips face export controls, and long-term custom AI chip orders are volatile. Also monitoring rumors of NVIDIA entering the custom AI chip market.

Valuation-wise, since Broadcom has laid out a big vision, let's be optimistic from FY27. Assuming current 70% market share holds, a $60-90B SAM implies $42-63B revenue. Non-AI semiconductor and software growing at 5% CAGR. At 55% Non-GAAP net margin, FY27 net income $48-60B. Implies FY24-FY27 CAGR of 26-36%. FY25 net income $30-32B. At Broadcom's 5-year valuation midpoint of 38x PE, that implies a $1.14-1.23T market cap — officially the third trillion-dollar semiconductor company.

Broadcom's earnings trajectory is not linear and carries significant uncertainty. If ASIC truly explodes in 2027 as Broadcom claims, wouldn't that make TSMC — with its higher certainty — look cheap?