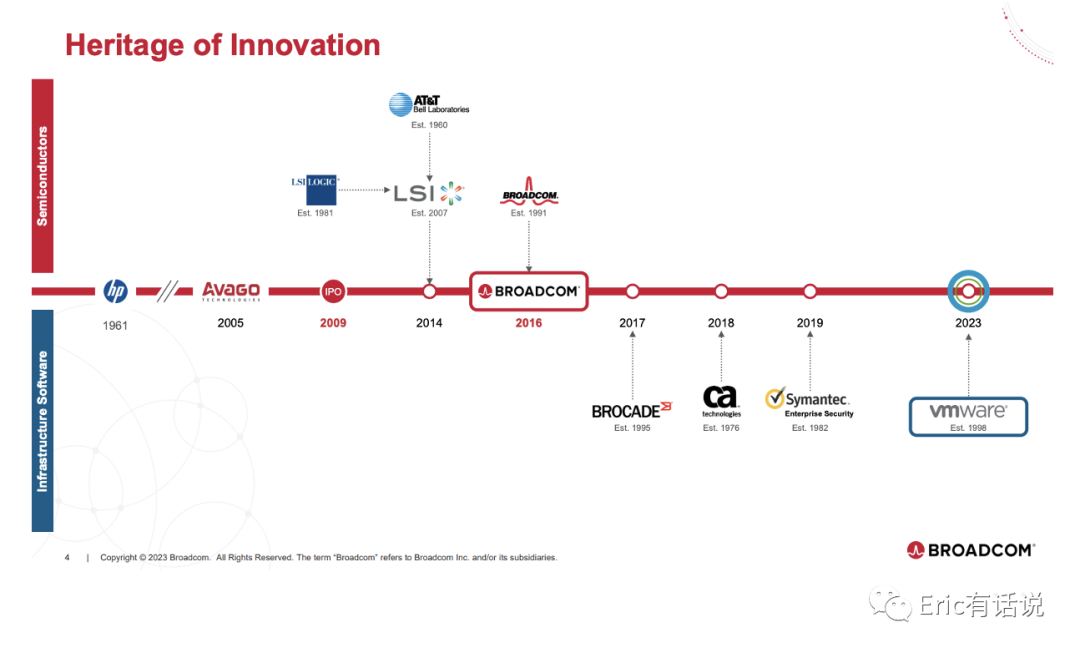

4

Broadcom FY23 Q4 corresponds to August/September/October 2023 results.

Broadcom FY23 Q4 Earnings:

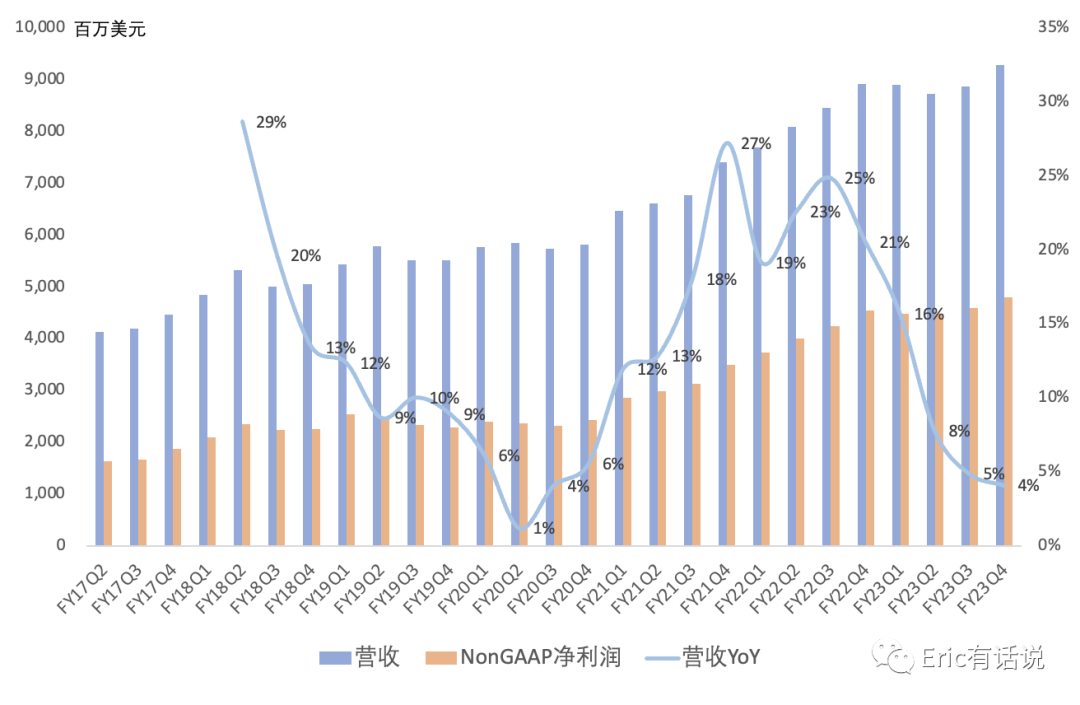

Revenue reached $9.295B, up 4% year over year and 5% sequentially, marking a third straight quarter of single-digit growth.

GAAP gross margin 69%, operating margin 46%, both maintained at historical highs.

GAAP net income $3.524B, up 18% year over year and 7% sequentially; GAAP net margin 37.9%; Non-GAAP net income $4.81B, up 13% year over year and 5% sequentially; Non-GAAP net margin an extraordinary 51.7%.

FY23 share repurchase has 7M shares (approx. $6.3B) remaining unexecuted; the company will continue buybacks.

Broadcom's net margin remains firmly in the semiconductor industry's first tier (NVIDIA 51%, TSMC 39%, Texas Instruments 38%).

By Segment Q4:

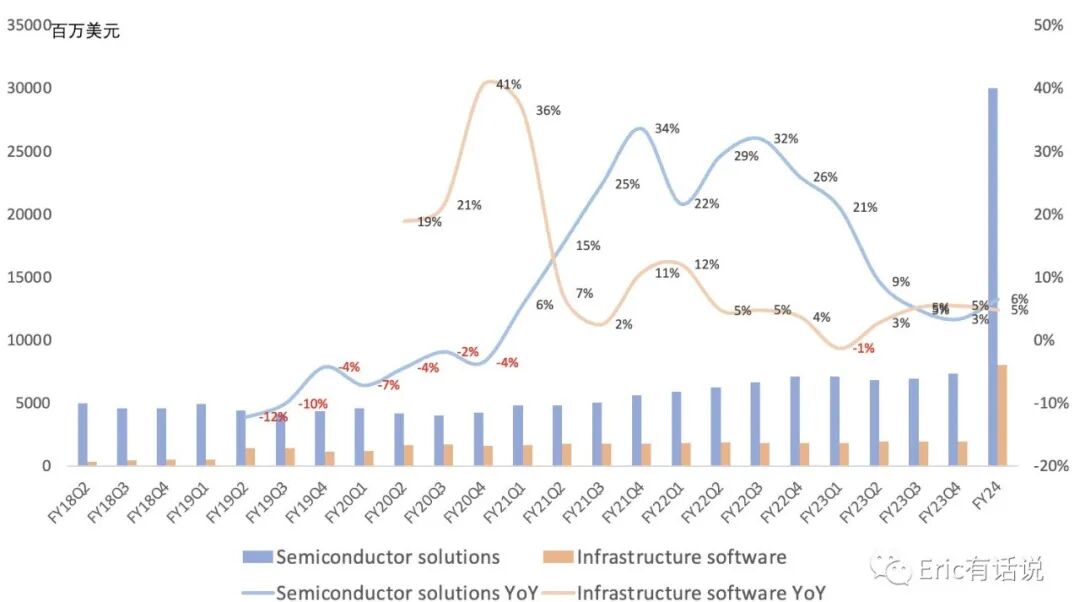

Semiconductor revenue $7.326B, up 3% year over year, 79% of revenue; hyperscalers remain strong, but enterprise and telco remain weak; semiconductor gross margin near 70%, down 1.1 percentage points year over year; operating margin 58%.

Software revenue $1.969B, up 5% year over year, 21% of revenue; software gross margin 92%, operating margin 75%; Q4 ARR data not provided.

Semiconductor Segment Details Q4:

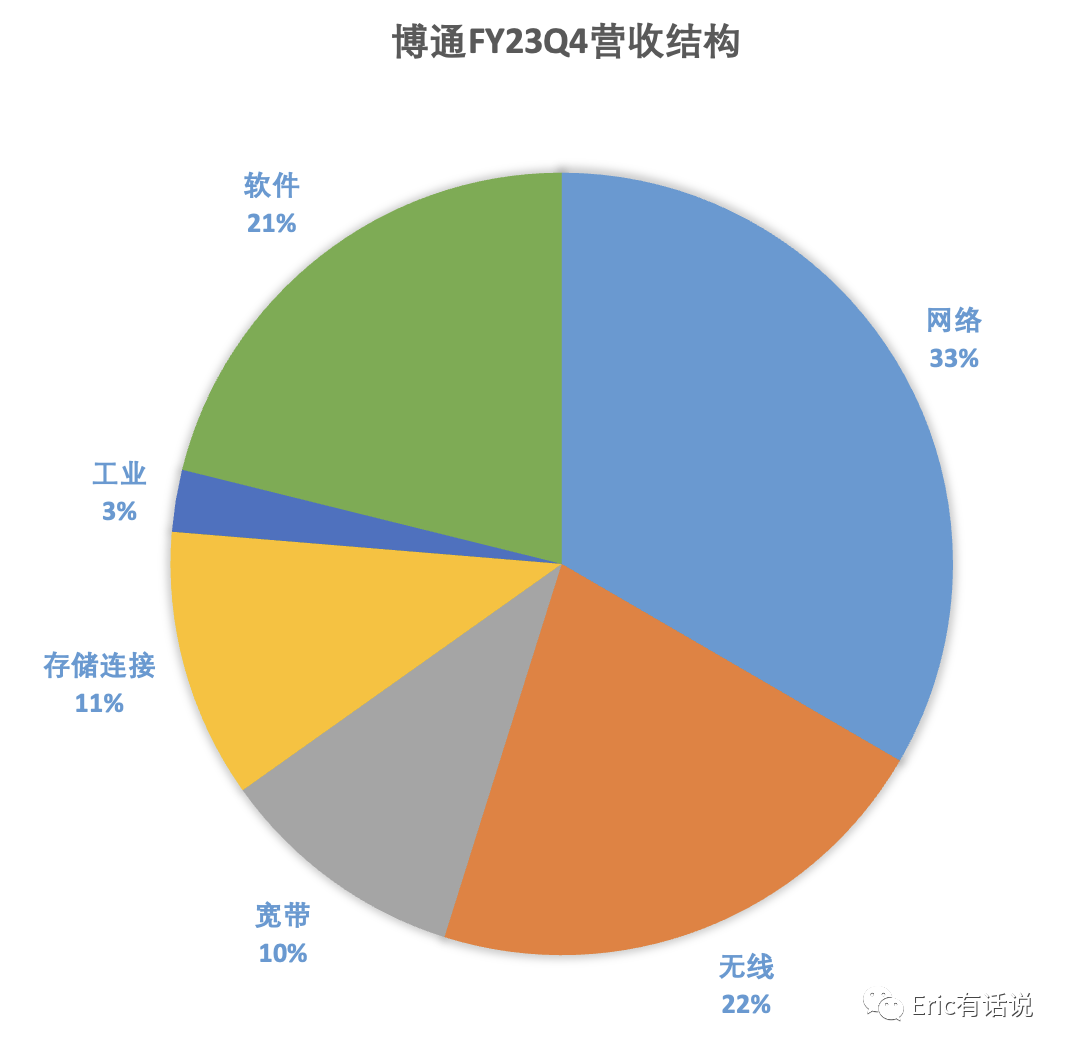

Networking revenue $3.1B, up 23% year over year, 42% of semiconductor revenue; AI-related switches, routers, and custom compute offload chips grew strongly; management believes Ethernet remains the best choice for AI; FY23 networking interconnect chip revenue excluding custom compute offload chips was $8B; FY24 networking revenue expected to grow 30% year over year, driven primarily by networking interconnect chips and custom compute offload chips.

Wireless revenue $2.0B, down 3% year over year, up 23% sequentially, 27% of semiconductor revenue; FY24 wireless revenue expected to be flat year over year.

Broadband revenue $950M, down 9% year over year, 13% of semiconductor revenue; FY24 broadband revenue expected to decline low- to mid-teens year over year; industry downcycle continues through FY24.

Storage connectivity revenue $1.0B, down 17% year over year, 14% of semiconductor revenue; FY24 storage connectivity revenue expected to decline mid- to high-teens year over year.

Industrial revenue $236M, flat year over year; FY24 industrial revenue expected to decline low single digits year over year.

Outlook:

FY24 semiconductor revenue expected to grow mid- to high-single digits year over year, benefiting from VMware consolidation (11 months, $12B); FY24 total revenue expected at $50B (software $20B), adjusted EBITDA $30B (VMware FY24 Q4 run rate $8.5B).

VMware integration expected to take one year, generating $1B in costs; future VMware focus will be on private and hybrid cloud; will divest end-user computing and Carbon Black businesses (approx. $2B, not in guidance).

VMware business model transformation: last quarter VMware subscription/SaaS revenue was only 37%; plan to fully SaaS-ify by end of FY24; by end of FY24, VMware annualized expense run rate $1.4B, down 14% year over year; VMware revenue expected to sustain double-digit growth over the next three years.

Customer inventory levels are healthy; only storage connectivity inventory is slightly elevated; broadband and networking inventory levels are normal; overall DOI decreased to 76 days.

No longer providing next-quarter outlook, only updating full-year outlook, mainly because VMware's full SaaS transition will cause near-term revenue volatility.

FY24 H2 expected to be better than H1; AI growth dragged down by traditional business declines.

AI Revenue Composition:

FY23 Q4 AI revenue ~$1.5B (below prior guidance of $1.7B), 20% of semiconductor revenue, up from 17% last quarter; management target for FY24 is 25%+, implying FY24 AI revenue ~$7.5B, estimated year-over-year growth of ~60-80%.

In the previous 'Marvell Earnings' article, we expressed concern about Broadcom's performance, but Broadcom's traditional business did not decline sharply like Marvell's. Per FY24 guidance, excluding AI, semiconductor revenue is only flat to slightly down year over year. Overall, Broadcom's earnings slightly missed expectations, mainly due to AI growth slightly below expectations and traditional business remaining stagnant.

Broadcom remains the second-largest beneficiary of AI among chip companies. However, management's FY24 AI revenue outlook is conservative, similar to AMD; last quarter's FY24 outlook was $7B, this quarter only raised to $7.5B.

Since quarterly guidance will no longer be disclosed, we conservatively estimate FY24 net income at a 35% net margin, yielding $17.5B net income on $50B revenue; applying Broadcom's 5-year valuation midpoint of 34x PE implies a market cap of $600B, assuming VMware integration proceeds without issues. The Apple exposure is a long-term risk, but near-term impact appears manageable.