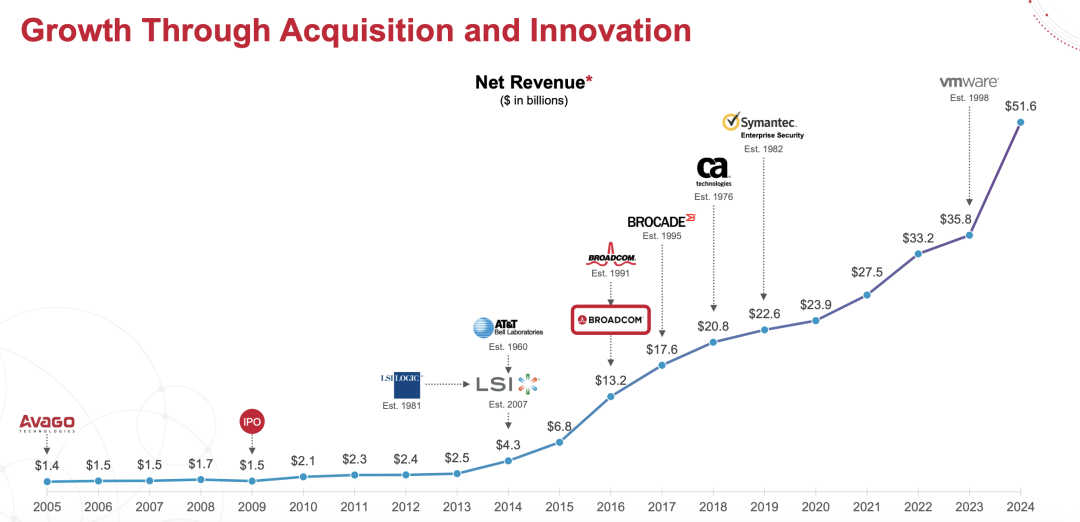

Broadcom FY25Q3 covers May/June/July 2025 results.

Broadcom FY25Q3 Results:

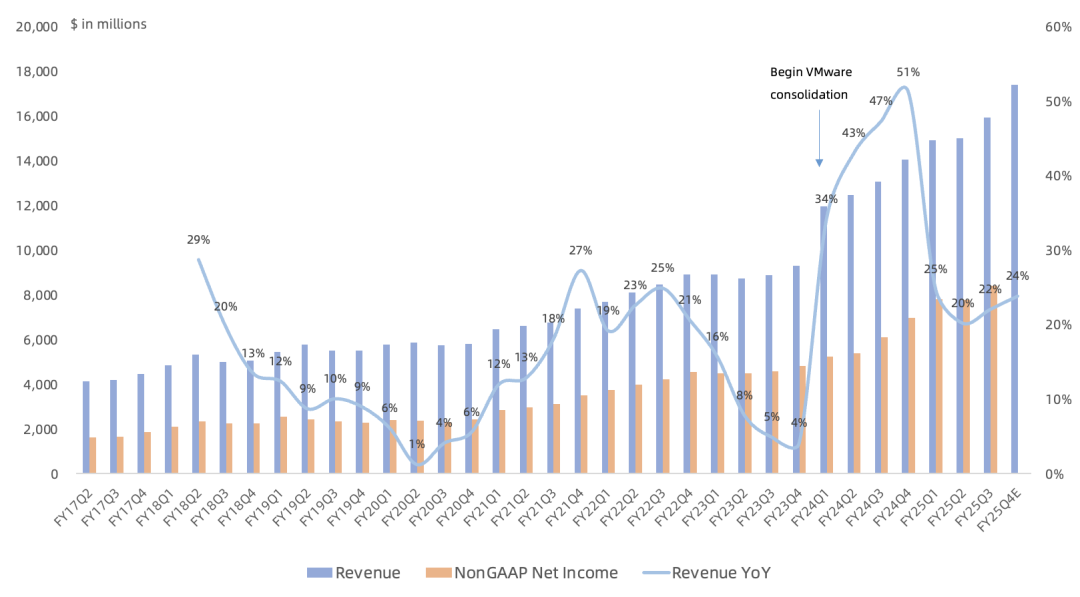

Revenue reached a record $15.952B, up 22% year over year and 6% sequentially.

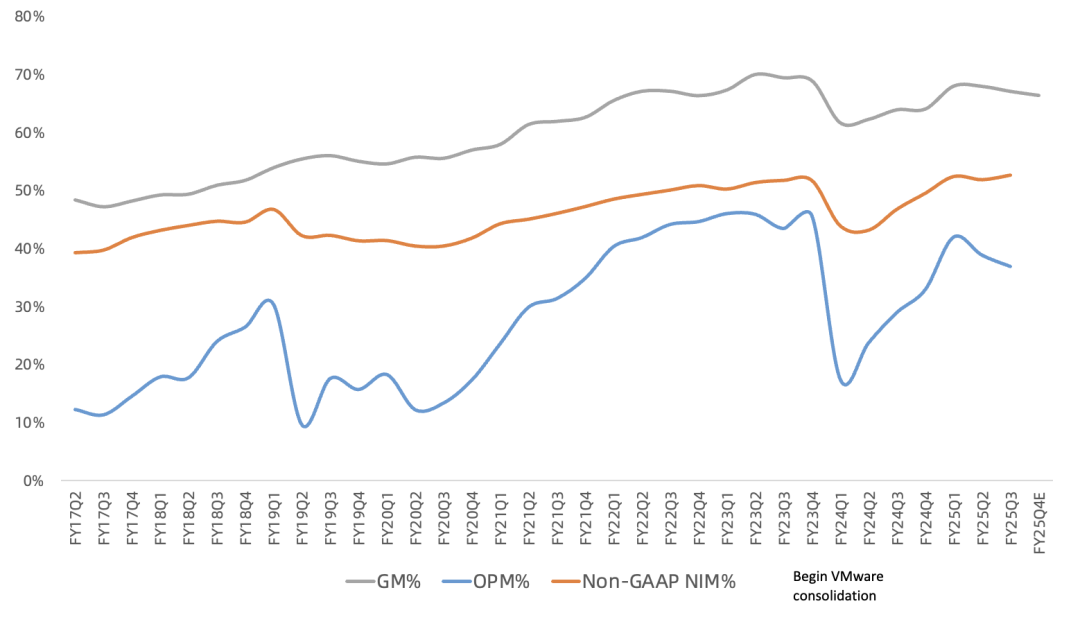

GAAP gross margin 67%, up 3.2 points year over year, down 0.9 points sequentially. Operating margin 37%, up 7.9 points year over year, down 1.9 points sequentially. Non-GAAP operating margin 53%, up 5.9 points year over year, up 0.8 points sequentially.

GAAP net income $4.14B, up 95% year over year. Non-GAAP net income $8.404B, up 56% year over year. Non-GAAP net margin 53% (vs 52% last quarter).

No share repurchases this quarter; $2.8B in dividends. Gross principal debt $66.3B.

Hock Tan to remain CEO, term through at least 2030.

By business, FQ3:

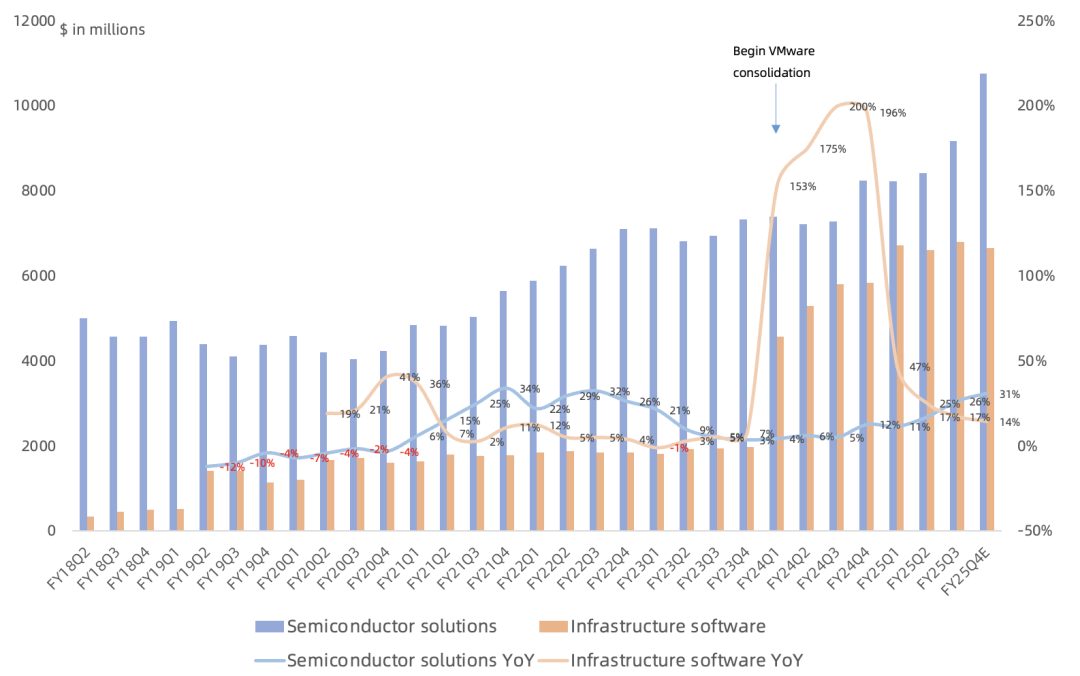

Semiconductor revenue $9.166B, up 26% year over year, 57% of revenue. Semiconductor gross margin 67%, down 0.3 points year over year, down nearly 2 points sequentially. Operating margin 57%, up 1.3 points year over year.

Software revenue $6.786B, up 17% year over year, slowest growth since VMware acquisition, 43% of revenue. Software gross margin 93%, operating margin 77%. Total contract value (TCV) signed this quarter exceeded $8.4B. VMware has 300K customers; over 90% of top 10,000 customers subscribe to full-stack VCF (up from 87% last quarter). FQ4 software revenue guided at $6.7B, up 15% year over year, growth continuing to decelerate. (Note: VMware revenue scale no longer disclosed since FY25Q1.)

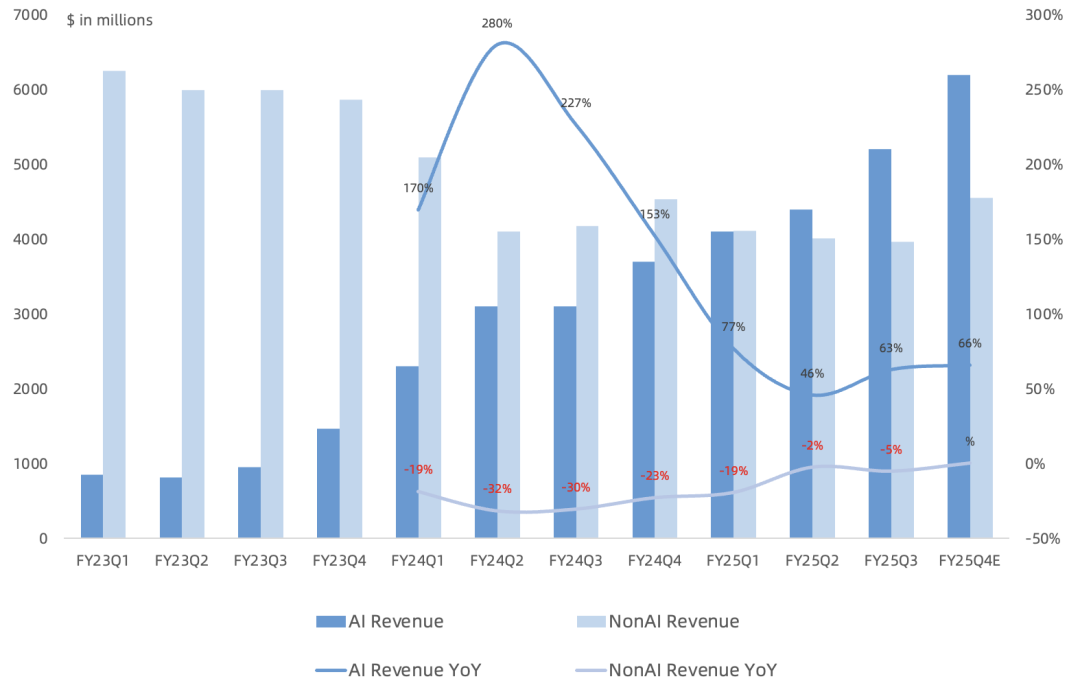

Semiconductor detail, FQ3: (Note: since FY25Q1, only semiconductor AI vs non-AI disclosed, not individual business lines.)

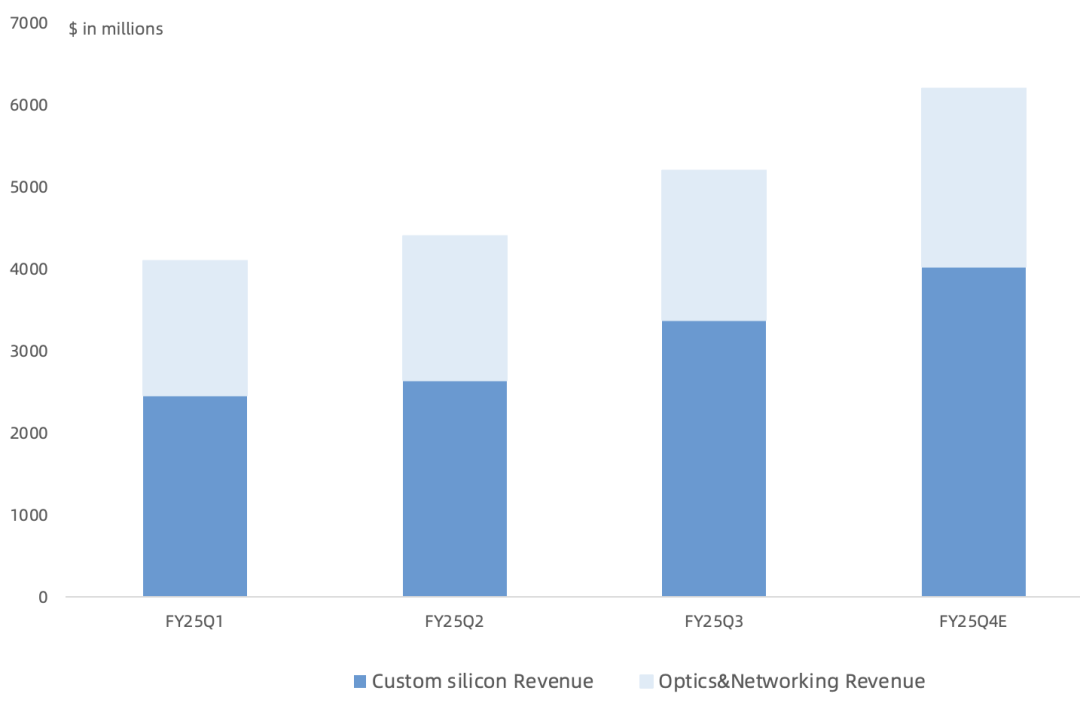

Semiconductor AI revenue $5.2B, up 63% year over year and 18% sequentially, slightly above prior guidance of $5.1B, accounting for 57% of semiconductor revenue. Of this, custom AI chip revenue $3.38B; Ethernet-based AI networking chip revenue $1.82B (NVIDIA's AI networking chip revenue this quarter was $7.25B, shipped primarily as server systems; Broadcom sells in chip form). AI networking vs custom AI chip revenue split 35%/65%; AI networking share expected to continue declining.

Semiconductor non-AI revenue $4.0B, flat year over year. Management says non-AI semiconductor demand recovery remains slow. While broadband posted strong sequential growth, enterprise networking and server storage declined sequentially; wireless and industrial were flat sequentially. FQ4 non-AI semiconductor revenue expected to grow low-double-digits sequentially to ~$4.6B driven by seasonality, with broadband, server storage, and wireless (iPhone 17 series) improving, while enterprise networking continues to decline sequentially. Management says meaningful recovery may not appear until mid-to-late 2026.

Broadcom's custom AI chip exposure is concentrated in three hyperscalers (Google, Meta, ByteDance). FY25Q1 announced four new partners (OpenAI, rumored Apple, etc.). This quarter announced landing the fourth customer (OpenAI) with a $10B deal, expected to begin delivery in FY26Q3.

FY25Q4 semiconductor AI revenue guided at $6.2B, up 66% year over year and 19% sequentially. Non-AI semiconductor revenue guided at $4.5B, up slightly year over year. Management says with the fourth customer's $10B deal, FY26 AI revenue growth will exceed FY25 (>60%), implying FY26 AI revenue near $34B.

Total backlog $110B, with semiconductor business >50%, and AI > non-AI within semiconductor.

Company XPU does not address enterprise AI market; focused solely on frontier LLM market.

Outlook:

FY25 Q4 revenue guided at $17.4B, up 24% year over year. Semiconductor revenue $10.7B, up 30% year over year, of which AI $6.2B (up 66%), non-AI $4.5B (up slightly). Software revenue $6.7B, up 15%. Gross margin 66.4%, down 0.7 points sequentially, mainly due to higher custom chip and wireless mix. Adjusted EBITDA $11.7B.

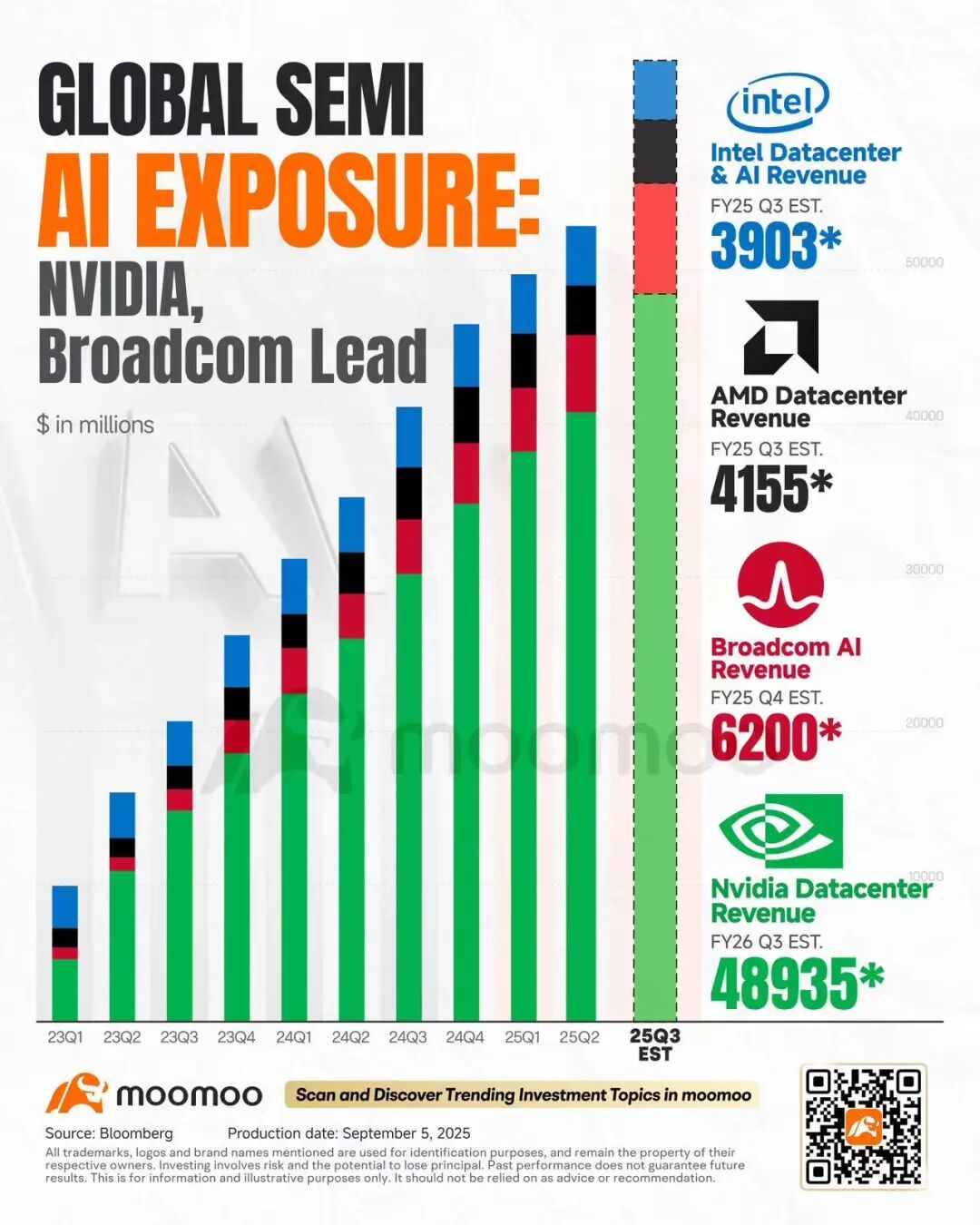

Overall, strictly from the numbers, Broadcom's report was mediocre (still falls short of NVIDIA, but market expectations for Broadcom were too low). AI revenue beat guidance only modestly; next-quarter AI guidance slightly above expectations. The key confidence boost came from Hock Tan announcing the fourth customer's $10B deal driving FY26 high growth. Over the past year many investors unwilling to accept NVIDIA dominance rotated into AMD, Broadcom, even Marvell; currently crowding into Broadcom and Google is common. Given cloud is the highest-ROI AI monetization venue, the cloud AI capex pie is large enough, and enterprise/sovereign AI are just starting, leaving ample growth runway for all.

Incorporating the FY26 AI revenue details from this earnings call, we optimistically raise FY26 revenue to ~$85B. At a non-GAAP net margin of 53%, that implies $45B net income. At 30x PE, that corresponds to a $1.35T market cap.