ASML stopped disclosing quarterly net bookings just as memory and advanced-node expansion began. Management nudged up its 2026 outlook but left the 2030 framework unchanged.

Lithography Leader ASML Q1 Earnings:

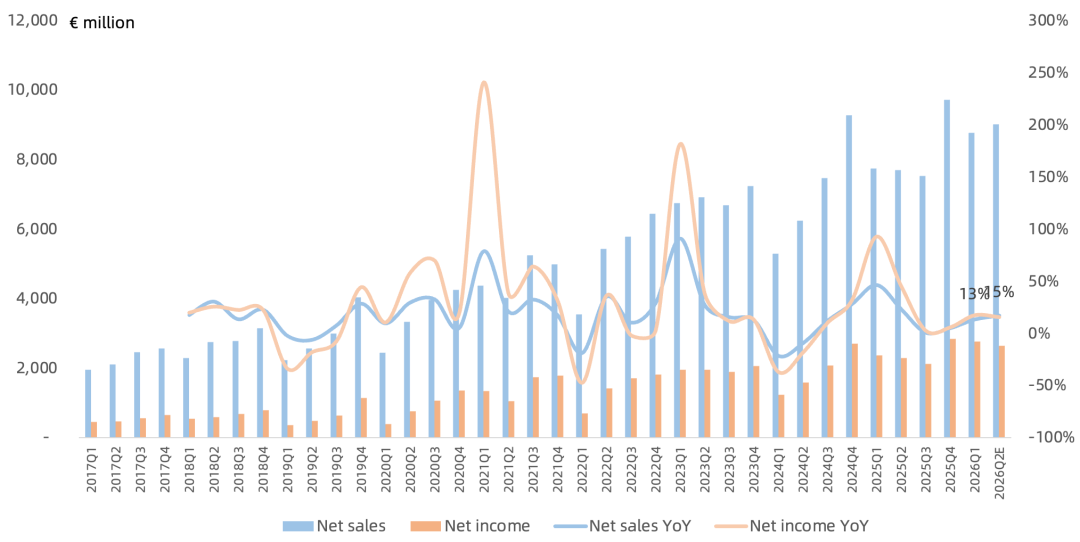

Revenue of €8.77B, up 13% year over year, at the upper end of the prior revenue guidance range of €8.2-8.9B;

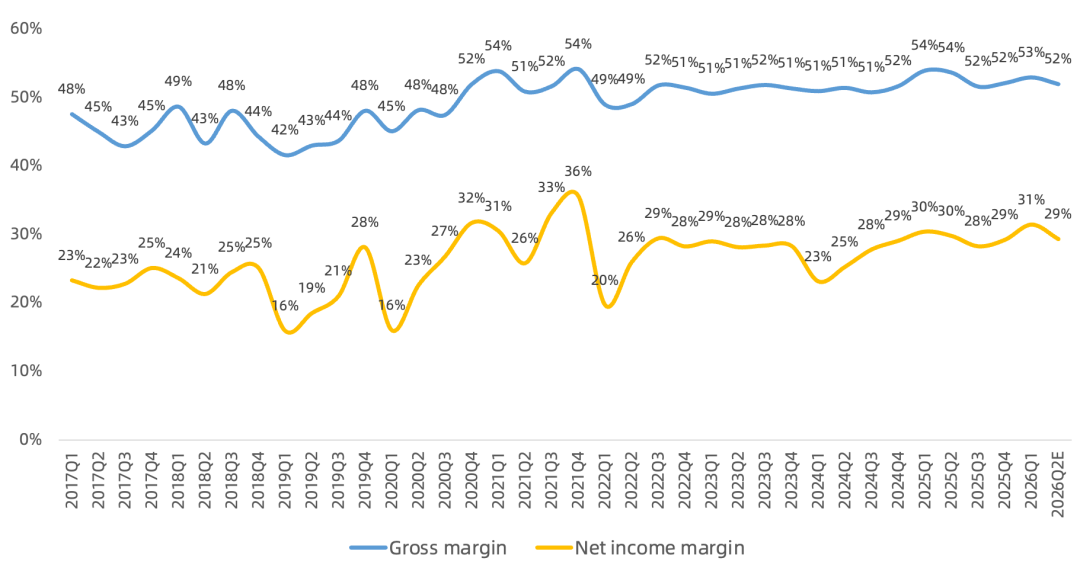

Gross margin of 53%, down 1 percentage point year over year, at the upper end of the prior gross margin guidance range of 51%-53%;

Net income of €2.76B, up 17% year over year, net margin of 31.4%;

Q1 share repurchases of €1.1B, marking the fifth consecutive quarter of buybacks;

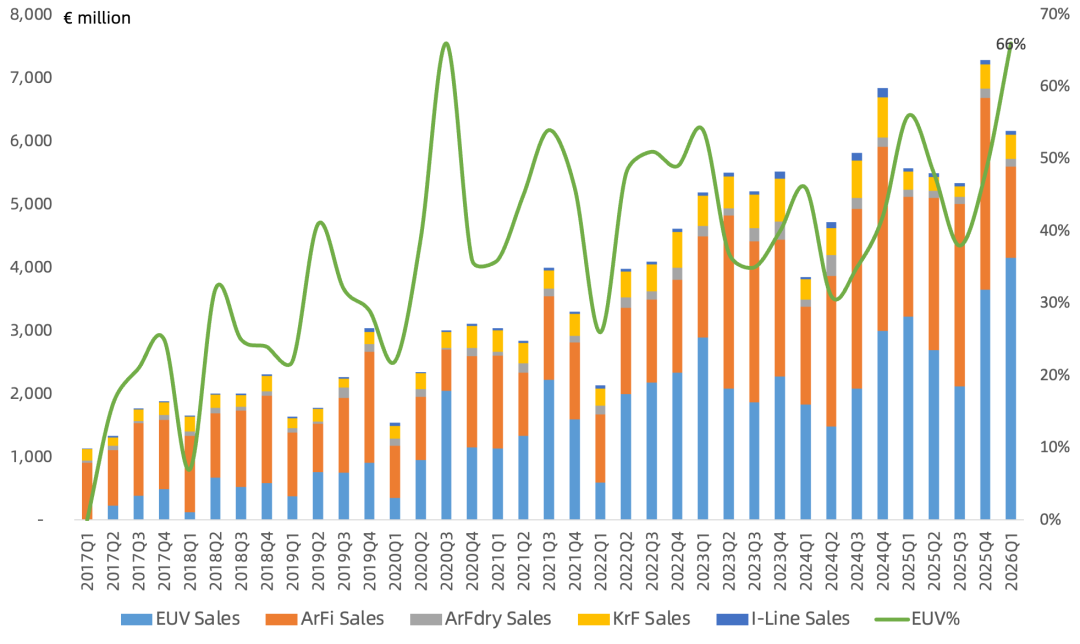

Looking specifically at lithography systems, Q1 shipped 79 systems, total volume up 3% year over year:

EUV: 16 systems, revenue of €4.14B, accounting for 66% of system revenue, ASP of €260M.

ArFi: 17 systems, revenue of €1.44B, accounting for 23% of system revenue, ASP of €84.96M.

ArF dry: 5 systems, revenue of €130M, accounting for 2% of system revenue, ASP of €25.12M.

KrF: 30 systems, revenue of €380M, accounting for 6% of system revenue, ASP of €12.56M.

I-Line: 11 systems, revenue of €60M, accounting for 1% of system revenue, ASP of €5.71M.

EUV revenue hit a record high this quarter, with a revenue share of 66%; revenue from 2 High NA EUV systems was recognized; DRAM customers face a relatively lower barrier to adopting High NA, and it cannot be ruled out that DRAM customers may accelerate High NA EUV adoption due to tight supply; management indicated that the previous cleanroom constraints limiting a customer's (Micron?) expansion have eased.

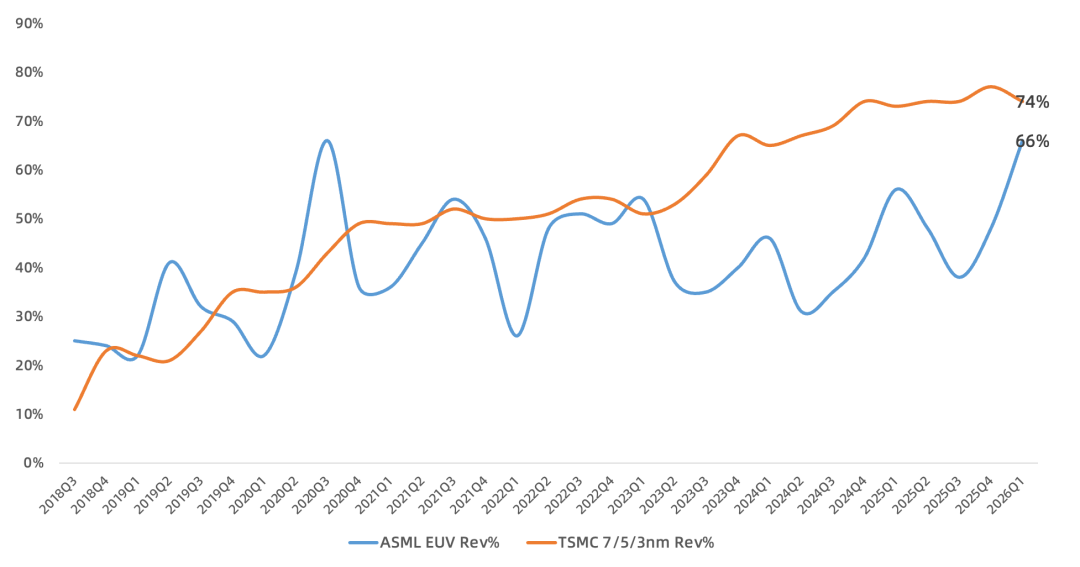

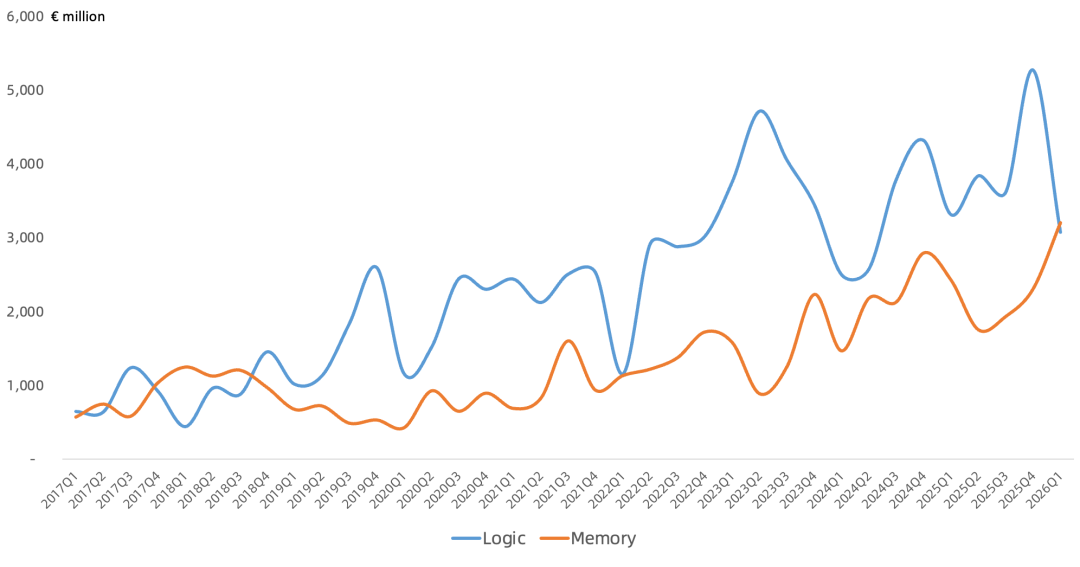

Memory revenue this quarter was €3.2B, up 32% year over year; logic revenue was €3.1B, down 7% year over year, marking the first time in recent years that logic revenue has been overtaken by memory; advanced-node logic and memory customers remain in short supply through 2026 and beyond.

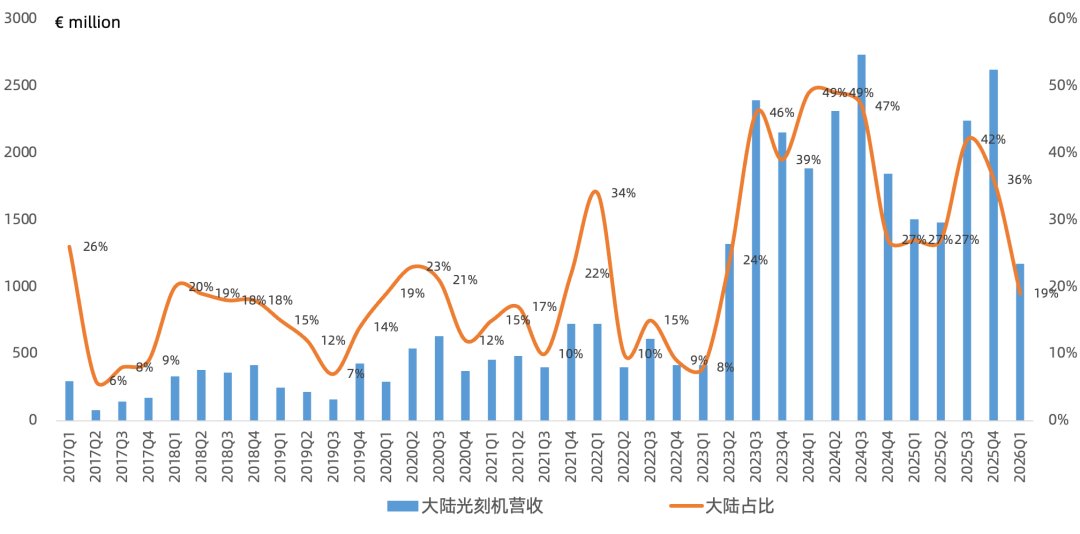

Mainland China lithography revenue this quarter was €1.2B, down 22% year over year; lithography revenue share fell to 19%; management maintained full-year Mainland China revenue share guidance at around 20%.

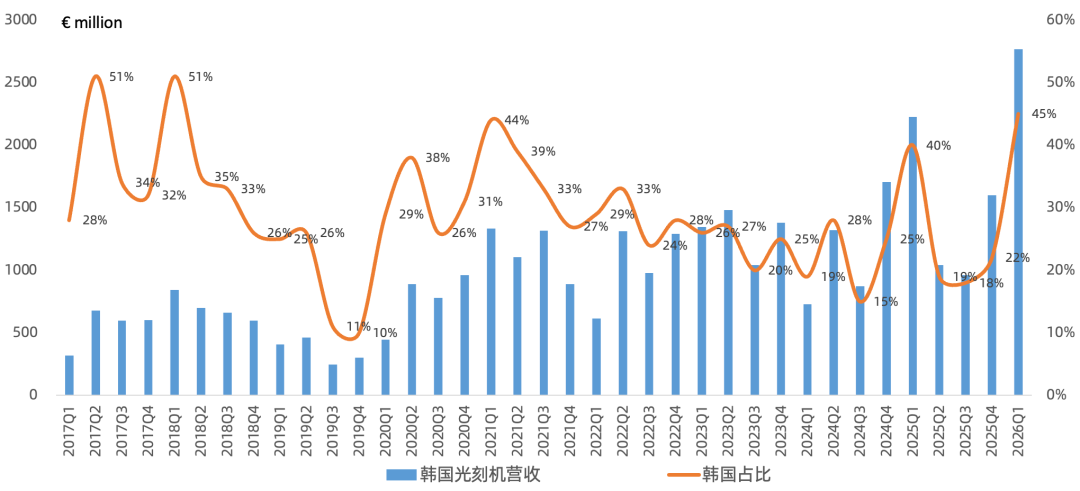

Benefiting from massive memory expansion, Korea became ASML's largest customer region this quarter; Korea lithography revenue was €2.8B, up 24% year over year; lithography revenue share rose to 45%, a new high since 2018.

Outlook:

Q2 revenue guided at €8.4-9.0B, up 9%-17% year over year; Installed Base revenue of €2.5B; Q2 gross margin guided at 51%-52%; based on the upper end of revenue guidance, net income of €2.6B, up 15% year over year;

2026 revenue guidance raised from €34-39B to €36-40B, up 10%-22% year over year; gross margin maintained at 51%-53%; EUV business growth outlook raised; DUV business also expected to grow (previous guidance was flat), primarily driven by non-Mainland China customers; revenue cadence skewed to H2 due to capacity ramp; guidance already incorporates impact of export controls such as the MATCH Act;

Installed Base expected to continue growing in 2026, benefiting from rising EUV installed base and significant customer upgrade demand; EUV service gross margin has improved from a loss 4-5 years ago to near the overall gross margin level;

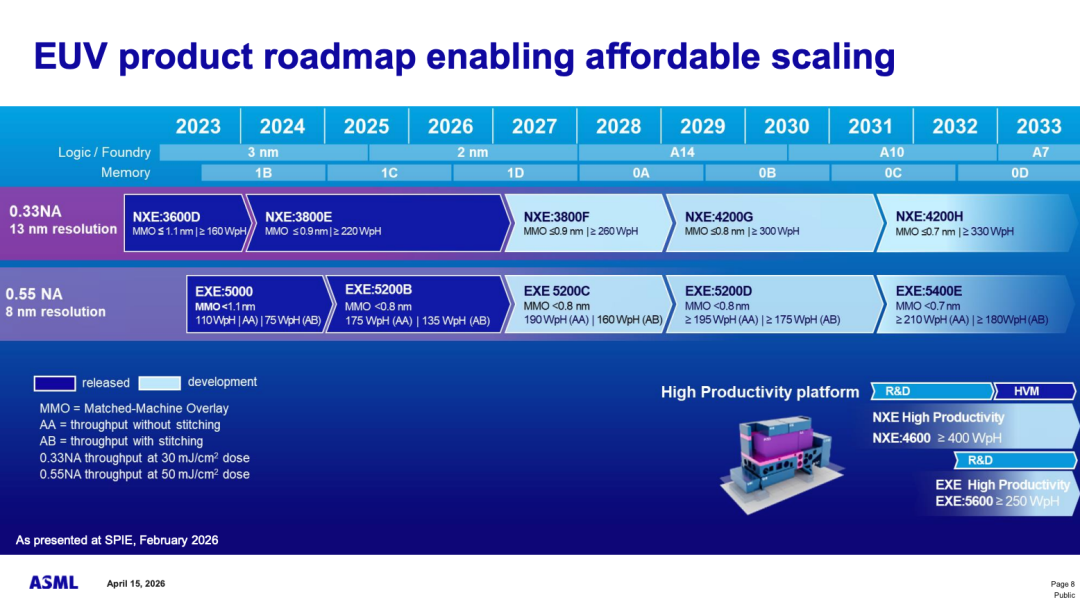

The company has multiple levers to increase EUV capacity: number of tools, wafers per hour per tool, Installed Base upgrades, etc.

Capacity/shipment guidance update: 2026 Low NA EUV shipments of at least 60 units; immersion DUV shipments near 2025 levels; 2027 Low NA EUV shipments of at least 80 units (2025: 44 units); DUV capacity expanding in sync; management states supply chain has been prepared for Low NA EUV capacity of 90 units/year and DUV capacity of 600 units/year; previous Zeiss optics bottleneck has significantly improved;

ASP guidance update: Management states lithography ASP is directly linked to wafers per hour; 2026 EUV shipments mostly NXE systems, ~20% EXE systems, while 2027 EUV shipments will have almost no EXE systems, mostly NXE, with High NA (EXE:5000/5200) beginning to ramp; 2027 ASP expected to be significantly higher than 2026;

Puzzlingly, management still has not updated the 2030 revenue target of €44-60B, especially since the 2026 guidance upper bound of €40B is already approaching the lower bound of the 2030 target; combined with the bullish 2027 growth guidance, this is perplexing, perhaps management is saving an upward revision for the H2 Investor Day?

Recap of Prior 24Q3 View:

ASML's biggest issue at this stage is growth. ASML's 2024 results showed no growth; if 2025 revenue comes in at €30-35B, combined with gross margin and OpEx guidance, net income optimistically reaches only ~€9B, which at the current market cap still looks expensive.

While ASML's monopoly position is unchallenged, that does not mean lithography demand grows linearly, nor does it directly capture the AI demand explosion. TSMC, positioned in midstream manufacturing, can directly interface with downstream AI customers and capture the full AI dividend.

Due to the unique position of lithography in the supply chain, ASML's growth in recent years has been constrained by weak memory customers, relying mainly on the Mainland China mature-node expansion wave and TSMC's expansion wave to drive growth.

Now memory customers have returned as kings, and TSMC continues massive expansion. The only constraint on ASML is capacity, and on this point management delivered a better-than-expected answer in this earnings report.

ASML's 2030 financial targets still originate from the 2022 Investor Day; the semiconductor industry has since undergone a sea change. The focus now is on whether an Investor Day will be held in H2 this year to raise the 2030 guidance.