As it turned out, ASML truly had no growth in 2024, and a 2025 breakout may still need help from TSMC.

Lithography leader ASML reports Q4 earnings:

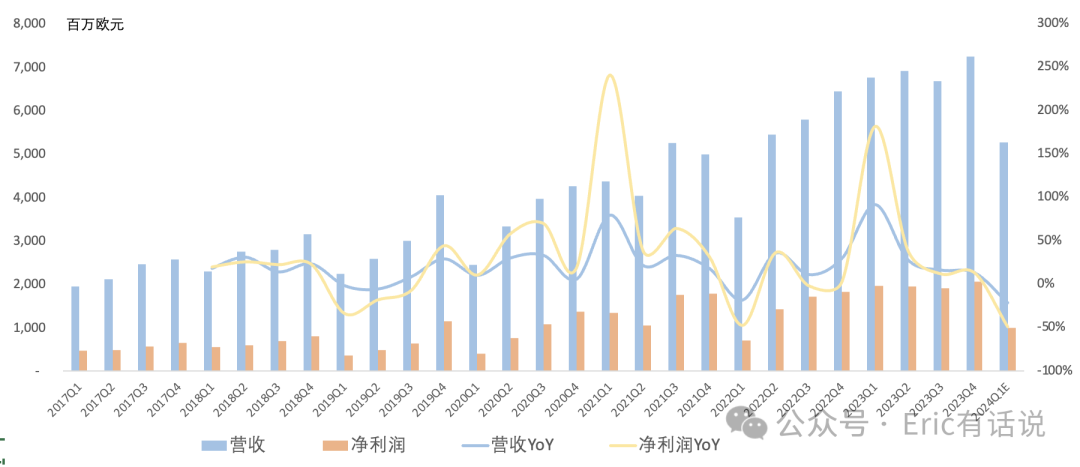

Revenue was €7.237B, up 13% year over year and 9% sequentially, a new all-time high.

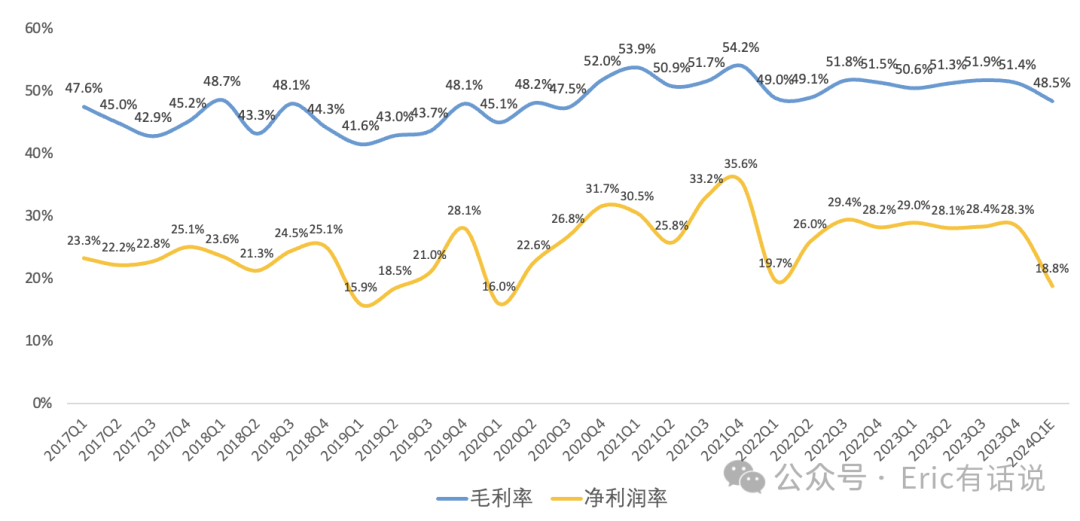

Gross margin was 51.4%, down 0.1 percentage points year over year and 0.5 percentage points sequentially, slightly above expectations, mainly driven by Installed Base Management business lifting gross margin.

Operating income was €2.392B, up 13% year over year and 10% sequentially; operating margin 33.1%.

Net income was €2.048B, up 13% year over year and 8% sequentially; net margin 28.3%.

Backlog was €39B.

No share repurchases in Q4.

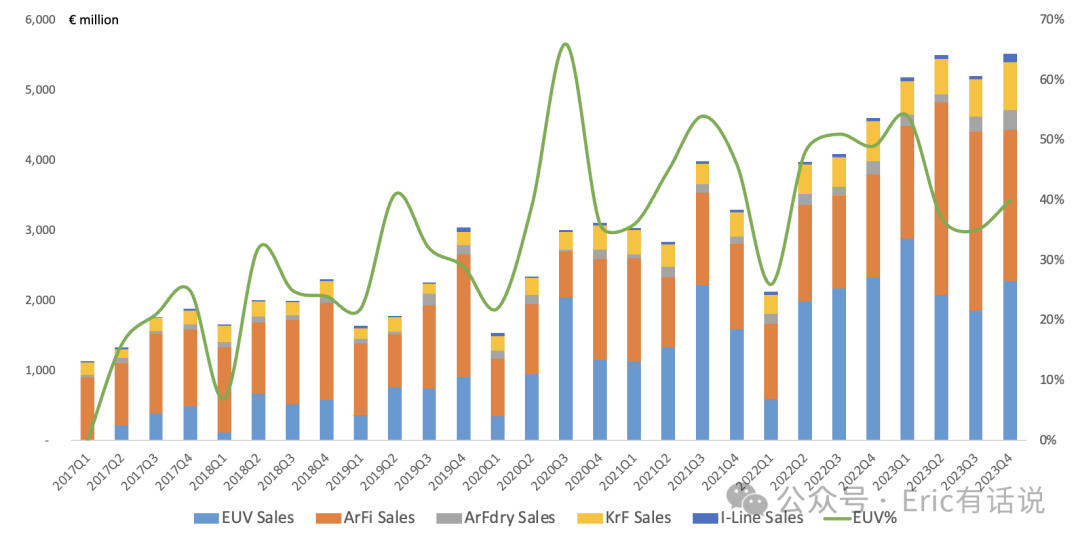

On the lithography front, Q4 shipped 124 systems, a new record:

EUV: 13 units, revenue €2.273B, 40% of system revenue, ASP €175M.

ArFi: 29 units, revenue €2.16B, 38% of system revenue, ASP €74.47M.

ArF dry: 10 units, revenue €284M, 5% of system revenue, ASP €28.42M.

KrF: 54 units, revenue €682M, 12% of system revenue, ASP €12.63M.

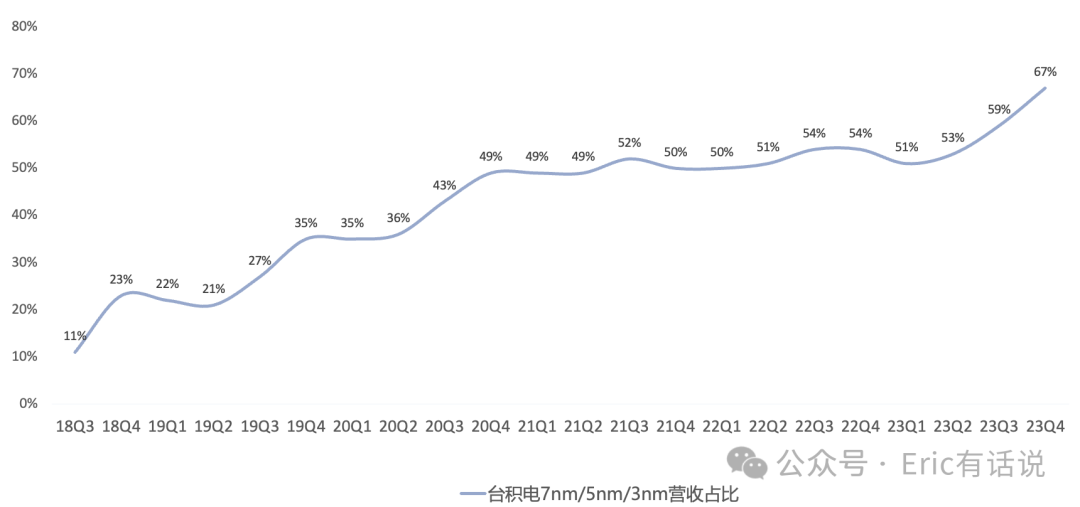

EUV shipments recovered sequentially this quarter, with revenue surpassing immersion DUV; on the TSMC side, 3nm ramp drove 7nm/5nm/3nm mix to a record 67%.

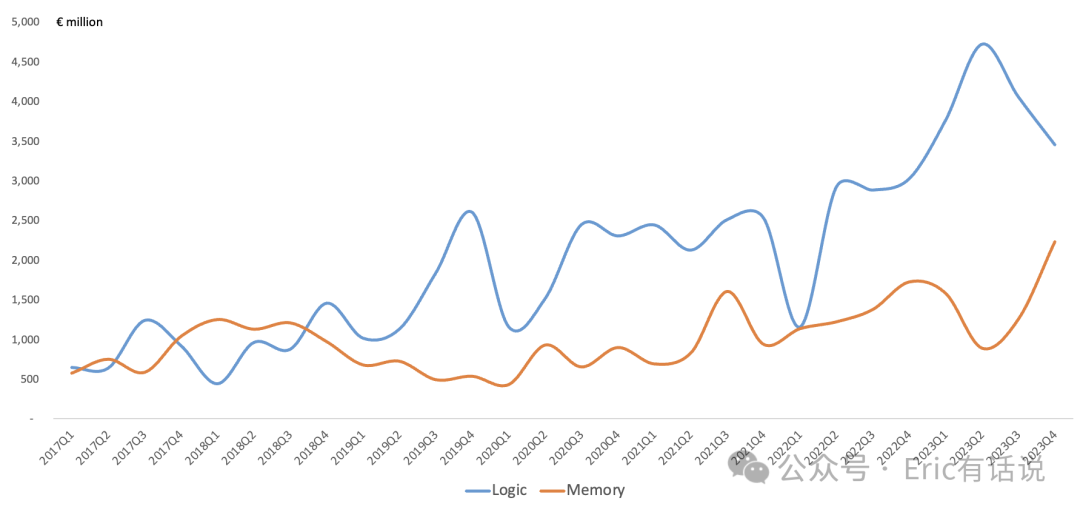

The biggest highlight of this report is the memory rebound. Q4 memory revenue was €2.232B, up 29% year over year, ending two consecutive quarters of declines while setting a new all-time high, accounting for 37% of system revenue. Logic revenue, while not a new high, still achieved its seventh consecutive quarter of growth.

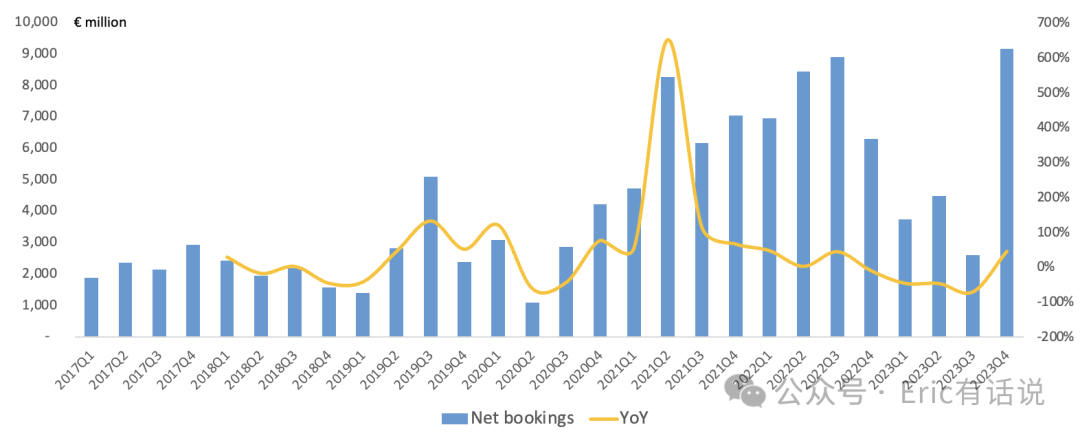

Steady logic plus rebounding memory drove a booking beat: Q4 net bookings hit a record €9.2B. Memory orders saw a massive return; memory bookings share rose to 47%, amount up 730% sequentially. Of the €9.2B in bookings, EUV accounted for €5.6B, including Low-NA and High-NA.

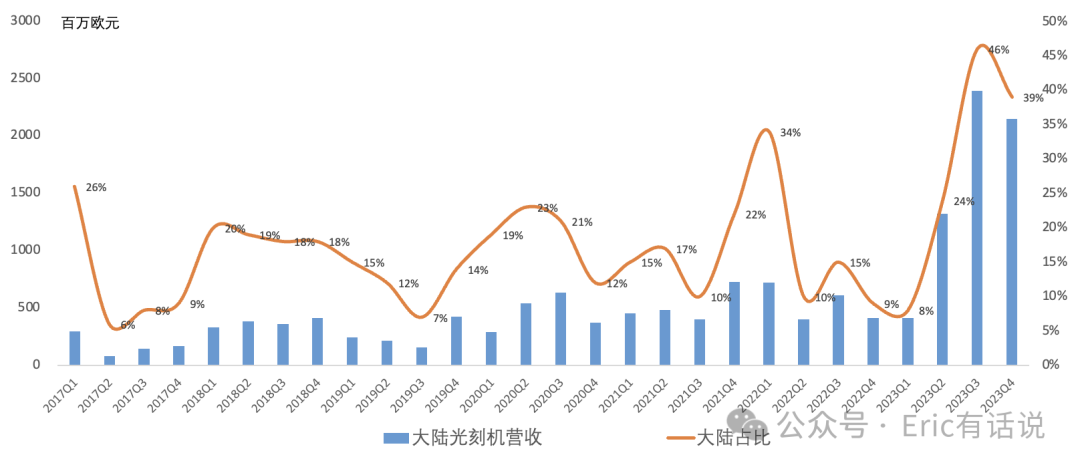

Mainland China lithography revenue remained elevated this quarter at €2.15B per quarter, up 419% year over year, accounting for 39% of system revenue, remaining ASML's largest customer region.

On the latest export controls, the Dutch government revoked export licenses for the 2050i and 2100i on January 2, 2024, adding to prior restrictions on the 1980i and 1970i; ASML estimates a 10%-15% impact on 2024 mainland China revenue.

Outlook:

Guides 2024 Q1 revenue of €5.0-5.5B, down 19%-26% year over year; full-year revenue flat year over year, with H2 > H1.

The shape and pace of the semiconductor recovery remain uncertain, but three positive signals: 1) industry inventory levels gradually normalizing; 2) lithography utilization rising (still below normal); 3) Q4 new bookings surged; ASML memory warming up, 2024 revenue to grow (DRAM DDR5+HBM), while logic revenue to dip slightly.

Expects 2024 EUV revenue to continue growing; shipments of NXE 3800E and 1-2 High-NA units will lift overall ASP; non-EUV revenue to dip slightly, especially immersion DUV; Installed Base Management flat year over year.

All existing EUV customers have ordered High-NA EUV.

Q1 gross margin 48%-49%; full-year gross margin down slightly year over year, mainly due to immersion DUV revenue decline and capacity expansion investment.

2025 operating targets unchanged: revenue €30-40B, gross margin 54%-56%; confidence from High-NA EUV ramp, higher ASP EUV mix, and a wave of new fabs coming online.

Last quarter I said "ASML near-term advanced-node EUV demand slowing, backfilled by mainland mature-node DUV, a bit like a spent arrow"; this report shows EUV demand improving on the memory rebound, but DUV will subsequently decline, while High-NA EUV volume must wait until 2025.

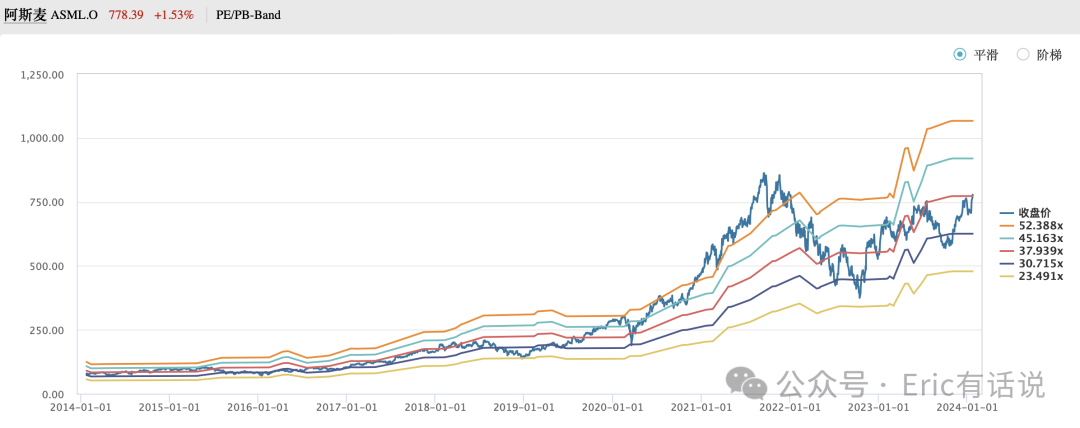

Overall, it returns to the growth question: ASML 2024 earnings flat; if the 2025 €30-40B revenue target holds, that implies 2025 growth of 9%-45%, a range too wide, so valuation levels still need consideration.