As previously emphasized, ASML's biggest current issue is a growth problem; this quarter management indicated 2026 results may not grow.

Lithography Leader ASML Q2 Earnings:

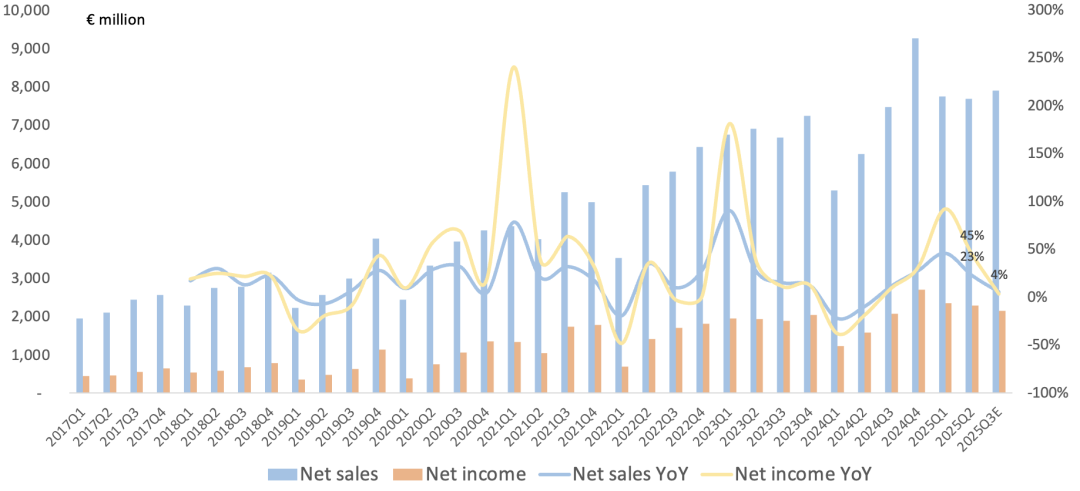

Revenue of €7.692B, up 23% year over year, down 1% sequentially, at the high end of prior guidance.

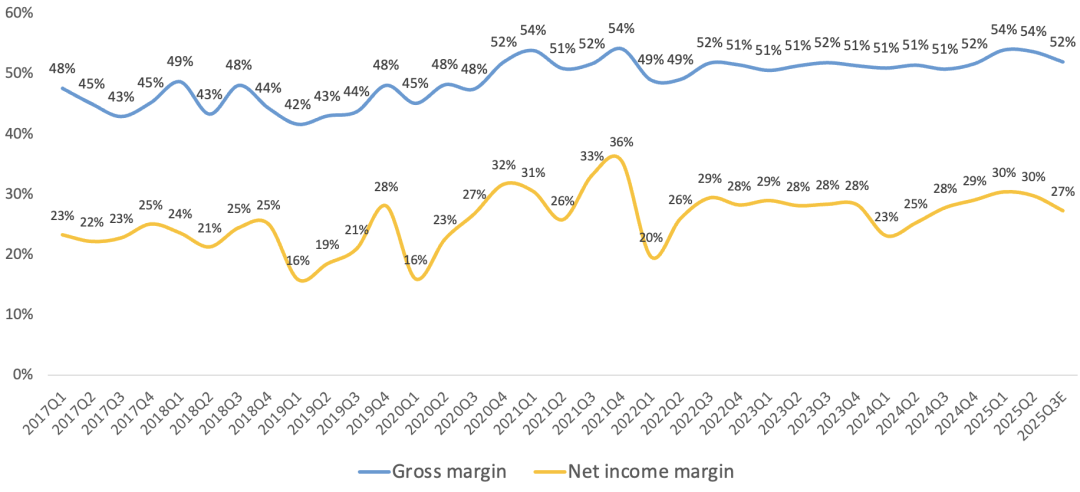

Gross margin of 53.7%, up 2.2 percentage points year over year, down 0.3 percentage points sequentially, above the prior guidance ceiling, primarily due to better-than-expected Installed Base and NXE:3800 performance, and lower-than-expected tariff impact; second-half margins pressured by High-NA ramp.

Operating income of €2.66B, up 45% year over year, down 3% sequentially, operating margin of 34.6%.

Net income of €2.29B, up 45% year over year, down 3% sequentially, net margin of 29.8%.

Q2 share repurchases of €1.4B, the 2nd consecutive quarter of buybacks.

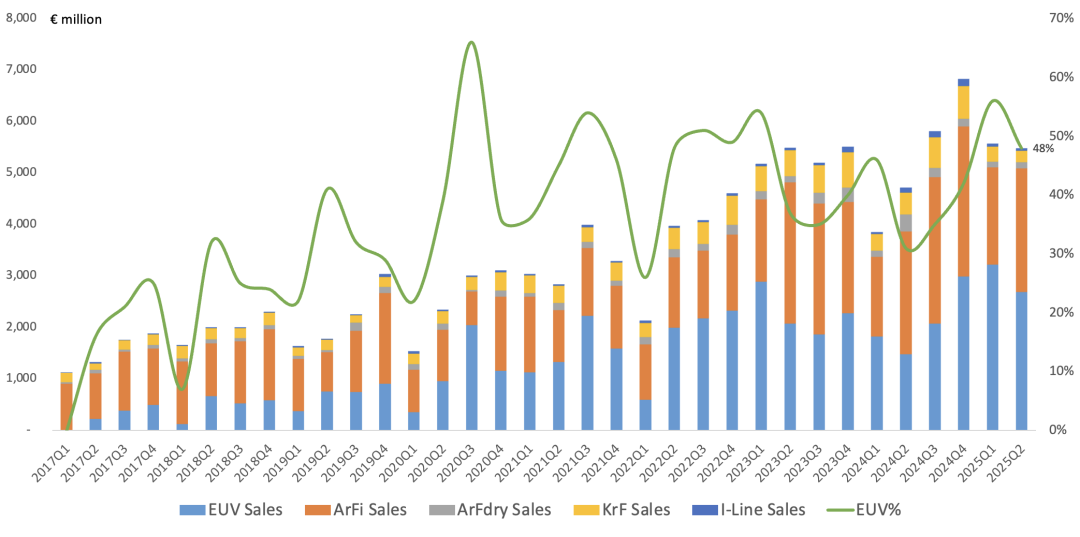

In lithography, Q2 shipped 76 systems total, down 24% year over year:

EUV: 11 systems, revenue of €2.686B, 48% of system revenue, ASP of €240M.

ArFi: 31 systems, revenue of €2.406B, 43% of system revenue, ASP of €77.62M.

ArF dry: 4 systems, revenue of €112M, 2% of system revenue, ASP of €27.98M.

KrF: 16 systems, revenue of €224M, 4% of system revenue, ASP of €13.99M.

I-Line: 14 systems, revenue of €56M, 1% of system revenue, ASP of €4M.

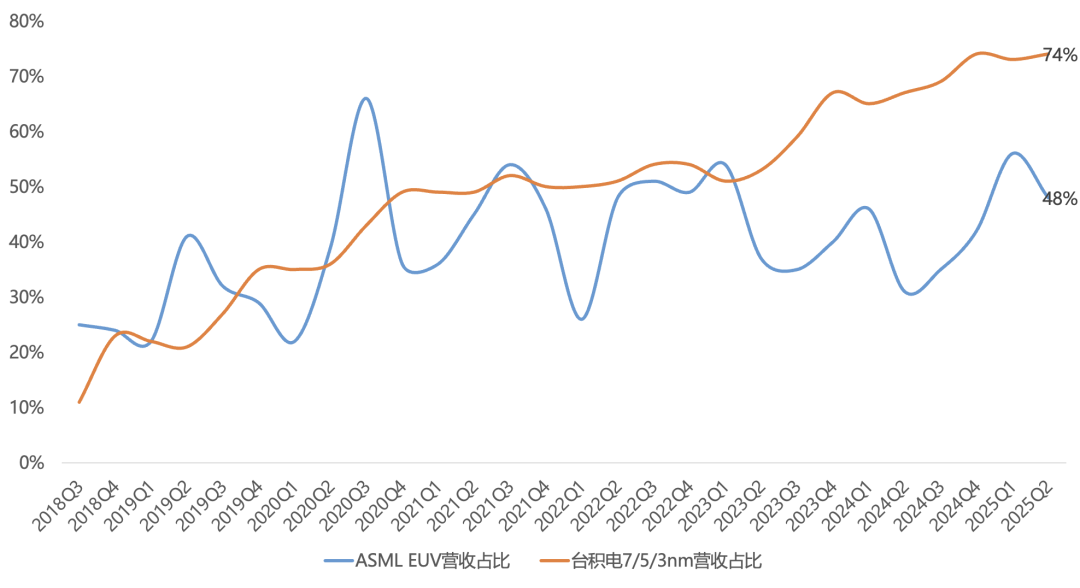

EUV revenue share declined this quarter; EUV ASP hit a new high, driven by a higher mix of the 3800 model; NXE:3800 throughput increased to 220 wph (+30%), making it the mainstream choice for low-NA customers; shipped the first High-NA EXE:5200B this quarter, which pressured margins; second-half High-NA shipments will exceed the first half.

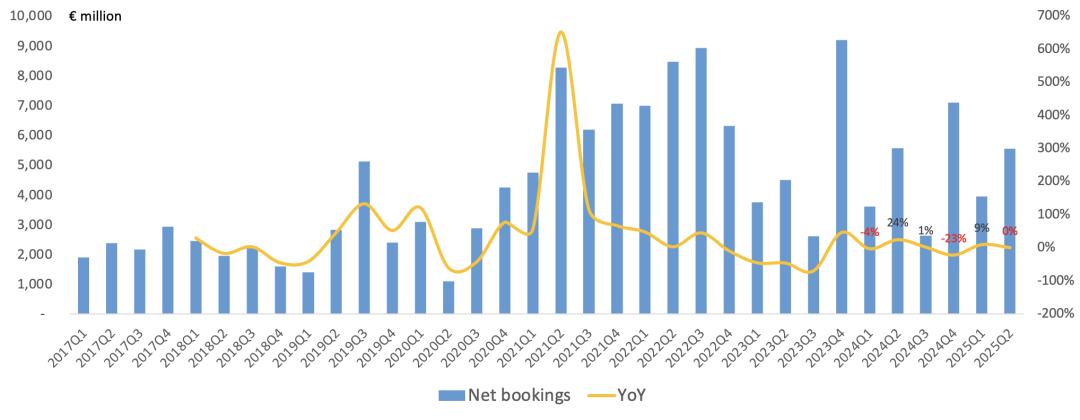

Net bookings of €5.541B, down 1% year over year, of which EUV was €2.3B, down 8% year over year but up 92% sequentially; logic and memory accounted for 84%/16% of net bookings, with logic up 24 percentage points sequentially and memory down 24 percentage points.

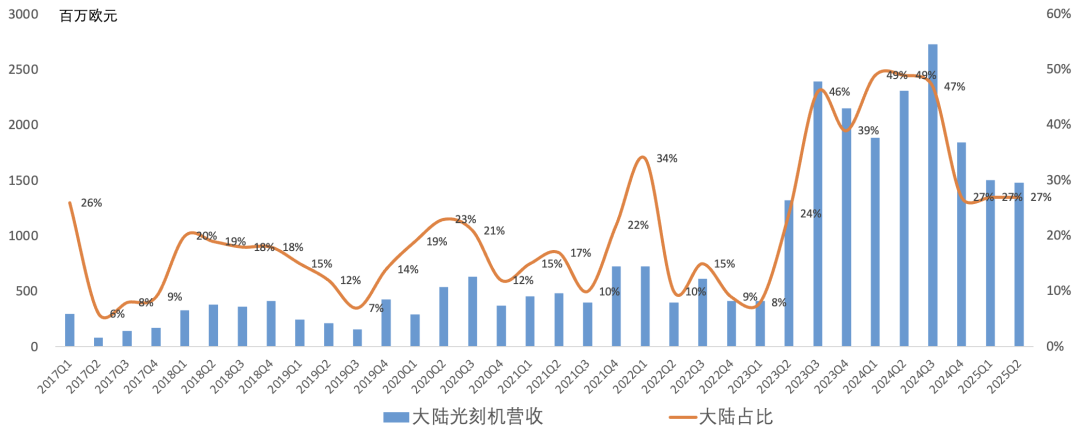

Mainland China single-quarter lithography revenue of €1.5B, down 36% year over year, representing 27% of lithography revenue; Taiwan replaced Mainland China as ASML's largest customer region, consistent with prior management guidance of ~25% full-year Mainland China revenue share.

Outlook:

Guiding Q3 revenue of €7.4-7.9B, down 1% to up 6% year over year; Installed Base revenue of €2B; Q3 gross margin of 50%-52%.

Maintaining 2025 revenue guidance of €32.5B, up 15% year over year; full-year EUV revenue up 30%, DUV flat, Installed Base revenue up 20%; maintaining 2025 gross margin of 52%, with High-NA pressuring margins; second-half revenue higher than first half.

Management expects the 2025 logic market to continue growing on exploding AI demand, and the memory market to see strong growth driven by HBM/DDR5; 2026 has too much uncertainty from tariffs and other factors, and results may not grow.

Management maintains the 2030 revenue target of €44-60B unchanged, with gross margin of 56%-60%.

Maintaining Previous 24Q3 View:

ASML's biggest issue at this stage is growth. ASML's 2024 results showed no growth; if 2025 revenue comes in at €30-35B, combined with gross margin and OpEx guidance, net income optimistically reaches only ~€9B, which at the current market cap still looks expensive.

While ASML's monopoly position is unchallenged, that does not mean lithography demand grows linearly, nor does it directly capture the AI demand explosion. TSMC, positioned in midstream manufacturing, can directly interface with downstream AI customers and capture the full AI dividend.