Previously emphasized that ASML's biggest issue at this stage is growth. Even with this quarter's shocking net bookings, management maintained the 2030 financial targets unchanged. However, the memory capacity expansion wave has been confirmed, which is positive for the entire semiconductor equipment sector.

Lithography Leader ASML Q4 Earnings:

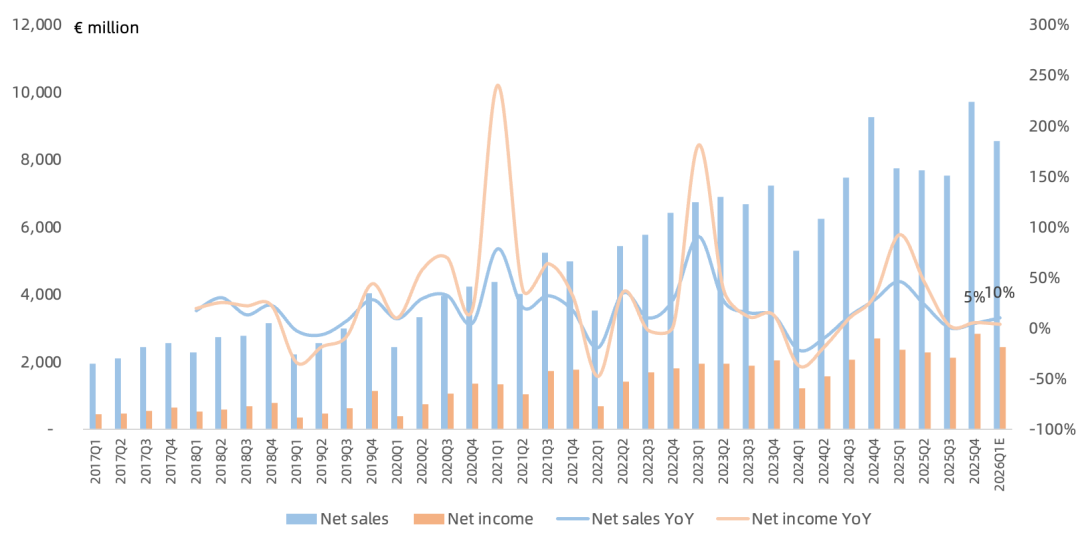

Revenue of €9.72B, up 5% year over year, above consensus of €9.56B, at the upper end of prior guidance range of €9.2-9.8B.

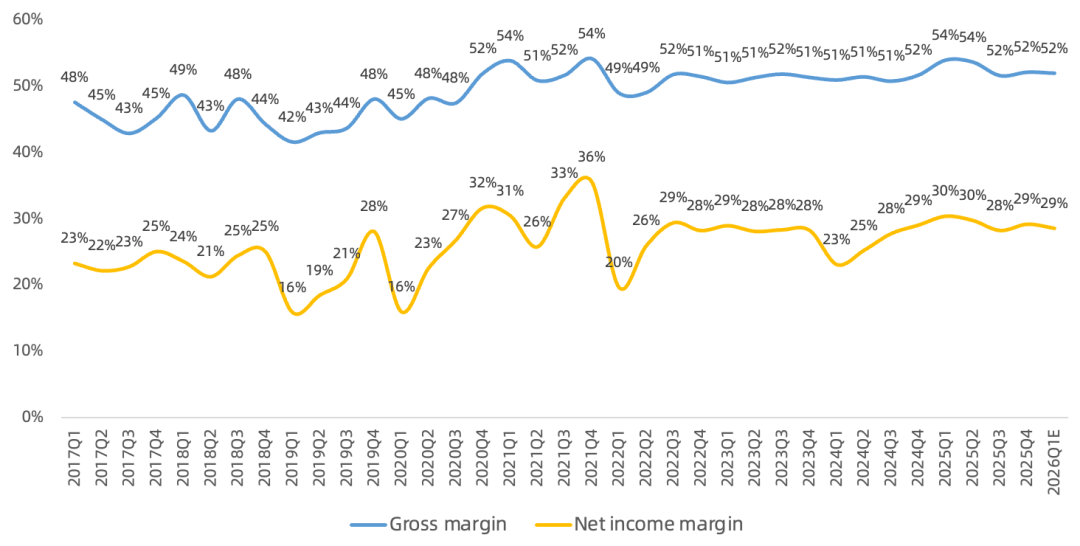

Gross margin of 52.2%, up 0.5 percentage points year over year, above consensus of 51.9%, at the upper end of prior guidance range of 51-53%.

Net income of €2.84B, up 5% year over year, below consensus of €2.91B; net margin of 29.2%.

Q4 repurchases of €1.7B, fourth consecutive quarter of buybacks; announced a €12B three-year repurchase program.

Backlog of €38.8B, of which EUV is €25.5B.

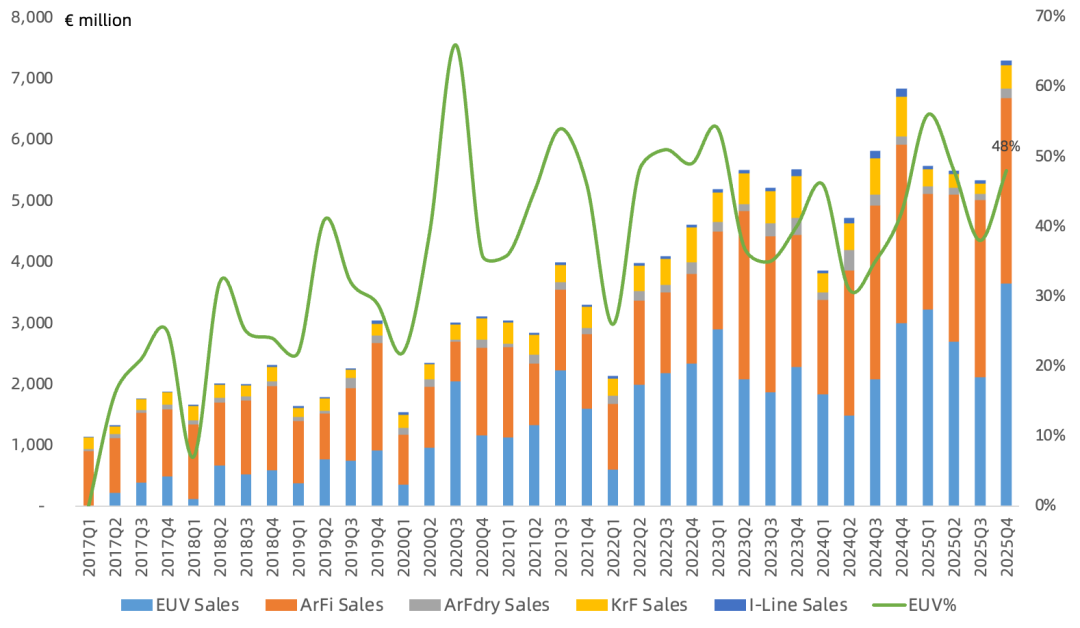

Lithography specifics: Q4 shipped 102 systems, total down 23% year over year:

EUV: 14 units, revenue €3.64B, 48% of system revenue, ASP €260M.

ArFi: 37 units, revenue €3.03B, 40% of system revenue, ASP €81.99M.

ArF dry: 5 units, revenue €150M, 2% of system revenue, ASP €30.34M.

KrF: 29 units, revenue €380M, 5% of system revenue, ASP €13.08M.

I-Line: 17 units, revenue €76M, 1% of system revenue, ASP €4.46M.

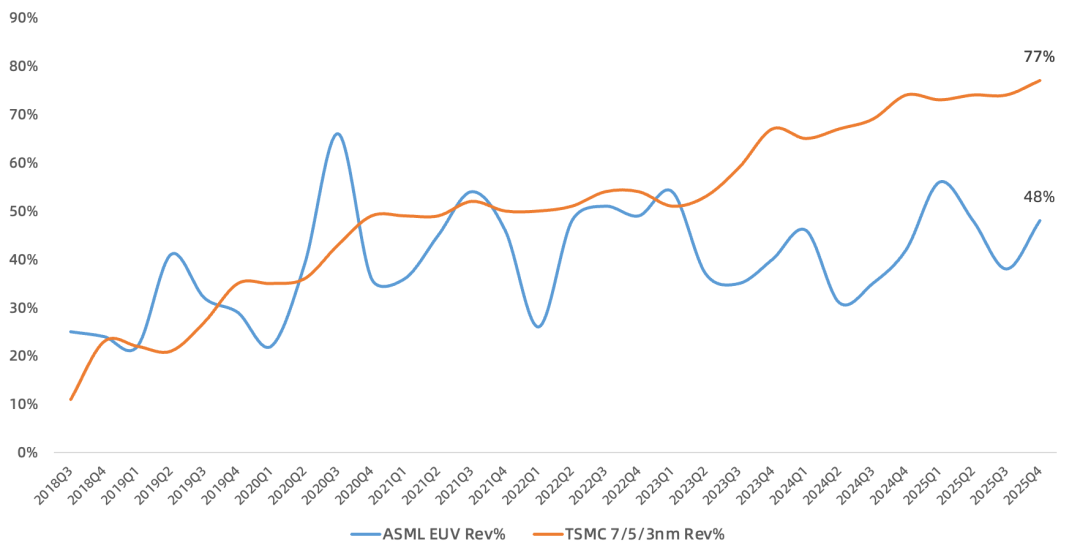

EUV revenue share finally increased this quarter; confirmed revenue from 2 high-NA EUV systems. Logic customers growing more confident in long-term AI demand sustainability; 2nm ramping faster. DRAM customers' HBM and DDR demand very strong; 1b/1c nodes entering volume production, meaning customers are truly investing in capacity and accelerating mid-term expansion plans. These nodes all increase EUV layer counts. DRAM customers actually expect non-EUV demand there to rise as well. During DRAM's transition from 6F² to 4F², both immersion and low-NA are expected to see increased usage.

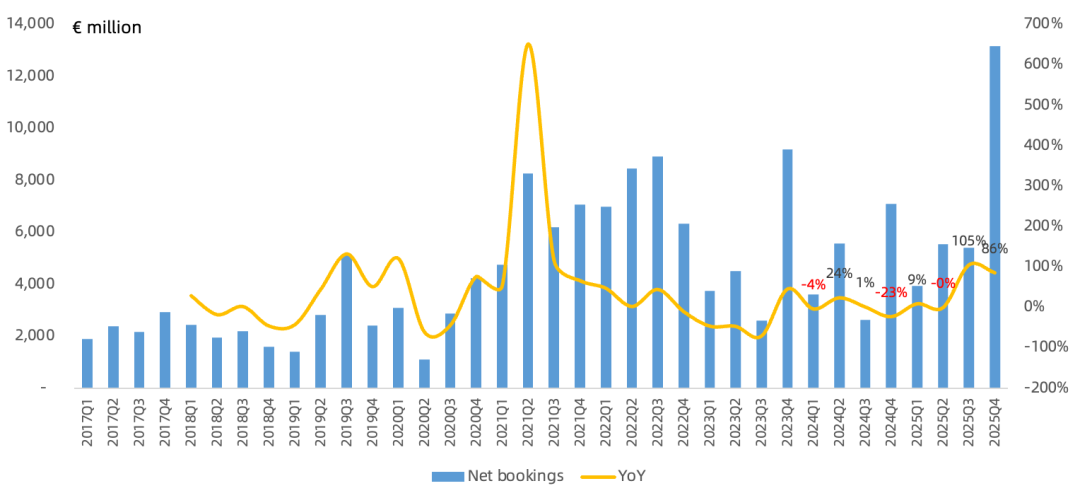

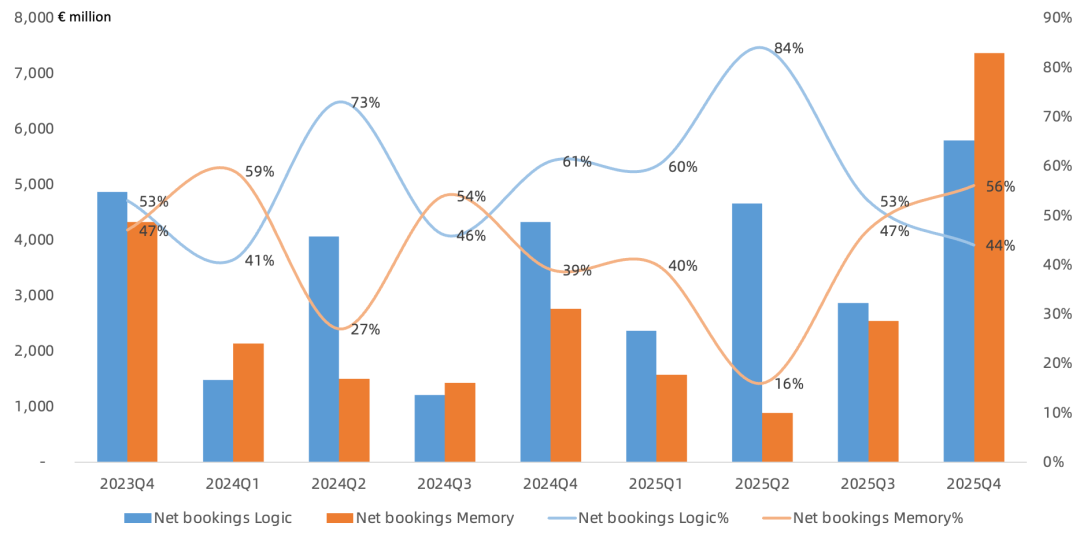

Q4 net bookings of €13.2B, up 86% year over year, far above consensus of €6.8B, of which EUV €7.4B, up 147% year over year. Breaking down net bookings composition: memory share jumped to 56%, up 17 percentage points year over year; logic 44%. In absolute terms, the memory capacity expansion wave has officially begun. Memory net bookings this quarter were €7.34B, up 167% year over year, a multi-year high.

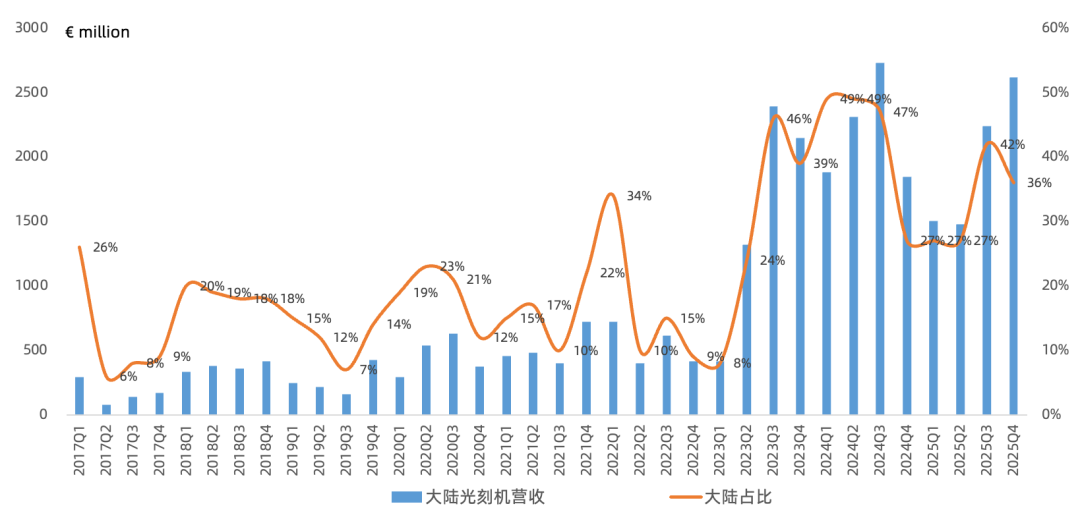

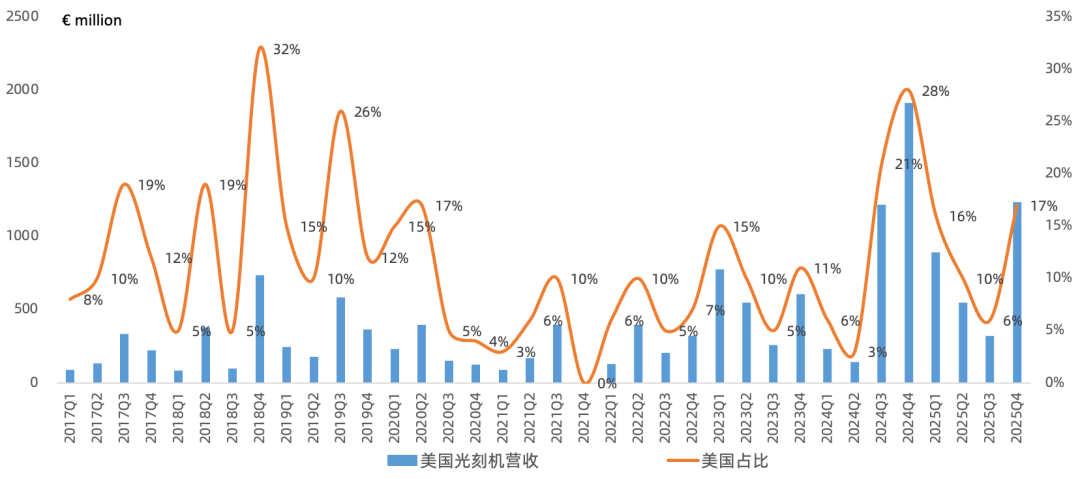

Mainland China single-quarter lithography revenue of €2.6B, up 42% year over year, 36% of lithography revenue, remaining ASML's largest customer region this quarter. However, management indicated 2026 Mainland China revenue share will decline to around 20%.

Outlook:

Projected Q1 revenue of €8.2-8.9B, up 6-15% year over year; installed base revenue €2.4B; Q4 gross margin 51-53%; implied net income of €2.45B at revenue midpoint, up 4% year over year.

Projected 2026 revenue of €34-39B, up 4-19% year over year; gross margin 51-53%; EUV business to grow significantly; non-EUV business flat; metrology tool demand within non-EUV very strong.

On the earnings call, management still expects 2026 logic market to grow on AI demand explosion, and memory market to continue strong growth driven by HBM/DDR5.

Installed base expected to keep growing in 2026, benefiting from rising EUV installed base and significant customer upgrade demand, as this is the simplest and fastest way for customers to gain additional output capacity.

Most puzzling: despite such above-expectations net bookings, management maintained the 2030 revenue target of €44-60B unchanged, gross margin 56-60%. At midpoint, this implies ASML 2025-2030 revenue CAGR below 10%, net income CAGR only 6%. Whether this was already baked into management's expectations or they are saving room for future upward revisions is unknown.

Recap of Prior 24Q3 View:

ASML's biggest issue at this stage is growth. ASML's 2024 results showed no growth; if 2025 revenue comes in at €30-35B, combined with gross margin and OpEx guidance, net income optimistically reaches only ~€9B, which at the current market cap still looks expensive.

While ASML's monopoly position is unchallenged, that does not mean lithography demand grows linearly, nor does it directly capture the AI demand explosion. TSMC, positioned in midstream manufacturing, can directly interface with downstream AI customers and capture the full AI dividend.

Due to the unique position of lithography in the supply chain, ASML's growth in recent years has been constrained by weak memory customers, relying mainly on the Mainland China mature-node expansion wave and TSMC's expansion wave to drive growth.

Despite mediocre guidance growth, the memory expansion wave driving massively above-expectations net bookings eased near-term growth concerns, and combined with TSMC's above-expectations capex, lifted sentiment across the semiconductor equipment sector.