ASML, the lithography leader, reported Q2 earnings today:

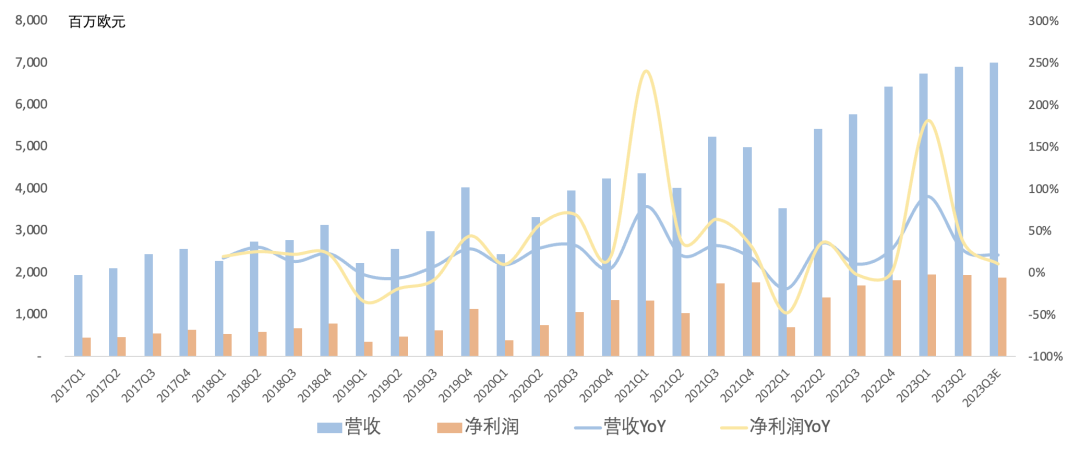

Revenue was €6.902B, up 27% year over year and 2% sequentially, setting a record high for the fifth consecutive quarter — a rarity in the semiconductor industry.

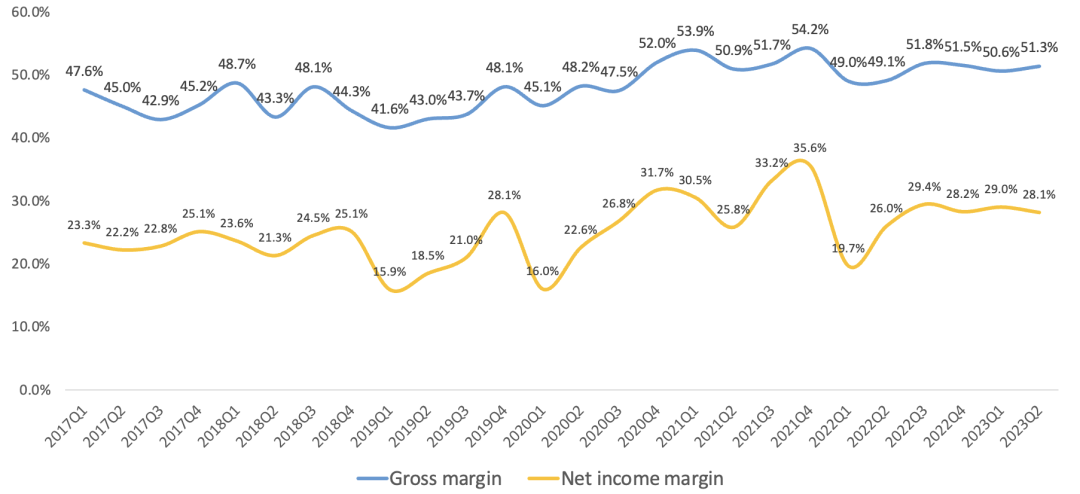

Gross margin was 51.3%, up 2.2 percentage points year over year and 0.7 percentage points sequentially.

Operating income was €2.263B, up 37% year over year and 3% sequentially, a record high for the third consecutive quarter; operating margin was 32.8%.

Net income was €1.942B, up 38% year over year and slightly down sequentially; net margin was 28.1%.

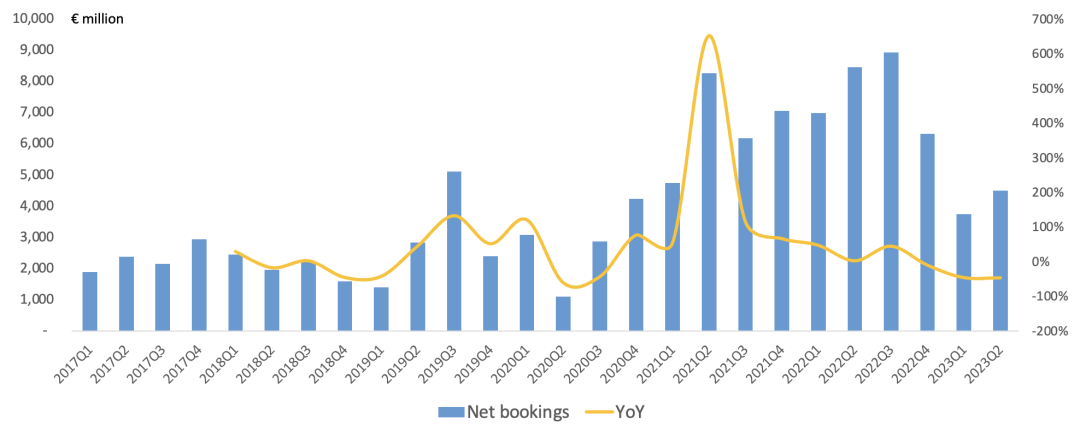

Backlog was €38B.

Q2 share repurchases of €500M.

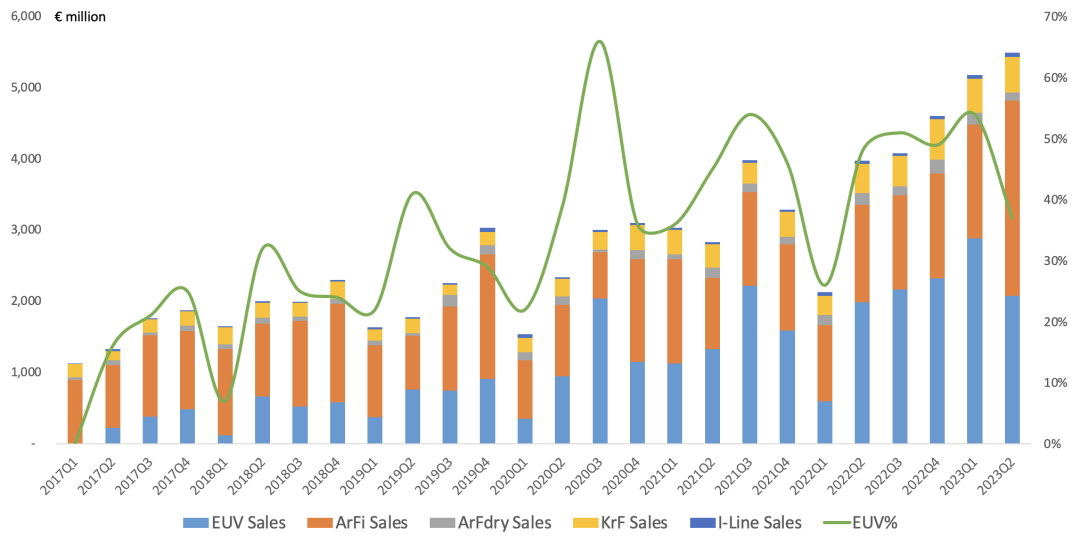

On the lithography side, Q2 shipped 113 systems in total:

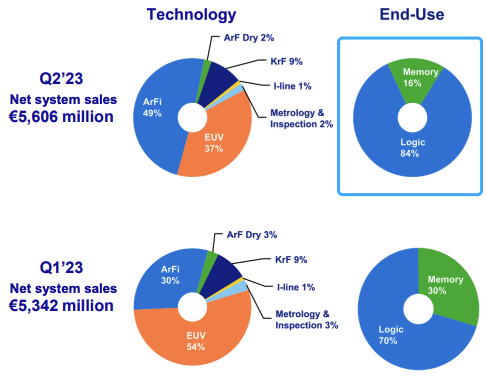

EUV: 12 systems, revenue €2.074B, 37% of system revenue, ASP €173M.

ArFi: 39 systems, revenue €2.747B, 49% of system revenue, ASP €70.43M.

ArF dry: 6 systems, revenue €112M, 2% of system revenue, ASP €18.69M.

KrF: 43 systems, revenue €505M, 9% of system revenue, ASP €11.73M.

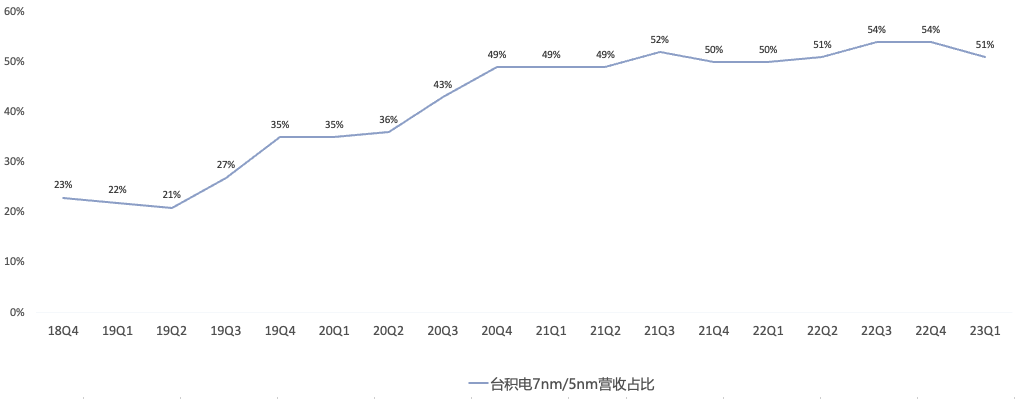

EUV shipments this quarter slowed due to a deceleration in advanced-node fab expansion, while immersion DUV demand exceeded expectations; immersion DUV revenue exceeded EUV for the first time in nearly five quarters. By comparison, TSMC's 7nm/5nm share trend basically mirrors ASML's EUV share trend.

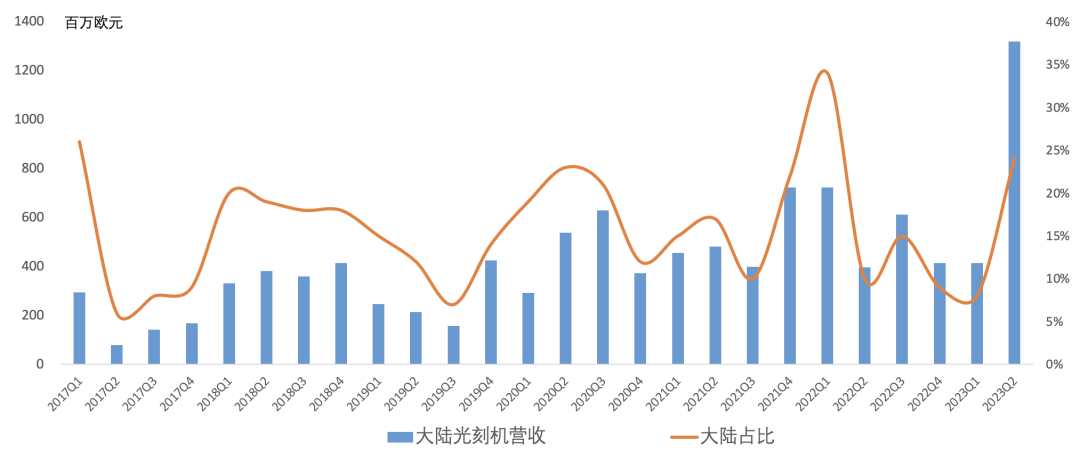

The biggest highlight this quarter was the China market. As ASML previously indicated, China lithography revenue exploded as expected, reaching €1.319B in a single quarter, up 232% year over year, a record high; lithography revenue share rose from 8% in Q1 to 24%.

ASML stated China demand surged because China fab expansion timing differs from the rest of the world. "Our Chinese customers say: We are happy to take the machines that others don't want. Because their fabs are ready."

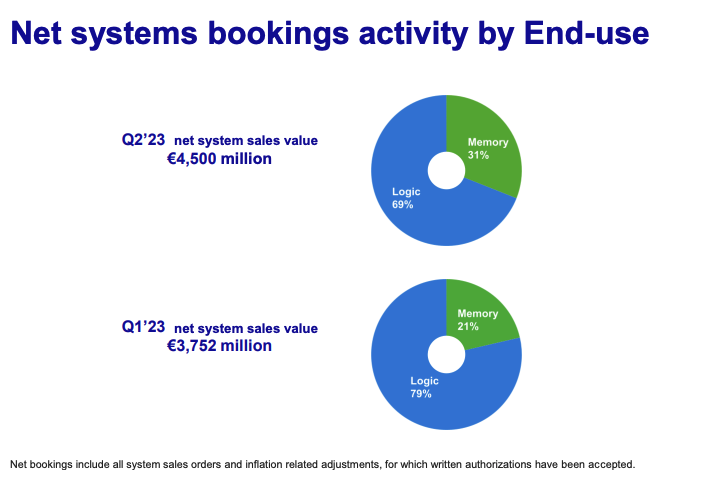

Due to continued memory capex contraction, memory revenue share fell to 16%, logic rose to 84%, an extreme split. Looking at bookings, memory share warmed slightly to 31%, up 77% sequentially, confirming memory has indeed bottomed.

Regarding ASML export controls, they currently target only NXT:2000i and above; NXT:1980i is unaffected, but still awaiting the latest US restrictions; management expects no material impact on results.

Outlook:

Q3 revenue guided to €6.5B–€7B, up 12%–21% year over year. Full-year revenue ~€27.5B, up 30% year over year, with EUV growth revised from 40% to 25%, DUV growth revised from 30% to 50%, and installed base business growth revised from 5% to flat.

Q3 gross margin guided at 50%; full-year gross margin slightly up year over year.

Full-year DUV shipments expected to exceed 375 systems, driven by strong immersion demand.

2023 fast shipments allow recognition of an additional €700M revenue; ~€2.3B of 2023 fast shipments deferred to 2024, primarily EUV products.

2025 revenue target €30-40B, gross margin 54%-56%; 2030 revenue target €44-60B, gross margin 56%-60%, on track.

Overall, ASML achieving 30% full-year growth in a semiconductor downcycle is exceptional. While EUV demand deceleration will draw investor criticism, I view this demand as merely "deferred" — the advanced-node arms race will not pause. Let's see how TSMC, under immense pressure as the advanced-node leader, guides for the full year tomorrow.