Previously, the key issue for ASML was always identified as growth. Management previously indicated 2026 results might not grow; this quarter they upgraded to growth being achievable.

ASML Q3 Earnings:

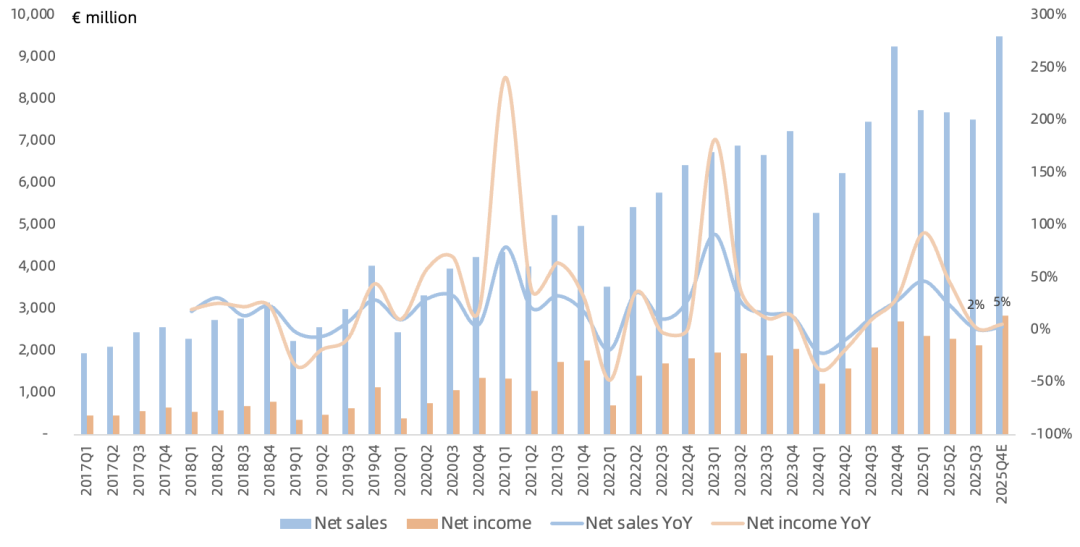

Revenue was €7.52B, up 1% year over year and down 2% sequentially, below consensus of €7.71B, at the low end of the prior guidance range of €7.4-7.9B.

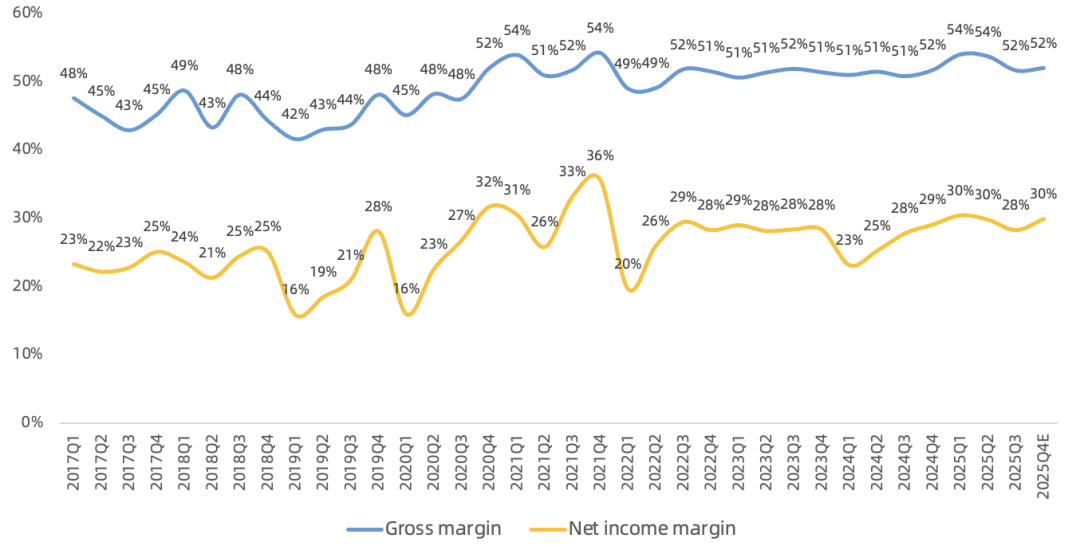

Gross margin was 51.6%, up 0.8 percentage point year over year and down 1.1 percentage points sequentially, above consensus of 51.4%, at the high end of the prior guidance range of 50-52%.

Net income was €2.13B, up 2% year over year and down 7% sequentially. Net margin was 28.3%.

Q3 share repurchases were €150M, the third consecutive quarter of buybacks. A new buyback program is expected to be announced in January 2026.

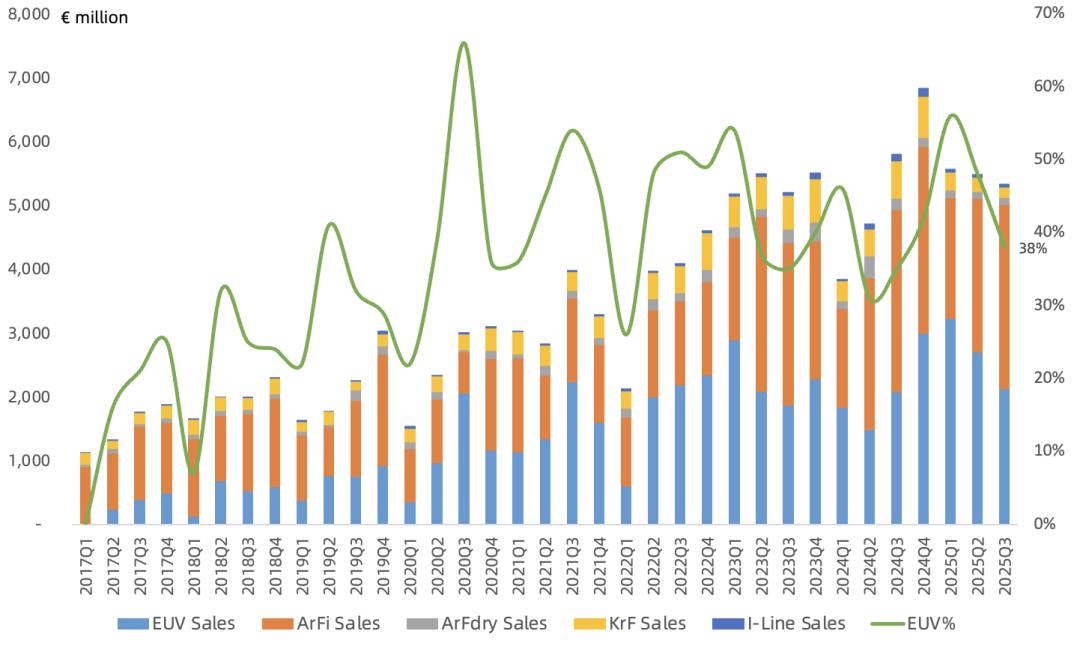

Lithography System Details: Q3 shipped 72 systems total, down 38% year over year:

EUV: 9 systems. Revenue €2.11B, 38% of system revenue. ASP €230M.

ArFi: 38 systems. Revenue €2.89B, 52% of system revenue. ASP €76M.

ArF dry: 4 systems. Revenue €110M, 2% of system revenue. ASP €27.77M.

KrF: 11 systems. Revenue €170M, 3% of system revenue. ASP €15.15M.

I-Line: 10 systems. Revenue €56M, 1% of system revenue. ASP €5.55M.

EUV revenue share declined again this quarter. One High-NA EUV system was recognized in revenue this quarter, which pressured gross margin. Customers report High-NA EUV maturity is higher than Low-NA EUV at the same stage. SK Hynix announced on September 3 that it has installed the memory industry's first High-NA EUV EXE:5200B at its Icheon M16 fab in Korea.

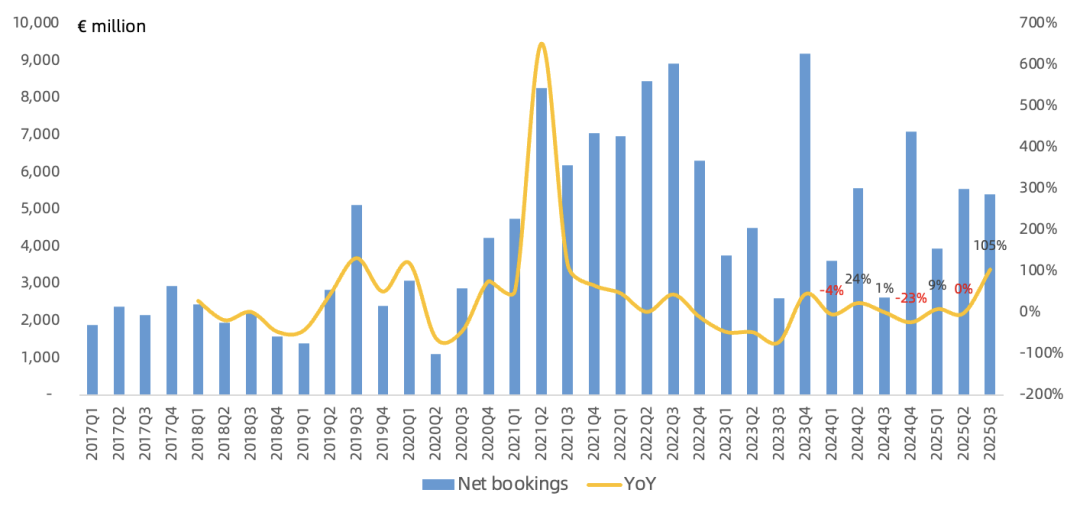

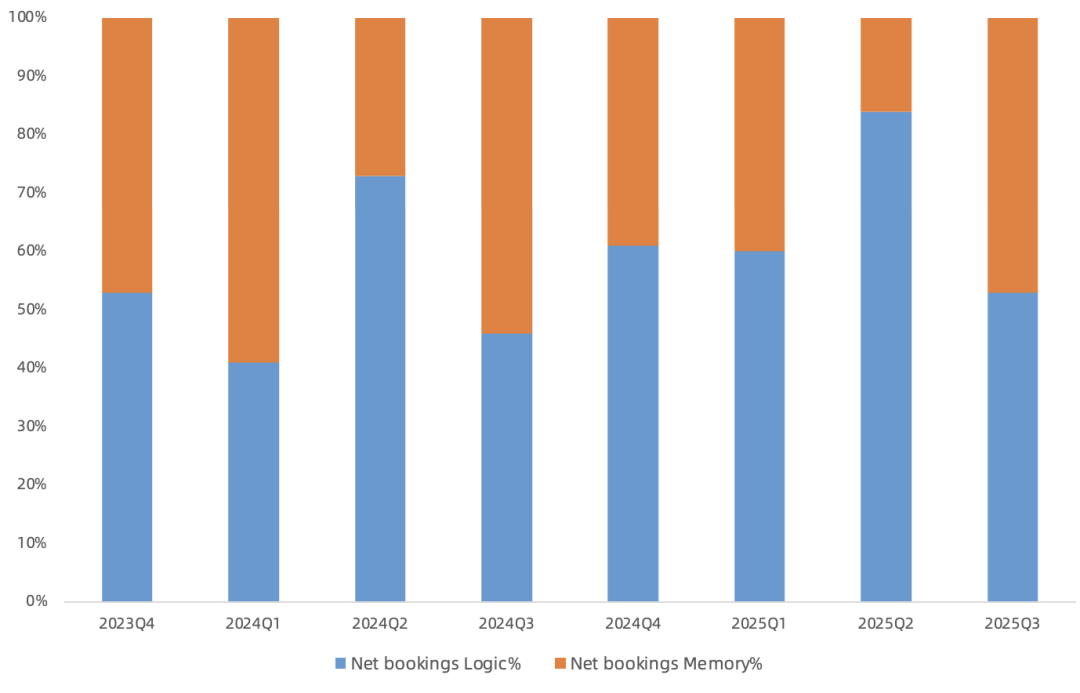

Net bookings this quarter were €5.4B, up 105% year over year, of which EUV was €3.6B, up 157% year over year. Logic and Memory accounted for 53%/47% of net bookings, with Memory share up 31 percentage points sequentially.

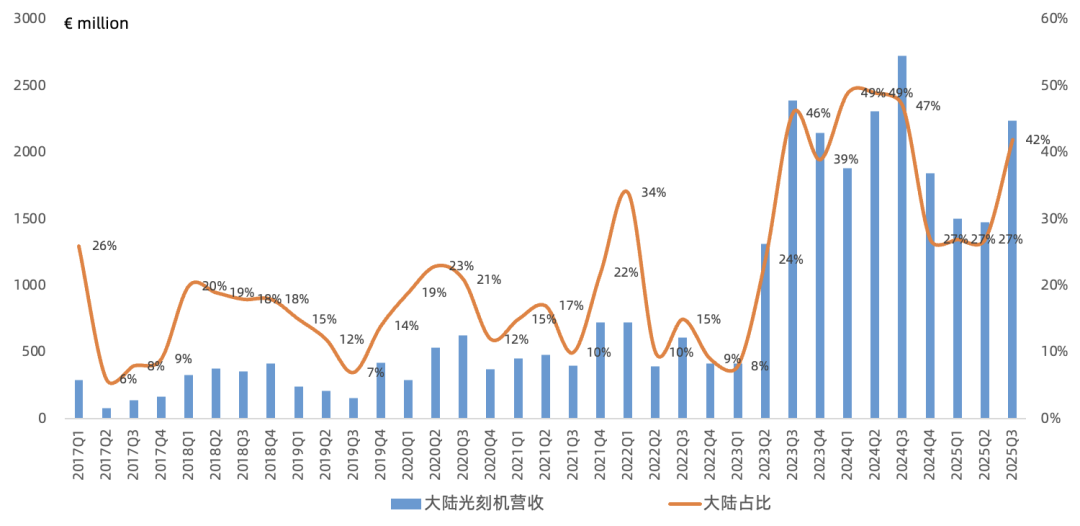

Mainland China lithography revenue this quarter was €2.2B, down 18% year over year, representing 42% of lithography revenue, making it ASML's largest customer region this quarter, unexpectedly exceeding management's prior full-year guidance of 25% revenue share from Mainland China.

Outlook:

Q4 guidance: Revenue €9.2-9.8B, down 1% to up 6% year over year. Installed base revenue €2.1B. Q4 gross margin 51-53%. Two High-NA EUV systems will be recognized in Q4, pressuring gross margin.

2025 revenue maintained at €32.5B, up 15% year over year. Gross margin maintained at 52%.

2026 Mainland China revenue expected to decline significantly and will pressure gross margin (Mainland shipments are primarily high-margin DUV). However, 2026 full-year company revenue can maintain growth. EUV revenue share will increase. DUV will be weak due to Mainland China demand decline.

On the earnings call, management still expects the 2025 logic market to grow driven by AI demand explosion, and the memory market to continue strong growth driven by HBM/DDR5.

No new High-NA EUV orders for two consecutive quarters. Next wave of orders expected after second half of next year. From a shipment perspective, after 2028. Even by 2030, High-NA EUV will still pressure company gross margin.

First advanced packaging lithography system XT:260 shipped. Based on I-Line technology. Efficiency up to 4x.

Management maintains 2030 revenue target of €44-60B unchanged, gross margin 56-60%. At the midpoint, ASML 2025-2030 revenue CAGR is under 10%, net income CAGR only 6%.

Maintaining Previous 24Q3 View:

ASML's biggest issue at this stage is growth. ASML's 2024 results showed no growth; if 2025 revenue comes in at €30-35B, combined with gross margin and OpEx guidance, net income optimistically reaches only ~€9B, which at the current market cap still looks expensive.

While ASML's monopoly position is unchallenged, that does not mean lithography demand grows linearly, nor does it directly capture the AI demand explosion. TSMC, positioned in midstream manufacturing, can directly interface with downstream AI customers and capture the full AI dividend.