In last quarter's ASML article, I noted that ASML's 2024 results would show no growth, with the inflection expected in 2025; this quarter is no different.

Lithography leader ASML reports Q2 results:

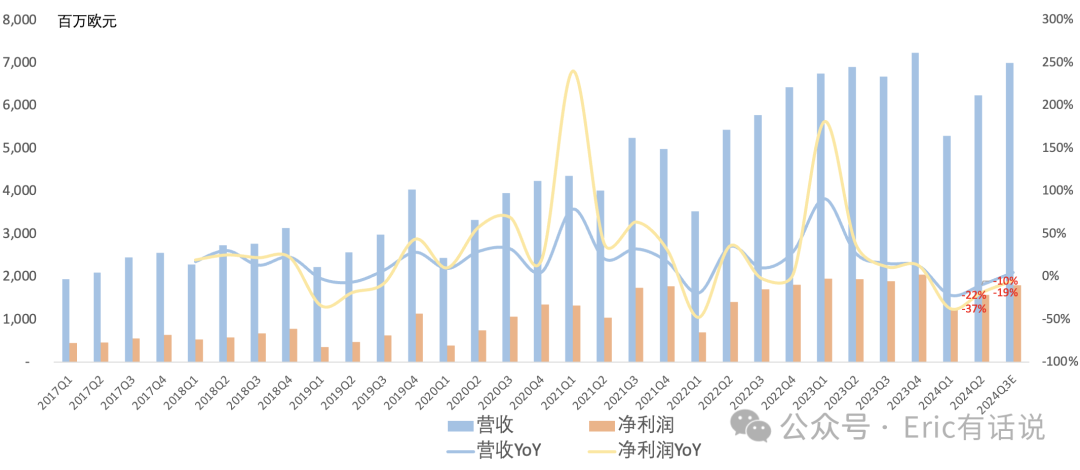

Revenue was €6.24B, down 10% year over year and up 18% sequentially, in line with the upper end of prior guidance.

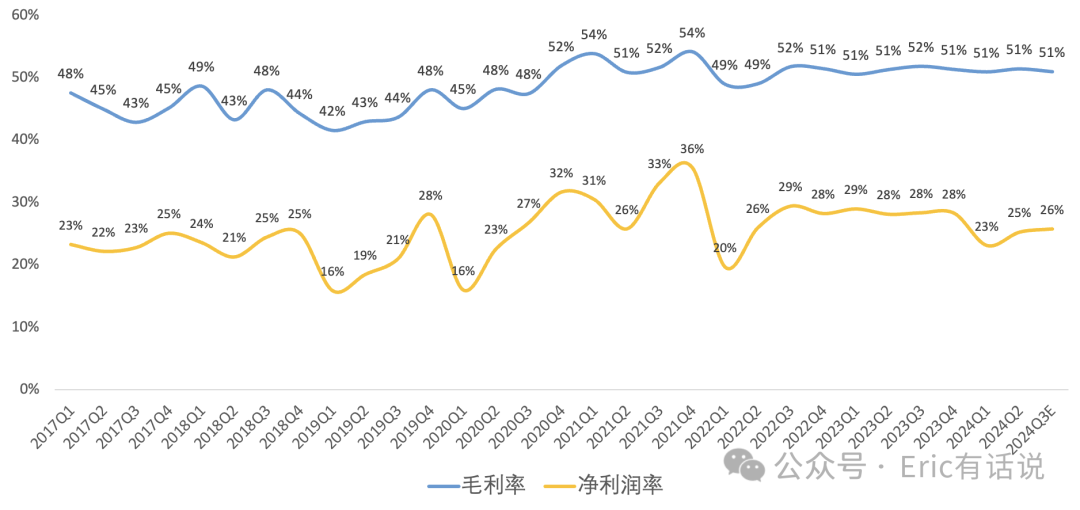

Gross margin was 51.5%, up 0.2 percentage points year over year and 0.5 percentage points sequentially.

Operating profit was €1.84B, down 19% year over year and up 32% sequentially, with an operating margin of 29.4%.

Net income was €1.58B, down 19% year over year and up 29% sequentially, with a net margin of 25.3%.

Q2 share repurchases were €96M.

Q2 backlog was €39B, up €1B sequentially.

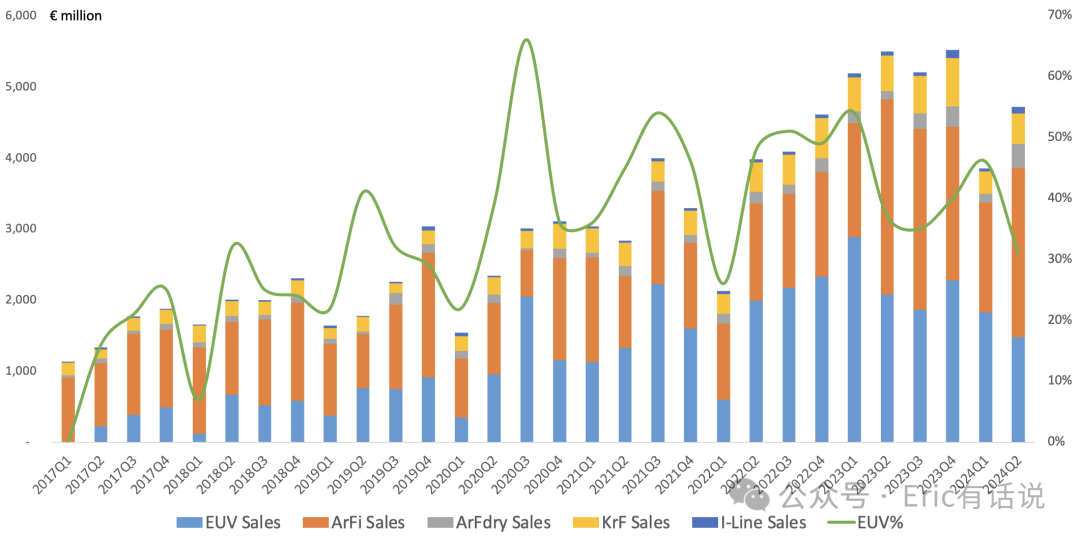

On the lithography front, Q2 shipped 100 systems, down 12% year over year in total:

EUV: 8 units, revenue of €1.476B, accounting for 31% of system revenue, ASP of €184M.

ArFi: 32 units, revenue of €2.381B, accounting for 50% of system revenue, ASP of €74.39M.

ArF dry: 11 units, revenue of €333M, accounting for 7% of system revenue, ASP of €30.3M.

KrF: 33 units, revenue of €428M, accounting for 9% of system revenue, ASP of €12.98M.

I-Line: 16 units, revenue of €95M, accounting for 2% of system revenue, ASP of €5.95M.

EUV revenue share plunged this quarter, while DUV share exceeded 50%; Q2 also shipped a 0.33 NA NXE:3800 system, which is expected to continue ramping and become the EUV revenue mainstay in the second half; the company says customer demand for High-NA is strong, with both memory and logic customers in qualification.

ASML's EUV remains weak while TSMC's advanced-node revenue share stays high, so the near-term correlation between ASML and TSMC results has diverged sharply. Following TSMC's announcement that N2 will not use High-NA EUV, last quarter it also disclosed that A16, slated for 2026 volume production, will not use High-NA EUV either.

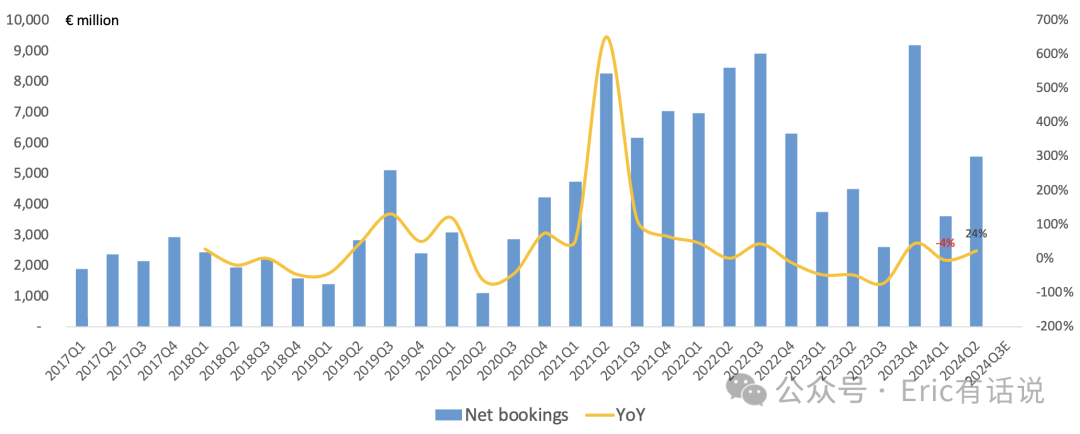

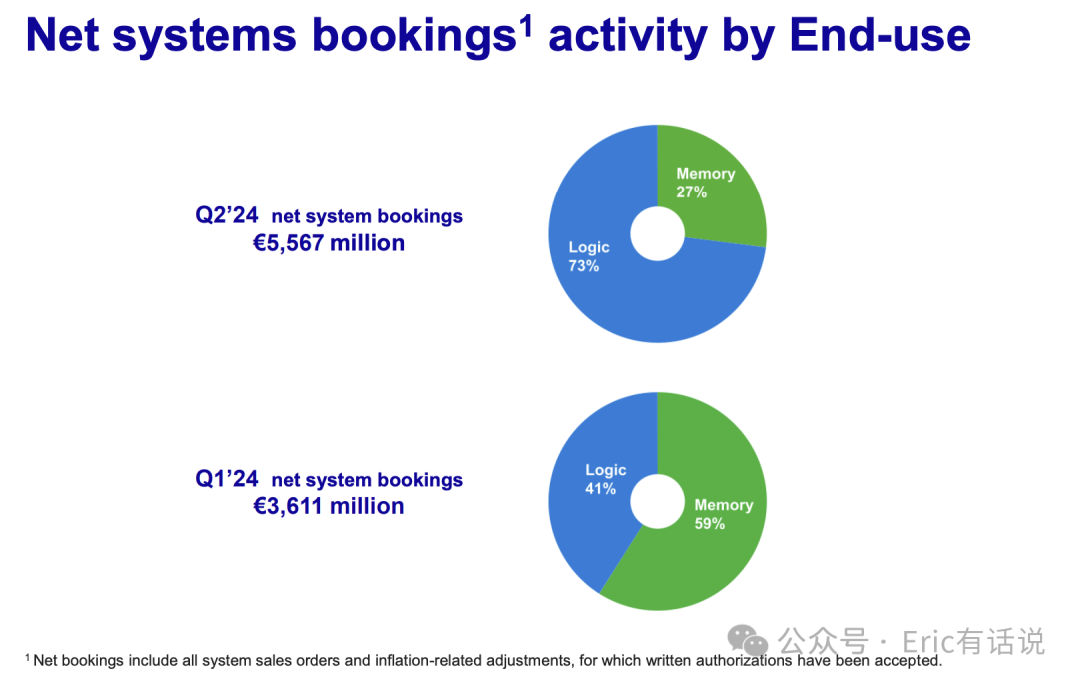

This quarter's bookings were €5.567B, up 24% year over year, of which EUV bookings were €2.5B, up 56% year over year and 281% sequentially, signaling a recovery.

Management previously indicated that to maintain the 2025 revenue target of €30-40B, each remaining quarter in 2024 would need bookings above €4B.

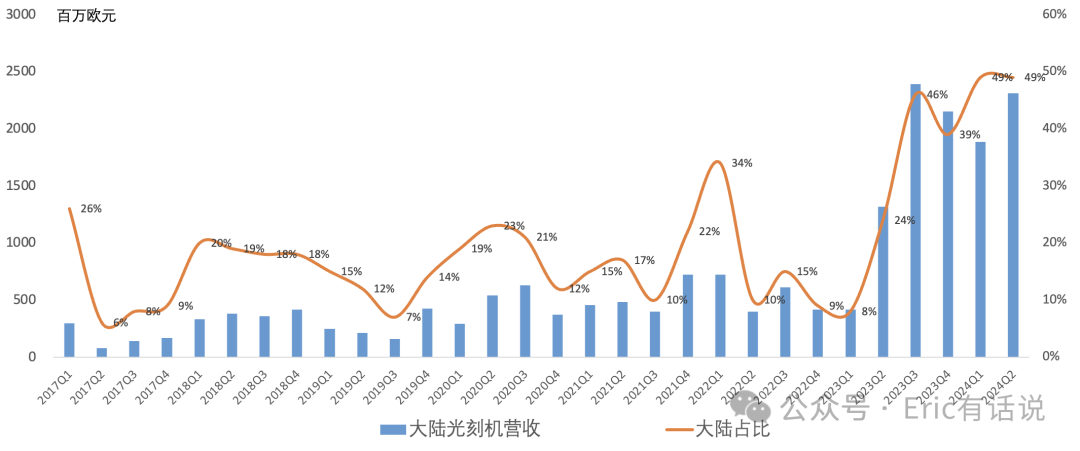

Mainland China lithography revenue remained elevated this quarter at €2.31B, up 75% year over year, accounting for 49% of system revenue, making it ASML's largest customer region for the fourth consecutive quarter.

Outlook:

Q3 revenue is guided at €6.7-7.3B, up 0-9% year over year; full-year revenue is expected to be flat year over year, with second-half revenue exceeding the first half.

Q3 gross margin is guided at 50-51%; full-year gross margin is expected to decline slightly year over year.

The semiconductor industry ex-AI is expected to recover in the second half.

Full-year logic revenue is expected to decline slightly year over year, while memory revenue is expected to grow year over year, driven by strong advanced DDR5 and HBM demand; Installed Base Management revenue is expected to be flat year over year.

The 2025 revenue target of €30-40B and the 2030 target of €44-60B are maintained, with an update expected at the November Investor Day.

As noted in the prior two quarters, ASML's core issue at this stage is growth. With 2024 revenue flat, the 2025 target of €30-40B implies 9-45% growth; even at a peak historical net margin, net income would optimistically reach €10B, suggesting the current market cap is clearly overvalued.

By comparison, tomorrow's TSMC earnings are more worth anticipating.