Qualcomm FY25 Q3 corresponds to actual period Apr/May/Jun 2025.

Qualcomm FY25 Q3 Earnings:

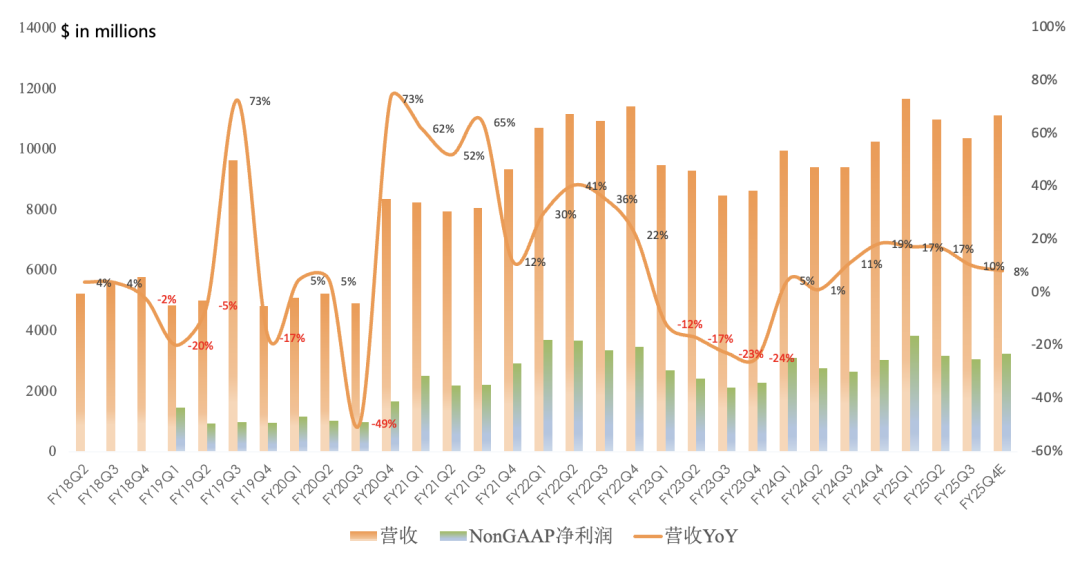

Revenue $10.4B, up 10% year over year, down 6% sequentially, second consecutive quarter of sequential decline.

GAAP gross margin 56%, flat year over year, up 0.6 pp sequentially.

GAAP net income $2.7B, up 25% year over year, down 5% sequentially (peak was FY22 Q3 $3.7B).

Non-GAAP net income $3.0B, up 15% year over year, down 4% sequentially (peak was FY25 Q2 $3.8B).

Expected FY25 Q4 revenue of $10.3-11.1B, up 1%-8% year over year; net income midpoint of $2.6B, down 12% year over year; Non-GAAP net income midpoint of $3.1B, up 3% year over year.

The company paid $967M in dividends and repurchased $2.8B of shares this quarter.

The top customer contributed 21% of revenue, the second 18%, and the third 13%; the top three customers combined accounted for 52% of revenue.

Business Segments:

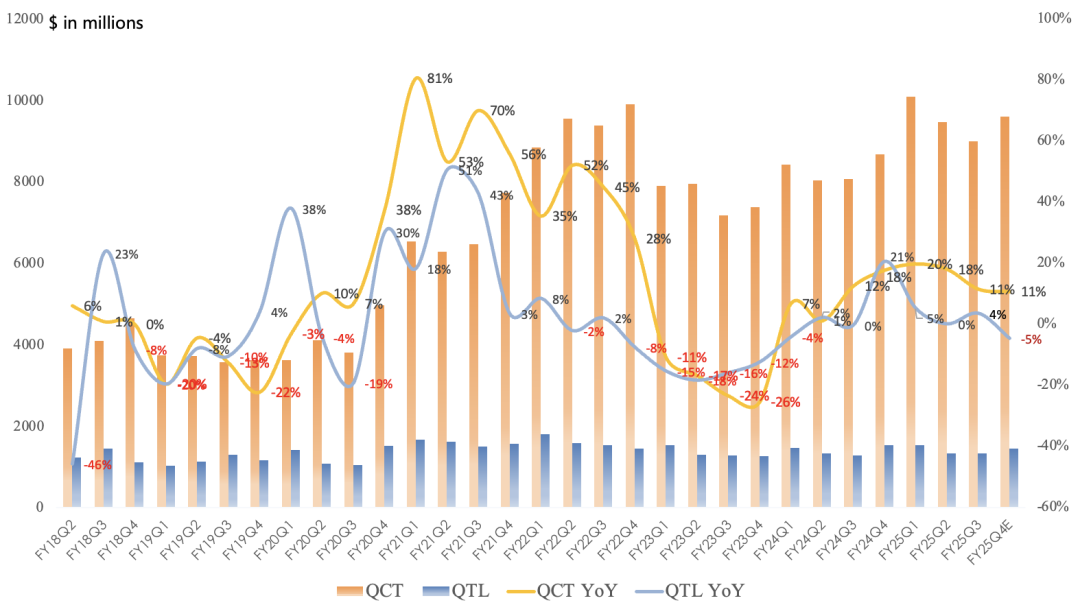

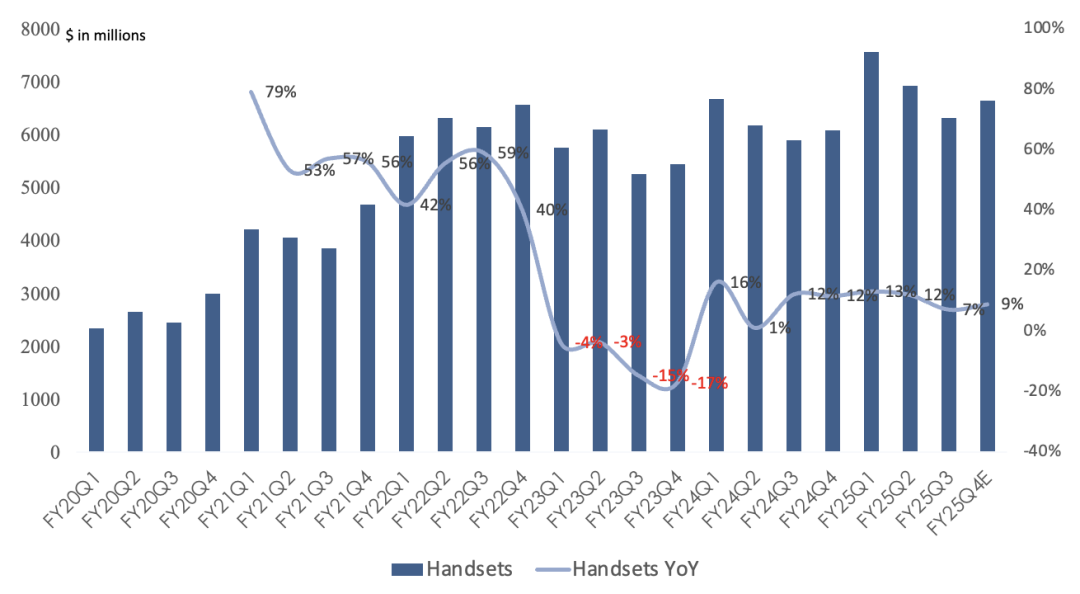

Handset revenue was $6.328B, up 7% year over year and down 9% sequentially, representing 61% of revenue; Qualcomm expanded its partnership with Xiaomi through a multi-year agreement; the Samsung agreement has locked in a new baseline of roughly 75% share for Qualcomm, with any amount above that being upside.

Management expects FY25 to mark the second consecutive year of over 15% year-over-year growth in QCT non-Apple revenue; Android revenue in FY25 grew approximately 10% versus FY24.

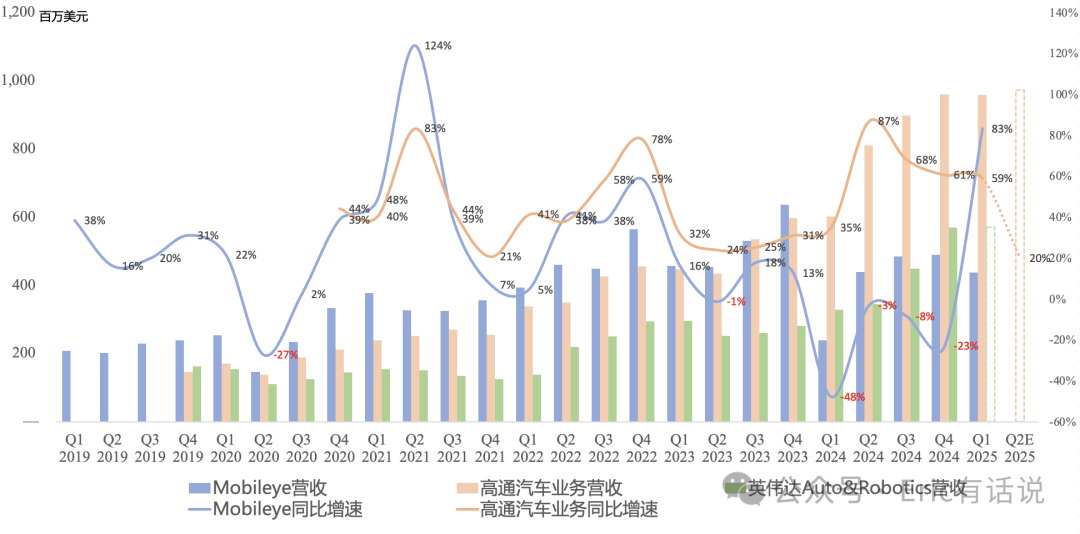

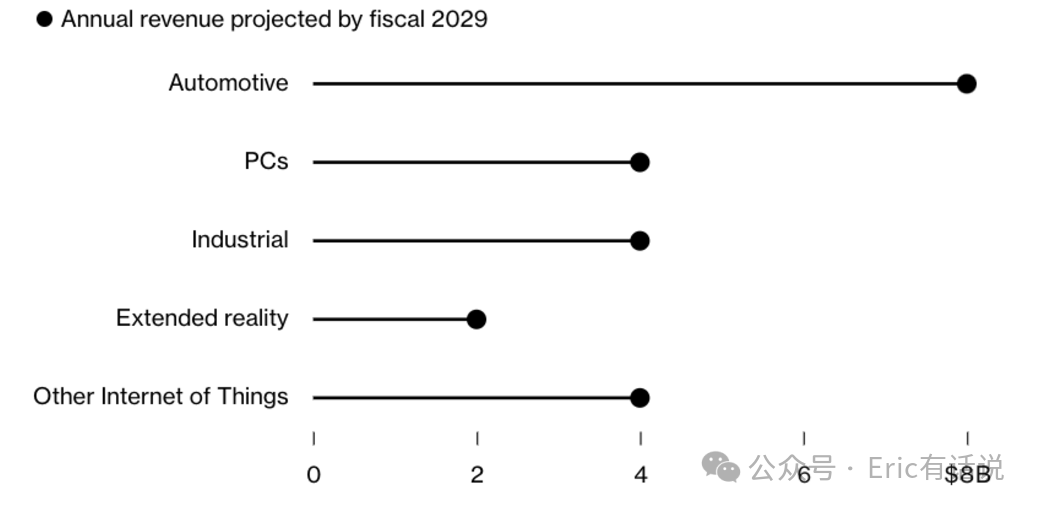

Automotive revenue was $984M, up 21% year over year and 9% sequentially, marking the 19th consecutive quarter of double-digit year-over-year growth, and accounting for 9% of revenue; the company secured 12 ADAS design wins this quarter; it maintains the FY29 automotive revenue target of $8B.

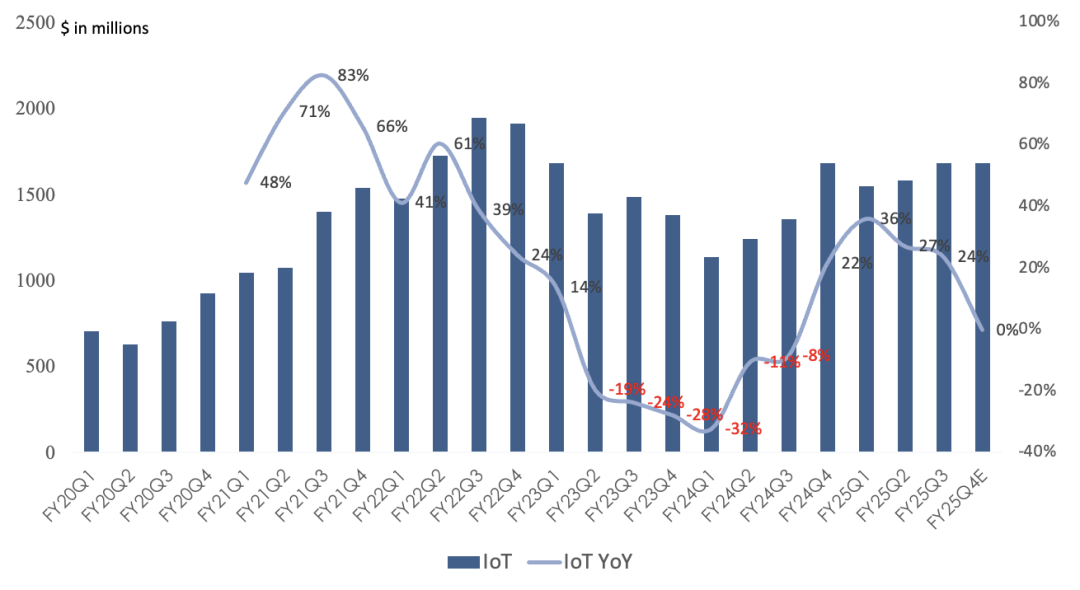

IoT revenue was $1.681B, up 24% year over year, representing 16% of revenue; the FY29 IoT revenue target of $4B is maintained; X Elite/Plus series captured 9% share of the >$600 Windows notebook market in the top five countries in the US/Europe in Q1; the FY29 Windows PC revenue target of $4B is maintained, with a $35B SAM and 12% share target; Meta AI smart glasses demand continues to exceed expectations, driving increased demand for the Snapdragon AR1 chipset; the FY29 XR revenue target of $2B, led by smart glasses, is maintained.

Next quarter handset revenue is expected to grow 9% year over year and 5% sequentially, driven primarily by Android; IoT revenue is expected to be flat year over year and sequentially; automotive revenue is expected to be $1B, up 17% year over year.

The biggest highlight on the earnings call was the $2.4B acquisition of AlphaWave, expected to close in 2026, with the goal of entering the data center CPU and AI inference chip markets by FY28; the Orion CPU can integrate with NVIDIA GPUs, leveraging the NVIDIA NVLink Fusion architecture to build high-performance AI factories — although this opportunity will take a long time to materialize, it resonates better with the market than the IoT narratives.

At present, FY25 net income stands at $11.3B; applying a 10-year average valuation midpoint of 17x P/E yields a rough valuation of approximately $190B.

Overall, Qualcomm's quarterly results were mediocre, weighed by handset volumes, and the persistently high-growth automotive business is set to decelerate sharply. With Apple's in-house modem progress accelerating (the iPhone 17 series launches next quarter, yet sequential growth is driven by Android, implying severe Apple share loss), Qualcomm may have only one year to fill the Apple revenue gap. Long term, focus should be on Qualcomm's data center progress post-AlphaWave acquisition, as the traditional handset, PC, and automotive lanes offer limited runway.