Qualcomm FY26 Q1 corresponds to calendar October/November/December 2025.

Qualcomm FY26 Q1 Results:

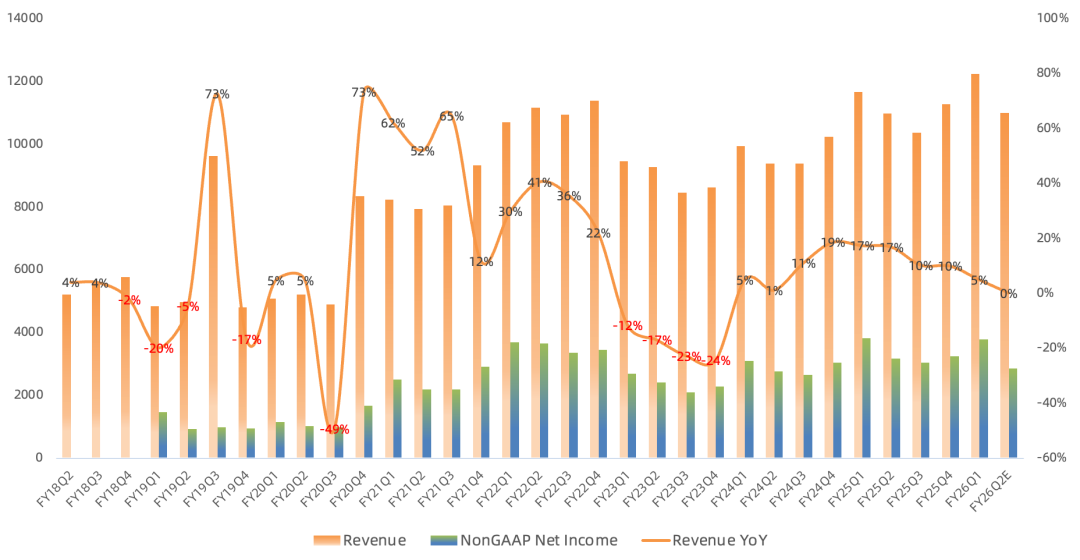

Revenue $12.25B, up 5% year over year and 9% sequentially.

GAAP gross margin 54.6%, down 1.2 percentage points year over year and 0.7 percentage points sequentially.

GAAP net income $3.0B, down 6% year over year; net margin 24.5% (net income peak was $3.7B in FY22 Q3).

Non-GAAP net income $3.78B, down 1% year over year, up 16% sequentially (net income peak was $3.8B in FY25 Q2).

Guiding FY26 Q2 revenue $10.2-11.0B, implying ~3% year-over-year decline at midpoint; Non-GAAP net income $2.64-2.86B, implying ~13% year-over-year decline at midpoint; first time since FY23 Q4 with two consecutive quarters of year-over-year declines.

$950M dividends and $2.65B repurchases this quarter.

Business Segments:

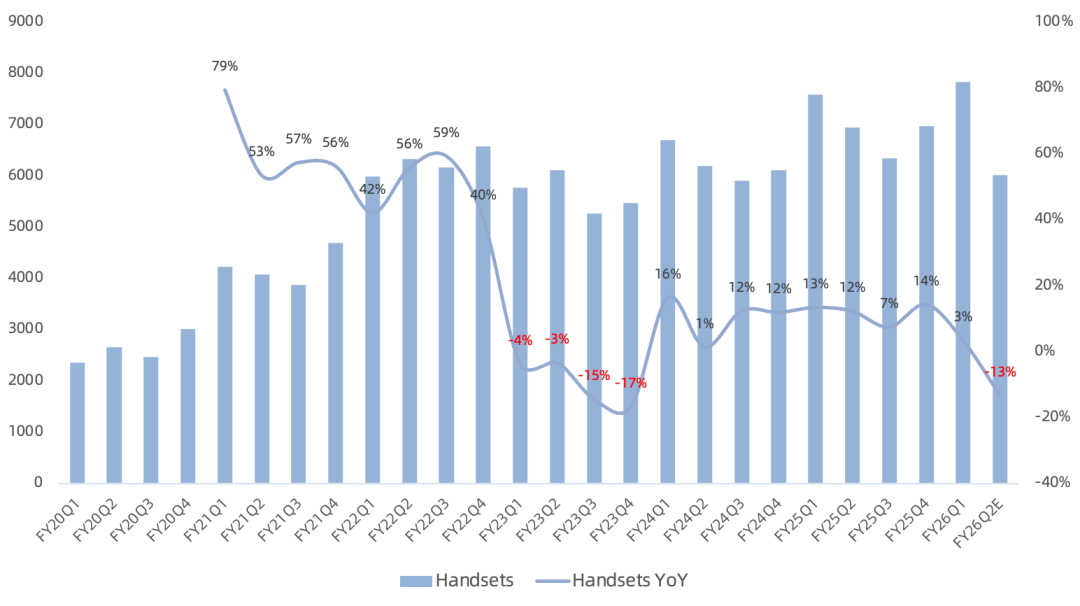

Handset revenue $7.82B, up 3% year over year, 64% of revenue; secured 75% share of Samsung's new flagship, in line with prior expectations; no progress in licensing negotiations with Huawei.

Observed healthy handset sell-through in FY26 Q1 and the first few weeks of 2026, but the handset industry will be constrained by memory (particularly DRAM) supply and pricing over the next several quarters; Chinese handset OEMs are cutting full-year production plans, reflected in Q2 guidance.

Although high-end handsets are more resilient to memory price increases, this is not just a price issue but an availability issue; management believes memory availability will determine the overall size of the FY26 handset market; Qualcomm processors support all memory suppliers including CXMT; advanced-node wafers also tight; management says handset revenue will return to prior run-rate and mid-term growth trajectory once memory supply-demand normalizes, but timing unknown.

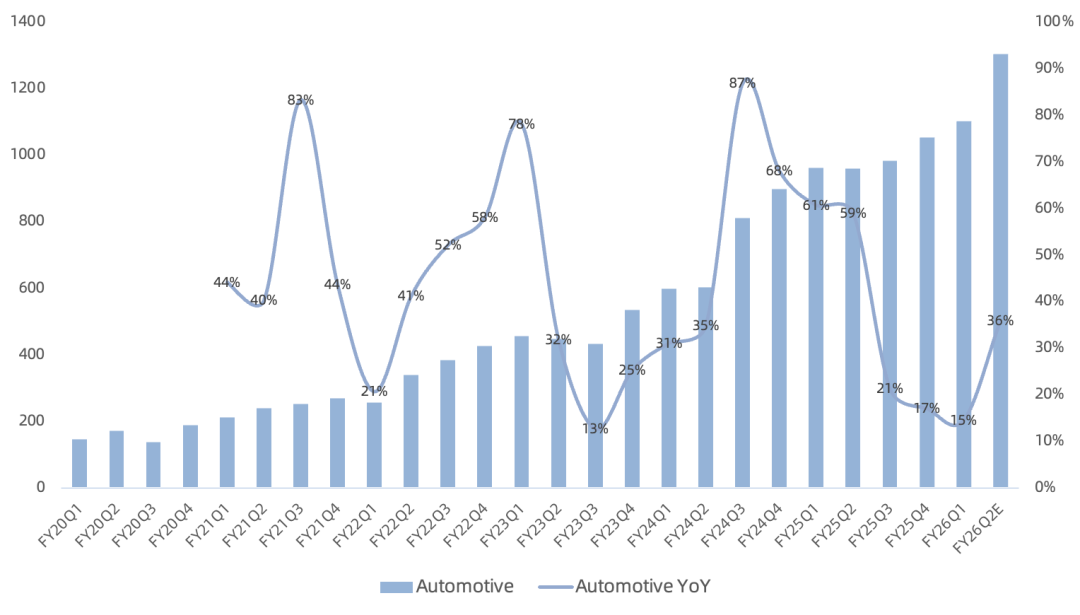

Automotive revenue $1.1B, up 15% year over year, growth continuing to decelerate, 9% of revenue; signed long-term supply framework agreement with Volkswagen Group covering multiple brands including Audi and Porsche; new Toyota RAV4 adopts Snapdragon Cockpit Platform; Elite platform design wins reach 10 projects; management guides Q2 year-over-year growth to accelerate further vs Q1, driven by share gains rather than industry tailwinds; automotive less sensitive to memory price increases; maintaining FY29 automotive revenue target of $8B.

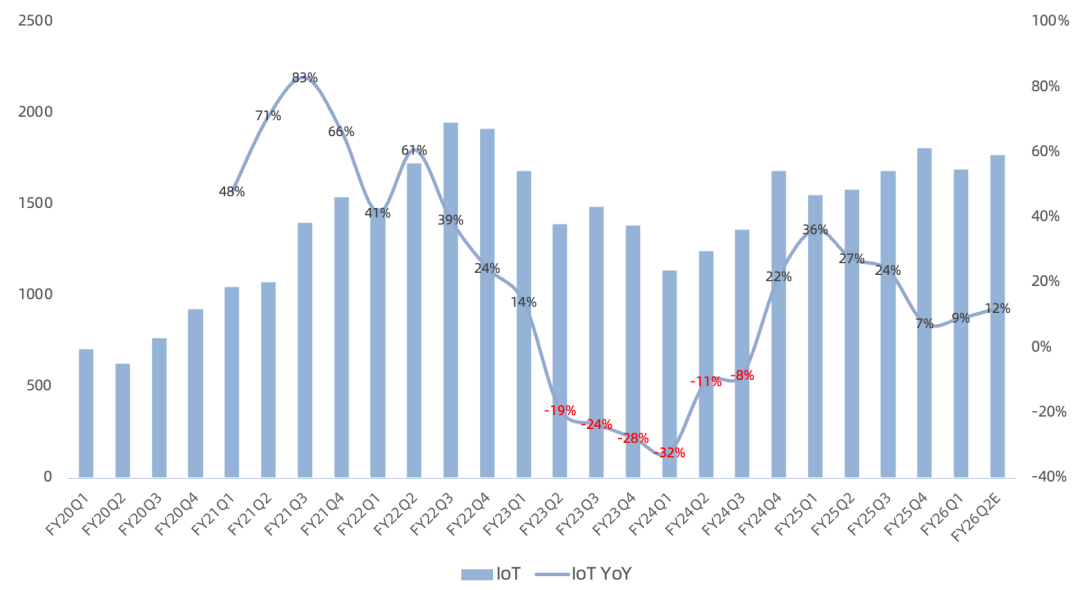

IoT revenue $1.69B, up 9% year over year, 14% of revenue; launched X2 Plus platform targeting enterprise commercial; X2 Elite Extreme features 18-core 3rd-gen Oryon CPU and 80 TOPS NPU, still on track for 150 designs with X Elite/Plus this year; Dragonwing IQ-X series marks entry into industrial PC; also announced expansion into advanced robotics with full robotics technology stack including Dragonwing IQ10 series; maintaining FY29 IoT revenue target of $14B.

Data center: Qualcomm states the only publicly announced data center customer is HUMAIN, progressing well with shipments underway; beyond Oryon (Arm), RISC-V CPU added to roadmap; future AI250 chip will use new memory architecture, details at Investor Day; maintaining guidance for data center revenue to ramp in FY27 (calendar 2026 Q4), with potential for multi-billion dollar revenue opportunity within a few years.

Continuing to develop data center solutions and collaborating with leading hyperscalers, cloud providers, sovereign AI projects, and other global partners; management encouraged by positive customer feedback on Qualcomm server CPUs and innovative AI processing and memory architectures for next-gen inference data centers.

Completed acquisition of Alphawave Semi, adding high-speed wired connectivity technology; acquired

Ventana Micro Systems, advancing high-performance RISC-V CPU development for data center workloads.

Guiding next quarter handset revenue $6B, down 13% year over year; automotive revenue $1.3B, up 35% year over year driven by share gains; IoT revenue ~$1.8B, up low-teens% year over year, driven primarily by industrial and consumer.

Overall, every Qualcomm business is either facing or approaching a growth ceiling, making AI a badly needed new growth engine. Geopolitical exposure adds another concern: mainland China represented 46% of FY25 revenue, versus just 24% from the United States and 21% from South Korea.

Qualcomm, already mired in a growth quagmire, faces a severe memory supply-demand imbalance that directly hits its core handset business. Despite management's optimistic guidance for sequential automotive acceleration next quarter and data center ramp in FY27, they were helpless when pressed by Wall Street on when memory supply-demand will normalize. Given current memory industry conditions, a full-year FY26 revenue and net income decline appears inevitable.