Qualcomm FY25Q2 corresponds to the actual period of January/February/March 2025.

Qualcomm FY25Q2 Earnings:

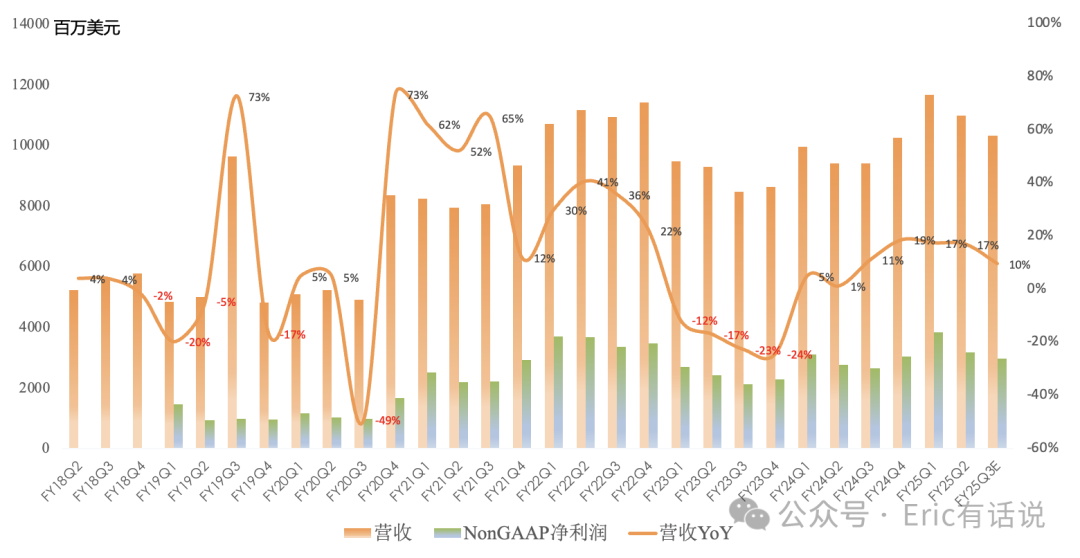

Revenue $11.0B, up 17% year over year, down 6% sequentially;

GAAP gross margin 55%, down 1.3 percentage points year over year, down 0.8 percentage points sequentially;

GAAP net income $2.8B, up 21% year over year, down 12% sequentially (net income peak was $3.7B in FY22Q3);

Non-GAAP net income $3.2B, up 15% year over year, down 17% sequentially (net income peak was $3.8B in FY25Q2);

Guiding FY25 Q3 revenue $9.9-10.7B, up 5%-14% year over year; net income midpoint $2.5B, up 16% year over year; Non-GAAP net income midpoint $3.0B, up 12% year over year;

Dividends of $938M and buybacks of $1.7B this quarter;

Top customer contributed 27% of revenue this quarter, second largest 18%, third largest 10%; top three customers combined contributed 55% of revenue;

Business Segments:

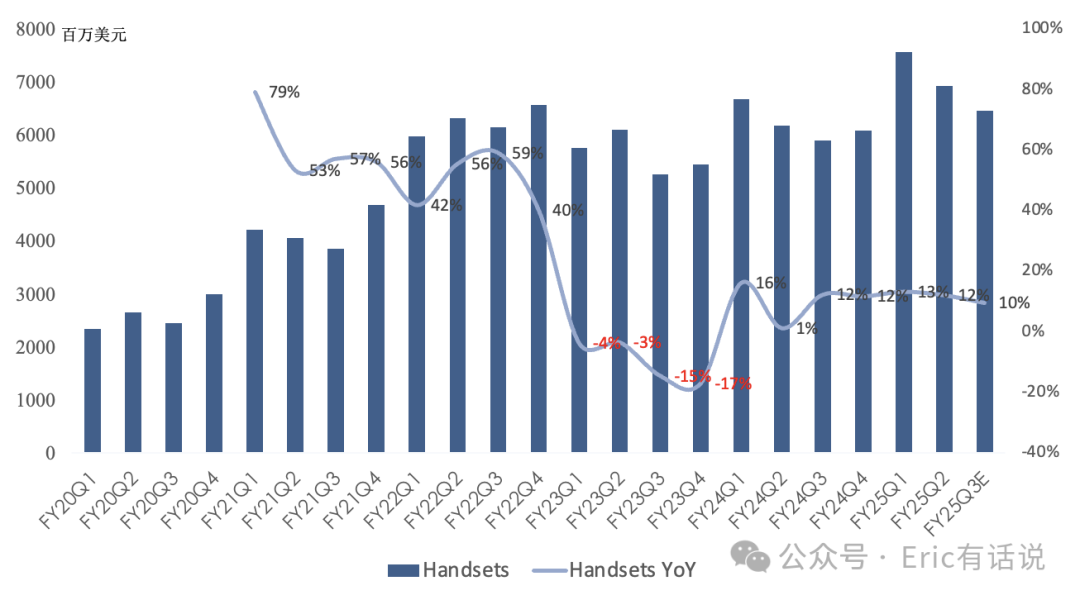

Handset revenue $6.929B, up 12% year over year, down 9% sequentially, accounting for 63% of revenue; This quarter benefited from China's consumer subsidies driving sustained growth in high-end Android flagship demand, but emerging market handset shipments remained weak; The X85 modem launched this quarter will only ship on Android platforms, with shipments in H2; No substantive advance orders received from customers at this time;

Management expects Apple iPhone 17 series modem share to decline to 70% this year, to 20% in 2026, and to 0% in 2027;

Huawei license renewal negotiations have made no progress and are not reflected in guidance;

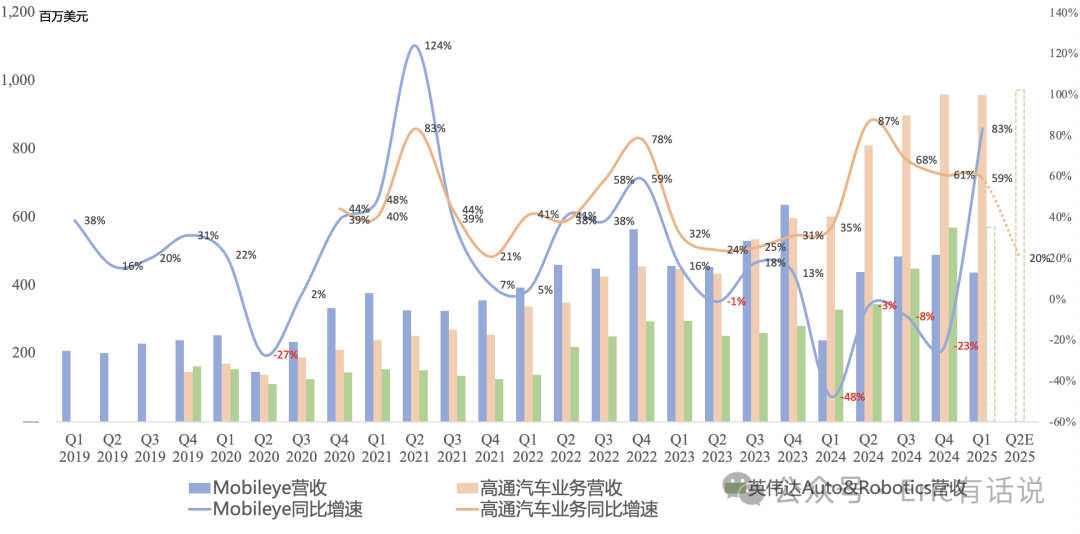

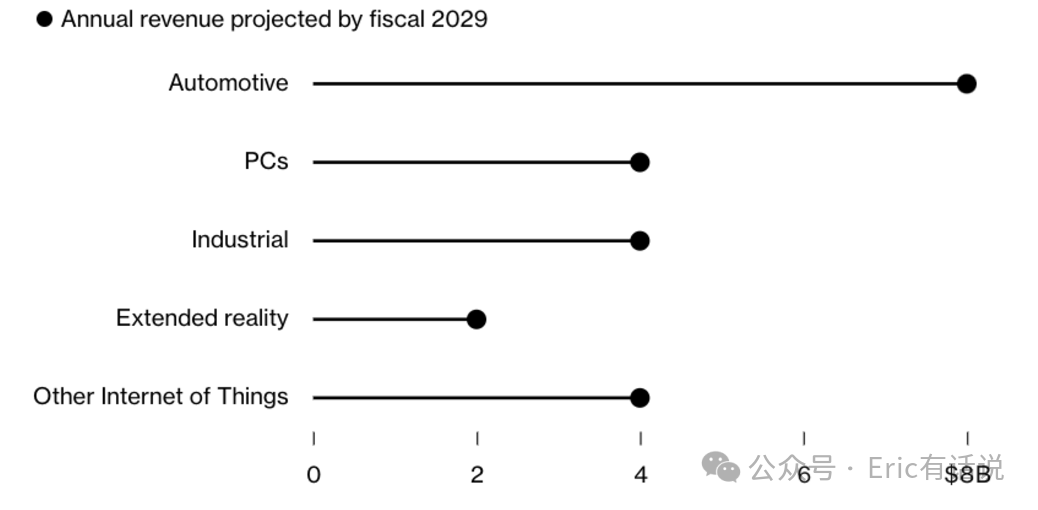

Automotive revenue $959M, up 59% year over year, down slightly sequentially, marking 18 consecutive quarters of double-digit year-over-year growth, accounting for 9% of revenue; Secured 5 ADAS design wins this quarter; Maintaining FY29 automotive revenue guidance of $8B;

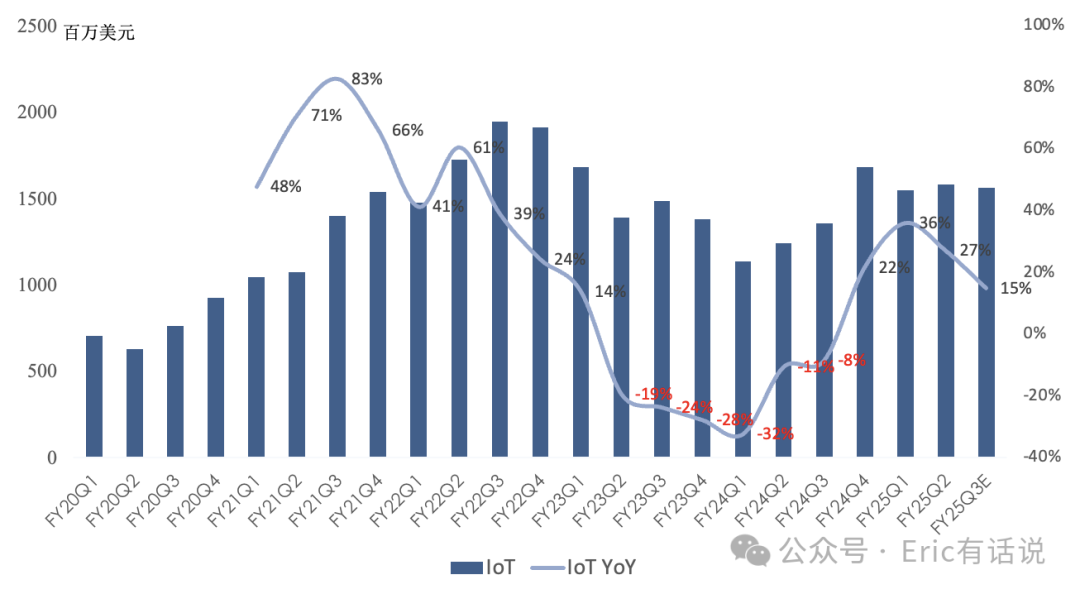

IoT revenue $1.581B, up 27% year over year, accounting for 14% of revenue; Consumer electronics, networking, and industrial all grew within IoT this quarter, with industrial contributing the most; Maintaining FY29 IoT revenue guidance of $4B; Acquired two edge computing companies this quarter, Edge Impulse and FocusAI; X Elite/Plus series captured 9% share of >$600 Windows notebooks in the US/Europe top five countries in Q1; Maintaining FY29 Windows PC revenue guidance of $4B, SAM $35B, market share 12%; Maintaining FY29 XR revenue guidance of $2B led by smart glasses;

Guiding next quarter handset revenue up 10% year over year, primarily driven by Android growth; IoT up 15% year over year, automotive up 20% year over year;

FY25 Q1-Q3 net income $8.5B, but FY25 Q4 (iPhone 17 series) profit outlook pending guidance. Using FY24 Q4 (iPhone 16 series) data, i.e., TTM net income $11.4B, and applying a 10-year valuation midpoint of 17x PE, a rough valuation comes to ~$190B. However, Qualcomm's biggest valuation overhangs remain China exposure and Apple exposure (FY24 China revenue share 46%, FY25 H1 Apple revenue share 21%).

Overall, Qualcomm's quarterly performance was mediocre due to handset volume impact, and the persistently high-growth automotive business will also decelerate sharply. With Apple's in-house modem progress accelerating (the first-gen C1 modem is adequate and more power efficient; the C2 modem is expected in the iPhone 17 series), Qualcomm may have only one year left to fill the Apple revenue gap.