Qualcomm's FY26Q2 covers January through March 2026.

Qualcomm FY26Q2 Results:

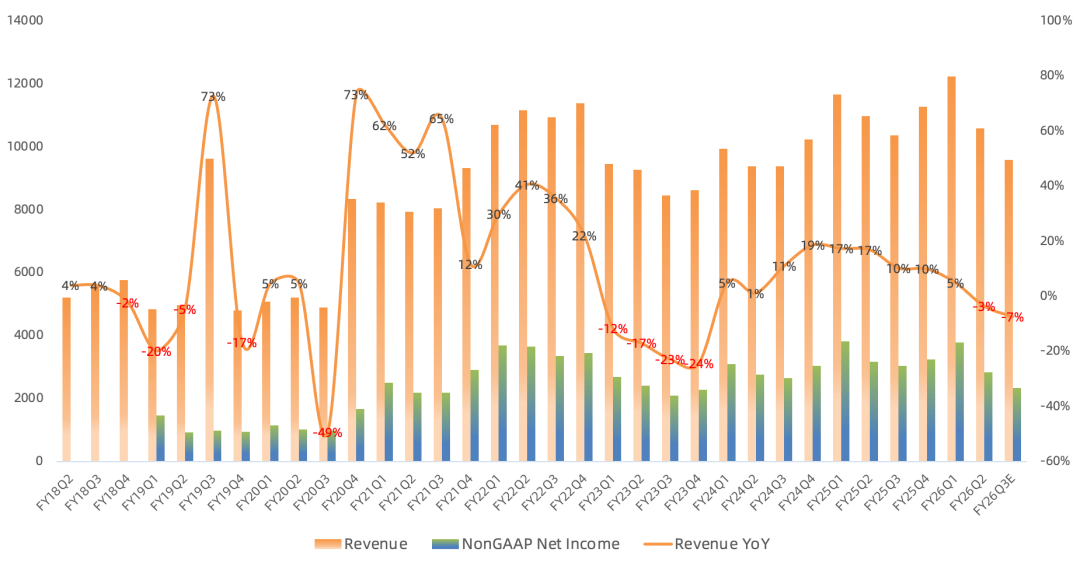

Revenue was $10.6B, down 4% year over year and 14% sequentially.

GAAP gross margin was 53.8%, down 1.2 percentage points year over year and 0.8 points sequentially.

GAAP net income reached $7.37B, driven primarily by a $5.1B tax benefit and therefore offering little insight into underlying performance. Qualcomm's previous quarterly net-income record was $3.7B in FY22Q3.

Non-GAAP net income was $2.84B, down 11% year over year and 25% sequentially. The record was $3.8B in FY25Q2.

Qualcomm expects FY26Q3 revenue of $9.2B-$10.0B, implying an 8% year-over-year decline at the midpoint. Non-GAAP net income is guided to $2.23B-$2.44B, down 23% at the midpoint. This would mark the first three-quarter streak of year-over-year declines since FY23Q4.

Qualcomm paid $950M in dividends and repurchased $2.8B of stock this quarter.

Business Segments:

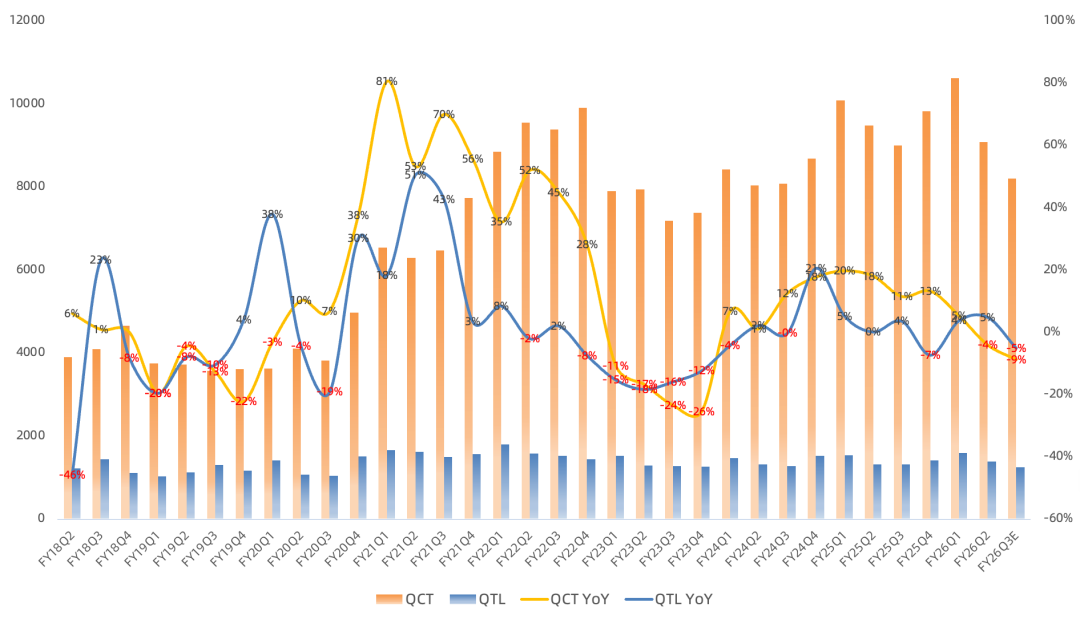

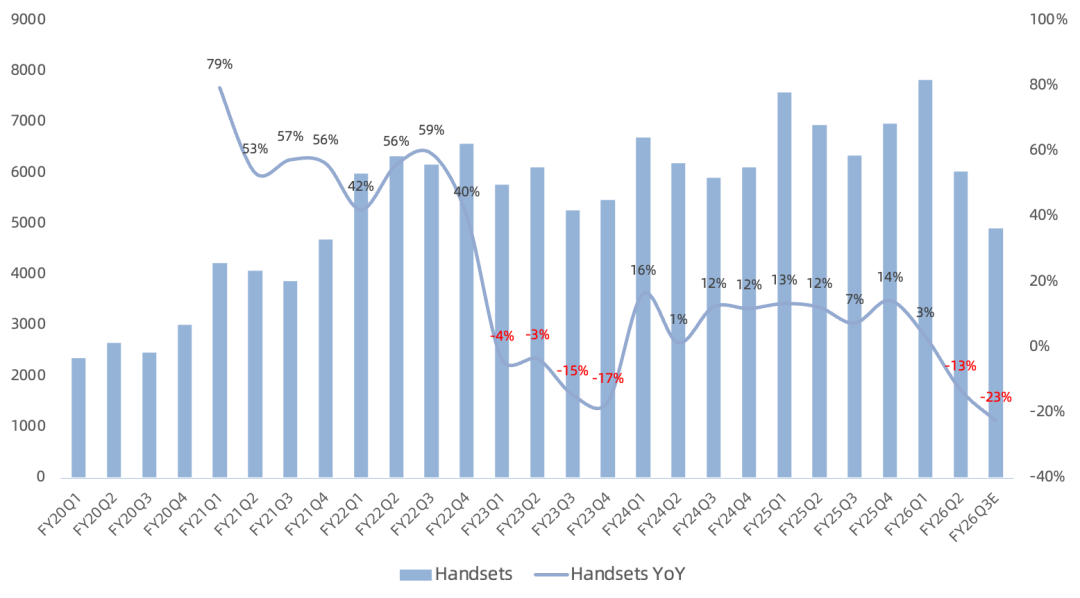

Handset revenue reached $6.02B, down 13% year over year and representing 57% of total revenue. Qualcomm's modem share in new iPhones is expected to fall to 20% in September 2026, limiting growth in Apple-related revenue, and then to zero in September 2027. Licensing revenue from Apple should still remain near a $2B annual run rate. Handset-chip shipments were materially below consumer sell-through this quarter, but channel inventory digestion should end soon. Revenue from Chinese Android customers is expected to bottom in FY26Q3, corresponding to calendar Q2 2026, and return to sequential growth in subsequent quarters.

Handset weakness is concentrated in the low and mid tiers.

Premium-tier demand is stronger. Qualcomm plans to introduce its first 6G chip in 2028, followed by the commercial launch of 6G in 2029.

Management sees new memory suppliers entering the market and building capacity, but believes it is still too early to forecast the memory environment in 2027.

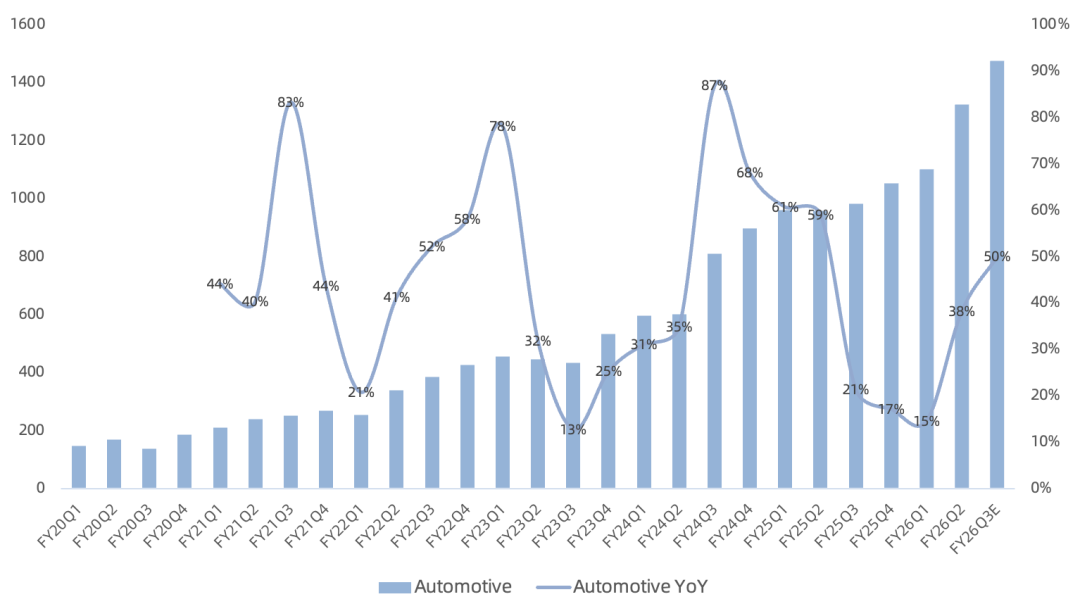

Automotive revenue reached $1.33B, up 38% year over year as growth began to reaccelerate, and represented 12% of total revenue. The business exceeded a $5B annualized revenue run rate this quarter and is expected to surpass $6B by the end of FY26. More than one million vehicles now run ADAS or automated-driving workloads on Snapdragon Ride processors. Commercial shipments of Qualcomm's automated-driving stack with BMW are scheduled to begin by the end of FY26. Automotive margins are in line with the company average.

IoT revenue reached $1.73B, up 9% year over year and representing 16% of total revenue.

In data centers, the Alphawave acquisition has added substantial custom-ASIC capability to Qualcomm's established connectivity expertise.

HUMAIN, Qualcomm's only publicly announced data center customer last quarter, has already begun receiving shipments. In addition to Oryon, which uses the Arm architecture, Qualcomm has now added RISC-V CPUs to its roadmap. The future AI250 accelerator will use a new memory architecture, with further roadmap detail due at Investor Day. Management maintained its outlook for data center revenue to begin ramping in FY27, starting in calendar Q4 2026, with the potential to become a multibillion-dollar opportunity within several years.

Qualcomm said the Alphawave integration is progressing well and that it is pursuing multiple opportunities with hyperscalers, cloud service providers, sovereign AI projects, and other global partners. The company has also entered custom silicon and is preparing for volume production with a leading hyperscaler, with initial shipments expected to begin in calendar Q4 2026. Further details are due at the June 24, 2026 Investor Day.

For the next quarter, Qualcomm expects handset revenue of $4.9B, down 23% year over year; automotive revenue of $1.5B, up 50%; and IoT revenue of about $1.8B, up at a high-single-digit rate.

Revisiting the Previous View:

Overall, every Qualcomm business is either facing or approaching a growth ceiling, making AI a badly needed new growth engine. Geopolitical exposure adds another concern: mainland China represented 46% of FY25 revenue, versus just 24% from the United States and 21% from South Korea.

Qualcomm was already struggling to find growth when the severe memory supply-demand imbalance dealt another blow to its core handset business. Combined with the loss of all new-iPhone modem share in 2027, this made Qualcomm the worst performer in the Philadelphia Semiconductor Index through mid-April 2026.

Sentiment turned as investors began aggressively pricing the server-CPU theme following AMD's Q1 results. Ming-Chi Kuo then mentioned Qualcomm in connection with an OpenAI phone, and management used this earnings report to give an optimistic outlook for server CPUs and ASICs. With Qualcomm still trading at a discount to other Philadelphia Semiconductor Index constituents, investors are now looking to the June Investor Day for further evidence of its AI transition.

For valuation, Qualcomm's trailing-twelve-month run rate can serve as a normalized handset-market scenario: $44.5B of annualized revenue and $12.9B of annualized non-GAAP net income. Excluding Apple-related revenue would reduce net income to about $10B, putting the current market capitalization at roughly 23 times earnings. The data center opportunity could add several billion dollars of revenue over the years following FY27, and Qualcomm's CPU design capability is no weaker than that of Intel or AMD, whose server-CPU prospects have attracted far more investor enthusiasm.