Qualcomm FY24Q4 corresponds to calendar July/August/September 2024.

Qualcomm FY24Q4 Earnings:

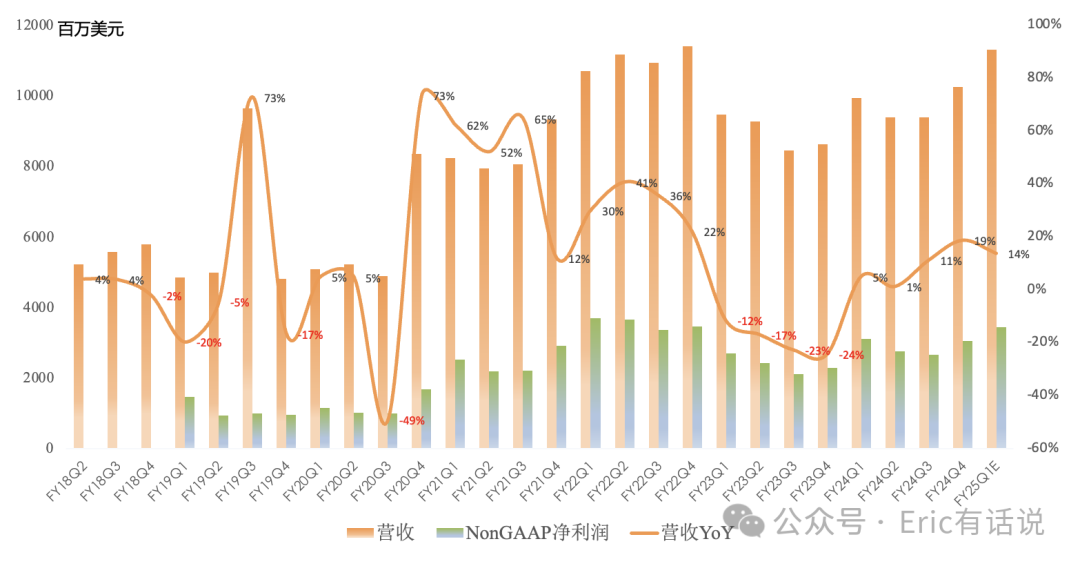

Revenue $10.244B, up 19% year over year, up 10% sequentially (revenue peak was FY22Q4 at $11.396B).

GAAP gross margin 56.4%, up 1.5 percentage points year over year, up 0.8 percentage points sequentially.

GAAP net income $2.92B, up 96% year over year, up 37% sequentially (net income peak was FY22Q3 at $3.73B).

Non-GAAP net income $3.036B, up 33% year over year, fourth consecutive quarter of double-digit growth, up 15% sequentially (net income peak was FY22Q1 at $3.686B).

Expect FY25 Q1 (year-end peak season: iPhone 16 series + Snapdragon 8 Elite) revenue $10.5B-$11.3B, up 6%-14% year over year; GAAP net income midpoint $2.811B, up 2% year over year; Non-GAAP net income midpoint $3.331B, up 7% year over year.

This quarter paid $947M in dividends, repurchased $1.3B; announced additional $15B repurchase program, previously $1B remaining authorization.

This fiscal year China revenue share 46%, US 25%, Korea 20%.

Business Segments:

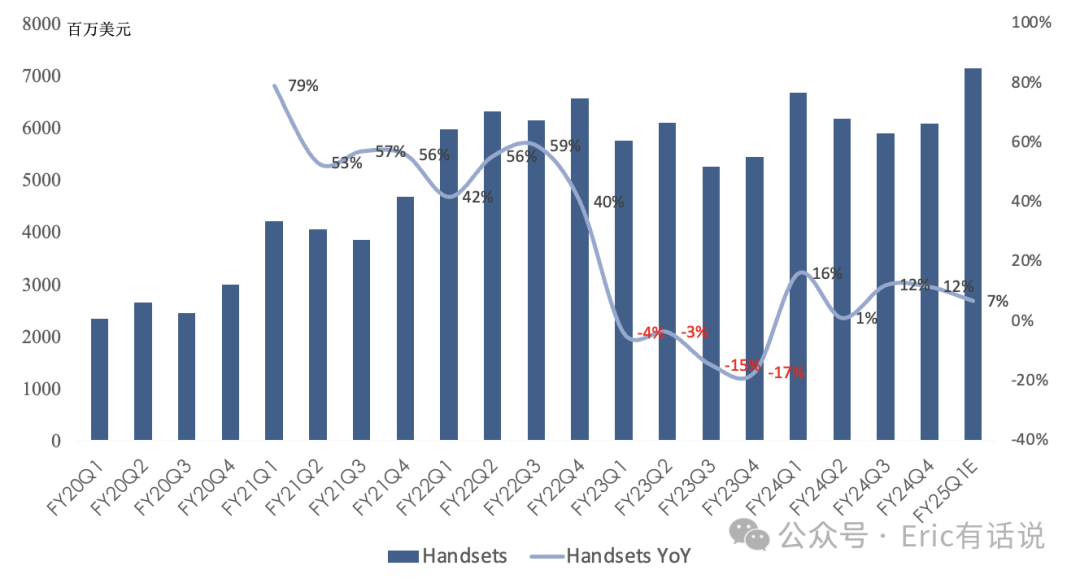

Handset revenue $6.096B, up 12% year over year, 60% of revenue; expect 2024 global handset unit growth low-to-mid single digits (raised); this fiscal year handset revenue up 10% year over year, Android revenue up 20%+ year over year, implying Apple revenue barely grew.

This fiscal year Android flagship chip revenue is 5x competitor's; Snapdragon 8 Elite uses custom non-Arm reference CPU and bundles modem/RF products, both lifting ASP; expect Apple modem share to decline to 20% by 2026 (unchanged).

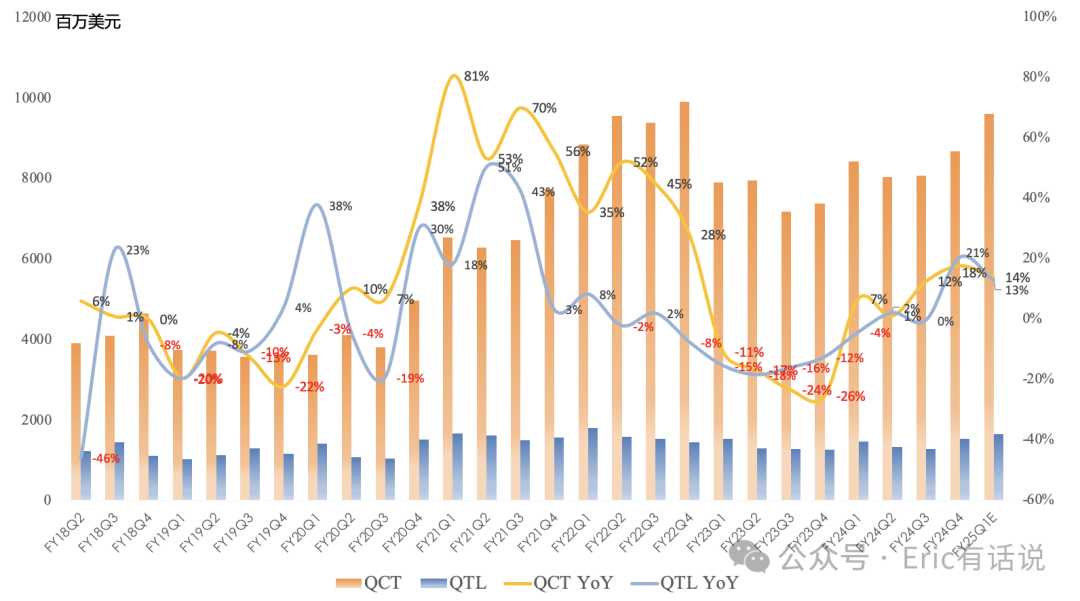

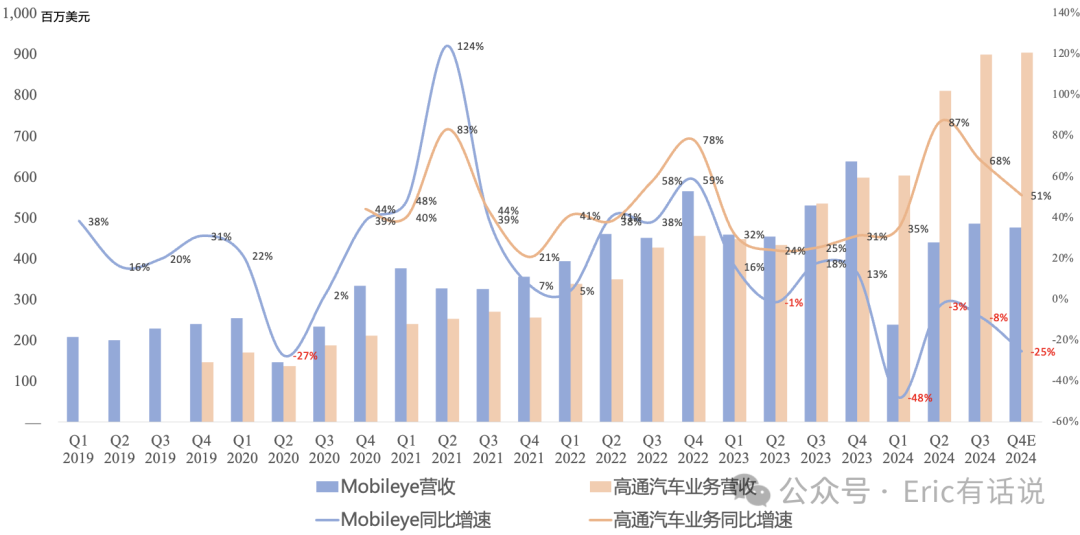

Automotive revenue $899M, up 68% year over year, 16th consecutive quarter of double-digit year-over-year growth, 5th consecutive quarterly record, 9% of revenue; company's automotive business defies weak broader auto semiconductor environment, mainly because products are more deeply tied to new vehicle platforms; Li Auto and Mercedes new models to feature latest Snapdragon Elite automotive platform; guidance update Nov 19.

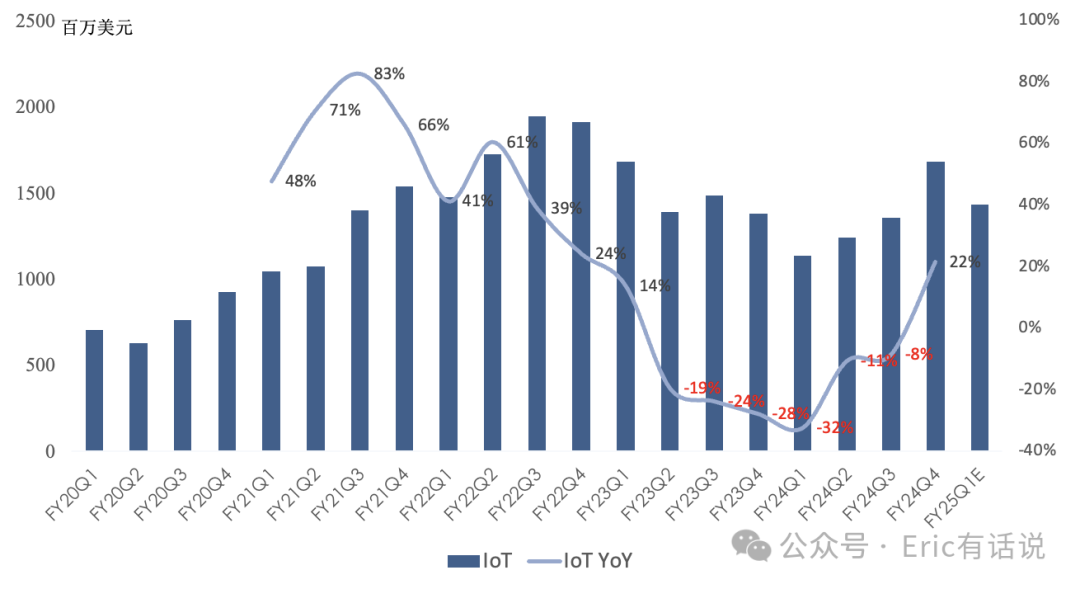

IoT revenue $1.683B, up 22% year over year, ending 6 consecutive quarters of year-over-year decline, 16% of revenue; IoT consumer, networking, industrial demand recovering; launched Qualcomm IQ series for industrial edge compute, up to 100 TOPS; Meta Quest 3S powered by Snapdragon XR2 Gen 2; Ray-Ban Meta glasses powered by Snapdragon AR Gen 1.

Expect next quarter handset revenue up mid-single digits year over year; China OEM handset revenue up 40%+ sequentially (implying Apple and Samsung down); IoT up 20%+ year over year driven by consumer, networking, industrial; automotive up 50% year over year, flat sequentially.

Overall, Qualcomm's core handset and automotive businesses beat expectations this quarter; $15B buyback adds some confidence; but next quarter core handset guidance slightly soft, especially Apple; as for the much-anticipated Arm PC, still a long shot (actual performance weak, pricing high); next year Xiaomi's custom silicon also a risk.

FY24 actual net income was $10.1B, non-GAAP net income was $11.5B. Combining the historical profit peak with a long-term valuation anchor of 20x PE yields a rough valuation range of $230B-$280B. Qualcomm's valuation has always been constrained by uncertainties such as China exposure and Apple exposure. (FY24 China revenue share was 46%, Apple revenue share was nearly 25%.)