Arm's FY26Q4 covers January through March 2026.

Arm FY26Q4 Results:

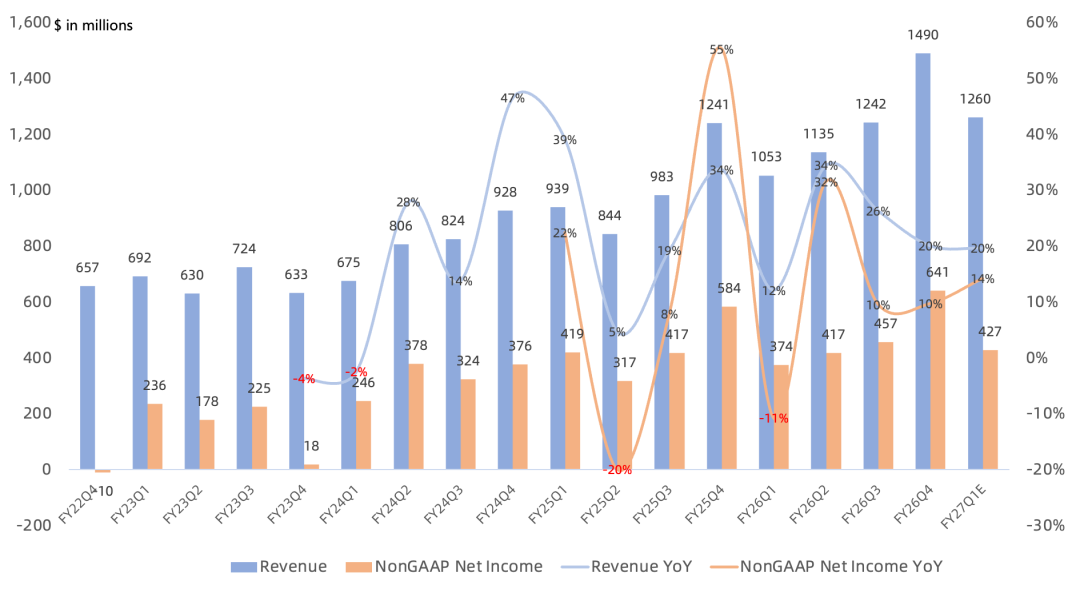

Revenue reached $1.49B, up 20% year over year and above the prior guidance of $1.47B.

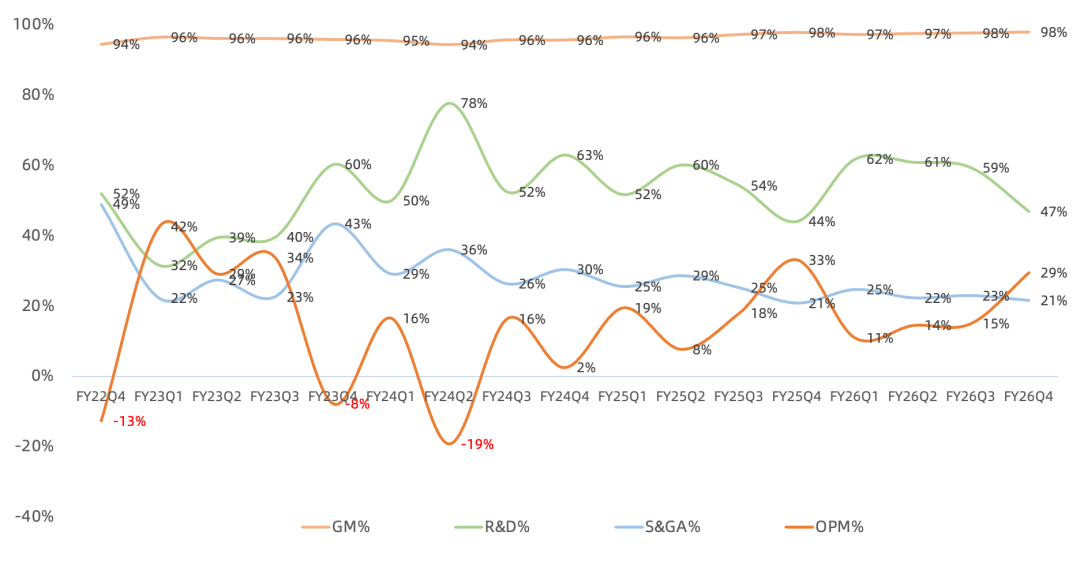

GAAP gross margin was 97.9%, up 0.1 percentage points year over year and still among the highest of any public company globally.

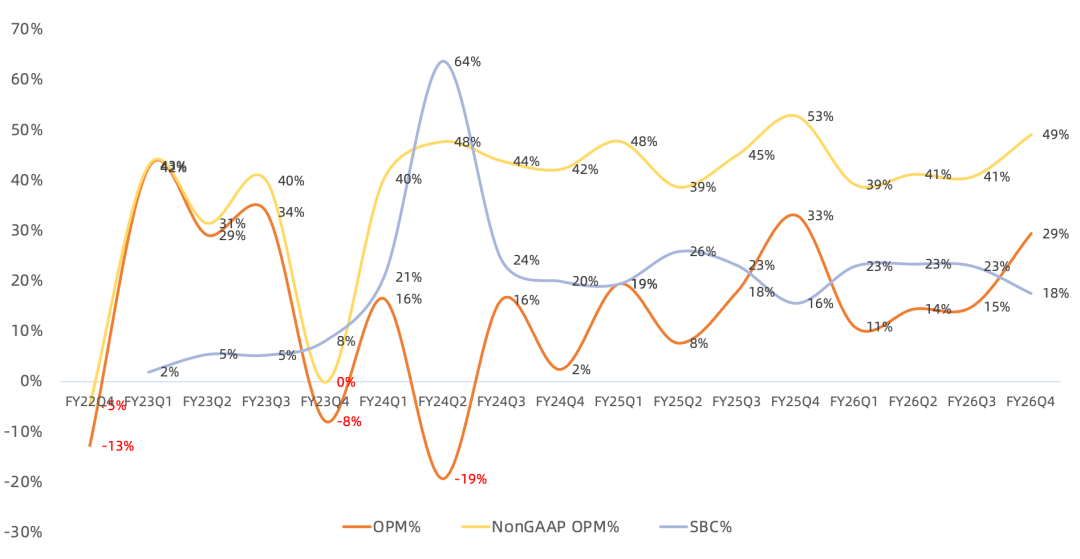

GAAP operating income reached $438M, up 7% year over year, while GAAP operating margin fell 4 percentage points to 29%.

Non-GAAP operating income reached $731M, up 12% year over year, while non-GAAP operating margin fell 4 percentage points to 49%.

GAAP net income reached $313M, up 49% year over year, and GAAP net margin improved 4 percentage points to 21%.

Non-GAAP net income reached $641M, up 10% year over year, while non-GAAP net margin fell 4 percentage points to 41%.

Despite a gross margin close to 100%, Arm's GAAP operating profit remains modest, and the company frequently posted operating losses in earlier periods. The main reason is elevated R&D spending, which represented 47% of revenue this quarter and grew 28% year over year, faster than revenue. Sales, general, and administrative expense was relatively stable at 21% of revenue. Whether the R&D ratio can decline will therefore determine whether operating margin can expand. Arm's move into designing its own CPUs will raise R&D spending further, fueling investor concern about long-term profitability.

Business Segments:

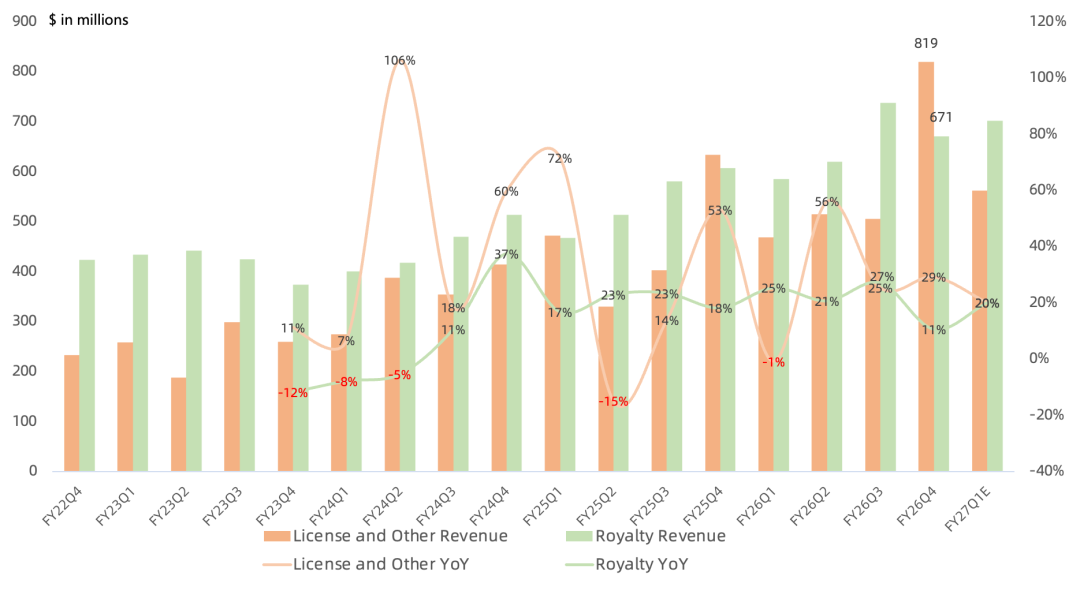

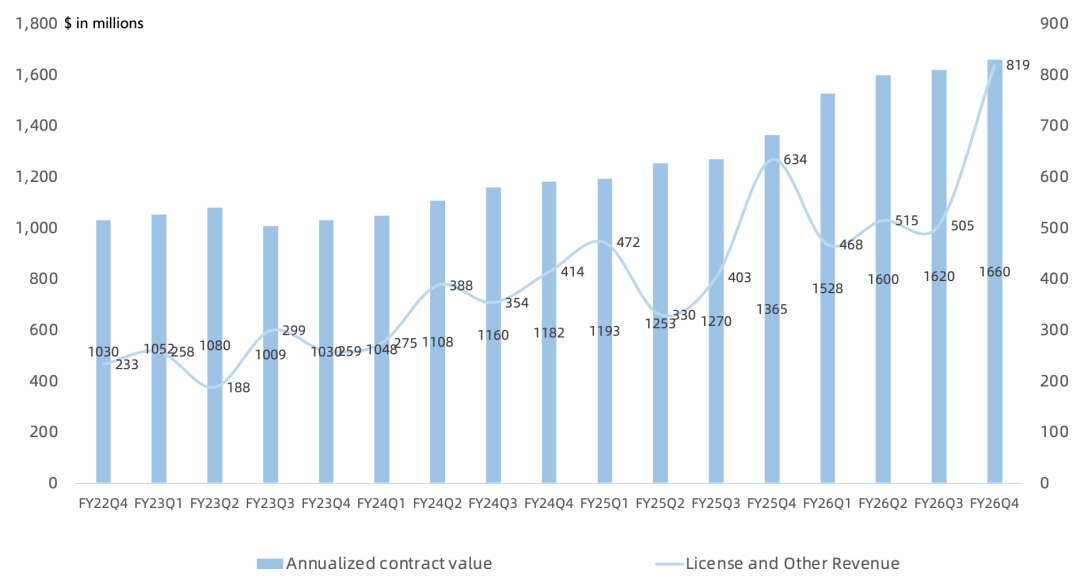

License and Other revenue reached $819M, up 29% year over year.

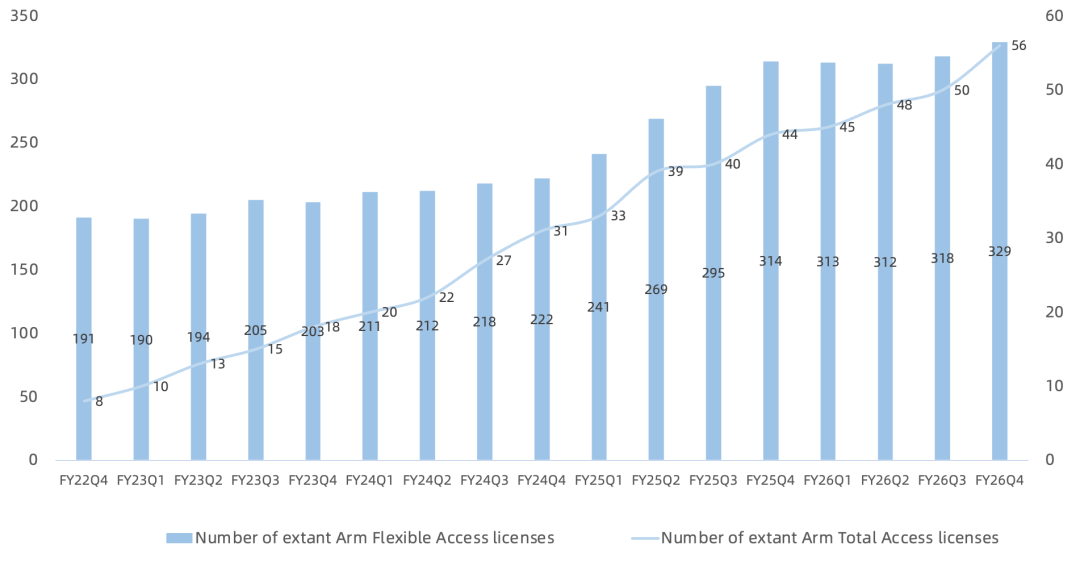

Arm Total Access, or ATA, had 56 cumulative agreements at quarter-end, up six sequentially. ATA annual fees rise 7% each year and contracts renew every three years. Arm Flexible Access, or AFA, reached 329 customers, up 11 sequentially.

License revenue benefited from one new handset customer and one new data center networking customer, bringing cumulative CSS licenses to 23. Arm also signed a long-term strategic partnership with the Indonesian government. Management expects long-term License revenue growth of at least 10%.

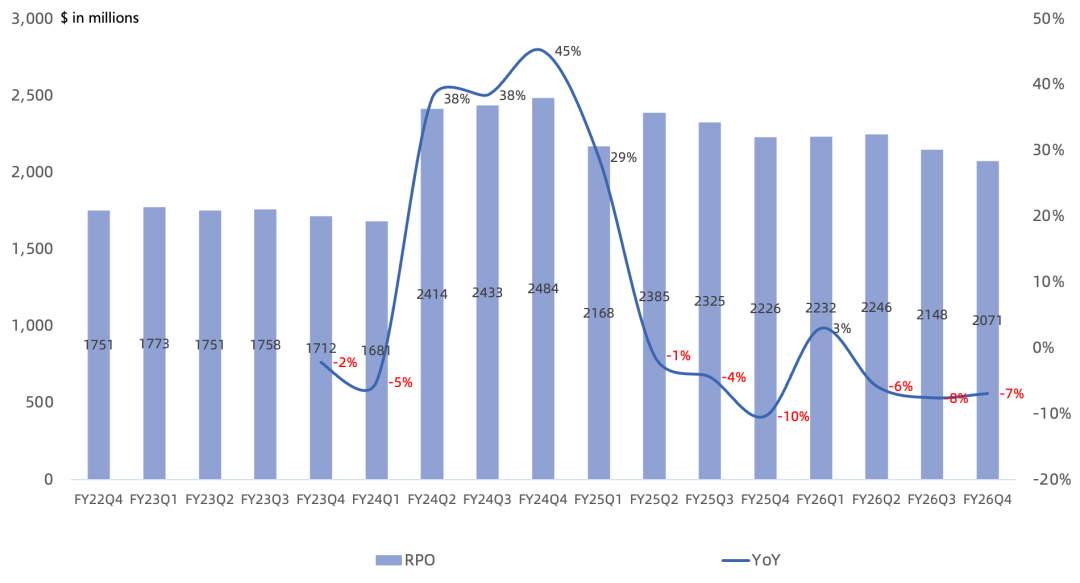

Annualized contract value reached $1.66B, up 22% year over year. Remaining performance obligations fell 7% to $2.07B, marking a third consecutive quarterly decline.

Royalty revenue reached $671M, up 11% year over year.

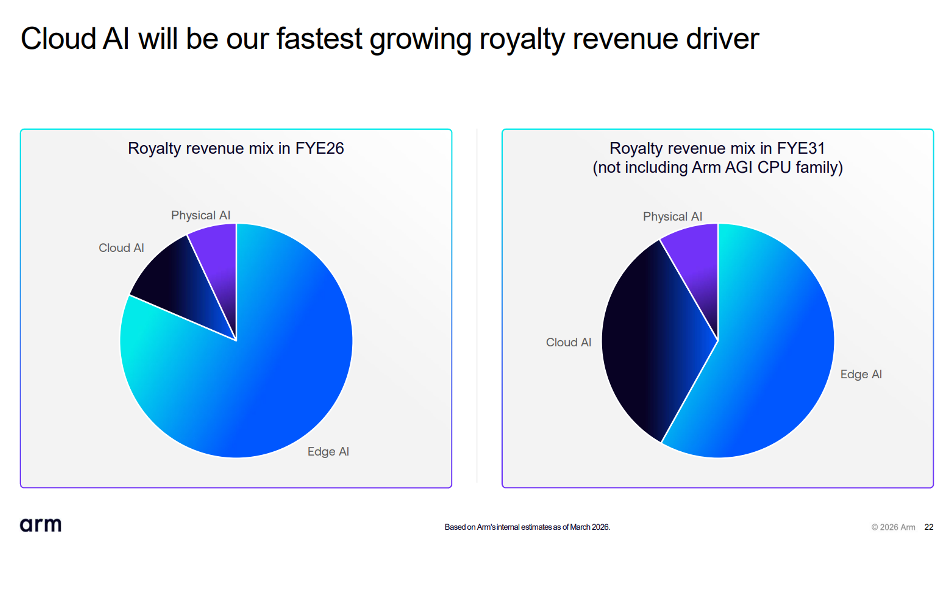

Cloud AI was the largest contributor to Royalty growth this quarter. Data center Royalty revenue doubled year over year and is expected to double again in FY27, driven by faster deployment of Arm-based server chips at major hyperscalers and rising adoption of data center networking chips, particularly DPUs and SmartNICs, where Arm holds close to 100% market share.

In edge AI, handset revenue continued to grow despite weak end-market demand, driven primarily by CSS and Armv9. ADAS and autonomous-driving systems also delivered growth.

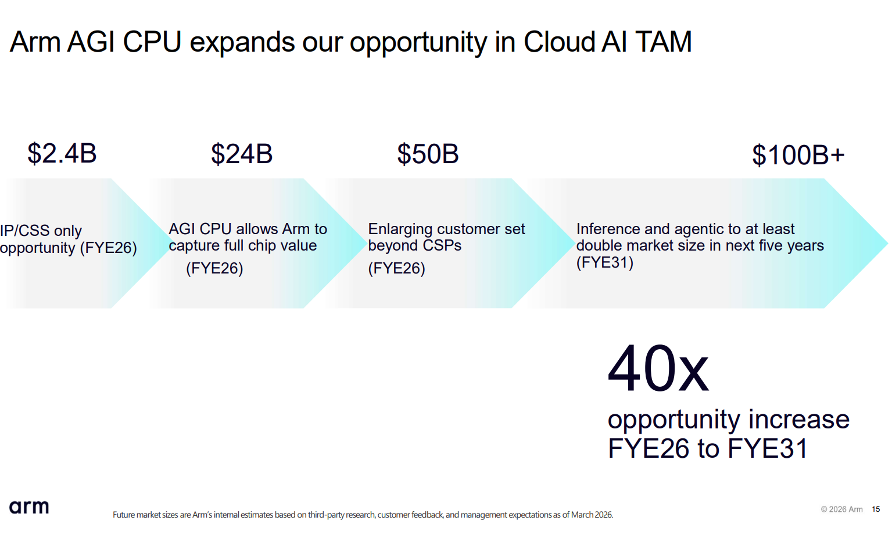

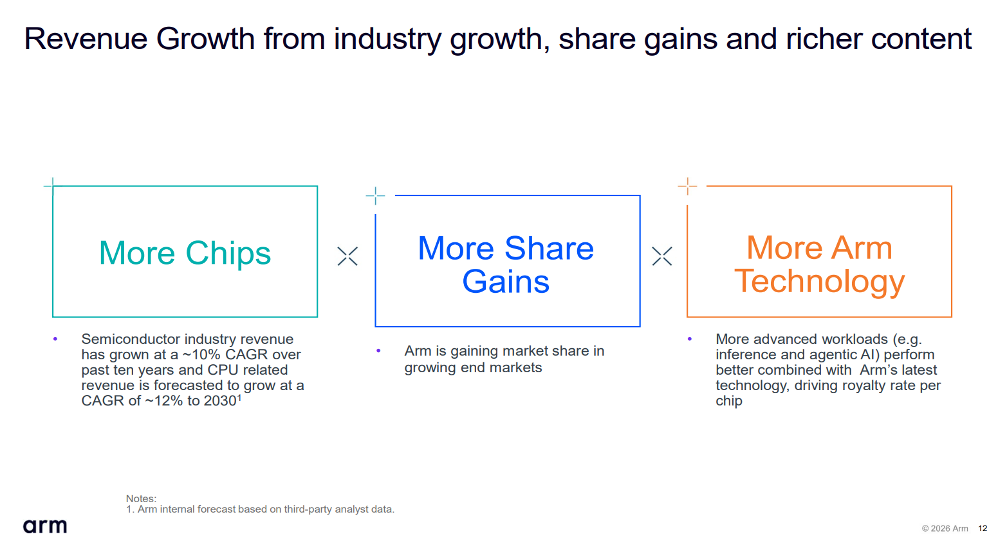

As agentic AI scales, data centers will require more than four times today's CPU capacity, creating a data center CPU opportunity exceeding $100B by 2030. Compared with x86 platforms, Arm's AGI CPU is expected to deliver more than twice the per-rack performance and could reduce AI data center capital expenditure by as much as $10B per gigawatt. Meta is among the first AGI CPU customers. NVIDIA, Amazon, and Google already use Arm-based CPUs as head nodes in accelerator-based systems, while Cerebras, OpenAI, Rebellions, and Positron are adopting Arm AGI CPUs for the same role. Arm currently holds roughly 50% share among leading hyperscalers.

First-generation CSS carries roughly twice the Royalty rate of Armv9, and the second generation is priced higher still. Armv8 historically earned about 2.5%-3% of chip ASP, Armv9 about 5%, first-generation CSS roughly 10%, and second-generation CSS more than 10%. CSS contributed a low-teens percentage of Royalty revenue in FY26 and could exceed 50% over the next several years.

Arm FY26Q4 Earnings Call Highlights:

Arm expects FY27Q1 revenue of $1.26B, up 20% year over year, and non-GAAP net income of $427M, up 14%.

Management expects both Royalty and License revenue to grow 20% year over year in FY27Q1. AGI CPU revenue should reach roughly $90M in FY27Q4 and about $910M in FY28. Handset Royalty growth is expected to slow against a high prior-year comparison as smartphone shipments begin to decline, with weakness concentrated in the low end while the high end remains resilient. For FY27, both Royalty and License revenue are expected to grow about 20%. License revenue should remain back-end weighted, as in the past three years, with roughly 40% in the first half and 60% in the second. Operating expenses are expected to increase by a few percentage points sequentially each quarter, with expense growth falling below revenue growth by year-end.

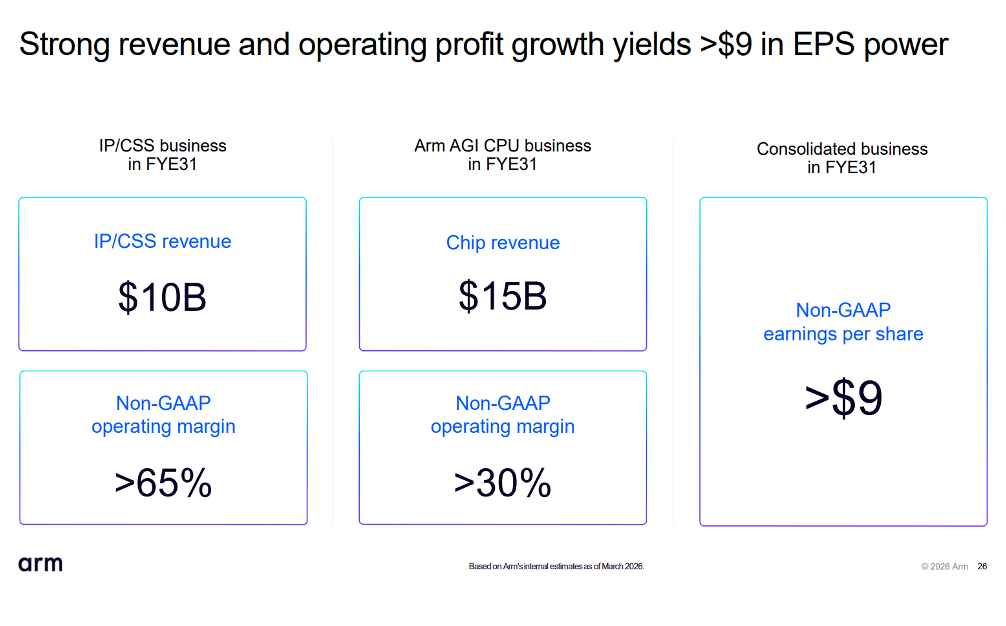

At its Arm Everywhere AGI CPU event in March, the company projected $15B of AGI CPU revenue and $10B of IP revenue by FY31, for $25B in total revenue and more than $9 of EPS. First-generation AGI CPU gross margin is expected to exceed 30%. By FY31, the IP business could reach an operating or EBITDA margin of about 65%, while the chip business could reach roughly 35%.

Arm now sees more than $2B of aggregate customer demand for CPUs across FY27 and FY28, more than double the level disclosed at launch, but supply capacity is constrained. Management expects to provide firm supply guidance in FY27Q3 and says the company remains on track toward its FY31 CPU revenue target of $15B.

Related-party revenue, including Arm China and SoftBank, reached $411M, up 85% year over year and representing about 28% of total revenue. SoftBank accounted for roughly $200M of related-party revenue through licenses and design services, with the design-services component carrying a lower margin.

Arm's strategy is to drive Royalty growth through IP and CSS while adding CPU chips as a new growth vector. SAP will migrate its core database and enterprise-application workloads to Arm, beginning with AWS Graviton and later expanding to Arm AGI CPUs. This represents a major strategic shift.

Arm's Core Growth Formula

The doubling of data center Royalty revenue and its rising share of the business had already persuaded investors that Arm could participate in the AI boom. The March announcement that Arm would build CPUs itself further aligned the company with the market's enthusiasm for CPU exposure, sending the stock sharply higher and effectively pricing in management's FY31 EPS target of $9.

I continue to believe Arm can capture the largest share of the data center CPU market and keep taking share from Intel and AMD. Even so, its current market capitalization already values the company at 23 times management's FY31 EPS target of $9.